What is it needed for

Registration of an M-4 order is necessary for warehouse accounting of operations for the receipt of materials, marketable products or other valuables.

This document is also drawn up upon receipt of raw materials and semi-finished products for production workshops and divisions of the organization. This document indicates the actual volume of all accepted accounting items.

In case of multiple deliveries of the same type of materials or goods during the day, a single order is allowed.

It is advisable to use a receipt order form M-4 when it is impossible to use other forms of accounting as receipt documentation.

You can issue a receipt for several types of materials, if they are supplied under one invoice. Keeping records of units of precious metals and stones deserves special attention.

The receipt order must display not only the number of valuables; the registration number of the technical passport for each type of metal or stone must be written in a special column.

When a cash receipt order is issued

Since the cash receipt order is the primary accounting document, therefore, it must be drawn up when committing a fact of economic life (Part 3 of Article 9 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting”), that is, according to the fact of receipt of cash at the cash desk of an organization or individual entrepreneur.

Thus, it is necessary to issue a cash receipt order at the time of depositing cash at the cash desk of a business entity.

General rules for filling out the Receipt Order

When filling out the Receipt Order, you must consider the following.

- All fields in the document must be completed.

- If there is no data in the column, a dash is placed

- The unit of measurement code is filled in in accordance with the All-Russian Classifier of Units of Measurement.

- If an organization takes into account the type of inventory data in units of measurement different from those specified in the supplier’s documents, the quantity is indicated in two units of measurement. First - in those units specified by the supplier, then in those installed in the organization. If the organization has developed and approved a system for converting from one unit to another, then the quantity can be indicated in the units of measurement adopted in the organization and a link to the relevant local regulation can be given.

- When a smaller/larger unit of measurement is indicated in the supplier's documents, the materials are accepted in the unit of measurement accepted by the organization.

- When accepting MPZ containing precious metals, the column “Passport number” is filled in; in other cases, a dash is placed in this column.

Legal regulation

Federal Law No. 129 of November 21, 1996 “On Accounting” in Article 9 includes a requirement for the need to document all management transactions with primary documentation.

Resolution of the State Statistics Committee of the Russian Federation No. 71a dated October 30, 1997 established a primary document for the posting of enrolled materials. Such a document is the form of receipt order M-4.

According to clause 49 of the “Methodological guidelines for accounting of inventories”, ratified by Order of the Ministry of Finance of the Russian Federation No. 119n dated December 28, 2001, an M-4 order accompanies any crediting of materials.

Organizations that, in addition to trade, are engaged in other types of activities must receive and receive goods in the same way as the procedure for registering material objects.

This is provided for in paragraph 224 of the above Guidelines. It is important that this procedure should not be followed by entities conducting only trading activities.

According to Article 9 of Federal Law No. 129, the receipt order M-4 specifies the date of receipt, the number of material assets and other essential details.

If receipt orders are not used in accounting, tax authorities have the right to make claims regarding shortcomings in the primary documentation and cancel the deduction of input VAT.

According to clause 3 of Article 120 of the Tax Code of the Russian Federation, failure to draw up primary documentation is considered a gross violation of the standards for accounting for income/expenses and taxable items.

The fine under this standard varies from five to fifteen thousand rubles. If the tax base is understated, the amount of penalties is equal to ten percent of the amount of unpaid tax, but not less than fifteen thousand rubles.

If the material assets received are capitalized without generating a receipt order, this may be taken into account as an understatement of the tax base.

For any business transaction, it is necessary to draw up primary documents with the presence of mandatory details. Only after proper preparation can the documents be accepted for accounting, and the business operation reflected on the accounting accounts.

From which it follows that the receipt of material assets on the organization’s balance sheet is reflected in the accounts only after drawing up the M-4 receipt order.

After this, the entity has the right to use the deduction of input VAT if other conditions for offset are met.

Registration deadlines

There are cases of large volume deliveries of goods during the day. The legislation allows you to draw up one receipt document, and enter all goods into it as they are received until the end of the working day. However, these must be homogeneous goods (for example, raw materials or semi-finished products of a certain group).

NOTE. The order is issued only on the day the goods or raw materials arrive. Accordingly, it must be drawn up upon receipt before the end of working hours.

Thus, an order must be drawn up only in the event of further use of goods and raw materials for the production of new products . And if the company is engaged in their sale, then it is enough to simply use the invoices for the goods and affix the organization’s stamp.

As a general rule, when materials are received by an organization, a receipt order is issued in form No. M-4. Is it necessary to draw up this document when receiving goods? After all, they are also inventories. Let's consider what problems may arise when maintaining document flow without using Form No. M-4.Primary document on materials... All business transactions must be documented in primary documents. This requirement is contained in Article 9 of the Federal Law of November 21, 1996 No. 129-FZ “On Accounting”. To record incoming materials, a primary document has been installed. This is a receipt order in form No. M-4 (approved by Resolution of the State Statistics Committee of Russia dated October 30, 1997 No. 71a). This document formalizes the receipt of materials in accordance with paragraph 49 of the Guidelines for accounting of inventories (approved by order of the Ministry of Finance of Russia dated December 28, 2001 No. 119n).

But there is another simplified option for processing incoming materials. Instead of a receipt order, their acceptance and posting can be formalized by affixing a stamp on the supplier’s document (invoice, invoice, etc.). The stamp imprint must contain the same details as in the receipt order. That is, the details of the specified stamp are filled in and the next receipt order number is entered. Such a stamp is equivalent to a receipt order.

So, the procedure for documenting the operation to obtain materials is clearly established. Now let's look at the situation when goods arrive at the organization.

Is it necessary to fill out form No. M-4 in this case, or is an invoice from the supplier sufficient for the receipt of goods?

...aka - for goods For organizations that, in addition to trade, conduct other types of activities, operations for the acceptance and posting of goods are formalized in a similar manner as materials. This is provided for in paragraph 224 of the Guidelines for accounting of inventories. Such organizations include, for example, a manufacturing enterprise that includes a trading division. Therefore, when goods arrive at this department, a receipt order must be drawn up in Form No. M-4 or a stamp must be placed on the documents received from the supplier. Please note: this procedure does not apply to organizations that conduct exclusively trading activities.

As we have already noted, paragraph 1 of Article 9 of the Federal Law of November 21, 1996 No. 129-FZ states that all operations “must be documented with supporting documents.” From the literal interpretation of this norm it follows that the buyer must himself draw up a primary document according to which he capitalizes the received values. This will be the receipt order in form No. M-4. It indicates the date of receipt, the number of valuables and other mandatory details (Article 9 of the Federal Law of November 21, 1996 No. 129-FZ). And a bill of lading in form No. TORG-12 cannot replace a receipt order when goods arrive at a division of a company. Despite the fact that the second copy of this document received from the supplier is the basis for recording the received values.

Therefore, when goods arrive at the trading department, you need to draw up a receipt order in form No. M-4. If this document is not available, during the audit, tax authorities may file claims not only for the lack of primary documents, but also deduct input VAT.

With a fine and without deducting VAT. The absence of primary documents is equated to gross violations of the rules for accounting for income and expenses and objects of taxation (clause 3 of Article 120 of the Tax Code of the Russian Federation). According to this provision of the code, the fine ranges from 5 to 15 thousand rubles. If the tax base is underestimated, then the amount of sanctions is equal to 10 percent of the amount of unpaid tax, but not less than 15 thousand rubles.

The last option of punishment is due to the fact that tax accounting is based on data from primary accounting documents (Article 313 of the Tax Code of the Russian Federation). Capitalization of received materials or goods without drawing up a receipt order may be considered as an understatement of the income tax base.

In addition, the absence of a receipt order in Form No. M-4 may result in a refusal to deduct input VAT on purchased materials or goods (if the department receives them). For them, the tax is deducted if an invoice is received from the supplier, and the inventory items are paid for, accepted for accounting and will be used in transactions subject to VAT (clause 2 of Article 171, clause 1 of Article 172 of the Tax Code of the Russian Federation).

For each business transaction, primary accounting documents are drawn up. In this case, the documents must be drawn up according to the forms contained in the albums of unified forms of primary accounting documentation. If the album does not contain the required form, the primary document must contain the required details. After the documents are prepared, they are accepted for accounting (Article 9 of the Federal Law of November 21, 1996 No. 129-FZ). Only after this the transaction can be reflected in the accounting accounts. Consequently, the receipt of materials into the organization or goods into the trading division is reflected in the accounts only after a receipt order has been drawn up in Form No. M-4. From this moment on, the organization can take advantage of the deduction of input VAT provided that the remaining conditions for the offset are met. Oleg Gulst, UNP expert

/"Accounting, taxes, law", 06.12.2005/

Requirements for placing an order

The M-4 receipt order form was developed by the State Statistics Committee and approved by the 1997 Resolution. This document records all receipts of materials that come to the organization from suppliers or from processing departments.

The order must be filled out by the financially responsible employee; this document is drawn up upon receipt of inventory materials for warehousing, as well as upon transfer of semi-finished products for use in production. The order must be drawn up in a single copy: this document specifies the quantity of materials received by the unit. One order can be issued for several types of incoming products if they are transferred to the enterprise by one supplier and delivered within one day.

The form can be filled out manually, but more often automated computer programs are used for this. Electronic filing saves time and ensures accurate records

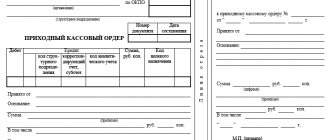

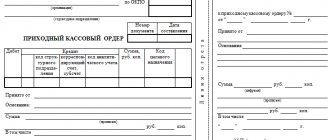

The procedure for filling out a cash receipt order

The cash receipt form is issued in one copy by an accounting employee and signed by the chief accountant or a person authorized to do so.

In this case, the receipt for the cash receipt order is signed by the chief accountant or a person authorized to do so, and by the cashier, certified by the seal (stamp) of the cashier.

What kind of document is this?

First of all, the form of this receipt order was approved by the State Statistics Committee of the Russian Federation in Resolution No. 71a of October 30, 1997. Today it is not mandatory for use, but its use is not prohibited by law.

In order to safely use the specified document for accounting purposes, you only need to approve it in.

This document formalizes the registration of materials that arrived at the enterprise from suppliers or from processing. It is worth noting that this form is used only when receiving materials for which there are no claims to their qualitative or quantitative content, i.e. if the actual data corresponds to the documents from the supplier. This is stated in paragraph 49 of the Methodological Instructions of the Ministry of Finance of the Russian Federation (order No. 119n dated December 28, 2001).

Warrant M-4 serves as the basis

warehouse, tax and accounting of materials.

In particular, paragraph 1 of Article 9 of Law No. 402-FZ states that all facts of economic activity must be documented in primary documents. Thus, the receipt order M4 serves as confirmation of the acceptance (!) of assets for accounting

. It is filled out based on the actual amount of material assets accepted and on the basis of the primary documentation accompanying them.

In addition, the preparation of this document performs another function - it serves as recognition of the supply of materials without claims against the supplier (processor).

Who can sign the document

Certification of the order with the signature of an authorized person is a mandatory requirement. Moreover, the signature of the financially responsible employee who has the right to accept the goods is affixed. If such a person is absent, the authority is transferred to another employee. In case of a long absence (business trip, vacation, etc.), a power of attorney may be drawn up to perform such actions.

The document is considered finally accepted after the signature is placed. Accordingly, no corrections can be made to it after this. And at the time of signing, all empty columns must be crossed out. Even small amendments will lead to the order becoming invalid, so a new one will have to be drawn up.

After this, the operation is reflected in the accounting documents, and the document itself is sent to the archive and is provided only at the request of the inspectors.

Application of this order

As stated earlier, receipt order M4 is used to register

materials, which include:

- various raw materials;

- purchased semi-finished products;

- materials (basic and auxiliary);

- components and spare parts;

- fuel and containers;

- construction materials, and other similar assets, which, on the basis of PBU No. 5/01 “Accounting for inventories”, are recognized as materials.

However, form M-4 is used not only when materials arrive at the enterprise from a supplier (i.e., and for other reasons) or from processing.

With the help of such a receipt order, assets are registered

, which:

- came as a contribution from the founders to;

- joined the organization free of charge;

- purchased by an accountable person;

- manufactured in-house;

- identified during the audit as surplus, etc.

In other words, for any reason for the receipt of materials, an M-4 order must always be issued! But only if there are no discrepancies in their quality and quantity.

As for the application of this document at enterprises, it can be used by legal entities of any form of ownership and legal form, including budgetary structures. But entrepreneurs decide for themselves whether to use the M-4 order in accounting or not. The fact is that Resolution of the State Statistics Committee of the Russian Federation No. 71a dated October 30, 1997. applies only to organizations. This normative act does not apply to entrepreneurs. But if they decide to use the document to simplify tax accounting or for warehouse accounting purposes, then they should approve the use of the specified form in the Order.

If you have not yet registered an organization, then the easiest way is

This can be done using online services that will help you generate all the necessary documents for free: If you already have an organization and you are thinking about how to simplify and automate accounting and reporting, then the following online services will come to the rescue and will completely replace an accountant at your enterprise and will save a lot of money and time.

All reporting is generated automatically, signed electronically and sent automatically online. It is ideal for individual entrepreneurs or LLCs on the simplified tax system, UTII, PSN, TS, OSNO. Everything happens in a few clicks, without queues and stress. Try it and you will be surprised

how easy it has become!

Filling out the receipt order form M-4

Form M-4 was approved by Decree of the State Statistics Committee of the Russian Federation dated October 30, 1997 No. 71a. The form is double-sided and includes information about the seller company, the buyer and the product being purchased.

First you need to fill out the header of the document. Enter the serial number of the M-4 form, according to the company’s internal document flow. Then fill in the name of the purchasing company in full, indicating the organizational and legal form, OKPO code and structural division of the company.

The first page of Form M-4 contains 2 tables. The first table contains the following information:

- date of filling out the form;

- transaction type code;

- name of the warehouse;

- information about the supplier: name and code;

- information about the insurance company;

- Correspondent account data: account, subaccount and analytical accounting code;

- document data: number of accompanying and payment document.

The second table contains detailed data about the incoming goods. It includes 12 columns:

- name of the value, its characteristics: color, grade, etc.

- item number of value;

- then the code of the unit of measurement is indicated;

- name of the unit of measurement;

- number of values according to documents;

- the number of values actually accepted;

- price of goods received in form M-4;

- amount in rubles excluding VAT;

- VAT amount;

- amount including VAT;

- passport ID;

- number in order according to the warehouse card index.

The table contains quite a lot of rows. Unfilled lines must be crossed out - for example, crosswise.

The last line of the receipt order table f.M-4 summarizes the total data on the quantity of goods, the price of goods (cost excluding value added tax, VAT amount, total amount, which includes tax).

The document is signed by the responsible employee who accepted the goods - the position of the receiver and the transcript of the signature are indicated. And the responsible employee who handed over the goods - also indicating the position and decoding of the signature.

The receipt of material assets at the company's warehouse may be accompanied by the execution of a receipt order of the standard form M-4. This form will be transferred to the accounting department as a basis for making the necessary entries to accept materials for accounting.

The receipt form is filled out at the warehouse upon receipt of material assets from the supplier. If several batches of materials are received from the same supplier in one day, then all of them can be reflected in one M-4 form.

General drafting rules

When receiving several types of material using one invoice, you can create one receipt order. But the main thing is to draw up the document correctly.

To do this, you need to know what information is required to be provided:

| Code by type of operation | You only need to enter the code if the receiving party has a classifier for the types of operations. If there is no such classifier, a dash is placed in this line |

| Code by supplier | This code is indicated if the economic entity has a classifier for supplier codes. The absence of a classifying document requires a dash to be placed in this line |

| Insurance organization | The name of the insurance company that insured the received object is written here. If there is no insurance, a dash is indicated |

| Number value of the accompanying document | The number of the document on the basis of which the materials were credited is indicated. This may be an invoice from the supplier or a delivery note |

| Number corresponding to the payment document | Write down the number of the document according to which the materials were paid for. This may be considered a payment request or order |

| Price (7 columns) | The cost value for one unit of the accepted object is written down, excluding VAT. |

| VAT amount (9 columns) | The VAT amount is shown for the entire volume of products received |

| Passport number (11th column) | This column is filled in when accepting precious stones or metals, for which a special passport is a necessary accompanying document. |

| Serial number according to the warehouse card file (12 columns) | The number value of the materials registration card according to the M-17 form is written here |

Filling out the “header” and first table of form M-4

The first table is the “header” of the document. First, it indicates the order number for the company’s internal document flow. Then enter the name of the organization receiving the goods, indicating its legal form (IP, LLC, OJSC, CJSC), the OKPO code (All-Russian Classifier of Enterprises named after Organizations - the code is contained in the constituent papers of the company), as well as (if necessary) the structural unit , which issues the order.

Next, the table includes the date the document was compiled, the transaction type code (if such coding is used), the supplier’s warehouse number, its full name, code (if any) and the insurer (if the inventory items are insured). Then the accounting account numbers, analytical accounting code (if such a system is used), and the numbers of the accompanying and payment documents are indicated here.

Filling out the second table of form M-4

The second table of the receipt order relates directly to incoming products . First, the name of the product and its item number are indicated, then the unit of measurement: its code - in accordance with the Unified Classifier of Units of Measurement, and the name (pieces, kilograms, cubes, meters, etc.). Next, information is entered on the number of accepted inventory items (according to documents and actually) - they must match.

After this comes information about the cost: in the seventh column the price per piece is entered, then the total cost excluding VAT, then the allocated VAT, and then the total price including VAT. The passport number is indicated if inventory items have this accompanying document (for example, jewelry). Lastly, the card number according to the warehouse card index is entered into the table.

Filling out the reverse side of the M-4 form

The reverse side of the document summarizes the receipt : the total quantity of goods received, its total cost excluding VAT, the amount of VAT and the cost including VAT. There is no need to decipher the amounts in writing.

Finally, the receipt order must be signed by the direct recipient of the goods (in this case, the storekeeper) and the supplier’s representative (in this case, the forwarder) with a mandatory decoding. There is no need to certify the order with a seal, because Since 2016, legal entities may not have their documents stamped.

Who signs the order

The completed receipt order M-4 must be certified by a signature. Only the person who is financially responsible and who directly accepts the materials received by the organization has the right to sign.

Once the order is signed, it is not permissible to make changes to the items on the form. A document with corrections will be considered invalid.

After the receipt order is properly executed and the business transaction is taken into account in accounting, the document is sent for archival storage.

The tax authority may request it during an inspection. Therefore, receipt orders should be stored in the manner prescribed for preserving primary accounting documentation.

2022 sample

This year, the form of the document has not changed at all compared to the previous year. An order in form M-4 is drawn up as shown in the figure:

- The document number is written (in the center).

- Then - the full name of the organization, as well as the structural unit.

- The corresponding OKPO code is written in the right corner.

- In the first table, all columns are filled in - date of arrival, code, warehouse number, information about the supplier and insurance company, the corresponding account, as well as the numbers of the accompanying and payment documents.

- The main table indicates all the data about the arrived product - name, how many pieces, amount with and without VAT, total amount.

- All empty lines are crossed out.

| column name | filling rules |

| name of the company or structural unit | The full name of the company or individual entrepreneur at whose disposal the relevant goods or raw materials for production was received is indicated. It is important to indicate the name in full, as it appears in official documents, for example Limited Liability Company “Proxy” or Individual Entrepreneur Alexander Pavlovich Bondarenko. In the structural unit column we mean the internal department of the enterprise. Usually it is written as “warehouse”. |

| supplier information | The name of the supplier is written here as it is specified in the contract (abbreviations IP, LLC, etc. are allowed). Document numbers are transferred from the payment and accompanying document respectively. |

| account information | Details of the bank account on the basis of which funds are credited are provided. Accounting entries are also made for the same account. |

| information about goods received from the supplier | Basic information is a complete list of information about goods, raw materials, semi-finished products and other valuables that were received from the supplier. Enter the number, full name, parameters, grade, brand, in what units the goods are measured, and the quantity in these units. The cost per unit is indicated, which must exactly correspond to the contract. The cost without VAT is given, then the VAT itself for each product, after which the total cost is filled in. It is the receiving party that sends it to the supplier. |

| code by type of operation | This option does not always fit. It should be recorded only if the company has installed a special classifier that takes into account various business transactions. If this document is not maintained, it is permissible to simply put a dash. |

| supplier code | Here the situation is the opposite. This code is affixed in accordance with the classification of business transactions adopted by the organization that supplied the goods or raw materials. If such a document is not maintained, a dash is again added. |

| Insurance Company | In some cases, the supplier or receiving party insures the goods against various risks. Accordingly, in this case you need to write the full name of the insurance company, as it is indicated in the contract. If the goods were not insured, a dash is placed. |

| number of the accompanying document | In most cases, the accompanying document is the invoice for the goods. This can be either the actual invoice for the goods, or a consignment note, which, among other things, provides information about the delivery route. In this column you only need to enter the invoice number |

| payment document number | The document number confirming the fact of payment is indicated here. This is an order or requirement. |

| column 12 | The card number is entered in accordance with how it is described in form M-17 |

If precious metals and/or products made from them are being accepted, column 11 is also filled out in the table, which indicates the number of the technical passport for each unit of goods.

The form and example of a completed receipt order are presented below.

The accountant is not required to print out the receipt order. It’s enough to simply compose it in the 1C program. You can do without a paper form of the document if acceptance and posting are formalized on the invoice or invoice of the supplier of the goods. A stamp is placed and its details are filled in, which are considered an analogue of the receipt.

How to fill out a receipt order? Basic Steps

Each order, which records the receipt of inventory items at the enterprise, must be numbered, and a date must be put on the document. The following main filling stages can be listed:

- Indication of the full name of the enterprise. His legal name is also stated. address and necessary contact information.

- The structural unit of the organization to which material assets are transferred is indicated.

- In the table you must enter the date of the transaction code, the name of the inventory, and the name of the supplier. If the company uses supplier coding, the corresponding code is indicated, and if not, a dash is added.

- The insurance company is indicated if the material assets were insured during the transfer. If this has not been done, you need to put a dash in the column.

- Next, accounts for accounting are written down, as well as details of accompanying documents.

After this, you need to fill out separate fields that contain detailed information about the product. The name of material assets, item number, unit of measurement, quantity, cost excluding VAT, and the amount of VAT are indicated. If materials of high value are transferred, for example, precious stones, the data of the product passport must be indicated. In column 12 you must enter the serial number according to the warehouse card file.

After the table in the order, the total amounts are indicated; in empty columns you need to put dashes. The M4 order must bear the signatures of the supplier’s representative who provides the materials and the receiving financially responsible employee. After registration, the order is redirected to the accounting department for accounting and control.

Filling out the M-4 receipt order allows you to ensure control of all incoming materials, semi-finished products and other material assets, as well as control cooperation with suppliers. Maintaining documentation in accordance with all the rules allows you to avoid the loss of material assets or excessive payments to the supplier.

Stamp instead of a receipt order

In some cases, instead of a receipt order, the storekeeper may use a stamp. This can be done if goods arrive at the warehouse based on an invoice, act, or sales receipt. A sample stamp instead of an M-4 receipt order will contain the following fields to fill out: date, receipt order number, company name, data of the receiving party. The stamp in this case will contain the same details as in the M-4 receipt order. There is no point in adding details to the stamp that will reflect the quantity of goods received. It is worth keeping in mind that you can put a stamp on an incoming document if the document does not contain corrections and the quantity of goods received corresponds to what is indicated in the documents.

If, upon receiving inventory items, a warehouse employee understands that the declared quantity of goods differs from the quantity that actually arrived at the warehouse, or the quality of the goods does not meet the requirements for them (for example, the goods arrived with damage, scratches, dents, etc. .), then an act of acceptance of materials should be issued. For example, in this case, you can use the unified form No. M-7.

2022 sample

This year, the form of the document has not changed at all compared to the previous year. An order in form M-4 is drawn up as shown in the figure:

- The document number is written (in the center).

- Then - the full name of the organization, as well as the structural unit.

- The corresponding OKPO code is written in the right corner.

- In the first table, all columns are filled in - date of arrival, code, warehouse number, information about the supplier and insurance company, the corresponding account, as well as the numbers of the accompanying and payment documents.

- The main table indicates all the data about the arrived product - name, how many pieces, amount with and without VAT, total amount.

- All empty lines are crossed out.

A detailed explanation of all columns is presented in the table.

| column name | filling rules |

| name of the company or structural unit | The full name of the company or individual entrepreneur at whose disposal the relevant goods or raw materials for production was received is indicated. It is important to indicate the name in full, as it appears in official documents, for example Limited Liability Company “Proxy” or Individual Entrepreneur Alexander Pavlovich Bondarenko. In the structural unit column we mean the internal department of the enterprise. Usually it is written as “warehouse”. |

| supplier information | The name of the supplier is written here as it is specified in the contract (abbreviations IP, LLC, etc. are allowed). Document numbers are transferred from the payment and accompanying document respectively. |

| account information | Details of the bank account on the basis of which funds are credited are provided. Accounting entries are also made for the same account. |

| information about goods received from the supplier | Basic information is a complete list of information about goods, raw materials, semi-finished products and other valuables that were received from the supplier. Enter the number, full name, parameters, grade, brand, in what units the goods are measured, and the quantity in these units. The cost per unit is indicated, which must exactly correspond to the contract. The cost without VAT is given, then the VAT itself for each product, after which the total cost is filled in. It is the receiving party that sends it to the supplier. |

| code by type of operation | This option does not always fit. It should be recorded only if the company has installed a special classifier that takes into account various business transactions. If this document is not maintained, it is permissible to simply put a dash. |

| supplier code | Here the situation is the opposite. This code is affixed in accordance with the classification of business transactions adopted by the organization that supplied the goods or raw materials. If such a document is not maintained, a dash is again added. |

| Insurance Company | In some cases, the supplier or receiving party insures the goods against various risks. Accordingly, in this case you need to write the full name of the insurance company, as it is indicated in the contract. If the goods were not insured, a dash is placed. |

| number of the accompanying document | In most cases, the accompanying document is the invoice for the goods. This can be either the actual invoice for the goods, or a consignment note, which, among other things, provides information about the delivery route. In this column you only need to enter the invoice number |

| payment document number | The document number confirming the fact of payment is indicated here. This is an order or requirement. |

| column 12 | The card number is entered in accordance with how it is described in form M-17 |

If precious metals and/or products made from them are being accepted, column 11 is also filled out in the table, which indicates the number of the technical passport for each unit of goods.

The form and example of a completed receipt order are presented below.

NOTE. The accountant is not required to print out the receipt order. It’s enough to simply compose it in the 1C program. You can do without a paper form of the document if acceptance and posting are formalized on the invoice or invoice of the supplier of the goods. A stamp is placed and its details are filled in, which are considered an analogue of the receipt.

Actions of the cashier after receiving funds

After this, the cashier accepts the money and, after receiving it, puts his signature, surname and initials on the receipt order and receipt.

On the receipt, the cashier also indicates the date the money was received and certifies his signature with a seal. The receipt is stamped so that the edge overlaps the receipt order itself

After the money arrives at the cash register, the cashier tears off the receipt for the PKO along the cut line and hands it to the person who handed over the money, and leaves the cash order at the cash register.

Journal of registration of incoming and outgoing cash documents

Before an incoming cash order reaches the cash desk, it must be registered in the register of incoming and outgoing cash documents (Form No. KO-3).

Journal of registration of cash documents KO-3 - is intended for registration of cash documents in the course of conducting cash transactions and is used for registration by the accounting department of incoming and outgoing cash orders.

Form No. KO-3 consists of a cover and a loose leaf, according to which all pages of the magazine are designed, filled out and printed.

The insert sheet is divided into two parts: one is intended for registering incoming cash documents (columns 1-4), the other - for expenses (columns 5-8).

Penalties for lack of PCO

The absence or improper execution of primary cash documents, which, in particular, include a cash receipt order, may result in penalties for the taxpayer in accordance with Art. 120 of the Tax Code of the Russian Federation.

So, according to this article, a gross violation of the rules for accounting for income and (or) expenses and (or) objects of taxation, if these acts were committed during one tax period, in the absence of signs of a tax offense, entails a fine of ten thousand rubles.

At the same time, a gross violation of the rules for accounting for income and expenses and taxable items means the absence of primary documents, including primary cash documents.

Also, the absence of primary cash documents from the purchasing organization may become the basis for the refusal of the tax authority to recognize the specified expenses of the organization for the purposes of taxation of profits or a single tax in accordance with the simplified taxation system (the object of taxation is income reduced by the amount of expenses incurred).