Cash register in law

As the law states, all individual entrepreneurs who sell goods or provide services for cash or by accepting payments through bank cards are required to have and use cash registers when making payments to clients. This rule applies mainly to those business representatives who conduct business with the public, since it is citizens who pay for goods and services using cash or bank cards.

The absence of a cash register for an entrepreneur is possible if he carries out financial transactions using non-cash transfers to the bank accounts of legal entities or other individual entrepreneurs.

Requirements for cash register equipment

The law establishes a number of requirements that cash register machines must meet.

- all cash registers used in commercial activities must be registered with the tax office at the place of residence of the individual entrepreneur;

- Only those models of cash register equipment that are listed in the state register are suitable for use. You can make sure that a particular cash register is in the register in two ways: either by checking the holographic sticker with the necessary information when purchasing, or by independently studying the list of state registrations. register on the official website of the tax service.

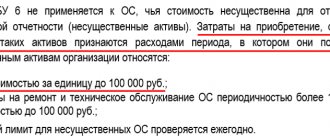

Please note the file:

Attention! Each cash register machine prints receipts with certain details, depending on the type of activity. Therefore, before choosing one or another cash register, you need to make sure that it is suitable for the work of this individual entrepreneur.

Important! In addition to cash registers, there are check printing machines. These devices are not considered cash register equipment by tax authorities, since they do not have an EKLZ memory unit. Receipt printing machines are used in their work mainly by those entrepreneurs who work on UTII.

Requirements for an online cash register for the simplified tax system

The online cash register used by individual entrepreneurs and legal entities must comply with the requirements set out in Art. 4 of the Federal Law of May 22, 2003 No. 54-FZ:

- there is a case and a serial number on it;

- inside the case there is a real-time clock, a device for printing fiscal receipts and software and hardware necessary to comply with Federal Law;

- verification of the control number of the cash register registration number is ensured;

- it is possible to install a fiscal drive inside the case;

- fiscal data is transferred to the fiscal drive;

- fiscal receipts are generated electronically;

- it is possible to print QR codes measuring at least 20x20 mm;

- there is a technical capability to receive confirmation from the fiscal data operator;

- there is a function to inform the user about the lack of confirmation from the operator and about a malfunction of the cash register;

- there is a function to print a report on the current state of calculations;

- there is a function to search and print a receipt recorded in the drive by its number;

- The cash desk executes information exchange protocols.

For persons selling labeled goods, the cash register requirements are even more extensive (Clause 1.1, Article 4 of Federal Law No. 54-FZ of May 22, 2003).

The requirements for an online cash register are the same for everyone. They do not depend either on the taxation system or on the organizational and legal status.

Where to buy a cash register

Cash register machines are not sold in regular stores. Their sales and servicing are carried out by special organizations that have passed the State Expert Commission on Cash Register. These companies sell cash registers both at their head offices and through an extensive retail network. At the same time, they sell not only new cash registers, but also used ones.

It should be noted that those cash register models that have already been in use must be deregistered with the tax office and have a new EKLZ unit.

How to benefit from switching to online cash registers

Online cash registers help the tax office keep track of payments via the Internet. They are useful for business for the same reason: the director can go on vacation and understand what is currently happening at the outlet. In the OFD personal account, you can see whether employees have opened a shift and how much money comes from customers. For example, look at the demo version of Kontur.OFD.

For trading, online cash registers are useful in conjunction with goods accounting services. The entrepreneur checks out the goods at the checkout and the service automatically updates the balances. Therefore, it is always clear how many products are in the store and which ones it is time to order. And also which products help a business flourish, and which ones lie on the shelves for too long. For example, similar opportunities are available in the goods accounting service of Kontur.Market.

Individual entrepreneur cash register under simplified tax system

An individual entrepreneur who has opted for a simplified taxation scheme when making cash payments to clients must have a cash register. In cases where the buyer or consumer of individual entrepreneur services makes payments through bank debit or credit cards, it is also necessary to issue cash receipts.

Exceptions:

- cash register equipment may not be used if an individual entrepreneur-"simplified" works only through non-cash bank transfers to the settlement accounts of legal entities and other individual entrepreneurs;

- an individual entrepreneur works in a remote or hard-to-reach area where the use of cash registers is impossible for some reason;

- When providing certain types of services to the population, there is a statutory right to replace cash receipts with the issuance of strict reporting forms.

Fines for not using online cash registers

The amount of the fine does not depend on the taxation system, but the amount is different for individual entrepreneurs and legal entities. Failure to use the cash register will result in a fine under Art. 14.5 Code of Administrative Offenses of the Russian Federation:

- 25-50% of revenue received without using an online cash register, but not less than 10,000 rubles - for officials and individual entrepreneurs;

- 75-100% of revenue received without using an online cash register, but not less than 30,000 rubles.

When calculating the amount of the fine, all cash and non-cash receipts that were processed without an online cash register will be taken into account.

A repeated violation, provided that the turnover “past the online cash register” exceeded 1 million rubles, will lead to suspension of activities for up to 90 days or disqualification of the official for a period of 1-2 years.

For the use of a cash register that does not comply with the requirements of the Law, a fine is provided under paragraph 4 of Art. 14.5 Code of Administrative Offenses of the Russian Federation:

- 1,500 - 3,000 rubles - for officials and individual entrepreneurs;

- 5,000 - 10,000 rubles - for legal entities;

- a monetary fine may be replaced by a warning.

Checking the cash register (test purchase) is not an on-site tax audit. The Federal Tax Service can conduct purchases and issue fines on a daily basis. Therefore, it is in the interests of the company to use the cash register and ensure that all requirements are met.

Individual entrepreneur cash register for UTII

Those individual entrepreneurs who have switched to UTII have the right not to use a cash register. Instead, if the buyer or consumer of services requests, he must be issued either a strict reporting form, or a sales receipt, or a receipt. Moreover, each of these documents must contain strictly established information:

- the name of the document itself - receipt, BSO or sales receipt;

- basic data: serial number and date of issue of the document to the client, initials of the individual entrepreneur; his TIN;

- name of goods and services and their quantity;

- full payment amount;

- required: position and full name of the employee who issued the document with his signature.

Many individual entrepreneurs located on UTII use the check printing machines already mentioned above to print such documents. Since they do not need to be registered with the tax authorities, this is especially convenient for entrepreneurs who are on UTII.

Attention! Even in cases where the use of cash register equipment is not a legal obligation of an entrepreneur, he can acquire it on a voluntary basis, for example, to control sellers. In this case, there is no need to register the cash register with the tax office.

General exceptions

Regardless of what taxation system an individual entrepreneur is in, in some cases he has the right not to use cash registers. For example, the use of a cash register is not necessary if the entrepreneur is engaged in :

- sale of periodical printed products: magazines and newspapers;

- sale of travel cards and coupons for public transport;

- sale of lottery tickets;

- sale of securities;

- retail sale of soft drinks on tap and ice cream;

- sale of religious items;

.

In these and a number of other cases, specified in detail in the law of the Russian Federation, entrepreneurs have the right not to use cash register equipment.

Exemption from online cash registers for the simplified taxation system “Income” and “Income minus expenses”

Not all individual entrepreneurs and LLCs using the simplified tax system “Income” and the simplified tax system “Income minus expenses” are required to use cash registers. The following services and activities are exempt from the use of online cash registers (Article 2 of the Federal Law No. 54-FZ of May 22, 2003):

- sale of newspapers, magazines and related products at kiosks, provided that the share of sales of magazines and newspapers is at least 50%, and the range of related products is approved by the executive authority of the Russian Federation; at the same time, accounting for revenue from the sale of newspapers and accompanying goods must be kept separately;

- sale of securities;

- providing meals to students and employees of educational organizations during their studies;

- trade at markets, fairs, exhibitions, except for sales in stores, pavilions and counters located in these places;

- peddling trade in goods, except for technically complex goods and food that require special conditions for storage and sale;

- sale of ice cream in kiosks and bottling of soft drinks, milk and water;

- sales of kvass, milk, vegetable oil, live fish, kerosene from tank trucks;

- seasonal hawking of vegetables;

- shoe repair and painting;

- production and repair of metal haberdashery and keys;

- supervision and care of children, the sick, the elderly and disabled;

- sale of folk arts and crafts;

- plowing gardens and sawing firewood;

- porter services at railways, cars, air terminals, airports, sea and river ports;

- sales through mechanical vending machines without power supplies;

- provision of parking spaces for a fee, provided that the proceeds go to the budget;

- services of state and municipal libraries (the list of paid services provided without cash register is approved by the Decree of the Government of the Russian Federation);

- retail sale of shoe covers;

- sale of tickets and subscriptions to theaters belonging to state or municipal institutions (with the exception of sales via the Internet);

- sale of religious items and provision of services for religious ceremonies;

- leasing of residential premises owned by individual entrepreneurs and so on.

To use the online cash register, you need the Internet. But it is not found in all places in vast Russia. Therefore, companies and entrepreneurs operating in remote locations without communications use online cash registers in a mode that does not require the mandatory transfer of fiscal documents to the tax authorities. Individual entrepreneurs and LLCs operating in a similar regime operate on the territory of military units, facilities of the FSB, state security and foreign intelligence agencies (clause 7 of Article 2 of the Federal Law of May 22, 2003 No. 54-FZ).

The online cash register may not be used by pharmacies in village paramedic and paramedic-obstetric centers, and separate divisions of medical organizations licensed for pharmaceutical activities (Clause 5 of Article 2 of the Federal Law of May 22, 2003 No. 54-FZ).

A complete list of activities that give the right to exemption from the use of online cash registers is listed in Art. 2 Federal Law dated May 22, 2003 No. 54-FZ.

Self-employed individual entrepreneurs are exempt from using CCT.

LLCs and individual entrepreneurs on the simplified tax system do not use online cash registers when selling goods through an agent. However, the agent himself, when further selling goods to individuals, must use cash register systems.

Entrepreneurs and companies do not use online cash registers when making payments between legal entities and individual entrepreneurs, since payment between them occurs through a bank account.

Table of application of cash registers depending on the taxation system

| Tax system | Kind of activity | KKM is required | BSO can be issued | You can issue a sales receipt or |

| BASIC | Trade and other | + | ||

| Providing services to the public | + | |||

| simplified tax system | Trade and other | + | ||

| Providing services to the public | + | |||

| Unified agricultural tax | Trade and other | + | ||

| Providing services to the public | + | |||

| UTII | Trade and other | + | ||

| Providing services to the public | + | |||

| PSN | Trade and other | + | ||

| Providing services to the public | + |