Tax offenses and liability for their commission are regulated by the Tax Code and the Code of Administrative Offenses of the Russian Federation, although prosecution under the Criminal Code is also possible (for significant violations that are recognized as crimes). In the article you will find information about the types of liability to which a violator may be held, and the dependence of the punishment chosen by the authorized body on various factors.

In mid-July 2022, “Clerk” will host a free webinar “Tax crimes: schemes, subsidies, tax reconstruction.” Sign up.

Tax offenses - concept and essence

A tax offense is a failure to comply with tax law by a person who has certain obligations to pay taxes.

The current Tax Code of the Russian Federation defines an exhaustive list of such violations (Chapter 16 of the Tax Code of the Russian Federation). In particular, these include:

- failure to comply with the procedure for registering with the Federal Tax Service as a taxpayer;

- failure to submit documents containing the calculation of the amount of mandatory payments, or failure to comply with the method of submitting them for verification;

- improper accounting of expenses incurred and income received, which caused a change in the size of the taxable base;

- non-payment (full or partial) of taxes;

- refusal to submit to the Federal Tax Service reports and other documentation necessary for tax authorities to perform supervisory functions.

IMPORTANT! The violator cannot be punished if more than 3 years have passed since the commission of the illegal act (in cases recorded in Articles 120 and 122 of the Tax Code of the Russian Federation - from the end of the tax period).

The grounds for recognizing an act as an offense and imposing a certain sanction on the culprit are:

- The presence of a legal norm that qualifies such an act as an offense.

- The fact that such an act has been committed.

- Availability of a documented decision of an authorized authority to punish the violator.

Persons who are responsible for tax offenses

Responsibility for committing tax offenses lies not only with organizations, but also with individuals, and the latter are not held accountable if they were under the age of 16 at the time of the violation of the law.

Sanctions for the violator, in accordance with Art. 107 of the Tax Code of the Russian Federation apply regardless of whether the offense was committed intentionally or through negligence. However, it is obvious that the punishment for intentional failure to comply with the requirements of the legislator will be more severe than for a violation committed accidentally.

The conditions that must be met when making a decision to apply sanctions to a citizen or organization are determined by Art. 108 Tax Code of the Russian Federation:

- The violator can be brought to justice only in the manner prescribed by law.

- Repeated prosecution of a person for the same violation is not permitted.

Types of liability for tax offenses

Liability for tax offenses depends on a number of factors, which must be assessed when deciding on the punishment applied to the taxpayer.

Moreover, the current Tax Code of the Russian Federation is not the only regulatory document establishing sanctions and the procedure for their application to the violator. The Code of Administrative Offenses and the Criminal Code of the Russian Federation also determine penalties for tax offenses. The division of illegal acts into different categories and the application of different types of liability to them is due to their diverse nature and the different amount of damage that their commission entails. That is why, in addition to tax liability for tax offenses, administrative and criminal liability may arise.

A violator can be brought to any of the listed types of liability only in court, and the type of court to which the tax authority applies depends on which category the taxpayer belongs to.

So, the claim is filed:

- to the arbitration court if the violator has the status of an individual entrepreneur or is an organization;

- to a court of general jurisdiction if the law was violated by an individual who is not an entrepreneur.

Penalties for tax offenses

According to paragraph 1 of Art.

114 of the Tax Code of the Russian Federation, the measure of responsibility is expressed in the imposition of a tax sanction on the guilty person. At the same time, paragraph 2 of the same article indicates that the sanction applied is the imposition of a monetary penalty on the culprit in the amount established by the Tax Code of the Russian Federation. Depending on the type of violation, fines may be as follows:

- For failure to comply with the registration procedure with the Federal Tax Service - up to 10 thousand rubles. (clause 1 of article 116 of the Tax Code of the Russian Federation).

- For conducting activities without registration - 10% of the income received, but not less than 40 thousand rubles. (clause 2 of article 116 of the Tax Code of the Russian Federation).

- For failure to submit reporting documents - 5% of the tax that should have been included in the declaration for each month of delay, but not more than 30% and not less than 1 thousand rubles. (Clause 1 of Article 119 of the Tax Code).

- For failure to comply with the method of submitting the declaration to the regulatory authority - 200 rubles. (Article 119.1 of the Tax Code of the Russian Federation).

- For failure to comply with accounting rules:

- one-time - 10 thousand rubles;

- committed over more than one tax period - 30 thousand rubles;

- which caused a downward change in the tax base - 20% of the amount of arrears, but not less than 40 thousand rubles. (Article 120 of the Tax Code of the Russian Federation).

- For non-payment (full or partial) of tax:

- unintentional - 20% of the amount of arrears;

- intentional - 40%.

- For failure to fulfill the duties of a tax agent - 20% of the amount of tax not withheld from the taxpayer.

What are violations of the tax code?

There are quite a lot of tax violations; let’s look at the most common ones, which happen at least once in the life of every company or entrepreneur.

The main violations are enshrined in Articles 116 – 126 of the Tax Code of the Russian Federation.

- Article 116 of the Tax Code of the Russian Federation talks about liability for violating deadlines when submitting an application for state registration.

- If the tax return was not submitted to the tax authority, then Article 119 of the Tax Code of the Russian Federation provides for liability for this.

- Article 119.1 regulates the filing of returns electronically.

- If a company or entrepreneur commits serious violations in the reflection of income, expenses or taxable items, then responsibility for such violations must be sought in Article 120 of the Tax Code of the Russian Federation.

- Understatement of the tax base and, as a consequence, non-payment of tax, is regulated in Article 122 of the Tax Code of the Russian Federation.

- The responsibility of tax agents for non-transfer of taxes to the budget is enshrined in Article 123 of the Tax Code of the Russian Federation.

- If, at the request of the tax inspectorate, the company does not provide documents or other data, then liability will arise in accordance with Article 126 of the Tax Code of the Russian Federation

Administrative liability for tax offenses

A description of tax offenses and liability for their commission is contained in the articles contained in Chapter.

15 Code of Administrative Offenses of the Russian Federation. At the same time, administrative liability, in accordance with the note to Art. 15.3 of the Code of Administrative Offenses of the Russian Federation, only officials who have violated the law as a result of failure to perform or improper performance of their official duties can be prosecuted. Individuals (including those with individual entrepreneur status) are subject to administrative liability for tax offenses under Art. 15.4–15.9 and 15.11 Code of Administrative Offenses of the Russian Federation are not involved. The most frequently committed offenses for which the law provides for administrative liability include:

- Failure to comply with reporting deadlines (Article 15.5 of the Code of Administrative Offenses of the Russian Federation). For this, the responsible person will have to pay from 300 to 500 rubles to the state budget. (in some cases, a warning may be issued instead of a fine).

- Failure to submit to the Federal Tax Service the documents necessary to carry out control (Article 15.6 of the Code of Administrative Offenses of the Russian Federation). In this case, the legal representative of the organization will have to pay from 300 to 500 rubles, an official of a government agency - from 500 to 1 thousand rubles.

- Improper accounting (Article 15.11 of the Code of Administrative Offenses of the Russian Federation). For such a violation, a fine in the amount of 5 to 10 thousand rubles is imposed on the responsible person. The same violation committed repeatedly is punishable by a monetary penalty in the amount of 10 to 20 thousand rubles. or deprivation of the right to work in the current position for a period of 1 to 2 years.

Responsibility for violation of tax laws

One of the stages of tax control is bringing to responsibility for committing a tax offense. Legal liability for violation of tax laws is a set of compulsory punitive measures applied to violators as punishment in the cases and manner established by the legislator.

The basis for applying liability measures is a tax offense. It is understood as a committed unlawful act of a taxpayer, tax agent and other persons, for which the Tax Code of the Russian Federation provides for liability. The rules on tax liability apply to both individuals and organizations. Tax liability has all the features of legal liability:

- is a means of law enforcement;

- consists in the application of measures of state coercion;

- comes for violation of legal norms;

- is a consequence of a criminal act;

- consists of applying sanctions.

Specific features of liability for tax offenses are:

- firstly, the establishment by law of only the judicial procedure for bringing to responsibility;

- secondly, regulating the application of liability by tax law;

- thirdly, a special subject of responsibility is the taxpayer.

Depending on the subjects, 3 types of liability are established:

1. Responsibility of the taxpayer for violation of the procedure for calculating and paying taxes - Chapter 16 of the Tax Code of the Russian Federation: violation of the deadline for registration with the tax authority; evasion of registration with the tax authority; violation of the deadline for submitting information about opening and closing a bank account; failure to submit a tax return; gross violation of the rules for accounting for income and expenses and objects of taxation; non-payment or incomplete payment of tax amounts; failure by the tax agent to withhold and (or) transfer taxes; failure to comply with the procedure for possession, use and (or) disposal of property that has been seized; failure to provide the tax authority with information necessary for tax control; unlawful failure to report information to the tax authority, Art. 15.3-15.6, 16.12, 16.22 Code of Administrative Offenses of the Russian Federation;

2. Responsibility of tax collectors for violation of the procedure for withholding and transferring taxes (Chapter 16 of the Tax Code of the Russian Federation, Article 15.6 of the Code of Administrative Offenses of the Russian Federation);

3. Responsibility of credit institutions for the duties provided for by the legislation on taxes and fees (Chapter 18 of the Tax Code of the Russian Federation: violation by the bank of the procedure for opening an account for a taxpayer; violation of the deadline for executing an order to transfer a tax or fee, Articles 15.7-15.10 of the Code of Administrative Offenses of the Russian Federation).

Failure by the bank to comply with the decision of the tax authority to suspend transactions on the accounts of the taxpayer, fee payer or tax agent; failure by the bank to comply with the decision to collect taxes and fees, as well as penalties; failure to provide tax authorities with information about the financial and economic activities of taxpayers who are bank clients.

By type, liability for violation of tax laws is classified into:

- administrative in accordance with the Code of Administrative Offenses of the Russian Federation[23] (Articles 15.3, 15.4, 15.5, 15.6, 15.7, 15.8, 15.9, 15.10, 16.12, 16.22);

- tax (financial) - the procedure and conditions for bringing to tax liability are established by Art. 108 of the Tax Code of the Russian Federation and provide for: the inadmissibility of bringing to tax liability other than in the manner prescribed by the Tax Code of the Russian Federation; the inadmissibility of repeated prosecution for the same offense; absence of signs of a criminal offense in the activities of an individual; the possibility of further administrative and criminal prosecution of officials of organizations after bringing the organization to tax liability; preservation of the taxpayer’s obligation to pay taxes and penalties when he is brought to tax liability; the person held accountable is innocent until proven otherwise.

A person is not subject to tax liability if

- there is no tax violation event;

- there is no guilt in committing an offense;

- the offense was committed by a person under 16 years of age;

- The statute of limitations for prosecution has expired (3 years) from the date of commission of the offense.

Responsibility for a tax offense is expressed in tax sanctions, which are established in the form of fines in the amounts determined by the Tax Code of the Russian Federation. If there is at least one mitigating circumstance, the amount of the fine is subject to reduction by at least 2 times. If there is an aggravating circumstance, it increases by 2 times.

The following are recognized as mitigating circumstances for committing tax offenses:

- commission of offenses due to a combination of difficult personal or family circumstances;

- committing offenses under the influence of threat or coercion, or due to financial, official or other dependence;

- other circumstances that may be recognized by the court as mitigating liability.

An aggravating circumstance is the commission of tax offenses by a person who was previously held accountable for a similar tax offense.

Tax authorities have the right to file a claim in court to collect a tax sanction no later than 6 months from the date of discovery of the tax offense and the drawing up of the corresponding act; Criminal liability is provided for in articles 198, 199, 199.1, 199.2 of the Criminal Code of the Russian Federation[24];

Responsibility of tax authorities. Tax authorities are responsible for losses caused to taxpayers as a result of their unlawful actions (decisions) or inaction, as well as unlawful actions (decisions) or inaction of officials. Losses caused to taxpayers are reimbursed from the federal budget. Officials bear responsibility in accordance with the Code of Administrative Offenses of the Russian Federation.

One of the stages of tax control is bringing to responsibility for committing a tax offense. Legal liability for violation of tax laws is a set of compulsory punitive measures applied to violators as punishment in the cases and manner established by the legislator.

The basis for applying liability measures is a tax offense. It is understood as a committed unlawful act of a taxpayer, tax agent and other persons, for which the Tax Code of the Russian Federation provides for liability. The rules on tax liability apply to both individuals and organizations. Tax liability has all the features of legal liability:

- is a means of law enforcement;

- consists in the application of measures of state coercion;

- comes for violation of legal norms;

- is a consequence of a criminal act;

- consists of applying sanctions.

Specific features of liability for tax offenses are:

- firstly, the establishment by law of only the judicial procedure for bringing to responsibility;

- secondly, regulating the application of liability by tax law;

- thirdly, a special subject of responsibility is the taxpayer.

Depending on the subjects, 3 types of liability are established:

1. Responsibility of the taxpayer for violation of the procedure for calculating and paying taxes - Chapter 16 of the Tax Code of the Russian Federation: violation of the deadline for registration with the tax authority; evasion of registration with the tax authority; violation of the deadline for submitting information about opening and closing a bank account; failure to submit a tax return; gross violation of the rules for accounting for income and expenses and objects of taxation; non-payment or incomplete payment of tax amounts; failure by the tax agent to withhold and (or) transfer taxes; failure to comply with the procedure for possession, use and (or) disposal of property that has been seized; failure to provide the tax authority with information necessary for tax control; unlawful failure to report information to the tax authority, Art. 15.3-15.6, 16.12, 16.22 Code of Administrative Offenses of the Russian Federation;

2. Responsibility of tax collectors for violation of the procedure for withholding and transferring taxes (Chapter 16 of the Tax Code of the Russian Federation, Article 15.6 of the Code of Administrative Offenses of the Russian Federation);

3. Responsibility of credit institutions for the duties provided for by the legislation on taxes and fees (Chapter 18 of the Tax Code of the Russian Federation: violation by the bank of the procedure for opening an account for a taxpayer; violation of the deadline for executing an order to transfer a tax or fee, Articles 15.7-15.10 of the Code of Administrative Offenses of the Russian Federation).

Failure by the bank to comply with the decision of the tax authority to suspend transactions on the accounts of the taxpayer, fee payer or tax agent; failure by the bank to comply with the decision to collect taxes and fees, as well as penalties; failure to provide tax authorities with information about the financial and economic activities of taxpayers who are bank clients.

By type, liability for violation of tax laws is classified into:

- administrative in accordance with the Code of Administrative Offenses of the Russian Federation[23] (Articles 15.3, 15.4, 15.5, 15.6, 15.7, 15.8, 15.9, 15.10, 16.12, 16.22);

- tax (financial) - the procedure and conditions for bringing to tax liability are established by Art. 108 of the Tax Code of the Russian Federation and provide for: the inadmissibility of bringing to tax liability other than in the manner prescribed by the Tax Code of the Russian Federation; the inadmissibility of repeated prosecution for the same offense; absence of signs of a criminal offense in the activities of an individual; the possibility of further administrative and criminal prosecution of officials of organizations after bringing the organization to tax liability; preservation of the taxpayer’s obligation to pay taxes and penalties when he is brought to tax liability; the person held accountable is innocent until proven otherwise.

A person is not subject to tax liability if

- there is no tax violation event;

- there is no guilt in committing an offense;

- the offense was committed by a person under 16 years of age;

- The statute of limitations for prosecution has expired (3 years) from the date of commission of the offense.

Responsibility for a tax offense is expressed in tax sanctions, which are established in the form of fines in the amounts determined by the Tax Code of the Russian Federation. If there is at least one mitigating circumstance, the amount of the fine is subject to reduction by at least 2 times. If there is an aggravating circumstance, it increases by 2 times.

The following are recognized as mitigating circumstances for committing tax offenses:

- commission of offenses due to a combination of difficult personal or family circumstances;

- committing offenses under the influence of threat or coercion, or due to financial, official or other dependence;

- other circumstances that may be recognized by the court as mitigating liability.

An aggravating circumstance is the commission of tax offenses by a person who was previously held accountable for a similar tax offense.

Tax authorities have the right to file a claim in court to collect a tax sanction no later than 6 months from the date of discovery of the tax offense and the drawing up of the corresponding act; Criminal liability is provided for in articles 198, 199, 199.1, 199.2 of the Criminal Code of the Russian Federation[24];

Responsibility of tax authorities. Tax authorities are responsible for losses caused to taxpayers as a result of their unlawful actions (decisions) or inaction, as well as unlawful actions (decisions) or inaction of officials. Losses caused to taxpayers are reimbursed from the federal budget. Officials bear responsibility in accordance with the Code of Administrative Offenses of the Russian Federation.

Criminal liability for tax offenses

Only an individual can be held criminally liable for committing a tax crime.

In the event that a violation of the law was committed by an organization, a sanction will be imposed on its director or chief accountant, although in some cases it is possible to hold accountable the founders or other persons who had a direct influence on its activities. The criterion for determining the severity of a crime (and, as a consequence, establishing punishment) is the amount of damage caused. In all the articles listed below, it is divided into 2 categories: large and extra large. Moreover, for different types of offenses, the value that the damage must meet in order to classify it into a certain category will be different. You can find out the exact amount of arrears at which the damage can be considered large or especially large in the text of the article establishing the sanction for a certain offense.

The fact of non-payment of taxes in an amount less than that established by the legislator for a large amount does not allow the offense to be classified as a criminal offense. However, this does not mean at all that the violator will not be held accountable, since he will continue to have the obligation to pay fines established by administrative legislation (if brought to administrative responsibility).

At the same time, the legislator exempts from criminal liability persons who committed a tax crime for the first time and paid off the debt they had accumulated, as well as paid all associated penalties and fines (clause 3 of Article 198, clause 2 of Article 199, clause 2 of Article 199.1 of the Criminal Code RF). For violators who have committed an act provided for in Art. 199.2 of the Criminal Code of the Russian Federation, such a relaxation is not provided.

Responsibility under Art. 198 and 199 of the Criminal Code of the Russian Federation

Provisions of Art.

198 of the Criminal Code of the Russian Federation determines the responsibility of an individual (including individual entrepreneurs) for tax evasion, realized by failure to submit mandatory documentation to the regulatory authority. In the same way, it is a violation to deliberately include in such documentation information that does not correspond to reality. If the damage is large, the violator will have to pay a fine of 100 to 300 thousand rubles. Alternatively, the court may rule on the recovery of funds earned by the culprit for a period of one to two years, or sentence him to forced labor (for no more than a year). As a last resort, the court may imprison the person for up to a year.

For evasion, the size of which is particularly large, the violator can be fined in the amount of 200 thousand to 0.5 million rubles. or the equivalent of his income for a period of one and a half to 3 years. In addition, the court may sentence the perpetrator to forced labor for up to 3 years or imprisonment for the same period.

In Art. 199 of the Criminal Code of the Russian Federation establishes liability for a similar violation of the law committed by an organization. The sanction for the manager in this case is more stringent: for large-scale damage, the violator will be fined in the amount of 100 thousand to 0.5 million rubles. or be deprived of income for a period of one to two years. In addition, the court may decide to subject him to forced labor (for no more than 2 years), arrest him (up to six months) or imprison him for up to 2 years.

A particularly large amount of damage is punishable by a fine in the amount of earnings for a period of one to three years or in the form of a fixed amount from 200 to 500 thousand rubles. The court may also impose forced labor on the convicted person for up to 5 years or imprison him for up to 6 years.

Grishchenko A. V. Ph.D., certified auditor of the Ministry of Finance of Russia

The article will discuss the types of tax offenses and responsibility for their commission. Let us separately dwell on the sanctions provided for by the Tax Code and the Code of Administrative Offences. In addition, since January 1, 2010, changes have been made to the Criminal Code - the main changes affected the articles regulating liability for non-payment of taxes on a large and especially large scale.

A tax offense is an unlawful act committed by a taxpayer, tax agent and other persons, for which the Tax Code of the Russian Federation establishes liability (Article 106 of the Tax Code of the Russian Federation). In addition to the liability established in the Tax Code of the Russian Federation, administrative and criminal liability is provided for the commission of certain types of offenses in the field of taxes and fees. Tax legislation provides for the liability of individuals and legal entities for committing a tax offense, and an individual can be brought to tax liability from the age of 16.

Chapter 16 of the Tax Code of the Russian Federation establishes the types of tax offenses and responsibility for their commission. The most common tax offenses encountered in practice can be presented in Table 1.

Table 1

Tax liability

| № | Type of offense | Base | Who is responsible | Fine |

| 1 | Violation of the deadline for filing an application for registration with the tax authority for a period of no more than 90 calendar days | Art. 116 Tax Code of the Russian Federation | Taxpayers | 5,000 rub. |

| 2 | Violation of the deadline for filing an application for registration with the tax authority for a period of more than 90 calendar days | Art. 116 Tax Code of the Russian Federation | Taxpayers | 10,000 rub. |

| 3 | Conducting activities without registering with the tax authority for no more than 90 calendar days | Art. 117 Tax Code of the Russian Federation | Organizations and individual entrepreneurs | 10% of income, but not less than 20,000 rubles. |

| 4 | Conducting activities without registering with the tax authority for more than 90 calendar days | Art. 117 Tax Code of the Russian Federation | Organizations and individual entrepreneurs | 20% of income received over a period of more than 90 days, but not less than 40,000 rubles. |

| 5 | Violation of the deadline for submitting information about opening/closing an account in a bank to the tax authority | Art. 118 Tax Code of the Russian Federation | Taxpayers | 5,000 rub. |

| 6 | Failure to submit a declaration to the tax authority at the place of registration within no more than 180 days after the deadline for submitting the declaration | Art. 119 Tax Code of the Russian Federation | Taxpayers | 5% of the tax amount payable for each full or incomplete month, but not more than 30% of the specified amount and not less than 100 rubles. |

| 7 | Failure to submit a declaration to the tax authority at the place of registration for more than 180 days after the deadline for submitting the declaration | Art. 119 Tax Code of the Russian Federation | Taxpayers | 30% of the amount of unpaid tax, as well as 10% of the amount of unpaid tax for each full or partial month, starting from the 181st day |

| 8 | Gross violation of the rules for accounting for income, expenses or taxable items, if these acts were committed during one tax period | Art. 120 Tax Code of the Russian Federation | Organizations | 5,000 rub. |

| 9 | Gross violation of the rules for accounting for income, expenses or taxable items, if these acts were committed in several tax periods | Art. 120 Tax Code of the Russian Federation | Organizations | 15,000 rub. |

| 10 | Gross violation of the rules for accounting for income, expenses or taxable items, if these actions resulted in an understatement of the tax base | Art. 120 Tax Code of the Russian Federation | Organizations | 10% of the amount of unpaid tax, but not less than RUB 15,000. |

| 11 | Non-payment or incomplete payment of tax amounts as a result of understatement of the tax base, other incorrect calculation of tax or other illegal actions | Art. 122 Tax Code of the Russian Federation | Organizations and individual entrepreneurs | 20% of the unpaid tax amount |

| 12 | Non-payment or incomplete payment of tax amounts as a result of underestimation of the tax base, other incorrect calculation of tax or other illegal actions committed intentionally | Art. 122 Tax Code of the Russian Federation | Organizations and individual entrepreneurs | 40% of the unpaid tax amount |

| 13 | Unlawful non-transfer or incomplete transfer of tax subject to withholding and remittance by the tax agent | Art. 123 Tax Code of the Russian Federation | Tax agents | 20% of the amount to be transferred |

| 14 | Failure to submit documents or other information within the prescribed period | Art. 126 Tax Code of the Russian Federation | Taxpayers, fee payers, tax agents | 50 rub. for each document not submitted |

Note! Presumption of innocence of a person brought to tax liability. A person is considered innocent of committing a tax offense until his guilt is proven in the manner prescribed by federal law and established by a court decision that has entered into legal force. A person held accountable is not required to prove his innocence of committing a tax offense. The responsibility for proving circumstances indicating the fact of a tax offense and the guilt of a person in committing it rests with the tax authorities. Irremovable doubts about the guilt of the person held accountable are interpreted in favor of that person. The principle of the presumption of innocence is enshrined in Art. 49 of the Constitution of the Russian Federation and paragraph 6 of Art. 108 Tax Code of the Russian Federation. The taxpayer is in good faith until the contrary is proven (clause 1 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation of October 12, 2006 No. 53).

Administrative liability for tax offenses

An administrative offense is an unlawful, guilty action (inaction) of an individual or legal entity, for which the Code of Administrative Offenses of the Russian Federation has established administrative liability, while individual entrepreneurs are equated to officials.

A person is considered innocent until his guilt is proven and established by the body that examined the case. Irremovable doubts about a person's guilt are interpreted in favor of that person.

The following circumstances are recognized as mitigating administrative liability: repentance; voluntary reporting by a person of an offense committed by him; prevention by the person who committed the offense of its harmful consequences, voluntary compensation for the damage caused or elimination of the harm caused; committing an offense in a state of strong emotional excitement (affect) or due to a combination of difficult personal or family circumstances; commission of an offense by a minor or a pregnant woman or a woman with a young child.

The body considering the case of an administrative offense may recognize other circumstances as mitigating. If these circumstances exist, a minimum fine may be applied.

The following are recognized as circumstances aggravating administrative liability: continuation of illegal behavior, despite the demand of authorized persons to stop it; repeated commission of a similar offense within a year; involvement of a minor in committing an offense; commission of an offense by a group of persons; committing an offense during a natural disaster or other emergency circumstances, while intoxicated. If these circumstances exist, the maximum fine may be applied.

It is also possible to simultaneously hold an organization and an official of the organization liable if the article of the Code of Administrative Offenses provides for both an official and a legal entity as a subject.

Responsibility for administrative offenses in the field of taxation is established by Articles 15.3 - 15.9 and 15.11 of the Code of Administrative Offenses.

table 2

Administrative responsibility

| № | Type of offense | Base | Who is responsible | Fine |

| 1 | Violation of the deadline for registration with the tax authority | Art. 15.3 Code of Administrative Offenses of the Russian Federation | Officials, except individual entrepreneurs | 500 – 1000 rub. |

| 2 | Violation of the deadline for registration with the tax authority, associated with conducting activities without registration with the tax authority | Art. 15.3 Code of Administrative Offenses of the Russian Federation | Officials, with the exception of individual entrepreneurs | 2000 – 3000 rub. |

| 3 | Violation of the deadline for submitting information to the tax authority or the body of the state extra-budgetary fund about opening or closing an account with a bank or other credit organization | Art. 15.4 Code of Administrative Offenses of the Russian Federation | Officials, except individual entrepreneurs | 1000 – 2000 rub. |

| 4 | Violation of deadlines for submitting a declaration to the tax authority | Art. 15.4 Code of Administrative Offenses of the Russian Federation | Officials, except individual entrepreneurs | 300 – 500 rub. |

| 5 | Failure to submit on time or refusal to submit to the tax authorities, customs authorities and bodies of the state extra-budgetary fund documents or other information necessary for the implementation of tax control. Or presentation of such information incompletely or in a distorted form | Part 1 Art. 15.6 Code of Administrative Offenses of the Russian Federation | Citizens | 100 – 300 rub. |

| 6 | The same | Part 1 Art. 15.6 Code of Administrative Offenses of the Russian Federation | Officials, except individual entrepreneurs | 300 – 500 rub. |

| 7 | Gross violation of the rules of accounting and presentation of financial statements[1] | Art. 15.11 Code of Administrative Offenses of the Russian Federation | Officials, except individual entrepreneurs | 2000 – 3000 rub. |

An administrative case is considered initiated from the moment the protocol is drawn up. The Code of Administrative Offenses provides for both open and closed consideration of cases. A person against whom proceedings are being conducted for an administrative offense has the right to: get acquainted with all the materials of the case; give explanations; present evidence; file petitions and challenges; use legal assistance from a lawyer; enjoy the right to protection of rights and legitimate interests by legal representatives; participate in the consideration of the case.

The following persons have the right to draw up a protocol on tax violations: judges; officials of internal affairs bodies, tax and customs authorities. The protocol shall indicate the date and place of its compilation, position, surname and initials of the person who compiled the protocol, information about the person against whom the case was initiated, surnames, first names, patronymics, addresses of the place of residence of witnesses, if any, place, time of commission and event offenses, article of the Code of Administrative Offenses providing for liability, explanation of the person against whom the case was initiated. In addition, the protocol must indicate that the person against whom the case has been initiated has been informed of their rights and obligations.

The protocol is signed by the official who compiled it, the person against whom the case was initiated. These persons have the right to refuse to sign the protocol, about which a corresponding entry must be made in it. A copy of the protocol, at the request of the person against whom the case has been initiated, may be handed over against signature. The person against whom the case has been initiated has the right: to familiarize himself with the protocol; provide explanations and comments that must be attached to the protocol.

A protocol is drawn up immediately after a violation is detected. If additional clarification of the circumstances of the case or information about the person against whom the case is being initiated is required, then a protocol is drawn up within two days from the moment the offense was discovered.

Criminal liability for tax offenses

For economic crimes, including tax crimes, citizens are held criminally liable in accordance with Chapter 22 of the Criminal Code of the Russian Federation. A crime is a socially dangerous act committed guilty of guilt, prohibited by the Criminal Code under threat of punishment.

Depending on the nature and degree of public danger, acts are divided into crimes of minor gravity, crimes of medium gravity, serious crimes and especially serious crimes.

Crimes of minor gravity are recognized as intentional and careless acts, for the commission of which the maximum punishment does not exceed two years of imprisonment.

Crimes of medium gravity are considered intentional acts, for which the maximum penalty does not exceed five years of imprisonment, and careless acts, for which the maximum penalty exceeds two years of imprisonment.

Serious crimes are intentional acts for which the maximum punishment does not exceed ten years in prison.

Particularly serious crimes are intentional acts, the commission of which is punishable by imprisonment for a term of over ten years or a more severe punishment.

A person who has reached the age of sixteen at the time of committing a crime is subject to criminal liability.

Types of penalties are: fine; deprivation of the right to hold certain positions or engage in certain activities; deprivation of a special, military or honorary title, class rank and state awards; compulsory work; correctional work; restriction on military service; restriction of freedom; arrest; detention in a disciplinary military unit; deprivation of liberty; life imprisonment.

Federal Law No. 383-FZ of December 29, 2009 “On Amendments to Part One of the Tax Code of the Russian Federation and Certain Legislative Acts of the Russian Federation” introduced significant changes to the Criminal Code of the Russian Federation in terms of articles providing for the possibility of bringing to criminal liability for committing tax offenses. The law came into force on January 1, 2010.

Table 3

Criminal liability

| № | Type of crime | Base | Who is responsible | Fine | Arrest | Deprivation of liberty | Deprivation of the right to a position or activity | Statute of limitations |

| 1 | Tax evasion from an individual by failure to submit a tax return, or by including knowingly false information in a tax return, committed on a large scale[2] | Part 1 Art. 198 of the Criminal Code of the Russian Federation | Individual entrepreneurs, lawyers, notaries, other individuals | from 100,000 to 300,000 rubles. or income for a period of 1 to 2 years | From 4 to 6 months. | Up to 1 year | — | 2 years |

| 2 | The same thing committed on an especially large scale[3] | Part 2 Art. 198 of the Criminal Code of the Russian Federation | Individual entrepreneurs, lawyers, notaries, other individuals | from 200,000 to 500,000 rubles. or income for a period of 18 months to 3 years | — | Up to 3 years | — | 6 years |

| 3 | Evasion of taxes from an organization by failure to submit a tax return or other documents, or by including knowingly false information in a tax return or such documents, committed on a large scale[4] | Part 1 Art. 199 of the Criminal Code of the Russian Federation | Gene. director, chief accountant, and other responsible persons | from 100,000 to 300,000 rubles. or income for a period of 1 to 2 years | From 4 to 6 months. | Up to 2 years | Up to 3 years | 2 years |

| 4 | The same thing committed by a group of persons by prior conspiracy on an especially large scale[5] | Part 2 Art. 199 of the Criminal Code of the Russian Federation | Gene. director, chief accountant, and other responsible persons | from 200,000 to 500,000 rubles. or income for a period of 1 to 3 years | — | Up to 6 years | Up to 3 years | 10 years |

| 5 | Failure to fulfill the duties of a tax agent in personal interests, committed on a large scale (Large amount is defined in Article 199 of the Criminal Code of the Russian Federation, footnote 4) | Part 1 Art. 199.1 of the Criminal Code of the Russian Federation | IP, gen. director, chief accountant, and other responsible persons | from 100,000 to 300,000 rubles. or income for a period of 1 to 2 years | From 4 to 6 months. | Up to 2 years | Up to 3 years | 2 years |

| 6 | The same thing committed on an especially large scale (Especially large scale is defined in Article 199 of the Criminal Code of the Russian Federation, footnote 5) | Part 2 Art. 199.1 of the Criminal Code of the Russian Federation | IP, gen. director, chief accountant, and other responsible persons | from 200,000 to 500,000 rubles. or income for a period of 2 to 5 years | — | Up to 6 years | Up to 3 years | 10 years |

| 7 | Concealment of funds or property of an organization or individual entrepreneur, at the expense of which taxes should be collected | Art. 199.2 of the Criminal Code of the Russian Federation | The founders of the organization, gen. director (manager) and other responsible persons | from 200,000 to 500,000 rubles, or income for a period of 18 months to 3 years | — | Up to 5 years | Up to 3 years | 6 years |

Thus, from January 1, 2010, the Criminal Code of the Russian Federation has been in effect in a new, more acceptable version for taxpayers. Federal Law No. 383-FZ of December 29, 2009 provides that a person who has committed a crime for the first time is exempt from criminal liability if he has fully paid the amounts of arrears, penalties and fines (Articles 198, 199, 199.1 of the Criminal Code of the Russian Federation). This amendment applies to persons who are under investigation or who are serving a sentence.

Since January 1, 2010, the amount of arrears has been significantly increased, which can lead to criminal liability (Articles 198, 199 of the Criminal Code of the Russian Federation). For legal entities – three times, for individuals – six times (Table 3).

[1] A gross violation of the rules of accounting and presentation of financial statements means: 1. distortion of the amounts of accrued taxes and fees by at least 10%; 2. distortion of any article (line) of the financial reporting form by at least 10%.

[2] Arrears for three consecutive years exceeding 600,000 rubles are recognized as large amounts if they exceed 10% of the tax amount, or 1,800,000 rubles.

[3] A particularly large amount is recognized as arrears for three consecutive years exceeding 3,000,000 rubles, if it exceeds 20% of the tax amount, or 9,000,000 rubles.

[4] An arrear of more than 2 million rubles for three years in a row is recognized as a large amount, if it exceeds 10% of the tax amount, or 6 million. rub.

[5] A particularly large amount is recognized as arrears exceeding 10 million rubles for three years in a row, if it exceeds 20% of the tax amount, or 30 million rubles.

Under what article of the Criminal Code of the Russian Federation does tax agent liability arise?

For tax offenses, responsibility arises not only for taxpayers, but also for tax agents.

A tax agent is a person obliged to timely calculate the amount of tax payments, withhold funds from taxpayers and transfer them to the state budget (Article 24 of the Tax Code of the Russian Federation). A striking example of a tax agent is an employer who withholds personal income tax from the salaries of its employees and independently transfers it to the Federal Tax Service. Provisions of Art. 199.1 of the Criminal Code of the Russian Federation establishes the extent of liability of a tax agent who does not fulfill the obligations assigned to him in order to satisfy personal interests. If the damage caused to the state is large, the court may impose a fine from the violator in the amount of 100 to 300 thousand rubles. or in the form of income for a period of time from 1 to 2 years. In addition, the court has the right to send the convicted person to forced labor for up to 2 years or imprison him for the same period.

If the amount of arrears corresponds to the status of especially large, the convicted person will have to pay a fine in the amount of 200 thousand to 0.5 million rubles. or in the amount of income for a period of time from 1 to 2 years. As an alternative punishment, the court may impose the obligation to perform forced labor (for no more than 5 years) or deprive the offender of liberty for up to 6 years. An additional penalty may be a ban on working in a certain position for up to 3 years.

Tax

The statute of limitations for tax violations is three years. Delay in payment or non-payment of tax in the Russian Federation requires a fine in the amount of 1/300 of the Central Bank refinancing rate for each day of delay (for individual entrepreneurs and individuals). Legal entities have a different scheme: for the first 30 days they will pay 1/300 of the refinancing rate, and from 31 days - 1/150 for each day of delay (Article 75 of the Tax Code of the Russian Federation).

IMPORTANT!

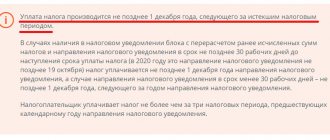

If a taxpayer filed a return on time and indicated the amount to be paid, but did not transfer contributions to the budget, he will be charged not a fine, but a penalty.

For example, a fine for non-payment of taxes by an individual on property is assessed after December 1 of the year following the accounting year (Article 409 of the Tax Code of the Russian Federation). If the owner does not pay the amount requested by the Federal Tax Service, he will be charged a penalty in the amount of 1/300 for each day of delay.

Employers have additional responsibilities and penalties. If an organization does not withhold personal income tax or withholds it but does not transfer it to the budget, it will be charged not only a fine, but also a penalty (Article 123 of the Tax Code of the Russian Federation). The amount of the fine is from 20% to 40% of the amount of non-withheld income tax (Article 122 of the Tax Code of the Russian Federation). The same rule applies to other obligatory fiscal payments and insurance contributions.