In what case is the unified statement T-49 used?

Payroll T 49 is used by an entity in the case where it simultaneously calculates wages and subsequently makes payments.

This document differs from the T-12 form in that it does not provide columns for deciphering work time data for each day.

However, its most important advantage is that this form combines sections on accrual and payment of remuneration to employees. That is, this document allows you to visually check the calculation of wages, their payment, calculated taxes, as well as the amount of debt incurred.

But a significant disadvantage of this statement is that it contains a large amount of information, so it is not used in organizations with a large number of employees.

Attention! In addition, the use of such a document assumes that payment of wages will be made in cash, that is, through the company’s cash desk. Therefore, such a salary sheet does not apply when salaries are transferred to cards.

Business entities in these cases can use payroll form T-51. Payments are processed either in the form of a transfer register or in separate payment transfers.

In this regard, payroll has been used less frequently lately; many are switching to payroll projects and abandoning it.

Most payroll programs include this form. It is formed on the basis of timesheets, which are verified by relevant specialists, as well as information on the amount of payment from the staffing table or employment contract.

Attention! Data on the accrual of vacation pay and disability benefits should be indicated in this document on the basis of separate calculations in total amounts for each person.

Here the personal income tax amounts are calculated, which is then summed up for all employees and transferred to the budget. The completed forms are transferred to the company’s cash desk, and according to them, employees receive their salaries on time.

Which document form to use?

From 01/01/2013, organizations have the right to independently develop primary accounting documents, including those for the payment of wages. The primary documents must provide for the presence of all mandatory details in accordance with Part 2 of Art. 9 of Law No. 402-FZ.

But many companies continue to use forms approved by Goskomstat. Thus, Resolution No. 1 of January 5, 2004 approved the following forms:

- T-49 “Payment and payroll”;

- T-51 “Payment sheet”;

- T-53 “Payroll”.

If the organization uses form T-49, forms T-51 and T-53 are not drawn up. Next, we will tell you in more detail about the rules for filling out the unified form T-49 (the payroll sheet can be found at the end of the article).

Sample of filling out a unified payroll statement according to form T-49

The registration of the form T-49 must begin with the header of the form. The full name of the company is indicated here, as well as the code assigned to it according to the OKPO directory.

The statement can be used to determine the earnings of the entire company, or only a specific division. In the latter case, its name is indicated on the next line, otherwise a dash is placed.

bukhproffi

Important! Next, you need to indicate the period of time during which the salary will be paid. According to the rules established by law, it should not be longer than three days.

On the next line, the total amount to be issued is written in words.

The document is signed by the head of the company and the chief accountant. They must transcribe the signatures and also record the date of approval.

To the right of the name of the document, you must write down the serial number of the statement, the date it was completed, as well as the time period for which the calculation was made.

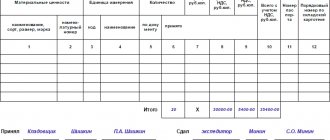

Next, fill out the table, which occupies the main part of the document. In each line you must indicate data (accruals, deductions, salary advances, etc.) for one employee.

Filling out a line begins by indicating its serial number, the employee’s number on the timesheet, his position, salary or tariff rate. All this information is transferred by the responsible person from the T-2 personal card.

After this, you need to fill out the columns with the subheading “Days worked” (columns 5-7). They alternately enter the number of working days, holidays and weekends worked during a given period. This information must be transferred from the time sheet.

Next come columns 8-13, which are united by the common subheading “Accrued”. This includes the amount of accrued payment for various types of payments - salary, bonus, sick leave, vacation pay, etc. In column 14, you must enter the total amount for all payments to the employee.

Columns 15-18 are collectively titled “Retained and Credited.” This includes the amount that was withdrawn from the employee’s earnings - personal income tax, alimony, coverage of damage caused, etc. All deductions are recorded in the columns separately, for each type.

Columns 19-21 are intended to indicate totals for the employee. In these columns you can enter information about the debts of the employee or organization at the time of determining the salary amount, as well as display the final amount that will be issued.

Columns with the subheading “Received money” are filled in when the employee receives a salary. In column 22 he writes down his full name, and in column 23 he puts down his personal signature. If the day was not paid to the employee on time, then a mark indicating their deposit is placed in these columns.

After the money has been issued, the cashier (accountant) who issued the money must do the following:

- Place your signature in the “payments made” field.

- Indicate the details of the cash receipt order used: number, date when it was issued.

- Indicate in words the amount that was issued according to the statement and duplicate the entry in numbers and indicate the deposited amount, if any.

You might be interested in:

Memo on the employee’s absence from the workplace: how to write it correctly

At the end, the document is signed, usually by the chief accountant or the person responsible for issuing wages.

When is the T-49 form used?

Form T-49, approved by Decree of the State Statistics Committee of the Russian Federation dated January 5, 2004 No. 1, is used to calculate wages in organizations that have a small number of staff and pay wages in cash.

It includes signature fields, so it is also a payroll. When using form T-49, other documents (payroll on form T-51 or payroll on form T-53) are not drawn up. ConsultantPlus experts explained the nuances of paying salaries from the cash register:

If you do not have access to the K+ system, get a trial online access for free.

For use, the T-49 form, which is classified as unified, is not mandatory and can be replaced by another independently developed document of a similar purpose. However, it is familiar to use and contains all the fields that may be necessary to fill out. This makes it in demand, despite its optional use.

The accounting department of the employer who has decided to use the T-49 form calculates wages on its form monthly in the usual manner based on the initial data necessary for calculating wages:

- tariff rate, salary;

- time sheet;

- documents confirming the reason for absence during paid periods (sick leave, vacation order, business trip);

- administrative documents for additional payments;

- documents confirming the issuance of money against the accruals made.

Errors when filling out

When entering data into a document, the responsible person may make mistakes. But it must be remembered that this document is a primary one, and corrections are not allowed in it. If inaccuracies were identified before the payment of wages, then it is necessary to issue a new statement and destroy the old erroneous one.

However, if payments have already been made on the document, then you should not destroy it. It is necessary to make a correction directly in the document; the director and chief accountant must sign next to it. In addition, an accounting certificate is prepared, which sets out the reasons for making the corrections.

Using accounting programs to compile it will allow you to avoid errors in the document.

Typical errors that are made in the statement:

- Errors in personal data of employees;

- Incorrect indication of the amounts of accruals, deductions, etc.

- Incorrect application of tax deductions;

- Arithmetic errors when calculating totals.

Who draws up and maintains the T-49 form in 2020?

Filling out and maintaining this document is carried out by an accountant or cashier of the organization. The basis for filling out this document is the working time sheet.

The accountant fills out the title page and table, and also puts his signature on the document. Once the T-49 form is signed, it is given to the cashier.

Before issuing funds, the statement is signed by the head of the enterprise.

After issuing money to employees, the cashier passes the document back to the accounting department. In accounting, the document is checked and a corresponding entry is made in a special journal.

Please note that if there is no cashier at the company, an accountant can issue and fill out the T-49 payroll sheet.

How are errors corrected in the T-49 payroll form?

If there was an error in the document that was discovered before the payment of wages to the employee, the cashier submits the statement to the accounting department for correction.

If an error is discovered in the document after the funds are issued, the incorrect data must be carefully crossed out. The correct information is indicated at the top.

When making corrections in the payroll statement, the use of a prime is not allowed.

All corrections must be certified by the signatures of the cashier, accountant and head of the organization.

In the absence of appropriate signatures and the date of data change, the adjustments made will not be considered valid.

Filling procedure

It can be compiled in either paper or electronic form. The electronic payment document must be signed with an electronic signature. The filling procedure is regulated by Directive of the Central Bank of the Russian Federation No. 3210-U dated March 11, 2014.

Next, we will tell you how the salary sheet is formed; you were able to download the form earlier.

First of all, the title page is filled out: all organizational details of the institution are indicated (name, INN/KPP, OKPO). It is also necessary to indicate the total amount paid, indicate the billing period, number and date of the PO. The head and chief accountant put their signatures in the title part.

The tabular part is formed from the following information data:

- serial number;

- employee position;

- Personnel Number;

- FULL NAME.;

- salary (rate) according to the tariff;

- the amount of time worked according to the time sheet;

- deductions and accruals carried out for each employee;

- signature column.

The bottom lines indicate the total amounts for all employees: how much money was paid and how much was deposited. It is also noted who made the salary payment, the name and initials of the responsible employee - the accountant, as well as the date of verification of the payment document.

The terms for issuing funds are limited - no more than five working days. In the event that the employee has not received wages within the specified period, the amount is deposited, and the corresponding mark is placed in the notice.

Payment statement

The form has a unified form according to OKUD 0504403. Documentation is provided to reflect the issuance of wages and advance payments from the institution’s cash desk. If a government agency pays salaries in cash, then a PV is drawn up. The current form in 2022 looks like this:

Information is entered on the basis of settlement documents for the reporting month. You should also take into account information about advances paid and the amounts of arrears in payment of wages.

The final data of the payment and settlement forms must match. The only exceptions will be amounts of deposited wages that employees were unable to receive on the day of issue for valid reasons.

Upon receipt, each employee of the institution is required to count the money received at the cash desk and sign the PO.

Note that if an organization transfers the salaries of its employees directly to bank cards, for example, to the MIR salary card, then it is not necessary to draw up a PO.

The completed sample document looks like this: