Organizational financial statements

Accounting statements are a unified system of organized data on the financial condition of a company, which is compiled on the basis of accounting records.

Absolutely all organizations are required to present financial statements to internal and external interested users. Let's consider the main accounting regulations that establish the procedure for its preparation by commercial organizations.

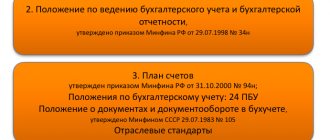

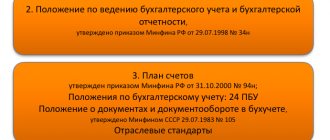

The basic rules for the preparation and submission of financial statements are enshrined in the Regulations on Accounting and Reporting in the Russian Federation, approved by Order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n.

This document was developed on the basis of the Law “On Accounting” dated December 6, 2011 No. 402-FZ and consists of 6 sections.

| No. | Section title | Theses |

| 1 | General provisions |

|

| 2 | Basic rules for accounting |

|

| 3 | Basic rules for drawing up and submitting accounting reports |

|

| 4 | Procedure for submitting accounting reports |

|

| 5 | Basic rules for consolidated accounting |

|

| 6 | Storage of accounting documents |

|

The content and list of forms of financial statements are approved in PBU 4/99.

According to clause 5 of section. 3 PBU 4/99 accounting includes:

- Balance sheet (form 1).

- Profit and loss statement of the company (Form 2).

- Appendixes to forms 1 and 2.

- Explanatory note.

- Auditor's report, if the company is subject to mandatory audit in cases established by law.

Also find out whether the tax office can fine you if the audit report is not submitted.

P. 6 section. 3 PBU 4/99 requires accounting records to provide reliable and complete information about the financial position of the company. In order to correctly reflect business transactions on the accounting accounts on the basis of which financial statements are formed, it is necessary to adhere to certain norms and rules that are independently approved by each organization in the main document regulating the procedure for maintaining accounting and tax accounting - the company’s accounting policy. Let's consider the order of its compilation.

Company accounting policies and accounting regulations

Accounting policy (AP) is a set of methods for maintaining accounting (and tax) accounting for each specific organization. It is approved upon creation of the company and is valid until its liquidation.

A sample accounting policy can be downloaded here.

In this case, the document is applied from year to year, and possible amendments to it are made from January 1 (unless a different date is due to significant reasons) if there are changes (clauses 5, 6, article 8 of Law No. 402-FZ):

- requirements of regulations governing accounting;

- method of accounting;

- operating conditions of the company.

The main accounting document of the company must reflect:

- Working chart of accounts.

- Primary forms used by the company.

- Document flow schedule.

From 01/01/2022, FSB 27/2021 “Documents and document flow” will become mandatory. Let us remind you that the document flow schedule is a mandatory appendix to the accounting policy.

ConsultantPlus experts explained in detail how to organize document flow for accounting purposes under the new FAS 27/2021. Get trial demo access to the K+ system and upgrade to the Ready Solution for free.

- Property accounting procedure.

- Algorithm for conducting audits of the company's liabilities and assets.

- Methods and procedure for determining the company's income and expenses.

- Methods and procedures for assessing property and other assets of an organization.

- Algorithm for monitoring business operations.

- Other important accounting nuances.

To correctly formulate each section of the accounting policy, companies need to focus on uniform accounting standards approved by the Ministry of Finance of Russia, namely: accounting regulations (PBU) and federal standards (FSBU).

PBU - legislative acts of the 2nd level, following the normative acts of federal significance. They establish the procedure and basic rules for accounting and reporting and are mandatory for all economic entities of the Russian Federation.

For the current list of PBUs, see this article.

The accounting policy of the organization is the accounting regulation PBU 1/2008, which establishes the rules for its formation, approved by Order of the Ministry of Finance of Russia dated October 6, 2008 No. 106n. It is compiled by the chief accountant and approved by the head of the company.

You will find the algorithm for generating this document in the article “How to draw up an organization’s accounting policy (2022)?”

Let's consider the main accounting regulations that must be relied upon when drawing up an organization's accounting policies.

Non-operating income and taxation

The significance of this type of profit is its influence on the formation of the tax base. Non-operating income must be taken into account when calculating the following types of taxes:

- profit tax - types of profit are summed up both from the sale of goods, works, services (under Article 249 of the Tax Code of the Russian Federation), and non-sales turnover (under Article 250 of the Tax Code of the Russian Federation);

- determination of the tax base under the special regime of the simplified tax system (Article 346.16 of the Tax Code of the Russian Federation);

- taxable base for the tax regime of the Unified Agricultural Tax (Article 346.5 of the Tax Code of the Russian Federation).

Inventory accounting: FSBU 5/2019

FSBU 5/2019 must be applied from 2022 instead of PBU 5/01. The new standard regulates the procedure for accounting for inventories of a company.

MPZ include:

- materials, raw materials;

- goods for resale;

- finished products.

Accounting for incoming assets is carried out at their cost, which includes the cost of receipt agreed upon by the buyer and supplier, and all overhead costs associated with the acquisition of these assets. In this case, micro-enterprises can take into account related costs as part of current expenses. Other companies that maintain simplified accounting can include such expenses as current expenses, provided that there are no significant material and production balances.

For information about who is allowed to conduct simplified accounting, read the article “Features of accounting in small enterprises.”

IMPORTANT! Companies that have the right to use a simplified version of accounting may provide in their policies a simple method of accounting, without using double entry (clause 6.1, section 2 of PBU 1/2008).

Disposal of inventories can be carried out:

- at average cost;

- at the cost of each unit;

- FIFO method (the asset that was first registered is written off first).

ConsultantPlus experts explained how to apply FAS 5/2020 in practice and what nuances to take into account when making changes to the accounting policies for 2022. Get free demo access to K+ and go to the Ready Solution to find out all the details of this procedure.

Accounting for fixed assets: FSBU 6/2020 (after 01/01/2022)

Currently, OS accounting is regulated by PBU 6/01. From 01/01/2022 it will no longer be in force and will be replaced by two new FSBUs: 6/2020 for OS and 26/2020 for capital investments.

ConsultantPlus experts explained what will need to be changed in accounting in this regard. You can view comments for free by getting trial access to the system.

According to FSBU 6/2020, the useful life (SPI) of objects depends on:

- from the expected period of operation,

- expected physical wear and tear;

- expected obsolescence,

- plans for the replacement and modernization of fixed assets.

In this case, objects can be taken into account as part of the inventory at a cost set by the taxpayer independently.

The initial cost is the amount of capital investment in the object. These include:

- the contractual value of the asset to be paid to the supplier;

- the cost of assets written off or depreciated in connection with their use in making capital investments;

- salary with deductions for compulsory social insurance accrued to employees participating in capital investments;

- estimated liability, including for future dismantling, disposal of property and environmental restoration.

The cost of fixed assets is repaid monthly by calculating depreciation. Depreciation is calculated:

- in a linear way;

- reducing balance method;

- proportional to the volume of products produced.

ATTENTION! Changes have occurred in the calculation of the base for calculating depreciation; now the latter is calculated not from the original or replacement cost, but from the difference between the book value and liquidation value. The last indicator is another innovation introduced by the standard. According to FAS 6/2020, liquidation value is the estimated value of assets that will remain after the liquidation of an asset, minus the costs of dismantling, disposal and other disposal.

In this case, organizations with simplified accounting and reporting can write off the amount of depreciation either once a year on December 31, or periodically throughout the year within the periods specified in its accounting policies. And the valuation of production and business equipment should be written off as depreciation charges at a time upon acceptance for accounting.

ATTENTION! Since 2022, companies are required to check for impairment of fixed assets in accordance with FAS 6/2020. Thus, assets cannot be accounted for at an inflated value in the financial statements.

Disposal of fixed assets is possible in various ways: through sale, write-off, contribution to the capital of another company, donation, etc. (clause 29 of PBU 6/01). When selling an asset, revenue is recognized as other income, and costs associated with the sale are included in other expenses.

Learn the specifics of using PBU 6/01 in this article.

Could other expenses be non-operating?

Listing in Art. 265 of the Tax Code is open, that is, it provides for the subclause “and others”. There are costs for which it is not always possible to unambiguously determine their affiliation; they can equally belong to both the implementation ones and their opposite. In such cases, the law provides the taxpayer with a choice; only this choice must be justified in the relevant internal documents.

NOTE! Other costs recognized as non-operating expenses must comply with the requirements of the Tax Code, that is, be economically justified, supported by documentation and related to the generation of income.

Examples of expenses that can be legitimately considered non-operating:

- banking fees;

- discounts provided;

- expenses for maintaining a trade union organization;

- legal costs if a case concerning the company’s production activities is being considered in court;

- interest on a loan taken to pay dividends or to purchase fixed assets.

ATTENTION! Interest is an independent type of expense, for which there are accounting rules provided for by the Tax Code. Therefore, depending on the purpose of the loan, interest on it can be classified as non-operating expenses or other types of expenses.

Accounting for an organization's income: PBU 9/99

Income is an improvement in the economic indicators of an enterprise due to the receipt of assets (cash, inventories, etc.), as well as a decrease in its liabilities, leading to an increase in the capital of this entity. In this case, contributions of its participants to the authorized capital are not taken into account.

According to PBU 9/99, income is divided:

- Those that arose from ordinary activities. This is, as a rule, revenue (clause 5 of PBU 9/99).

- Other: proceeds from rent, sale of fixed assets, receipt of interest, penalties, donated assets, exchange rate differences, etc. (clause 7 of PBU 9/99).

Revenue is recognized subject to the following conditions:

- The company has the right to receive income according to the contract (or on another basis).

- The amount of revenue is clearly defined.

- There is confidence that as a result of the transaction there will be an increase in the economic benefits of the company.

- Ownership of the asset passes to the buyer.

- The amount of expenses associated with generating income is determined.

IMPORTANT! If at least one of the listed conditions is not met, the assets received in fulfillment of obligations are recognized in accounting as accounts payable.

Companies that maintain simplified accounting have the right to recognize revenue using the cash method.

A sample accounting policy for enterprises using the simplified tax system was prepared by K+ experts. If you do not have access to the K+ system, get a trial online access for free.

What income is not realized?

When the definition states that the defined concept includes all indicators except those listed, then the necessary factors can be calculated by the method of elimination. It can be said that all types of income not mentioned in Art. 249 of the Tax Code of the Russian Federation. In turn, in Art. 250 of the Tax Code of the Russian Federation states that all income of an organization is recognized as non-operating, except :

- amounts received as a result of sales;

- tax-free financial income (they are specifically stipulated in Article 251 of the Tax Code of the Russian Federation).

Accounting for organizational expenses: PBU 10/99

Expenses according to PBU 10/99 include a decrease in economic benefits due to the disposal of funds or assets, as well as the occurrence of liabilities leading to a decrease in the company’s capital. This does not take into account the reduction of the authorized capital agreed upon by the founders.

Expenses fall into two categories:

- For ordinary activities: expenses directly related to production or sales (clause 5 of PBU 10/99).

- Other: expenses for renting premises, services of credit institutions, penalties and interest payable, etc. (clause 11 of PBU 10/99).

Expenses for ordinary activities are divided into the following cost items (clause 8 of PBU 10/99):

- material costs;

- depreciation;

- social expenses needs;

- wage;

- other costs.

At the same time, for the purposes of management accounting, the company has the right to create additional cost items at its discretion.

An expense is recognized if the following conditions are met:

- the expense is made in accordance with a specific agreement (or as required by law), as well as in accordance with business turnover;

- the amount of expenses is clearly defined;

- there is confidence that there will be a reduction in economic benefits.

IMPORTANT! If at least 1 of the listed points is not met, the company is obliged to take such expenses into account as accounts receivable.

Open list of non-operating expenses

Article 265 of the Tax Code of the Russian Federation lists 20 types of such expenses. Undoubtedly non-operating costs and financial losses of the organization include:

- funds spent on the maintenance and servicing of tangible assets rented or under a leasing agreement;

- interest that had to be paid on certain obligations during the reporting period: loans, credits, securities;

- costs of issuing the organization’s own securities (these include not only shares, but also forms, registers, magazines, publications in the media);

- registration costs;

- servicing purchased securities;

- losses caused by exchange rate fluctuations;

- expenses for liquidation of fixed assets, insufficient amount of accrued depreciation, liquidation of unfinished objects;

- expenses for conservation and re-preservation of the production process (to justify the costs, the decision of the manager and the availability of an estimate are required);

- costs for containers and packaging;

- obligation to pay fines, penalties, compensation;

- spending on various corporate events;

- funds for organizing and holding meetings of LLC founders or shareholders;

- the result of markdown of goods, inventories;

- some other expenses.

Results

PBUs are regulations that establish the procedure for maintaining accounting records in commercial organizations and are mandatory for execution by all economic entities of the Russian Federation. They contain general requirements for company accounting and are explained by methodological recommendations and letters from the Ministry of Finance and the Federal Tax Service of Russia.

All information about the procedure for maintaining accounting (and tax) records must be recorded in the accounting policy of the organization - accounting provisions form the legal basis of this document.

For information on the procedure for drawing up a company’s tax policy, read the article “How to draw up an organization’s tax policy?”

The article “The difference between accounting and tax accounting” will tell you how accounting differs from tax accounting.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How does Article 252 of the Tax Code of the Russian Federation group expenses?

There are many groupings of expenses: by areas, nature, types, costing items, accounting purposes (for example, for management or accounting).

To maintain tax records Art. 252 of the Tax Code of the Russian Federation establishes the following grouping of costs:

- Production costs and costs associated with the process of selling (selling) products.

- Expenses that are not included in the first point are non-operating costs.

Read about the principles on which this division is based in the material “Procedure and principles of accounting for income and expenses in an organization”