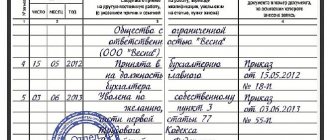

Chief accountant of the enterprise

So, the chief accountant of an enterprise is the person who should be entrusted with maintaining the company’s accounting records.

That is, this is a person who should be entrusted with the company’s finances, trade secrets, and control over the team. You can learn how to properly organize accounting from the materials in our “Accounting” section.

According to the requirements of Law No. 402-FZ, the organization of accounting is entrusted to the head of the enterprise. And to fulfill this duty he can:

- Maintain accounting records in person.

- Add a chief accountant to the staff.

- Transfer accounting maintenance to a third party (outsource).

However, all three methods are available only in small or medium-sized businesses. However, the law does not specify any clear requirements for the person who will ultimately be assigned the responsibility for keeping records.

If the company does not belong to such entities, then accounting should be entrusted to an employee of the organization or transferred under a contract. In a credit institution, there is only one option left - having a chief accountant on staff.

The Accounting Law sets out strict requirements for this position. In particular, it is mandatory to have a higher education, work experience of at least 3 years out of the last 5, and the absence of an outstanding conviction for economic crimes. However, they do not apply to all chief accountants, but only to persons holding this position in companies expressly specified in the law (see paragraph 4 of article 7 of law No. 402-FZ). These restrictions do not apply to chief accountants in small and medium-sized businesses.

Read more about the main accounting law in the section “Accounting Law”.

Find out whether it is possible to hold the chief accountant accountable after dismissal in the Ready-made solution from ConsultantPlus. If you don't have access, get a free trial online.

How and who determines the retention period for documents?

Paragraph 1 of Article 17 of the Federal Law of October 22, 2004 No. 125-FZ “On Archiving in the Russian Federation” states that organizations and individual entrepreneurs are obliged to ensure the safety of archival documents, including documents on personnel, during their storage periods.

These deadlines are established by federal laws, other regulatory legal acts of the Russian Federation, as well as special lists. First of all, this is a List of standard administrative archival documents generated in the course of the activities of state bodies, local governments and organizations, indicating their storage periods (approved by order of the Federal Archives of December 20, 2019 No. 236; hereinafter referred to as List No. 236);

In addition, storage periods are determined by other legal provisions. Thus, the minimum storage time for tax documents is established in the Tax Code, and for accounting documents - in the Accounting Law. And for joint-stock companies, there is also a Regulation on the procedure and periods for storing documents of joint-stock companies (approved by Resolution of the Federal Commission for the Securities Market dated July 16, 2003 No. 03-33/ps).

Important

The inclusion of documents in the archival fund does not depend on the method of their creation and the type of media (Article Law No. 125-FZ). Therefore, it is necessary to ensure the safety of both “paper” and electronic documents. The type of media in most cases does not affect the period during which the document must be preserved. At the same time, legally significant electronic documents can be stored without printing (see “The Ministry of Finance explained how to store electronic invoices”).

Exchange legally significant “primary data” with counterparties via the Internet. Free inbox.

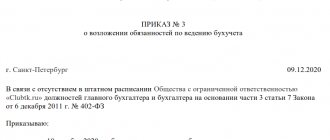

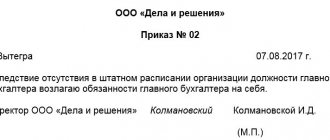

Rights and responsibilities of the chief accountant according to Law No. 402-FZ

Let's first talk about the rights of the chief accountant, a person who occupies a fairly high position in any company.

In general, the basic labor rights of any employee of any organization are controlled by the Labor Code of the Russian Federation, and the rights of the employee as a specialist are prescribed in his job description. What can you indicate when creating such instructions for the chief accountant? For example, the following:

- The chief accountant has the right:

- represent the interests of the organization’s accounting department, speaking in other structural divisions, before counterparty companies;

- request the necessary documents and information from other company specialists;

- submit for consideration to the director various financial plans, accounting structure, proposals for employee incentives or financial penalties;

- interact with other structural units to the extent necessary to perform their duties.

- By power of attorney, the chief accountant may be given the rights to represent the interests of the company in tax and other auditing structures.

We can also add that in addition to the main professional labor functions, the chief accountant, as a rule, himself selects the employees of his department, can regulate the search for an audit company to audit the enterprise, and, within the agreed framework, independently make decisions that affect the financial performance of the company, etc.

To determine the responsibilities of the chief accountant, you need to look not only at the law on accounting, but also at the professional standard. The current standard “Accountant”, approved. by order of the Ministry of Labor dated February 21, 2019 No. 103n. We wrote about it here.

Of course, compared to the rights, the responsibilities of the head of the accounting department are much more extensive. Let's consider it in detail; you can even divide all the responsibilities of the chief accountant into several groups.

- Financial group

- The main thing that the chief accountant does is keep records of the financial and economic activities of the company, and exercise control over the property of the enterprise.

- Forms the company's accounting policy in accordance with current legislation, including the development of a chart of accounts, primary forms, etc.

For an example of the correct approach to accounting policies, see our article “How to draw up accounting policies in an organization.”

- Organizes accounting of property received by the company, accounting of business transactions performed in the company.

- Organizes and controls the accounting of enterprise costs and sales of products.

- Generates complete and reliable accounting reports and, upon request, provides data on the company’s property status, income and expenses of the enterprise.

- Monitors compliance with tax legislation and the formation of tax reporting according to the rules corresponding to the Tax Code of the Russian Federation.

- Controls the correct calculation and payment of taxes, social contributions, administrative payments to state budgetary and extra-budgetary funds.

- Ensures the preparation of balance sheets and operational summary reports on income/expenses of funds, the use of the budget, and other statistical reporting, and their submission in the prescribed manner to the relevant authorities.

- Executive functions

- Monitors the job descriptions of his subordinates.

- Provides methodological assistance to employees of enterprise departments on issues of accounting, control, reporting and economic analysis.

- Informs the director of the enterprise about all identified shortcomings in the work of the accounting department of the enterprise, structural divisions with a mandatory explanation of the reasons for their occurrence, as well as proposing ways to eliminate them.

- Manages the accounting staff of the organization.

- Part of the work of controlling

- Takes measures to prevent shortages, uncontrolled spending of funds, and violations of current legislation.

- Responsible for conducting an inventory of fixed assets, inventory and cash.

- Analytical part of the work

- Takes part in the economic analysis of the company's activities.

- May take part in financial planning of the organization's activities.

To find out what it is, see our material “Main types of financial planning (description).”

Read more about the responsibilities of the chief accountant in our publications:

- “We are looking for extra responsibilities in the job description of the chief accountant”;

- “We are making changes to the job description.”

Fines for violating the document storage procedure

The most common situation when violation of the procedure or storage period can result in a fine is failure to submit a document at the request of the Federal Tax Service.

Let us remind you that such a request can be sent both during an inspection of the taxpayer himself (on-site or office), and within the framework of an “oncoming” inspection, or without ordering an inspection at all (Article and 93.1 of the Tax Code of the Russian Federation; for more details, see “The Federal Tax Service Inspectorate requires documents: for which requests need to be answered, and which ones can be ignored” and “The Federal Tax Service Inspectorate requested data on a counterparty or transaction: when is this legal, and what will happen if the request is not answered”). In all cases, failure to submit or untimely submission of each document that the taxpayer must have will result in a fine of 200 rubles. (Clause 1 of Article 126 of the Tax Code of the Russian Federation).

Attention

You can facilitate and speed up the process of sending documents to the inspection using special services, for example, the “Connector Kontur.Extern” web service.

It makes it possible to send tens of thousands of electronic documents to tax authorities at a time. Through the “Connector” you can transfer to the Federal Tax Service any electronic documents created in approved formats (for example, invoices, TORG-12 invoices, etc.), as well as scanned images of any documents created on paper: acts, contracts, payments etc. Connect to the Kontur.Extern system

In addition, the absence of primary documents or invoices may result in tax liability for gross violation of accounting rules. Here the size of the fine depends on the consequences. If the violation did not lead to an understatement of the tax base, then the fine will be 10,000 or 30,000 rubles. (Clause 1 and 2 of Article 120 of the Tax Code of the Russian Federation). If, due to the lack of documents, the tax base was underestimated, then the fine will be equal to 20% of the amount of unpaid tax, but not less than 40,000 rubles. (Clause 3 of Article 120 of the Tax Code of the Russian Federation).

Failure to comply with the storage deadlines for documents may become the basis for bringing the organization and its employees to administrative liability. Sanctions for violation of the rules for storing, compiling or using archival documents (including personnel and accounting) are established in Article 13.20 of the Code of Administrative Offenses of the Russian Federation. The punishment will be a warning or a fine in the following amount: from 3,000 to 5,000 rubles. for officials; from 5,000 to 10,000 rubles. for legal entities.

For failure to fulfill the obligation to store documents of a JSC or LLC within the time limits provided for by current legislation, organizations are punished more severely. The fine ranges from 2,500 to 5,000 rubles. for officials and from 200,000 to 300,000 rubles. for society itself (parts 1 and 2 of article 13.25 of the Code of Administrative Offenses of the Russian Federation). And for failure to comply with the storage deadlines for accounting and reporting documents on currency transactions, a fine of 4,000 to 5,000 rubles is provided. for officials and from 40,000 to 50,000 rubles. for organizations (Part 6 of Article 15.25 of the Code of Administrative Offenses of the Russian Federation). Slightly smaller penalties (from 1,000 to 2,000 rubles for officials and from 10,000 to 20,000 rubles for legal entities) are provided for violation of the terms of storage of accounting documents for foreign economic transactions with goods, information, works, services or results of intellectual activity for purposes of export control (Part 2 of Article 14.20 of the Code of Administrative Offenses of the Russian Federation).

Responsibility of the chief accountant

Of course, speaking about the rights and responsibilities of the chief accountant, we must not forget about his main responsibility - for the proper performance of official duties. All possible types and sanctions are given in the table below.

See also the article “Who is responsible for organizing accounting?”

| Responsibility | Types of violations | Forms |

| Disciplinary | Violation of labor discipline, and sometimes unprofessionalism (clause 9, part 1, article 81 of the Labor Code of the Russian Federation) | Reprimand, reprimand, dismissal |

| Material (Article 238 of the Labor Code of the Russian Federation) | Direct effective damage caused to the employer (real decrease in the employer’s property or deterioration in its condition) | Depending on the amount of damage |

| Administrative (regulated by a number of articles of Chapter 15 of the Code of Administrative Offenses of the Russian Federation) |

See also: “What an accountant can be fined for in 2019.” |

|

| Criminal liability | Occurs if the company evades taxes on a large and especially large scale for 3 years | Depending on the amount of damage (from a fine to imprisonment) |

Is it possible to hold the chief accountant, who is temporarily entrusted with the duties of the general director, liable for an industrial accident? The answer to this question is revealed by labor inspector in the Kirov region A. A. Berdyanskikh. Get trial access to the ConsultantPlus system and find out the controller’s opinion for free.

Retention periods for tax documents

Accounting and tax accounting data and other documents necessary for the calculation and payment of taxes, including documents confirming receipt of income, expenses, as well as payment (withholding) of taxes, must be stored for five years. These are the rules of subparagraph 8 of paragraph 1 of the article and subparagraph 5 of paragraph 3 of the article of the Tax Code of the Russian Federation. The countdown of the period begins after the end of the tax period in which the document was last used for preparing tax reports, calculating and paying taxes, confirming income received and expenses incurred (letter of the Ministry of Finance dated July 19, 2017 No. 03-07-11/45829).

Important

An exception is made for documents confirming the amount of loss incurred.

They are supposed to be kept for the entire period when it reduces the tax base of the current tax period by the amounts of previously received losses (clause 4 of Article 283, clause 7 of Article 346.18 of the Tax Code of the Russian Federation). A four-year shelf life is specified for the purchase ledger and sales ledger, including additional sheets to them. In this case, the countdown is carried out from the date of the last entry in the book (clause 24 of the Rules for maintaining the purchase book and clause 22 of the Rules for maintaining the sales book, approved by Government Decree No. 1137 of December 26, 2011). As for invoices, they should be kept for five years (Article 317 of List No. 236).

Carry out automatic reconciliation of invoices with counterparties Connect to the service

A five-year retention period is established for tax returns and calculations for all types of taxes. The exception is individual entrepreneur declarations for the period up to 2002 inclusive. They must be stored for 75 years (Article 310 of List No. 236). But the calculation of insurance premiums cannot be destroyed for 50 years from the date of its preparation (Article 308 of List No. 236).

Documents necessary for the calculation and payment of insurance premiums must be kept for six years (subclause 6, clause 3.4 of Article of the Tax Code of the Russian Federation). Such documents include, in particular, individual accounting cards for the amounts of accrued payments and other remunerations and the amounts of accrued insurance premiums (Article 309 of List No. 236).

Attention

In the absence of personal accounts or payroll records, individual accounting cards will have to be protected for 50 years (Article 309 of List No. 236).

From what point does the storage period for documents used to calculate insurance premiums begin? There is no direct explanation. In our opinion, in this case an analogy with tax documents can be applied. That is, the deadline is counted after the end of the billing period in which the document was last used to calculate and pay contributions and prepare reports on them.

Fill out, check and submit insurance premium calculations online

All correspondence with the tax office (notifications, demands, acts, decisions, resolutions, objections, complaints, applications) is required to be kept for five years. This period is doubled if the complaint is filed based on the results of an on-site or desk inspection (clauses 148 and 314 of List No. 236). All electronic documents with UKEP, and certificates of keys for verifying the electronic signature with which complaints and technological documents are endorsed, must be stored for at least five years. Here, the deadlines are counted from the date of receipt or sending of the relevant document (clause 3 of the Procedure given in Appendix No. 4 to the Federal Tax Service order dated December 20, 2019 No. MMV-7-9 / [email protected] ).

Reference

Contracts for the purchase of goods, works, and services to meet state and municipal needs must be kept for five years after the termination of obligations under them (Article 224 of List No. 236).

Receive notifications about government procurement for small and medium-sized businesses Set up newsletter

Results

As we can see, the list of functions of the chief accountant is quite wide, and it is a mistake to believe that all of his work involves drawing up a balance sheet. A modern chief accountant can analyze the financial condition of the company, clearly knows labor legislation and the rights of his employees, and can advise the director on methods of saving and tax optimization.

Sources:

Law “On Accounting” dated December 6, 2011 N 402-FZ

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Commentary to paragraph 2 of Art. 18

In paragraph 2 of Art. 18 of the commented Law establishes the deadline for submitting a legal copy of the annual financial statements to the state statistics body and other users of the financial statements. Differences from the norm of paragraph 2 of Art. 15 of the previous Accounting Law cannot be called significant, nevertheless they exist. Previously, there was a rule according to which organizations (with the exception of budgetary, government institutions and public organizations) were required to submit quarterly financial statements within 30 days after the end of the quarter, and annual financial statements within 90 days after the end of the year, unless otherwise provided by law RF.

Thus, firstly, there are no deadlines for the submission of interim reporting. This is likely due to the fact that the interim reporting package does not fall within the definition of legal deposit.

Secondly, it has been clarified that reporting is submitted no later than three months (and not 90 days) after the end of the reporting period (and not the reporting (calendar) year). This means that during a leap year, the deadline for submitting annual accounts (for organizations that were still in business as at 31 December) is now also 31 March. In addition, the issue with the deadlines for submitting a legal copy of financial statements in the event of liquidation or reorganization of an economic entity has been clearly resolved. In these cases, the “three month” rule will also apply. For example, if an organization was liquidated on December 15, then the deadline for submitting legal deposit accounts for it will be March 14 of the following year.

Rights and powers

The financier not only performs duties, but also has a number of powers and rights. For example, an accountant has the right to demand that company employees provide timely primary documents. In addition, the accountant can carry out counter-reconciliations with counterparties, inspectorates and funds to identify debts and adjust the correctness of calculations. Take part in control, audit and other verification activities.

Rights, powers and procedures for interaction with other structural divisions of the company should be specified in as much detail and clearly as possible. If we leave only general formulations, then disputes and disagreements are inevitable.