Who must submit an income statement?

The legislation determines that accounting is the responsibility of every business entity that is registered with the Federal Tax Service as a legal entity.

In this case, no exceptions are made and the organizational form of the enterprise, the taxation system used, etc. are not taken into account. Accounting statements, and in their composition the report on financial results, must be sent to the Rostat and INFS bodies without fail.

Non-profit organizations and bar associations must also submit a profit and loss statement, Form 2, since this form is required to be completed by all entities.

Only citizens who have registered an individual entrepreneur as a legal form are exempt from this obligation. The same right exists for divisions of foreign companies. All these entities can prepare reports and send them to the authorities on a voluntary basis. Previously, reports did not have to be prepared and submitted to the relevant authorities only by companies using the simplified tax system.

The company may be classified as a small business. In this case, the provisions of the law provide for a simplified reporting procedure for such companies.

Attention! Even if you use this benefit, the company must prepare and submit accounting reporting forms, but in a simplified form. Companies must remember that this set of statements includes both a financial statement, Form 2, and a balance sheet, Form 1.

Who rents it out

Each legal entity that is registered with the tax office and conducts financial and economic activities must reflect all transactions in accounting and submit periodic and final reports to the regulatory authorities.

According to the rules, the new form of financial statements (like the balance sheet) must be submitted by absolutely all economically active entities, regardless of their legal form and taxation system. This rule also applies to non-profit organizations.

Which form to use - simplified or complete

An enterprise that does not meet the criteria for being classified as a small business must submit a balance sheet form 1 and a financial statement form 2 in full according to the provided reporting forms.

Organizations that have the right to use simplified reports are determined by the legislation “On Accounting”, these include:

- Companies classified as small businesses.

- Non-profit organizations.

- Participants in research and development projects on Skolkovo legislation.

Only these entities are given the right to prepare simplified accounting statements. Based on the prevailing circumstances and characteristics of the enterprise, they can independently decide on the use of reporting forms. They must consolidate this decision in the company’s accounting policies.

However, the use of simplified reporting is unacceptable for such business entities as:

- Firms whose reporting must be verified by statutory audit. They are determined by relevant legislation.

- Companies belonging to housing and housing-construction cooperatives.

- Credit consumer cooperatives.

- Microfinance companies.

- Government organizations.

- Parties and their branches in the regions.

- Bar associations, law offices, chambers of lawyers, legal consultations.

- Notaries.

- Non-profit enterprises.

What the reference table shows

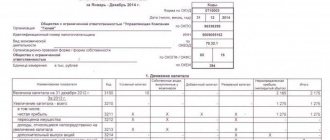

The 2nd table in the income statement contains background information divided into 2 parts:

- on income that increases the profit received by directly attributing it to capital (for example, the amounts of revaluation of fixed assets and intangible assets falling directly into additional capital) indicating the amount of the final profit of the period adjusted for these incomes;

- profit (loss) per 1 share (this data is needed for JSC).

The recommended form of the reference table is similar to the structure of the main report table and also requires the introduction of an additional “Code” column.

Report submission deadlines

Financial statements, including balance sheet form 1, financial performance statement form 2, etc., must be sent to the tax authorities and Rosstat no later than March 31 of the following year. This temporary restriction exists only for the above listed bodies.

However, for statistics, it is possible that upon the occurrence of certain events it will be necessary to attach to the standard package an auditor’s report regarding the prepared annual report. The company must submit it to Rosstat within ten days from the date the auditors issued their report, but no later than December 31 of the following reporting year.

In addition, reports can be submitted to other competent authorities, as well as published due to the characteristics of the type of activity being carried out in accordance with legal norms. For example, companies that are tour operators must submit accounting forms to Rostourism within three months from the date of its approval.

The rules of law establish a different reporting procedure for companies registered on October 1. They can exercise their right and submit reports not until March 31 of the following year, but a year later.

For example, Rassvet LLC was registered with the Federal Tax Service on October 23. By decision of management, the company will submit its annual report by March 31, 2019, including information for the entire period of activity in one report.

Attention! Companies must file reports annually. Reporting, especially the financial performance report Form 2, can be presented not only annually, but also monthly or quarterly.

As a rule, in this case, its recipients are the owners who use it to make management decisions, credit institutions to process loans and credits, etc. Such accounting statements are called interim.

You might be interested in:

Book of accounting of income and expenses for individual entrepreneurs on the simplified tax system: how to fill it out in 2020

What you need to know about the financial results report for 2022

The most important:

- All “private” legal entities must submit a report to the Federal Tax Service (GIRBO), except for those for whom special exceptions have been made at the legislative level;

- The financial results report is submitted as part of the annual financial statements. The deadline for submission for 2022 is 03/31/2022;

- You can submit financial statements for 2022 only electronically. The previously valid exemption for SMEs is no longer valid from 01/01/2022.

You will find more information about how you can submit annual financial statements for 2022 to the tax office, as well as instructions for submitting them through the Federal Tax Service website, in the article “Balance Sheet for 2022.”

For 2022, the report must be made in the form approved by Order of the Ministry of Finance dated 07/02/2010 No. 66n, as amended on 04/19/2019 (hereinafter in the text + Order No. 66n).

Companies that have the right to conduct simplified accounting also have the right to submit financial statements using simplified forms.

The financial results report for 2022 is still a required form in any reporting package (full or simplified).

The form, sample and rules for filling out a simplified statement of financial results for 2022 are in the article “Simplified financial statements for 2022”.

Let's look at the line-by-line procedure for filling out a full (not simplified) statement of financial results for 2022. Further in the text we will use the abbreviated name of the report – OFR.

Where is it provided?

The laws establish that financial statements and the included form okud 0710002 profit and loss report are submitted to:

- To the relevant tax authorities - it must be submitted at the place of registration. In this regard, if an entity has separate divisions, it should not send its reports to the Federal Tax Service. Their information is included in the consolidated report of the parent company, which submits it to its legal address.

- It is mandatory to send reports to the territorial bodies of Rosstat if the company does not want to be fined on a fairly large scale.

- Owners and founders of the company - the annual report must be approved by them.

- To other government bodies, if this is directly stated in federal laws.

When concluding large contracts, partners can request financial statements from counterparties to confirm their reliability and financial solvency.

Management can decide to grant it or deny it. However, it must understand that this data can be obtained using special programs or partner verification services.

Attention! Also, quite often, reporting forms are requested by banks and other credit institutions when a company receives various loans. For example, if you need to get a loan to develop or start a business.

What is the structure of Form 2 enterprises in 2021–2022

The structure of the income statement for 2021–2022 corresponds to that in force starting with the reporting for 2011. It still highlights the following to be filled out:

- the header part of the report, which indicates the period for which it was compiled, the date of compilation, all the main statistical codes (with their text interpretation) and the TIN of the legal entity are given, as well as the order of the unit of measurement in which the figures are entered into the report;

- the main table containing the calculation of the financial result itself;

- lookup table;

- manager's signature and date of signing.

The report form recommended by Order No. 66n contains under this information the text of notes clarifying the procedure for filling out individual indicators of the form.

Like any form recommended for use, the profit and loss statement can be supplemented with lines and columns or developed independently while maintaining its semantic load.

Delivery methods

The financial performance report Form 2, included in the annual report, can be sent to the competent authorities using the following methods:

- Come to the institutions and submit the financial statements to the responsible person in person on paper in two copies. Sometimes they may also ask you to provide an electronic file of it. This method is not available for companies with more than one hundred employees.

- Send a valuable letter through post offices or courier services. The post office will require an inventory of this letter.

- Using electronic document management, you can submit annual reports to all specified authorities if you have a qualified electronic digital signature (EDS). For this purpose, a specialized program, tax authorities website, etc. can be used.

Common errors when generating a report

The income statement is a form of strict accounting reporting and must be prepared properly. To avoid incorrect actions and inaccuracies, we will deal with common errors in the report in Form 2.

It is strictly forbidden to hide real data on the effectiveness of your financial and economic activities.

Serious errors include:

- Filling out line 2110 “Revenue” taking into account the amount of calculated VAT.

- Calculation of income tax without applying PBU “Accounting for income tax calculations”.

- Lack of a certificate deciphering the reporting indicators.

Follow your calculations and avoid arithmetic errors. To avoid inaccuracies in the total values when preparing a report, it is recommended to use specialized programs and services.

Form and sample for filling out a financial performance report in Form 2 in 2022

Financial results report form 2022 free download in Word format.

Download the 2022 financial results report form in Excel format.

Download the profit and loss statement form 2 with line codes in Excel format.

Download a simplified form of the profit and loss report in Excel format.

Profit and loss report form 2 sample completed download for free in Pdf format.

Form 1: balance sheet

The balance is a table divided into 2 parts:

- Part 1. Balance sheet assets are the assets and liabilities of a company that are used in its activities and can bring benefits to it in the future.

- Part 2. Balance sheet liability - reflects the sources of formation of the balance sheet asset.

In a correctly drawn up balance sheet, the equality is satisfied:

balance sheet asset items = balance sheet liability items

In more detail, this equality for Form 1 of the financial statements looks like this:

Section 1 + Section 2 = Section 3 + Section 4 + Section 5,

Where

- Section 1 - the value of non-current assets (long-term used property, the cost of which is repaid in installments).

- Section 2 - the cost of current assets (quickly turnover and quickly redeemed assets: materials, inventories, etc.).

- Section 3 - the value of capital and reserves (sources of the company's own funds).

- Section 4 and Section 5 are long-term and short-term liabilities expressed in monetary terms, respectively (the company's obligations to pay loans, loans, taxes, wages, etc.).

Using the balance sheet (Form 1 of financial statements) you can:

- analyze and evaluate the financial condition of the company as of a specific date;

- track the dynamics of changes in indicators over time (comparing indicators of balance sheets compiled as of previous reporting dates);

- conduct an economic analysis of the company’s activities and, on its basis, make informed management decisions.

How to fill out a profit and loss statement form 2: full version

When filling out the financial results statement Form 2, you should follow a certain sequence.

The period under review is written under the title of the report. Further in the table, on the right, the date of compilation of the report is reflected. Below you need to write down the full or abbreviated name of the company, and in the tabular part - the registration code with Rosstat.

Then the TIN of the reporting company is reflected. Next, the name of the main type of activity carried out by the company is written down in words, and the OKVED code 2 is indicated in numbers.

The next line indicates the organizational form and form of ownership of the organization and puts the corresponding codes next to it. Next, the unit of measurement used is recorded.

The report itself is a table in which the company’s performance indicators are reflected in terms, and in the columns their value in the period of time under review and the previous one similar to it. Thus, a comparison of two periods of activity occurs.

Line 2110 should reflect the income received during the reporting period from all types of activities. This indicator is equal to the credit turnover on the account. 90.1. In this case, VAT should be removed from the revenue amount.

In the following lines of this subsection, you can decipher the amounts of income by type of activity. Small businesses may not do this.

Line 2210 reflects the amount of expenses incurred by the enterprise for the manufacture of products or the provision of services (work). The amount of the account turnover is reflected. 90.2.

At the same time, depending on the cost formation method used, the amount of expenses may include administrative expenses or not. If they are not included in the cost price, these amounts are reflected in line 2220.

If necessary, a breakdown of expenses by area of activity is also made here.

You might be interested in:

Form 6-NDFL: deadlines, instructions for filling

Line 2100 determines the gross profit (loss), which is calculated as the difference between line 2120 and line 2210.

In line 2210, you should record the expenses incurred by the enterprise for the sale of products, goods, etc.

After this, in line 2200 the profit from sales is calculated, which is equal to the difference between lines 2100 and lines 2210, and line 2220.

Next, line 2310 indicates income received by the organization as dividends from other legal entities, other income from the participation of the company as a founder.

Line 2320 is used to reflect accrued interest on borrowed funds.

Line 2330 records the interest that the company must pay for the use of borrowed funds.

Line 2340 includes the amount of revenue received from non-core activities, including the sale of fixed assets, materials, etc.

Line 2350 reflects the amounts of expenses incurred for non-core activities, including the residual value of property sold and costs of materials sold.

Line 2300 calculates the enterprise's profit before tax. It is equal to the sum of lines 2200, 2310, 2340, from which the indicators of lines 2330,2350 are subtracted.

Line 2410 should reflect the income tax calculated on the basis of the relevant declarations. It is determined in profit declarations.

On line 2421 you should record the amount of the permanent tax liability or asset that affected accounting profit in the current year.

Lines 2430 and 2450 reflect discrepancies between the indicators of income and expenses for accounting and tax accounting, which are considered temporary, since their acceptance for accounting may occur in different periods. In this case, line 2430 reflects the amount of tax that will increase it in the future, and line 2450 will reduce it.

Line 2460 should reflect the amounts of indicators that were not considered and taken into account earlier, but nevertheless affect the company’s profit. For example, these could be various fines, a trading fee, etc. The indicator can take a positive value (turnover according to DT 99 is greater than turnover according to CT 99), or a negative value (vice versa).

Line 2400 is defined as the difference between line 2300 and line 2410, to which lines 2430, 2450, 2460 are added (subtracted).

Line 2510 records the change in the value of property based on revaluation, and line 2520 records other results that are not taken into account when determining profit.

Line 2500 reflects the adjusted profit indicator; it is equal to the sum of line 2400 plus lines 2510 and 2520.

Lines 2900 and 2910 are filled out as a guide and include information about basic and diluted earnings per share.

At the end, the document is signed by the manager and the date of approval of the document is set.

Other income

Line 2340 “Other income” of the 2021 income statement includes income that the company recognizes as other and which was not included in separate lines above. This:

- payment for temporary use (temporary possession) of the organization’s assets (if these receipts are not recognized as income from ordinary activities);

- payment for the rights to use the results of intellectual activity (if this is not income from ordinary activities);

- proceeds from the sale of fixed assets and other assets other than cash (if this is not a sale as part of the main activity;

- income related to long-term assets for sale (including changes in the amount of the reserve for impairment of value, the result of the sale), if they do not fall into other lines of the financial statement;

- fines, penalties, penalties for violation of contract terms;

- assets received free of charge, including under a gift agreement (except for those received from participants, founders, shareholders and those attributed to an increase in capital);

- profit from joint activities under a simple partnership agreement;

- proceeds to compensate for losses caused to the company;

- profit of previous years identified in the reporting year;

- amounts of accounts payable for which the statute of limitations has expired;

- positive exchange rate differences;

- receipts from operations with containers;

- the amount of additional valuation of fixed assets within the amount of depreciation of this fixed assets in previous reporting periods, attributed to other expenses;

- the amount of additional valuation of intangible assets within the amount of depreciation of this intangible asset in previous reporting periods, attributed to other expenses;

- the amount of the recovered loss from impairment of intangible assets recognized in previous reporting periods and charged to other expenses;

- amounts of revaluation of financial investments;

- negative business reputation when acquiring an enterprise as a property complex;

- other similar income recognized as other income.

Line 2340 does not reflect income recognized in the reporting period in connection with the receipt of budget financing. Such income is presented as a separate item, provided that the amount is significant.

Line 2340 includes credit turnover on account 91-1 minus subaccounts, which take into account what is included in separate lines (interest, income from participation, etc.) and minus debit turnover on account 91-2 in part VAT, excise taxes and similar payments included there.

Other income can be shown in the FIR “collapsed” minus expenses related to these income, if the accounting rules do not prohibit such reflection or if such reflection is not significant for characterizing the financial position of the company.

At the same time, if other income amounts to 5% or more of the total income for the reporting period, they are deciphered in the OFR for each type separately. To do this, the organization can enter additional lines into the OFR (clause 18.1 of PBU 9/99).

How to fill out a simplified income statement line by line

The simplified form for okud 0710002 differs from the main one in that in the tabular part it has a significantly reduced number of reflected performance indicators.

It states:

- Enterprise revenue (line 2000).

- Expenses of a company in its normal activities.

- Interest paid by the company for the use of borrowed funds (line 2330).

- Other income.

- Other expenses (2350).

- Income taxes taking into account all deferred and permanent assets and liabilities.

- Net profit (2400).

Attention! Indicators are calculated in the same order as in a standard report. It’s just that, as a rule, organizations using this form do not have all other information.

How to fill out the full form

When filling out a profit and loss statement, information is entered using turnover data from accounting accounts:

- 90 (for core activities) and 91 (for other income and expenses). VAT and excise taxes are excluded from revenue. The result obtained from the profit and loss statement in terms of the amount of profit (loss) before tax must coincide with the similar result of account 99.

- 09 and 77 (according to ONA and ONO) for legal entities applying PBU 18/02. The values of income tax and net profit generated using them in the report should give, respectively, the amount of tax received according to the declaration and the amount of the final profit (loss) that arose in accounting.

- 83 (for income not included in net profit) when entering data into the reference table.

A line-by-line comment on filling out the tabular part of Form 2 is given in the ConsultantPlus system. If you do not have access to the system, get a trial demo access and proceed to the explanations for free.

For information on the rules for drawing up a similar report for IFRS purposes, read the material “Preparing a profit and loss statement in the IFRS format” .

Common mistakes when filling out Form 2 of the balance sheet

Many errors when filling out this form are caused by arithmetic inaccuracies. Therefore, when filling out a report, it is best to use specialized complexes that perform all calculations automatically.

The most common mistakes made when filling out are:

- Quite often, when filling out the “Revenue” indicator, accountants forget to exclude the amount of accrued VAT from income.

- Another common mistake is to distribute income by type without taking into account the Accounting Regulations. Some professionals may include interest or income from participation in other organizations as other income.

- When determining the current tax, it is necessary to take into account the PBU “Accounting for income tax calculations”, which many do not do in practice.

- You also need to decipher some reporting indicators, which are given at the very end of the form in the form of a certificate. Experts quite often ignore this point.

Contents of the main report table

In the form of the profit and loss statement given in Order No. 66n, the main table consists of 4 columns:

- explanations that are filled out if there are deviations from the lines proposed by the form or if there are numbers in the report that require more detailed disclosure;

- unified names of indicators (rows of the table in which, sequentially, from the amount of revenue received before taking into account IT and ONA, which affect income tax, the financial result of work for the period indicated in the title is calculated);

- digital values of these indicators corresponding to the reporting period;

- digital values of these indicators corresponding to the same period of the previous year.

Only organizations whose information relates to state secrets, as well as in cases established by the Government, submit reports to Rosstat. Reporting lines submitted to Rosstat must be encoded. The codes required for this are given in Appendix 4 to Order No. 66n. In order not to adjust the reporting submitted to different authorities, it is more convenient to initially prepare it in a form containing the “Code” column between the 2nd and 3rd columns of the form recommended by the Ministry of Finance. Moreover, during current work with reports, it is often preferable to indicate the line numbers of the form rather than their names.