Blocking a current account: what is it and who is at risk?

Account blocking is a prohibition on carrying out banking transactions on the account(s) belonging to the owner.

A block can only be imposed if there are sufficient grounds. Several persons have the right to block an account:

- Performing tax control functions. In this case, the blocking procedure is subject to the requirements of the Tax Code of the Russian Federation, concerns only taxpayers and tax agents (legal entities, individual entrepreneurs, lawyers and notaries), and depends on the availability of decisions of the controlling tax authority on the entry into force of the procedure and on its cancellation.

- Conducting transactions with cash or other property that can be used for settlements. Here, the account is blocked in accordance with the law dated 08/07/2001 No. 115-FZ, called “On combating the legalization (laundering) of proceeds from crime and the financing of terrorism” - subject to conditions allowing this procedure. It must be carried out by the person (organization or individual entrepreneur) performing transactions with funds or property. In doing so, he should be guided by data published by a special supervisory body (Rosfinmonitoring) or a structure authorized by it (an interdepartmental commission). Most often in this situation we are talking about blocking the account by the bank. But a similar procedure can be carried out in relation to any owner of means of payment (both legal entities and individuals, including foreign or stateless).

Thus, account blocking can affect persons in any status, and both the Tax Code of the Russian Federation and Law No. 115-FZ can provide grounds for this. In this case, the blocking of the current account will actually be carried out by the bank or other person performing transactions with funds. In the case when it occurs in accordance with the requirements of the Tax Code of the Russian Federation, it is mandatory to have a decision made by the tax authority, and when this procedure is carried out in accordance with Law No. 115-FZ - data published by Rosfinmonitoring or an interdepartmental commission. The bank does not have the right to refuse to comply with the decision of the tax authority (clause 6 of Article 76 of the Tax Code of the Russian Federation), and failure to comply with the requirements of Law No. 115-FZ generally threatens it with the loss of its license to carry out banking activities (Article 13).

The unpleasant consequences of blocking an account by decision of the Federal Tax Service include not only restrictions on the use of funds, but also the inability to open new accounts or use electronic payment means during its operation (Clause 12, Article 76 of the Tax Code of the Russian Federation). If a legal entity or individual is included in the Rosfinmonitoring database as associated with criminal activity or suspected of it, then it is unlikely that he will be able to open a current account (clause 5.2 of Article 7 of Law No. 115-FZ).

How to challenge a bank's decision to block an account

You can challenge the bank’s decision to block an account only if the credit institution, by its own decision, froze the funds, since it cannot influence the Federal Tax Service’s requirement in any way. If it was the bank that blocked the current account, then you need to understand the situation in detail.

In this case, the bank must not only indicate the reason for its action, but also provide evidence of the doubts that caused the blocking. If they are unfounded and illegal, the client can go to court for compensation for material damage in the form of interest. In addition, since the bank informs other financial institutions about the blocking in connection with the issue of the company’s dishonesty, it can be obliged to recognize this information as invalid. This action is especially necessary, since otherwise other credit institutions may refuse the organization banking cooperation.

If the blocking of the current account is refused, the client has the right to appeal to the Interdepartmental Commission at the Central Bank of the Russian Federation with a complaint about the unlawful actions of the credit institution. At the same time, he must also provide official evidence that the bank blocked the account for illegal reasons.

Grounds for tax blocking of accounts

The rules that govern the blocking of accounts carried out by the tax service (in particular, the blocking of a legal entity’s bank account) are set out in Art. 76 Tax Code of the Russian Federation.

What are the tax reasons for blocking a current account? The main one among them is ensuring the implementation of the decision made by the Federal Tax Service regarding the need to collect unpaid tax payments (clause 1 of Article 76 of the Tax Code of the Russian Federation). But other reasons are also possible:

- failure to submit a tax return or calculation in form 6-NDFL after 10 working days from the deadline for submission (subclause 1, clause 3, clause 3.2 of Article 76 of the Tax Code of the Russian Federation);

- failure to provide the possibility of electronic interaction with the Federal Tax Service, if such is mandatory for the taxpayer according to the requirements of the Tax Code of the Russian Federation (subclause 1.1, clause 3, article 76, clause 5.1, article 23 of the Tax Code of the Russian Federation);

- failure to send to the tax authority an electronic document confirming the fact of receipt from the Federal Tax Service Inspectorate of information sent to the taxpayer electronically, within 16 working days from the date of sending (subclause 2, clause 3, article 76, clause 5.1, article 23 of the Tax Code of the Russian Federation);

- taking measures to compel compliance with the decision to pay arrears and penalties for taxes accrued based on the results of a tax audit (clause 10 of Article 101 of the Tax Code of the Russian Federation).

The time period for tax authorities to make a decision to block an account varies depending on the basis on which this measure is applied. You don’t have to bother yourself with calculations, but get free access to ConsultantPlus and see these deadlines there. K+ experts have already calculated everything.

Any taxpayer (tax agent) account may be blocked, except for such special accounts as election accounts and those related to referendum funds. That is, currency accounts and accounts in precious metals are also subject to the blocking procedure.

It is possible to block both all funds available in the account(s) and part of them. The entire amount of funds in the account will be frozen in the event of failure to submit reports, failure to provide the possibility of electronic interaction with the tax authority, or failure to send a document confirming the acceptance of information sent by the tax authority to the Federal Tax Service Inspectorate.

The second version of the limitation (partial) is applied when it comes to unpaid amounts of taxes (contributions), penalties or fines, the establishment of the final value of which does not pose a problem. This amount will be indicated in the collection decision, which must precede the decision to block the required amount in the account. In this case, for the situation of using a foreign currency account or a precious metals account for this account, the blocked amount will be determined, respectively, in an amount equivalent to its ruble value or calculated at the discount price of the precious metal on the date of suspension of operations on the account.

What payments can be made from a blocked account, see this article.

When it comes to non-payment of taxes by an investment partnership, transactions on the partnership’s accounts are subject to suspension. If there are not enough funds for them, then restrictions may extend to the accounts of managers and even ordinary partners.

Restrictions on the disposal of funds do not apply to payments that, in terms of priority of payment, prevail over tax payments or are equivalent to them.

Blocking for tax reasons occurs at the moment the bank receives a decision on this (clause 7 of Article 76 of the Tax Code of the Russian Federation). The decision is sent there electronically (clause 4 of article 76 of the Tax Code of the Russian Federation).

What is blocking a current account?

If your account has been blocked, or, as it is otherwise called, frozen, you will not be able to make almost any transactions on it. That is, you will not be able to use your own funds.

Why almost - because, for example, it is possible to make payments to pay off taxes. And in some cases, operations are available for transferring wages to employees. But simple external transfers are definitely prohibited.

In this case, you will have to decide everything and find out why the account was blocked and what to do now. Basically, banks prefer to distance themselves from this issue, telling only what documents you will now have to urgently obtain.

How to remove a block imposed by decision of the Federal Tax Service

So, your bank account has been blocked - what should a person subject to such sanctions do? First of all, eliminate the reason for which the blocking was carried out. That is, it is necessary:

- pay the amount of tax, penalties or fines that caused the restriction of the ability to use the account;

- submit unsubmitted reports (declaration or calculation in form 6-NDFL);

- organize electronic exchange of documents with the tax authority;

- send an unsent document to the Federal Tax Service - confirmation of acceptance of the information or perform the actions proposed for execution in this information.

You can see a detailed algorithm of actions for each situation in the ConsultantPlus ready-made solution for unlocking an account by receiving a free trial access.

A decision taken by a tax authority to block an account is canceled by a document of similar status drawn up by the same authority. Moreover, for such registration, the Tax Code of the Russian Federation (clause 3.1, 8, article 76) establishes a specific period, counted as one working day from the date:

- receipt by the Federal Tax Service of originals or copies of payment documents indicating payment of the required amount of tax debt;

- filing the required report;

- ensuring the possibility of electronic interaction with the Federal Tax Service;

- sending a document to the tax authority - confirmation of receipt of information or completion of the actions proposed in this information (response to a request or appearance of a representative at the Federal Tax Service Inspectorate).

One more working day is given to the tax authority to send the decision to the bank (clause 4 of article 76 of the Tax Code of the Russian Federation). It is also sent there electronically. At the same time, this document is brought to the attention of the taxpayer (tax agent).

Tips for unlocking your account

If the bank has blocked the account, it is necessary to quickly respond to this situation and first contact the credit institution. Employees are required to say for what reason the account was frozen - by decision of the bank itself or at the request of the tax office.

In a situation where the bank has blocked an account by its own decision, you should understand in detail what the reasons for this action are and what can be done to unblock it. As a rule, credit institutions require the provision of documentation indicating the legality of the transactions and the reliability of the counterparty.

If banks have blocked accounts at the request of the tax inspectorate, then you need to do the following:

Contact the inspector

In some situations, companies simply need to call the tax office. As a rule, if in the automated system of the Federal Tax Service a company has a debt on taxes or insurance premiums, the program must send a request to the organization to pay the debt. If the company does not repay its debt on time, the credit institution receives a request to suspend operations on the taxpayer’s accounts.

Logically, the company should have time to resolve a conflict situation, for example, to close a debt, but situations can be different - the program itself failed, the amounts were doubled and a “virtual” debt was formed, the payment request did not reach the taxpayer or the payment was incorrect posted to accounts.

To resolve such issues, it is enough to call the inspector at the territorial office of the Federal Tax Service or to the federal number by phone. 8.

Visit the Federal Tax Service office

It is easier to deal with blocking a current account at the request of the Federal Tax Service on the spot, and therefore, when visiting the inspector, it is advisable to take supporting documents with you (bank statements, payment orders, reports, notices received using 1C: Reporting). In addition, the latest reconciliation acts and certificates of absence of debt will be useful, on the basis of which you can confirm the absence of real debts on taxes and insurance premiums. You may also need reports from 1Spark Risks, with the help of which you checked the reliability of the counterparties to whom you sent money. You can read more about how counterparties are checked for reliability here.

Personally submit the decision to unblock the account to the bank

If the Federal Tax Service has decided to unblock the account, a notification about this is sent to the bank. However, due to a glitch in the program, sometimes this document may not be processed. In this case, it is better if the taxpayer receives the document on paper and takes it to the credit institution himself, although there is a risk that the employees will not accept it.

According to paragraph 4 of Art. 76 of the Tax Code of the Russian Federation, to unblock an account, banks must be guided by electronic documents received from the Federal Tax Service. Since the tax inspectorate program is periodically updated, and failures are often observed, the tax authorities themselves asked banks to accept documents on paper, as indicated in the Letter of the Federal Tax Service dated March 22, 2019 No. KCH-4-8 / [email protected]

If the bank still refuses to accept documents from the taxpayer, you should clarify what option they offer. For example, a covering letter from the Federal Tax Service can be attached to the decision to unblock an account. It is advisable to indicate in it exactly why the tax office cannot send an electronic notification about unblocking the current account.

Write a complaint

A complaint can be submitted either to the head of the territorial office or through the official website of the Federal Tax Service. It must indicate the basic facts related to the blocking of the current account by the bank, as well as attach copies or scans of supporting documents. As practice shows, filing a complaint is one of the most effective measures.

Important! When filing a complaint, you must use an official tone of address without unnecessary emotions or insults, otherwise the taxpayer may be fined under Art. 5.61 Code of Administrative Offenses of the Russian Federation. The fine for a company ranges from 50 to 100 thousand rubles, for an official - from 10 to 30 thousand rubles.

Reasons for blocking accounts according to law 115-FZ

Law No. 115-FZ, dedicated to the issues of countering the use of funds to finance criminal activities, obliges structures that carry out transactions with funds to carry out (Articles 6, 7) the following measures:

- checking of persons, both those wishing to open an account and those already having one, for involvement in illegal acts (including through their beneficial owners);

- control over certain types of transactions (with the possibility of their suspension) if their turnover exceeds the amounts established by law, or with the participation in them of persons suspected of involvement in terrorism;

- transfer of information about identified facts of illegal activities or counteraction to ongoing control to Rosfinmonitoring;

- freezing the accounts of persons suspected of involvement in criminal activities.

Thus, blocking of an account under 115-FZ is carried out by the bank itself or another person (organization or individual entrepreneur) performing transactions with funds. There are few reasons used for this. Essentially, the possible reasons for blocking a current account by a bank come down to two (Article 3 of Law No. 115-FZ):

- The client was included in the official list of persons involved in criminal activities (including those related to terrorism, extremism or weapons of mass destruction).

- The client is not included in the above list, but there are reasons to suspect him of extremist or terrorist activities, and based on these reasons, Rosfinmonitoring or the interdepartmental commission authorized by it made a decision to freeze the account.

In the first case, the information must be present on the Rosfinmonitoring website in the corresponding list (subclause 6, clause 1, article 7 of Law No. 115-FZ). And in the second, the decision on blocking should be published on the website of the same department or interdepartmental commission. However, regardless of which of the grounds the blocking occurs, it is carried out no later than one working day from the moment this ground arises (subclause 6, clause 1, article 7, clause 5, article 7.5 of Law No. 115-FZ).

Inclusion in the list of persons involved in criminal activities occurs in the presence of a judicial or administrative act that has entered into force, another procedural document, lists and judicial acts of the international level, indisputably indicating the client’s involvement in terrorism or extremism (Clause 2.1 Article 6 of Law No. 115-FZ).

If the grounds for freezing an account are identified by the person carrying out transactions with funds independently, then he must promptly bring this to the attention of Rosfinmonitoring (clause 3 of Article 7 of Law No. 115-FZ), and in this case he has the right to independently suspend the transaction. dubious transaction for up to 5 working days (clause 10 of article 7, clause 8 of article 7.5 of law No. 115-FZ) pending a decision on blocking made by Rosfinmonitoring. The decision to block in this case can be made for up to 30 days (Article 8 of Law No. 115-FZ), which is intended to clarify the circumstances in more detail and take measures that give the right to permanently freeze the account.

How to prevent account blocking

To protect your accounts from blocking, you need to follow some rules for organizing cash flow:

- Work only on selected types of activities or take care of adding a new OKVED in advance.

- Describe the purpose of the payment correctly and in detail.

- Check the reliability of partners through electronic .

- Do not cash out all the money at once, let it sit for several days, and then withdraw some of the money and leave 15-25% of the amount in the account.

- Pay taxes and insurance premiums on time, or better yet, open a second account and save money there for mandatory payments.

- Notify the bank and the tax office about a change in the manager or company details.

- Provide the bank with the necessary documents on time, and if some documents are missing, it is better to inform the bank about this and send them later.

Read the separate article: “Blocking an LLC or Individual Entrepreneur account: how to prevent it”

If you follow these rules, you can reduce the likelihood of your account being blocked.

How to unblock an account according to law 115-FZ

Is it possible to unblock an account under 115-FZ and how to do it? Yes, this is possible. There are three situations that allow this:

- The document that served as the basis for including the client in the list of those involved in criminal activities, including partially (i.e., in relation only to a specific person), has been canceled or terminated.

- The client was included in the official list of persons involved in criminal activities by mistake.

- An individual whose account has been blocked for good reason has lost his livelihood.

The first two situations allow the client to contact Rosfinmonitoring with a request to be excluded from the list. After a review lasting no more than 10 working days, this department will make a positive or negative decision (clause 2.3 of Article 6 of Law No. 115-FZ). The latter can be appealed in court.

In the third situation, an individual has the right to use blocked funds to support himself and his family members who do not have independent income, at the rate of 10 thousand rubles. per month per person, as well as make payments on obligations (including tax obligations) that arose before inclusion in the list of persons involved in criminal activities (clause 2.4 of Article 6 of Law No. 115-FZ).

If there are suspicions of international terrorism against a legal entity or individual, but it has not yet been included in the international list of those involved in it, then Rosfinmonitoring, in agreement with the international organization compiling such a list, can lift the blocking in whole or in part until it is included in the list (p 2.5 Article 6 of Law No. 115-FZ). This is done upon the application of the interested party submitted to Rosfinmonitoring, within one working day from the moment a positive decision is made by the international organization.

Appealing the actions of the bailiff to block the account

Unlawful restrictive measures applied against citizens and organizations that in fact are not malicious debtors, alas, are not uncommon. If there is no proper response from the FSSP to the submitted application, all that remains is to turn to the regulations that allow you to appeal the decision. Information is transmitted both through the hierarchy within the department - usually to a senior employee, who is subordinate to the culprit of the problem, and to the judicial authorities. The claim is sent to the location of the Federal Service within ten days from the receipt of notification of the arrest.

What to do to find out if your account is blocked

The client, as a rule, learns that the account has been blocked according to Law No. 115-FZ or by decision of the Federal Tax Service on the day this operation is carried out. No one will inform him about this in advance. Law No. 115-FZ (Article 4) generally prohibits informing the client that information about his involvement in criminal activity is being collected, making an exception for measures that have already actually been taken to limit the use of the account. And the Tax Code of the Russian Federation (clause 4 of Article 76) requires that the taxpayer be notified of the appearance of a decision to block no later than one business day from the date of adoption.

Therefore, it is unrealistic to know in advance whether a bank account will be blocked. The source of information could be data published on the website of Rosfinmonitoring, but the opportunity to use them is only available to persons performing transactions with funds, provided they have a personal account on the website of this department.

Information about tax blocking available to the client is provided by the website of the Federal Tax Service of Russia, but it appears there on the date the decision on it is made, i.e. just one business day before the official notice is sent to the taxpayer.

Read our article about how to check whether your counterparty’s account is blocked and why to do it.

Can I use a blocked account or open a new one?

If an account is frozen due to debt to the budget, only the amount specified in the decision to suspend transactions on the accounts will be blocked, in accordance with. The company can use the rest of the money at its own discretion.

If the account is blocked due to the fact that the organization did not file a declaration, then the entire amount may be frozen. In this case, the company cannot manage the money that is in the account and those that will flow into it in the future.

There are exceptions - funds from a blocked account can be used for these purposes:

- alimony and compensation payments;

- severance pay and royalties;

- salaries, payments to the Pension Fund and Social Insurance Fund;

- payments for administrative offenses and civil disputes;

- taxes and fees.

In accordance with, if the tax account is blocked, the entrepreneur cannot open a new account either in this bank or in another. You can try to open an account in a small bank outside the top hundred, but there are no guarantees.

If the bank has blocked the account under 115-FZ, there are ways to withdraw money.

Transfer money to a reserve account, and if there is none, to a counterparty.

To do this, the director of the company needs to take to the bank a payment slip for the counterparty, a certificate stating that the organization has no other accounts, and a letter indicating the need to fulfill obligations to the counterparty.

Transfer funds according to the writ of execution.

To do this, you need to create a document with a debt to the counterparty, receive a writ of execution and make payment.

Pay taxes.

To do this, you need to prepare a payment slip for taxes. You can pay both for your company and for your counterparty.

Results

Any person can face blocking of a current account: both legal entities and individuals. The basis for this procedure is contained in the Tax Code of the Russian Federation (in this case it applies to tax payers - organizations, individual entrepreneurs, lawyers, notaries) and Law No. 115-FZ (here we are talking about persons in any status related to criminal activity). Both of these documents are based on their lists of reasons why an account may be blocked. The actual termination of operations on the account is carried out by the person performing operations with funds, and this occurs as soon as possible from the date of occurrence of the grounds requiring such action from him.

Sources:

- Tax Code of the Russian Federation

- Federal Law of August 7, 2001 No. 115-FZ

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

What to do if your account is blocked illegally

There are cases when blocking an account (LLC or individual entrepreneur) by the tax inspectorate is illegal:

- If the organization did not submit its accounting reports on time, but at the time the decision to block was made, all reporting had already been submitted.

- The Federal Tax Service “lost” payments that were made correctly and without errors.

- We didn't have time to submit the documents due to the postal service.

We will help you find out the reasons for blocking your account and restore access to your money.

Find out the conditions

If the tax authorities illegally suspended the operation of a current account, this can be challenged in court and losses incurred during the blocking period can be reimbursed.

To do this, you can prepare an objection in which you should describe in detail what the violation of your rights is. Then the document must be sent to the regional or regional department of the Federal Tax Service. If the objections are not satisfied, you can appeal to the arbitration court at your place of residence.

An example of an objection to a decision to suspend transactions on a current account.

Source: atorcenter.ru In addition, the Federal Tax Service must pay interest to the company. They are charged at the refinancing rate for each calendar day of violation of the unblocking period. To calculate the amount of interest that an organization must pay, you need to follow.

An example of how to calculate the amount of interest that the tax service is obliged to pay to a company. Source: vc.ru

In addition, you can recover lost profits. To do this, the organization will have to prove that while its account was blocked, it could not receive income.

Illegal blocking of a tax account by the Federal Tax Service

It also happens that tax authorities illegally block accounts. Below we will talk about how such moments arise.

There have been certain innovations in tax legislation regarding what liability arises in the event of illegal blocking of accounts. So, if the tax authority allowed this scenario to happen, then the tax authorities are obliged to pay interest to the taxpayer. This, in my opinion, is a reasonable innovation, since there are often cases where tax authorities do not monitor such issues and make mistakes that entail certain consequences.

For example, it happens that the Federal Tax Service makes a block earlier than the deadline established by law. That is, the inspectorate does not have the right to block accounts when there has not yet been a decision to collect the tax.

Blocking restrictions

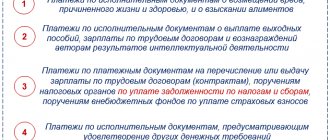

Despite the fact that blocking an account limits an organization's ability to use funds, some types of payments can still be made.

The fact is that account blocking does not apply to :

- Payments for transferring taxes, fees, insurance premiums, penalties and fines to the budget. This means that even after blocking the account, the company can send payment orders to the bank to transfer taxes, fees and contributions to funds to the budget, and the bank is obliged to execute these orders.

- Payments, the priority of which, according to civil law, precedes the fulfillment of the obligation to pay taxes, fees, penalties and fines. According to the Civil Code of the Russian Federation, payments on bank accounts are carried out in the following order: - first of all - according to executive documents on compensation for harm caused to life and health, as well as claims for the collection of alimony; - secondly - according to executive documents for calculations for the payment of severance pay and wages to resigning employees, as well as for the payment of remuneration to the authors of the results of intellectual activity; - in the third place - according to payment documents for paying salaries to working employees, on instructions from tax inspectorates and extra-budgetary funds to collect debts on taxes, fees and mandatory insurance contributions. Thus, collection of taxes at the request of the Federal Tax Service falls under the third priority. Therefore, the bank will execute payments of the first and second (and in some cases, third) priority unconditionally, even if the account is suspended.

Why can a bank block an account?

In order to comply with the requirements of Federal Law No. 115 dated January 7, 2001, the provisions of the Tax Code of the Russian Federation and Letter of the Bank of Russia No. 236-T dated December 31, 2014, banks are required to verify each client transaction. The financial monitoring service regularly checks the purpose of payments with registered types of activities, and also monitors data about the company, and carefully examines information about counterparties.

The slightest suspicion about the legality of a payment transaction is a reason to refuse it. Why can an account be blocked at the initiative of the bank itself? He has seven reasons for this.

- Inconsistency between the purpose of payment and the type of activity of the company. The account holder has the right to send and receive funds by non-cash method only within the framework of registered activities. Simply put, the payment must correspond to the OKVED codes specified in the Unified State Register of Legal Entities or Unified State Register of Individual Entrepreneurs.

- Fictitious leader. If it is discovered that the company is headed by a nominee director, the bank has the right to block the account until written explanations are received from the client. The manager's status is verified using a special service for verifying counterparties. A “mass” leader who heads several companies at once is a reason for control for a bank.

- Making updates to the Unified State Register of Legal Entities or Unified State Register of Individual Entrepreneurs without notifying the bank. If changes to the constituent documents are registered in the Federal Tax Service database, but they are not submitted to the bank, then it has the right to freeze the organization’s account. The agreement with the bank must include a clause on updating any information about the client: legal address, founders, management, amount of authorized capital, types of activities, etc.

- Inaccurate wording of the payment purpose. It is advisable that the wording of the “payment purpose” field differs from payment order to payment order. Duplication in relation to the same counterparty is possible. But the same phrase in relation to different partners raises doubts among the bank’s security service.

- Fictitious legal address. Blocking an account is possible after checking the address of the LLC, which can be arranged not only by the Federal Tax Service. The bank is also empowered to check its counterparties. The absence of a client at the specified address is a reason for termination of his service.

- Doubt about the integrity of the counterparty. Not only bank clients, but their counterparties are subject to verification. When receiving a payment from a company or individual entrepreneur from the list with mass addresses or managers, the list of malicious debtors of the Federal Tax Service or a company with a fictitious address, the bank has the right to block the account of its client.

- Frequent cash out. Taking too many withdrawals from an account without paying taxes on it. Although the bank’s functions do not include control over the payment of taxes, it is obliged to check cash withdrawals for laundering of proceeds from illegal transactions.

How can I find out if my current account is blocked? The bank decides individually whether or not to notify about the upcoming blocking - the law does not oblige this. But you can find out the reason for freezing the account - after all, the bank needs to both comply with the law and not lose the client. Establishing the reason is also important for preserving business reputation - contractor verification services that provide complete information about the partner are now popular. Account blocking is immediately reflected in their databases.

Open a current account in a partner bank

In what cases is blocking performed by counterparties?

The only reason why a counterparty has the right to block movement on a current account is debt. To carry out the blocking, he must obtain a writ of execution from the court and show it to the employee of the bank that opened the account. If the funds in the account are limited and do not allow repaying the debt, it will be seized and all funds received into it will be written off to pay off the debt.

How to solve a problem

If you did not know that a court decision had been made against you, you need to obtain information on the website kad.arbitr.ru and appeal the decision.

If it is not possible to solve the problem on appeal, you should file a cassation appeal and ask the court to suspend the implementation of the court decision. If there are grounds, you can apply for an installment plan or postponement of the implementation of the decision.

How to find out the exact reason and duration of blocking

You can find out whether your current account is blocked on the website of the Federal Tax Service of the Russian Federation. It is advisable to carry out such a check before concluding an agreement with a new partner.

You can find out about the status of your bank account without the Federal Tax Service - the operator will notify you about this. If he does not have the information or is not authorized to answer such questions, submit a written request to the manager. An alert is also enabled in the client bank service. Usually the notification indicates not only the fact, but also the reason for the blocking.

The period for lifting the seizure of an account depends on the reason and the authority that authorized it.

- Federal Tax Service. The blocking is lifted the next day after submitting the missed declaration or calculation, or within 3-4 days after the debt is repaid.

- Bank. He has his own rules. To lift the arrest for reasons independent of the Federal Tax Service, you will have to document or refute all suspicions of Financial Monitoring. It may take up to 2 months to review documents and make a decision.

- FSSP. Unfreezing of the account is carried out only after the obligations under the writ of execution have been repaid. But paying the debt does not automatically remove the arrest. You will have to write an application to the FSSP to lift the block and attach a document confirming the repayment of obligations. You need to get a decree from the bailiff to end the enforcement proceedings and provide a copy of it to the bank. If you do all this personally, without waiting for the bailiffs to do everything themselves, then it will take several days to unblock. According to the law, FSSP employees must complete this entire procedure independently, without reminders. But in practice, everything is different - only up to 10 days are allotted for consideration of the application.

How can I find out if my account is unblocked? Try making an online payment or just call your operator. Another way is to check on the Federal Tax Service website.