What are fixed contributions and why are they no longer fixed?

Fixed contributions were insurance contributions for compulsory pension insurance and compulsory health insurance paid by individual entrepreneurs, lawyers, notaries and other persons engaged in private practice.

Until 2014, defined contributions were truly fixed (set for the year) and the same for all persons paying them. Then amendments to the legislation came into force, changing the procedure for calculating contributions and, in fact, contributions ceased to be fixed, since part of the contributions depends on the income of the entrepreneur.

And from 2022, this name has been removed from regulatory documents. We will continue to call these contributions fixed for convenience and because the name is familiar to entrepreneurs.

Since 2022, the procedure for paying fixed insurance premiums is regulated by Chapter 34 of the Tax Code and contributions are paid not to extra-budgetary funds, but to the territorial tax inspectorates at the place of registration of the individual entrepreneur.

Sample payment order with KBK 18210202140061110160

Individual Entrepreneur Ivanov fills out a payment order for the transfer of ¼ of fixed contributions to compulsory pension insurance for the third quarter of 2022. He lives in Yekaterinburg (affects bank details).

Example of a payment order:

Work with payment orders in Kontur.Accounting to fill them out without errors and submit documents for payment faster. Accounting is integrated with the bank, so outgoing payment orders can be immediately sent to the bank, where all that remains is to sign them. And in the service you can calculate your salary, keep records and submit reports via the Internet. New users have a 14-day trial period to get acquainted with all the features of the service.

Who pays fixed fees

Contributions in a fixed amount are required to be paid by all individual entrepreneurs, regardless of the taxation system for individual entrepreneurs, business activities and the availability of income. In particular, if an individual entrepreneur works somewhere under an employment contract, and insurance premiums are paid for him by the employer, this is not a basis for exemption from paying contributions calculated in a fixed amount.

Since 2013, you can avoid paying fixed contributions for the following periods:

- conscription service in the army;

- the period of care of one of the parents for each child until he reaches the age of one and a half years, but not more than three years in total;

- the period of care provided by an able-bodied person for a group I disabled person, a disabled child or a person who has reached the age of 80 years;

- the period of residence of spouses of military personnel serving under contract with their spouses in areas where they could not work due to lack of employment opportunities, but not more than five years in total;

- the period of residence abroad of spouses of employees sent to diplomatic missions and consular offices of the Russian Federation, permanent missions of the Russian Federation to international organizations, trade missions of the Russian Federation in foreign countries, representative offices of federal executive authorities, state bodies under federal executive authorities or as representatives these bodies abroad, as well as to representative offices of state institutions of the Russian Federation (state bodies and state institutions of the USSR) abroad and international organizations, the list of which is approved by the Government of the Russian Federation, but not more than five years in total.

However, if entrepreneurial activity was carried out during the above periods, then contributions will have to be paid (clause 7 of Article 430 of the Tax Code of the Russian Federation).

What determines the size of contributions?

Until January 1, 2022, the amount of individual entrepreneur contributions depended on the minimum wage.

However, due to the fact that the minimum wage was increased to the subsistence level, individual entrepreneurs’ contributions were decided to be “delinked” from it, and starting in 2022, the fixed amount of contributions paid per year is indicated in the Tax Code.

Since 2014, the amount of fixed contributions also depends on the annual income of the individual entrepreneur, since if the income exceeds 300 thousand rubles during the year. it is necessary to charge another 1% contribution on the amount of income exceeding 300 thousand rubles.

Income is calculated as follows:

- Under OSNO - income accounted for in accordance with Article 210 of the Tax Code of the Russian Federation. i.e. those incomes that are subject to personal income tax (applies only to income received from business activities). When determining these incomes, expenses are taken into account (Resolution of the Constitutional Court of November 30, 2016 No. 27-P);

- Under the simplified tax system with the object of taxation, “income” is income taken into account in accordance with Article 346.15 of the Tax Code of the Russian Federation. Those. those incomes that are taxed under the simplified tax system (such income is indicated in column 4 of the book of income and expenses and is indicated in line 113 of the tax return under the simplified tax system);

- Under the simplified tax system with the object of taxation “income reduced by the amount of expenses” - income taken into account in accordance with Article 346.15 of the Tax Code of the Russian Federation. Those. those incomes that are taxed under the simplified tax system (such income is indicated in column 4 of the book of income and expenses and is indicated in line 213 of the tax return under the simplified tax system). However, there are decisions of courts, including the Supreme Court, that expenses can be taken into account. However, the Ministry of Finance still maintains that all income is taken to calculate contributions.

- Under the Unified Agricultural Tax - income accounted for in accordance with paragraph 1 of Article 346.5 of the Tax Code of the Russian Federation. Those. those incomes that are taxed under the Unified Agricultural Tax (such income is indicated in column 4 of the book of income and expenses and is indicated in line 010 of the tax return under the Unified Agricultural Tax). Expenses are not taken into account when determining income for calculating contributions;

- For UTII - the taxpayer's imputed UTII income, calculated according to the rules of Article 346.26 of the Tax Code of the Russian Federation. Imputed income is indicated in line 100 of section 2 of the UTII declaration. If there are several sections 2, then the income is summed up across all sections. When determining annual income, imputed income from declarations for the 1st-4th quarter is added up.

- With PSN - potential income, calculated according to the rules of Article 346.47 of the Tax Code of the Russian Federation and Article 346.51 of the Tax Code of the Russian Federation. Those. the income from which the cost of the patent is calculated.

- If an individual entrepreneur applies several tax systems at the same time, then the income from them is added up.

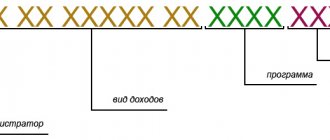

KBK 18210202140061110160: decoding for individual entrepreneurs

This code designation can be deciphered as follows:

- 182 – code designation of the payment administration operator, that is, in this case it is the Federal Tax Service;

- 1 – payment affiliation (1 – this is income, 2 – gratuitous deduction);

- 02 – digital designation of the receipt of contributions (02 – these are social);

- 02 — budget item/level (02 is regional or subject);

- 140 – sub-item of budget income;

- 06 – purpose of budget receipt or budget level (06 is the PFR budget). Other examples: 01 - federal, 02 - regional, and so on;

- 1110 – reason for expulsion. This combination of numbers means that deductions are related to the payment of insurance premiums;

- 160 – categorization of income (160 are insurance premiums). Other options: 110 - tax revenues and so on.

The purpose of the budget classification code in question when indicated in tax documents means that the individual entrepreneur’s contribution is deducted to the budget of the Pension Fund of Russia in the form of a fixed or additional payment (1%, if the entrepreneur’s income is more than 300 thousand rubles).

Return to content

Fixed Contribution Tariffs

IN 2020

The following tariffs apply

for payments to individual entrepreneurs “for themselves”

:

| Payers | Pension Fund, insurance part | FFOMS |

| Individual entrepreneurs (regardless of the taxation system), notaries, lawyers and other persons obligated to pay fixed fees | 22.0% (of which 6% is the joint part of the tariff, 16% is individual) | 5.1% |

Why do we need contribution rates if they are not calculated as a percentage of income for individual entrepreneurs? And how many pension points you will be awarded depends on the Pension Fund’s contribution rate.

KBK for personal income tax in 2022

| Personal income tax | Tax code | Code for penalty | Code for fine |

| paid by the tax agent | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| paid by entrepreneurs and persons engaged in private practice, notaries and lawyers (Article 227 of the Tax Code of the Russian Federation) | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| paid by the resident independently, including from income from the sale of personal property | 182 1 0100 110 | 182 1 0100 110 | 182 1 0100 110 |

| in the form of fixed advance payments from the income of foreigners who work on the basis of a patent | 182 1 0100 110 | – | – |

Calculation of contributions for incomes over 300 thousand rubles

If the income of the payer of insurance premiums for the billing period exceeds 300,000 rubles, in addition to the fixed pension contributions indicated above (32,448 rubles), contributions are paid in the amount of 1% of the income exceeding 300,000 rubles. Note! Health insurance premiums for incomes over 300 thousand rubles are not paid

! Those. The amount of contributions to the FFOMS is fixed for all individual entrepreneurs, regardless of the amount of annual income.

Example:

The income of an individual entrepreneur in 2022 was: 350,000 rubles. for activities subject to the simplified tax system and 100,000 rubles. for activities for which UTII is applied (how income is calculated is indicated above). Total 450,000 rub. The amount of contributions to the Pension Fund for 2022 will be 32,448 + (450,000 − 300,000) × 1% = 33,948 rubles. The amount of contributions to the FFOMS is 8,426 rubles.

The total amount of fixed insurance contributions to the Pension Fund for the year cannot be more than eight times the fixed amount of insurance contributions established for the year. Those. no more than 32,448×8 = 259,584 rubles.

Example:

The income of an individual entrepreneur using the simplified tax system in 2022 was: 30,000,000 rubles. The amount of contributions for 2022 would be 32,448 + (30,000,000 − 300,000) × 1% = 329,448 rubles, however, since it is greater than the maximum possible contributions of 259,584 rubles, 259,584 rubles are paid. contributions to the Pension Fund and contributions to the Federal Compulsory Medical Insurance Fund in the amount of 8,426 rubles.

BCC for contributions 2022 for individual entrepreneurs

others are indicated in the payment in 2022 . Namely:

| TYPE OF CONTRIBUTIONS | WHAT IS THE KBK IN 2022? |

| Pension contributions at the general rate. For which KBK individual entrepreneurs pay insurance premiums in 2022 at additional tariffs, you can see in the ConsultantPlus Ready Solution here. | 182 1 0210 160 Penalty: 182 1 0210 160 Fine: 182 1 0210 160 |

| Contributions for compulsory medical insurance | 182 1 0213 160 Penalty: 182 1 0213 160 Fine: 182 1 0213 160 |

| Contributions for VNIM | 182 1 0210 160 Penalty: 182 1 0210 160 Fine: 182 1 0210 160 |

| Contributions for injuries to the Social Insurance Fund | 393 1 0200 160 Penalty: 393 1 0200 160 Fines: 393 1 0200 160 |

have not changed compared to 2020 .

Due date for payment of contributions

Insurance premiums for the billing period are paid by individual entrepreneurs no later than December 31 of the current calendar year, with the exception of contributions in the amount of 1% on income exceeding 300 thousand rubles.

Insurance premiums calculated on the amount of income of the payer of insurance premiums exceeding 300,000 rubles for the billing period are paid by the payer of insurance premiums no later than July 1 of the year following the expired billing period.

Contributions (including contributions for compulsory health insurance) are paid from January 1, 2022 not to the Pension Fund, but to the tax office. Including contributions for previous years.

KBC for insurance contributions to the Pension Fund for employees for 2022 - 2023

For organizations and individual entrepreneurs that are employers of individuals and pay contributions to compulsory pension insurance, the following BCC will apply in 2022-2023:

| Payment type | KBK |

| Contribution to compulsory pension insurance | 18210202010061010160 |

| Penalty | 18210202010062110160 |

| Fines | 18210202010063010160 |

For organizations and individual entrepreneurs that are employers of individuals and pay contributions for compulsory health insurance, the following BCCs are valid in 2022 - 2023:

| Payment type | KBK |

| Compulsory health insurance contribution | 18210202101081013160 |

| Penalty | 18210202101082013160 |

| Fines | 18210202101083013160 |

ConsultantPlus experts explained what to do if the wrong BCC was mistakenly indicated on the payment. To do everything correctly, get trial access to the system and go to the Ready solution. It's free.

Since 2014, the state has frozen the funded part of the pension. The entire individual part of the insurance premium goes to finance the insurance pension (amendments to the Law “On Compulsory Pension Insurance” dated December 15, 2001 No. 167-FZ were introduced by the Law “On Amendments” dated December 14, 2015 No. 373-FZ).

Therefore, from 01/01/2014, employers pay the full insurance premium rate with one payment document according to the current BCC. If necessary, in accordance with paragraph 2 of Art. 13 of Law No. 167-FZ The Pension Fund independently distributes payment amounts between insurance and funded pensions based on personalized accounting data.

Read more about personalized accounting in the material “What is individual personalized accounting?” .