What is an income statement

When entrepreneurs receive income, they must be declared for further taxation. If an individual entrepreneur is in a special regime and pays a single tax to the budget, there is no obligation to submit form 3-NDFL. But when using the general taxation regime, as well as in some other cases, which will be discussed in more detail below, it is required to file a declaration of income of individuals. In 2022, it is necessary to report for 2017.

When submitting 3-NDFL to the tax authorities, data on the taxable base is indicated in terms of various income received and the amount of accrued tax. If deductions are claimed at the same time, additional information is provided that is required to process an income tax refund. Thus, in some cases filing a return is a taxpayer's responsibility, while in others it is a right.

When to submit the 3-NDFL declaration

The legislation of the Russian Federation clearly states situations when citizens who are not registered as individual entrepreneurs must submit a 3-NDFL declaration. An obligation arises when a person receives the following types of profit (Tax Code of the Russian Federation, Article 28):

- From individuals and companies not classified as tax agents. Cooperation is carried out on the basis of formalized labor and civil agreements, including profits from rental agreements or employment contracts.

- Sale of property assets (real estate and rights).

- Income from sources outside the Russian Federation.

- Winnings in programs of lottery and gambling organizers.

- A prize received by heirs (successors of rights) from the creators of literary, scientific or other works, including inventions, industrial designs and models.

- Gifts in monetary or property terms.

- Funds from real estate and securities used to replenish the capital of non-profit companies.

This category also includes other types of profit from which tax was not withheld with the involvement of tax agents (except for profit, information about which was not transmitted by the mentioned persons taking into account the Tax Code of the Russian Federation).

What is different about the 2022 income tax return?

The current income declaration form was approved by tax authorities in Order No. ММВ-7-11/671 dated December 24, 2014. The document was repeatedly edited due to amendments to the tax legislation of the Russian Federation, but continues to be used in 2022. The same Order contains the rules for generating reports for all sections. What exactly has been updated in 3-NDFL?

First of all, the adjustments made to the Tax Code of the Russian Federation by Laws No. 317-FZ of November 23, 2015, No. 327-FZ of November 28, 2015, No. 32-FZ of February 15, 2016 were taken into account. In connection with this, taxation standards have changed those citizens who receive profit in the form of dividends from foreign controlled companies (clause 66 of article 217 of the Tax Code). In addition, changes in deductions for parents of disabled children have been taken into account - with an increase from 3,000 rubles. up to 6000 rub. and 12,000 rub. (subparagraph 4, paragraph 1, stat. 218); to increase the maximum limit of 350,000 rubles. instead of 280,000 rubles. when providing employees with standard child deductions (Article 218). And finally, the specifics of taxation of transactions on individual investment accounts have been clarified (stat. 214.9, 219.1).

Subtleties of filing a declaration

The Tax Code of the Russian Federation (Article 80) states that a declaration can be submitted by the payer to the Federal Tax Service in three ways:

- On your own or with the assistance of a representative.

- By mail (in this case the contents of the letter are described).

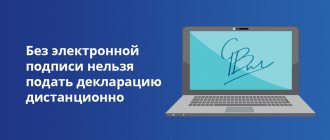

- In the form of electronic paper through the personal account of the tax payer (all manipulations are carried out through nalog.ru).

The option that takes the most time is to transfer 3-NDFL yourself or by a representative. To save time, it is recommended to choose the option of transferring electronically through your personal account. When choosing this method, there is no need to visit the Federal Tax Service, because the exchange file is generated automatically based on the format approved by the tax authority.

As noted, submitting a declaration electronically is only possible if you have an electronic signature (issued by a special center). When submitting a declaration through your personal account on the Federal Tax Service website, you are required to come to the tax authority and take a registration card. The latter contains the account information for logging into your personal account. This option is suitable for people who plan to submit their declaration regularly.

If the goal is to submit the declaration only once, it is better to use the mail. For reliability, it is recommended to use a valuable parcel post with a mandatory list of attachments and information about delivery. The date of transmission is the day indicated on the postal plug. This means that sending a declaration is possible even on the last day of the deadline for submitting 3-NDFL.

Who must file an income tax return?

The declaration of income of individuals is submitted by those taxpayers who are indicated in the stat. 227, 227.1, 228 (clause 1) Tax Code. First of all, these are entrepreneurs working on the general taxation system; these are also persons who have sold their own property. In addition, private practitioners and employees who received income as part of labor and/or civil law relationships with enterprises that are not tax agents are required to file 3-NDFL.

Who submits the 3-NDFL declaration:

- Persons registered in the general order as individual entrepreneurs and conducting activities at OSNO.

- Individual entrepreneurs under special regimes when receiving income that does not relate to imputed or simplified activities, or when the basis for using such a regime is lost.

- A number of civil servants, including employees of the Ministry of Internal Affairs (Decree No. 557 of 07/01/14, Decree No. 1574 of 12/29/14, Order No. 875 of 10/31/13). The same requirement applies to family members of civil servants.

- Foreigners operating in the Russian Federation on the basis of a patent issued in accordance with legal requirements.

- Private practitioners - notaries, lawyers, detectives, etc.

- Individuals who received income from non-tax agents (both from organizations and from other individuals). The obligation to file reports arises on the party who received the income only after notification by the employer. That is, the party that paid the income to the individual is obliged to notify in writing not only the territorial division of the Federal Tax Service, but also the citizen himself about the impossibility of withholding income tax. If a person has not received any notices, then he should not submit 3-NDFL.

- Individuals who sold property that was owned for less than 3 years. For example, it is necessary to submit a declaration of income when selling a car, apartment, house, garage, etc. But, if a citizen has owned the property for more than 3 years, there is no need to submit a declaration to the tax office.

- Individuals who received winnings from playing a lottery, casino, betting, or other risky entertainment activities.

- Individuals providing personal property for rent.

- Individuals receiving income abroad. An exception is civil servants who are residents of the Russian Federation and work abroad.

- Legal successors (heirs) of authors receiving income from such works.

- Individuals who have received property, securities and other objects as a gift from citizens who are not their relatives or individual entrepreneurs.

- Other persons in accordance with legal regulations.

Note! Employed citizens are not required to file a declaration; the employer performs these actions for them by submitting Form 2-NDFL on personnel income and deductions to the Federal Tax Service.

Citizens have the voluntary right to provide 3-NDFL in the event of a claim for social, property, professional deductions or when the employer provides standard deductions in a smaller amount than required by law (clause 2 of Article 229 of the Tax Code). In addition, if an individual has changed the status of a non-resident to a resident, filing a declaration will also help to return the income tax over-withheld by the employer. Moreover, the amount of overpayment is usually quite significant, since the rate changes from 30% to 13. This means that in order to return the difference, it is necessary to provide 3-NDFL and supporting documentation to the tax authorities (clause 1.1 of Article 231).

How to fill out and submit the 3-NDFL return to the tax office?

There are several options where you can fill out a tax return for individuals.

Firstly, this is the Taxpayer’s Personal Account (TPA). It’s not difficult to fill out, everything is step by step.

Secondly, this is the “Declaration 2021” program. You download this program from the Federal Tax Service website. It is set separately for each year.

You can submit a completed 3-NDFL declaration:

- in person at the Federal Tax Service;

- send by mail;

- send electronically via TKS;

- fill out and immediately send to LKN.

From January 1, 2022, the obligation of individuals to submit a declaration when selling real estate (residential houses, apartments, rooms, garden houses or land plots) in the amount of up to 1 million rubles, and other property (transport, garages, etc.) - up to 250 thousand rubles.

Please note that the amounts indicated correspond to the amounts of property tax deductions for personal income tax. These innovations apply to persons who sold property starting from the 2022 tax period.

Deadline for filing an income tax return

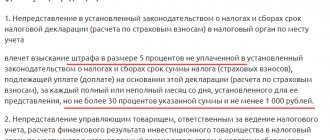

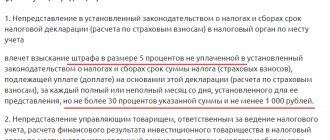

What is the deadline for filing an income tax return? To answer, let us turn to the provisions of stat. 229. It is stated here that when submitting a form by persons who are obliged to do this, the general submission deadline is set until April 30 of the calendar year following the reporting year (clause 1 of Article 229). If the activity of an individual (individual entrepreneur or private practitioner) is terminated before the end of the tax period, it is necessary to report within 5 days from the date of termination (clause 3 of Article 229). For foreigners, the period has been extended to 1 month.

Accordingly, the income declaration for 2022 is submitted by 04/30/19, for 2022 - by 05/03/18, taking into account the postponement of holidays and weekends. For taxpayers who are not required, but wish to submit f. 3-NDFL, there are no strict restrictions on the period. Filing a declaration at the individual’s residence address is possible at any time after the end of the tax period, but no later than 3 years (clause 7 of Article 78 of the Tax Code). For example, in 2022 you need to report for 2015, 2016 and 2022; and in 2022 – for 2014, 2015 and 2016. Next, we’ll look at how to fill out an income tax return based on current regulatory requirements.

How to fill out an income tax return correctly

There are several ways to submit a declaration. You can personally visit the Federal Tax Service Inspectorate or send the documentation by postal certified letter with the obligatory attachment of an inventory. Or submit the data through an official representative with preliminary notarization of the latter’s authority. Finally, you can take advantage of the Internet and submit the form through TKS.

In order to correctly fill out the income tax return for 2022 or for 2022, you first need to download the current form - standard form (KND 1151020) and a sample form is presented at the end of our article. The document, as well as the rules for entering data and the format for submitting the report in electronic form, were approved by Order No. ММВ-7-11 / [email protected] dated December 24, 2014. Let’s look at the basic rules for filling out the declaration.

Requirements for drawing up 3-NDFL:

- The document can be filled out on a computer or by hand. You can use software that provides printing of two-dimensional codes. The ink used is black or blue.

- Deformation of form sheets and presence of corrections is prohibited.

- The data to be included in the report is taken from income certificates issued by tax agents, payment and settlement documents available to the taxpayer, etc.

- Each indicator has a separate field/line.

- Monetary values are entered in rubles and kopecks, except for amounts converted at the currency exchange rate.

- Personal income tax values are subject to rounding according to the rules of mathematics - kopecks over 50 are rounded up to a whole ruble, less are discarded.

- Income and expenses subject to conversion into Russian rubles are calculated at the official exchange rate on the actual date of income or expense.

- All indicators are entered from left to right.

- If there is no indicator, a dash is indicated.

- When submitting supporting documents to the Federal Tax Service, it is recommended to additionally draw up a register of submitted forms - in writing and in free form.

- If the declaration is submitted by an official representative of the taxpayer, you should attach a copy of a document confirming his authority, for example, a notarized power of attorney.