Inventory procedure

In order to carry out an inventory, the director of the company issues an appropriate order. It states

- requirement for this event,

- persons who must take part in it,

- the tasks that are assigned to them,

- employees responsible for the execution of superior orders.

The purpose of the inventory is to monitor the presence and safety of inventory, search and identify property subject to write-off (due to obsolescence, irreparable breakdowns, etc.), as well as assess the conditions of storage and maintenance of the organization’s property.

During inventory activities, all property is checked, counted and verified with documentation, primarily related to accounting. Based on the results of the event, special reporting acts are drawn up, including an inventory list.

If it is not possible to carry out an inventory at one time, inventory labels are generated at intermediate intervals.

They contain preliminary information about the results of the inspection, which will subsequently be clarified. Before the next stage of the inventory, the room in which the property being inspected is stored is sealed.

In what cases is property inspection carried out?

Carrying out inventory activities is necessary in the following cases:

- when selling property, transferring it for rent or buying it out;

- when changing materially responsible employees;

- in case of theft, abuse of official position (for the purpose of profit),

- damage and damage to property;

- before preparing annual financial statements;

- as part of the reorganization or liquidation of the company;

- after various kinds of unforeseen situations and natural disasters.

Who conducts property inspections

A special commission is appointed to carry out the inventory. It includes employees of the enterprise from different structural divisions, including a representative of the management level, a specialist from the accounting department, a warehouse employee, etc. If necessary, people from what is called “outside” are also included in the commission, for example, experts from specialized auditing companies .

Among the commission there is a chairman and ordinary members. The chairman bears maximum responsibility for conducting an inspection of the property and preparing all accompanying papers.

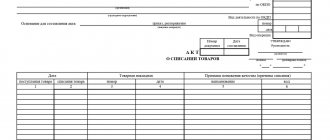

INV-1 sample filling

On the 1st page of the OS inventory list the following information is reflected:

Information about the company (name; structural unit in which the inventory is carried out; OKPO, main OKVED). Inventory information (details of the inventory order, inventory deadlines). Information about operating systems undergoing inventory

It should be noted that the inventory can be carried out both in relation to the company’s own property and in relation to fixed assets received by the company for rent. In this case, a separate inventory of such property is drawn up, one copy of which is transferred to the lessor, and information about it is indicated in the inventory. A receipt from the employee responsible for the property, which confirms that all the property assigned to him has been accounted for.

On the 2nd page a direct inventory of the property is made. The name, characteristics and numbers of the OS are indicated. The actual quantity and cost of fixed assets and according to accounting data are reflected.

On page 3, the inventory list of fixed assets is signed by all members of the commission and the employee responsible for their safety

Please note that the inventory must be carried out in the presence of all members of the commission and the employee who is financially responsible for this property. Violation of this rule entails the recognition of the inventory results as illegal

If discrepancies are identified between the actual state of the fixed assets and accounting data (shortages, surpluses), matching statements are compiled (official form INV-18).

More information about the inventory procedure, the timing of its implementation; cases where it is mandatory; regulatory framework and other issues, see the following video.

General Inventory Label Information

- The INV-2 form is unified. And although today unified document standards have been canceled, most organizations still prefer to use previously mandatory forms. This is due to the fact that such forms contain all the necessary data, they are convenient and easy to fill out. In addition, they can be modified as necessary by removing or adding the necessary lines.

- Information in the document can be entered electronically or by hand (if a printed version is used). There are no clear instructions for completing the form. The only thing that needs to be taken into account is that it must be signed by the responsible persons (in this case, the autograph of one member of the commission is sufficient) and stamped - if the use of stamps for endorsing internal papers is enshrined in the local documents of the company.

- An inventory label is generated in a single original copy and kept by the responsible employee.

- If there are any errors in the label, unlike many other forms, they can be corrected - this document does not apply to strict accounting forms. To edit, you need to cross out the incorrect information and write the correct information above or next to it (when there is free space), confirming the correction with the signature of the employee who fills out the document.

Sample of filling out the INV-2 form: inventory label

First, enter the following data into the form:

- name of the company where the inventory is carried out;

- structural unit whose property is being checked (if necessary);

- on the left, in a special plate - the details of the organization (OKPO code, type of activity according to OKVED (also in the form of a numerical value));

- reference to the order or instruction of the management of the enterprise on the basis of which inspection activities are carried out;

- date of inventory (day-month-year of its beginning and end);

- inventory label number and date of its preparation.

Below is a plate in which information about inventory items, calculated and accounted for, is entered. Here it means:

- storage location (details - shelf, rack, cell number);

- name and number (by nomenclature);

- all identification characteristics: brand (model), grade (category), profile, size, etc.;

- unit of measurement (according to OKEI code - in words, in numbers);

- quantity of inventory items available.

Next, the document must be signed by one of the commission members and the financially responsible person.

On the reverse side of the form is the date when the actually available property was counted, again the number of remaining inventory items (in words) and the signature of the person who accepted them for storage.

Where is the INV-2 form used?

The organization regularly faces the need to verify the correctness of accounting of goods in warehouses; an inventory is carried out to compare actual and accounting data. As a rule, this procedure is carried out annually when summing up annual results and filling out annual financial statements, as well as as necessary (change of MOL, theft, theft at an enterprise, etc.).

During the inventory procedure, the property of the enterprise in respect of which the inspection is being organized is checked and recounted. Members of the appointed inventory commission, as they receive information, enter it into special inventories; for each type of value, their own standard forms are used. In particular, with regard to inventory items, the INV-3 inventory is filled out.

When to Apply an Inventory Label

This form is designed to record intermediate inventory results. If, due to the large number of goods and materials, the commission does not have time to complete the inspection in one day, then a separate document is drawn up that records the preliminary results - an inventory label. Form INV-2 is drawn up in this way before completing the inventory based on the results of the inventory. And the information that is reflected in the label is subsequently used to compile an inventory list of goods and materials (form INV-3 is used for this).

Who signs the inventory label?

The INV-2 form is signed by the following persons:

- Responsible member of the inventory commission, confirming the correctness of the procedure;

- The person responsible for the safety of valuables, confirming that the specified name of the goods and materials is at the storage location in full, the documentation on it has been submitted to the accounting department, and there are no unaccounted goods in the warehouse.

These signatures are placed on the front side of the INV-2 form. On the reverse side, the employee of the enterprise who accepts for safekeeping the quantity of goods and materials indicated in the label puts his signature. By putting his signature in this field, the employee agrees that he received the valuables in exactly the quantity indicated in the INV-2 form.

How to properly issue an inventory label

Requirements for the content of primary accounting documents are given in Art. 9 of the Law on Accounting No. 402-FZ dated December 6, 2011. The details given in Article 9 (name and date of the document; content and value of the fact of economic life that are reflected in the document; name of the economic entity, positions and signatures of responsible persons, etc.) must be contained in the label, if you do not draw it up according to a unified form. If you use the unified INV-2 form, then all the necessary details are contained there.

Thus, the unified form includes:

- the name of the organization, its OKPO code and the name of the structural unit being inspected;

- details of the document-basis of the inventory (number and date of the order, instruction or resolution on conducting the inventory);

- inventory start and end date;

- details of the document itself (name, date, number);

- data about the place where inventory items are stored (shelf number, cell number, etc.);

- information about inventory items (name, quantity, grade, brand, etc.);

- Full name, position, signatures of the commission member and the responsible person;

- a note from the financially responsible person regarding the acceptance for storage of inventory items that were available on the day of the inspection.

INV-2 form form

Since this form is preliminary, the requirements for its design are somewhat simpler than for the final inventory forms. Unlike other forms, it does not need to be compiled in several copies; one is enough.

The signatures of all commission members are not required. The unified form provides for the signing of this document by one of the commission members. It is also signed by the person who is responsible for the safety of valuables in the warehouse.

If the inspection lasts more than one day, the premises where inventory items are stored should be sealed when the commission leaves (clause 2.12 of the Inventory Guidelines). According to the instructions given in Resolution No. 98, the inventory label remains in the storage location of the inspected inventory items.

The inventory label (INV-2 form) is recommended for use by Decree of the State Statistics Committee of August 18, 1998 No. 88. The form was a mandatory unified form until 2013. Since 2013, the given sample document can be used when carrying out inventory activities in its original form or a new form can be developed based on it.

What is document INV-2

Form INV-2, introduced into business circulation by the State Statistics Committee in the resolution “On approval of forms for recording inventory results” dated August 18, 1998 No. 88, is used for preliminary accounting of raw materials, products, goods and other inventory items (material assets) in warehouses when conducting an inventory at the enterprise in cases where:

- the commission that conducts the inventory takes more than 1 day to calculate inventory items and record information about them in a special inventory (another unified form, designated INV-3);

- the enterprise is quite large-scale, and for more accurate accounting of inventory items, the use of auxiliary primary forms is required, one of which is the INV-2 document.

The INV-2 form is fully consistent with its second name, since a label is usually understood as a form that complements another document that is considered the main one. In this case, it complements the main inventory list. Please note that it cannot be used instead of the INV-3 form, since these documents are completely different in structure.

Read about the rules for filling out INV-3 in the article “Unified form No. INV-3 - form and sample” .

You can download the form for the main inventory of goods and materials according to the INV-3 form for free by clicking on the picture below.

The auxiliary function of the inventory label is expressed in the fact that, in particular, it records:

- location of goods and materials;

- coordinates of cells and racks in which inventory items are stored;

- main characteristics of inventory items, for example, brand and grade;

- the number of inventory items of a certain type located in a specific location.

Read about the document reflecting the results of the inventory of fixed assets in the material “Unified Form No. INV-1 - Form and Sample” .

ATTENTION! The INV-2 document is filled out by representatives of the inventory commission in the amount of 1 copy per 1 warehouse facility. It is signed by only one of the commission members, as well as the person responsible for storing the MC. The form should be stored in the places where the inventory items recorded in it are located, that is, at the appropriate warehouse facility. Subsequently, the data from the INV-2 document is used when filling out the main inventory compiled according to the INV-3 form.

Inventory label: general information about the document

The label is used in the process of recounting inventory items. The document is not independent; it is issued as an auxiliary form in the following cases:

- if the range of products being tested is so wide that its exact number cannot be calculated in 1 working day;

- if material assets subject to recalculation are located in several warehouses remote from each other.

Form INV-2 acts as a supplement to form INV-3. The document is drawn up in a single copy, typewritten or by hand. The basis for using data from a document when compiling inventories is the presence of completed required details and affixed signatures, and the absence of empty columns. Simultaneous registration with INV-3 is not allowed.

The completed label form must remain in storage in the warehouse where the values recalculated and reflected in the document are located. A separate form is filled out for each inspected premises. At the end of inventory activities, members of the commission transfer information from all labels to the inventory.

Components of the form

The inventory has several pages. The first is introductory, it contains a part with a receipt, the second and subsequent elements are presented in the form of a table. At the conclusion, the signatures of the responsible persons are affixed.

First part of the form

Fundamentally important points are indicated at the beginning. In the form of a small table on the far right side of the sheet, the form numbers according to OKUD, OKPO, the code of the type of activity of the organization, the document number and the date of its preparation, two dates: the beginning and end of the inventory are listed (even if it was carried out on one day, indicating both identical ones is mandatory), type of transaction performed and accounting account number. The last two columns are filled in by the accountant after the signatures of the commission members and consideration by the manager.

Also, separate lines are left for the full name of the organization (abbreviations to LLC, OJSC, individual entrepreneur, etc.) and the name of the division are acceptable. The latter, in the vast majority of cases, is a warehouse under some serial number, since the INV-5 form is the most common in warehouse policy.

Important point! At the top, the basis for the inventory must be indicated. This may be an order, notification or order from the head of the company as a whole or its division.

In any case, the inventory process must be carried out under the guidance and knowledge of the persons concerned. This fact must have documentary evidence.

Part with receipt

On the first sheet of the document there is a receipt from the financially responsible person stating that by the time the inventory began, all the primary reporting documents necessary for this had been submitted to the accounting department, and goods and materials (inventory assets) had been capitalized and accepted for safekeeping.

Also, at the beginning of the verification process, all material resources written off from accounts must be indicated in the disposal papers. It is undesirable for them to actually be in the warehouse itself to avoid misunderstandings.

The receipt must also indicate the date of its signature and the deadline for removing the remaining material assets.

The second part of the form is tabular

The information is very compactly placed in the table. Using the latter is extremely convenient. The form was formed in the 90s, but still remains relevant. The rows of the table are filled in as the actual availability of inventory items in the warehouse is compared with the data in existing documents. The columns should contain the following information:

- The sequence number of the line.

- Name and OKPO code of the supplier or recipient.

- Nomenclature number of the product, its grade, type or group, full name.

- Storage location (usually the cell or location number is indicated).

- The date when the goods were accepted for responsible warehousing.

- Name, number and date of the document that indicates the receipt of goods and materials at the warehouse (for example, invoice 25 dated August 23, 2019).

- The unit of measurement of the purchased goods and the code of this unit according to OKEI (g, kg, l, pcs., etc.).

- How much inventory material actually exists, total quantity and cost.

- How much goods are available according to currently maintained accounting records.

If the last two columns of the same column are not identical, then this is a defect of the accountant or storekeeper (or other person financially responsible for the product being described). The INV-5 form is convenient precisely because it is possible to illustrate this kind of discrepancy.

Final part

When the inventory is nearing completion, the chairman of the commission and all its members must review the compiled table and put their signatures at the end of the inventory list of inventory items accepted for safekeeping. The signatures will indicate that the availability of goods, their actual quantity and cost have been verified.

Important! Separately at the end, the total amount of all inventory items is indicated in numbers and words. The financially responsible person puts his signature after all members of the commission as a sign that he has no complaints about their work and agrees with the data provided

The form leaves space for the signatures of two such MOLs, but there may be more. Below the signature of the responsible person is usually the signature of the accountant who verifies the calculations made in the document

The financially responsible person puts his signature after all members of the commission as a sign that he has no complaints about their work and agrees with the data provided. The form leaves space for the signatures of two such MOLs, but there may be more. Below the signature of the responsible person is usually the signature of the accountant who verifies the calculations made in the document.

INV-2: sample filling

The header of the document contains the following information:

- the name of the enterprise is given;

- indicates the department or warehouse where the inventory of goods and materials was carried out;

- OKPO and type of activity codes are entered;

- information about the order that is the basis for carrying out inventory activities;

- inventory period (written out from the order);

- number and date of issue of the label.

To correctly fill out INV-2, the form must contain information about the storage locations of inventory items, names of valuables, their units of measurement and nomenclature codes, and the number of units in stock. The storage location means not only the warehouse number, but more detailed information - the numbers of racks, shelves, cells in safes or cabinets, compartments. Converted values are indicated by location by actual location.

When specifying the name of the product, the brand and grade of the object are specified. It is allowed to provide information about the size of property assets. The item code must correspond to the warehouse numbering. Units of measurement are given in the form of text designation and OKEI code. The amount of valuables in the warehouse is reflected in numerical format and in words.

INV-2 is signed by the financially responsible person and a representative of the inventory commission. On the reverse side, the signature of the official of the enterprise who accepted for storage the property that has undergone the inventory procedure must be affixed. This signature indicates the employee’s consent to accept the values and confirms that the property objects in the warehouse are in the quantity indicated on the label. The completed form does not need to be submitted to the accounting department.

Recommendations for designing the INV-2 inventory label

For the inventory label, there is a standard unified form INV-2, developed and approved by the State Statistics Committee of Russia in Resolution No. 88 of August 18, 1999. Since the beginning of 2013, organizations have been exempted from the mandatory use of unified forms, this also applies to inventory documentation. An enterprise can develop its own form of inventory label, which will take into account all the specifics of the activities of a particular enterprise and the inventory values; you can use the unified INV-2 form.

The standard form is presented with a header part, a place for reflecting information about the storage location, indicating individual quantitative characteristics for the name of the inventory items stored in the specified location, as well as a receipt from the materially responsible person accepting the recalculated values for storage.

The label is filled out separately for each warehouse object.

The following information is filled in at the top heading of the INV-2 form:

- The name of the organization and structural unit where the reserves are stored;

- Main codes – OKPO and type of activity;

- Documentary justification for carrying out an inventory, usually the manager draws up an order in the INV-22 form or in any form - the number and date of the document is indicated at the top of the INV-2 form;

- The inventory period, according to the order;

- Label number;

- Date of preparation.

Filling out information about inventory items:

| Field name | Explanations for filling |

| MC storage location | Specifying information on the location of the inspected valuables in the warehouse is indicated; the following may be indicated:

The available information is filled in depending on the inventory storage system at the enterprise warehouse |

| Name of MC | The goods and materials stored in the specified location are indicated. If necessary, detailed information about the brand, grade, dimensions, and accompanying drawings is provided. The fields are filled in depending on the type of property |

| Nomenclature code | The corresponding code is entered according to the warehouse nomenclature |

| Unit | OKEY name and code |

| Quantity | In digital and capital form |

The responsible persons sign under the tabular part:

- One of the commission members who conducted the property recount;

- Financially responsible person.

The reverse side of the form contains a receipt from the person accepting the specified quantity of inventory items for safekeeping. This person confirms with his signature the fact of acceptance of exactly the quantity indicated in the receipt.