Who has the right to receive money

Accountable amounts are money that is given to employees to carry out company instructions.

New reporting rules have been established relatively recently - from August 19, 2022, with the adoption of a new edition of Bank of Russia Directive No. 3210-U. Employer, according to Part 1 of Art. 19 Federal Law dated December 6, 2011 No. 402-FZ “On Accounting”, is obliged to organize and maintain internal control of the facts of economic activity. The procedure for monitoring the issuance of money to accountable persons is determined by the head of the company. He issues an order with a list of persons entitled to receive funds from the organization's cash desk.

Accountable persons are persons to whom an organization or individual entrepreneur gives money to carry out instructions and who are obliged to provide a report on their use. They are any employees of the enterprise.

How to receive the money

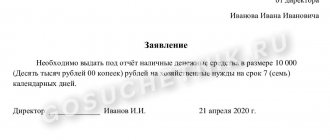

Before the introduction of the amendments, in order to receive money, the employee sent an application to the accounting department or human resources department, which indicated the required amount and an explanation of what it would be spent on.

But in 2022, from August 19, it has become easier to issue reports to employees. The changes are provided for by the instruction of the Central Bank of the Russian Federation dated June 19, 2017 No. 4416-U. From August 19, 2007, it is not necessary to submit an application. To issue money, an order or other administrative document of the company on behalf of the director is sufficient. The form of such a document is arbitrary. But it must contain the following details:

- FULL NAME. faces;

- document registration number;

- amount of cash;

- the period for which cash is issued; appointment (optional);

- director's signature and date.

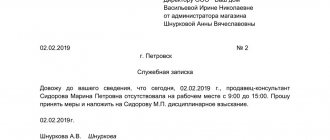

It is allowed to carry out settlements with accountable persons using a new sample of statements:

Features of issuing money for reporting to the director

The director is the main person in the company, but from the point of view of labor legislation, he is exactly the same employee as the rest of its employees. Therefore, all the above rules for issuing money on account also apply to the manager.

IMPORTANT! Relations arising as a result of election, appointment to a position or confirmation in a position are labor relations. In this case, the fact of concluding an employment contract with the general director does not matter (Articles 16–19 of the Labor Code of the Russian Federation). Therefore, the company can issue accountable funds to the director - the only founder.

The only peculiarity of issuing money for reporting to the director is that he cannot write an application for reporting and endorse it himself. Therefore, in this case, you should use not a statement, but an administrative document.

The director must comply with all other rules given in the previous section of the article, including the obligation to draw up an advance report, compliance with deadlines for submitting documentation to the accounting department confirming expenses incurred.

What amount should I report?

In Russia, payments in rubles that are carried out within the framework of one agreement should not exceed 100,000 rubles.

This is indicated in paragraphs 5 and 6 of the instructions of the Central Bank of the Russian Federation dated October 7, 2013 No. 3073-U. It is believed that this limit cannot be exceeded. But there are also nuances. This limit on expenses is established only for settlements with other organizations and individual entrepreneurs (see clause 6 of the instructions of the Central Bank of the Russian Federation No. 3073-U). But it does not apply to settlements with individuals who are employees of the enterprise. This includes wages, social benefits, personal needs of the head of the organization and the issuance of funds. Taking this into account, issuing a larger amount is not a violation of cash discipline.

What documents are needed to document accountable expenses?

Russian legislation on the management of cash affairs establishes a list of documents required to be provided when issuing finances for reporting:

- a memo that contains the reasons for issuing funds, including information about the initiator of the issuance and the recipient (the note is not needed if the initiator is the director of the company);

- an order drawn up and certified by the employer;

- Expense - cash order.

If funds are debited from a company account for business expenses associated with work assignments, then in order to receive cash, you may additionally need one of the following documents:

- travel certificate;

- travel worker registration book;

- work assignment;

- power of attorney to pay expenses on behalf of the organization;

- book of records of existing powers of attorney.

Is a report required for the amount received?

As stated in clause 6.3 of the instructions of the Central Bank of the Russian Federation dated 03/11/2014 No. 3210-U, until 08/19/2017 it was prohibited to issue money if the employee did not provide a report on previously received amounts.

Here the Central Bank made changes to the report. Now money can be issued even if the employee has not repaid the debt on previously issued funds. But this does not mean that employees no longer need to prepare advance reports on the amounts spent. The employee must submit reporting documents on the money spent to the accounting department.

Good to remember

- The company can pay for goods or services itself or with the help of an employee. The employee receives accountable money, completes the company's assignment and reports on expenses.

- Receive an advance report and documents confirming expenses from the employee. If he spent less money, he returns it to the company; if he spent more, he receives compensation.

- On the simplified tax system “Income minus expenses”, write off the accountable expenses spent as expenses. For the simplified tax system “Income”, also fill out the documents correctly, otherwise the tax office will charge personal income tax.

- If the employee left the reports to himself, within a month, issue an order to deduct from the salary. For large amounts, ask the employee to write a statement.

- Contact the court if you did not have time to issue an order a month in advance or the employee does not agree to the deductions.

- The tax office is suspicious of accountable directors: it may consider them income or an interest-free loan. In both cases, you will be charged additional taxes.

- Get accountable, and then buy for the company. Doing the opposite is risky.

The article is current as of 02/08/2021

Report deadlines

As stated in clause 6.3 of the instructions of the Central Bank of the Russian Federation dated March 11, 2014 No. 3210-U, the employee is obliged to provide a report on the amounts received no later than three working days after the expiration of the period for which these amounts were issued.

But the new requirements for the preparation of accountable amounts do not establish a specific period during which an employee must submit a report on the money spent. It is indicated in the employer's order. If the return period is not established, the employee submits the report on the same day on which he received them. This is indicated in the letter of the Federal Tax Service dated January 24, 2005 No. 04-1-02/704.

But for travel expenses there are special conditions for the advance report. According to clause 26 of the regulations, approved by Decree of the Government of the Russian Federation of October 13, 2008 No. 749, the employee is obliged to report on them within 3 working days from the date of return.

For what business expenses are funds issued for reporting?

In the Chart of Accounts (Order of the Ministry of Finance dated October 31, 2000 No. 94n), in the section describing account 71 “Settlements with accountable persons”, it is said that this account reflects transactions for settlements with employees of the enterprise for amounts issued for administrative, business and other expenses to the report.

What exactly administrative and economic expenses include is set out in the letter of the State Construction Committee of the Russian Federation “On the Procedure for determining the cost of construction and free (negotiable) prices for construction products in market conditions” dated December 29, 1993 No. 12-349. Despite the fact that the letter is related to pricing in construction, it quite fully reveals the meaning of the concept of “administrative expenses”.

In practice, accountable money is most often issued for the following needs:

- postage and communication costs;

- Inventory and materials for management personnel, including stationery;

- representation needs;

- travel expenses, etc.

Above we cited the following rule: in the application for the release of money to the account or the corresponding order of the manager, it is necessary to indicate the needs for which the money is issued. And although this is not formally directly established by law, in paragraph 6.3. Directive No. 3210-U states that money is issued “for expenses related to the activities of a legal entity or individual entrepreneur.” Therefore, in an application or order for the release of money for reporting, it is better to indicate the specific purpose for receiving the funds.

If money is issued from the cash register to an accountable person for household needs, the transactions may look like this:

| Dt | CT | Sum | Operation description |

| 71 | 50 | 10 000 | Money was given to an accountable person for the purchase of stationery |

| 26 | 71 | 7 500 | An advance report was received from the accountable person |

| 50 | 71 | 2 500 | The accountant returned the balance of unspent funds to the cash register |

What to consider in 2022

When accepting the report, take into account changes in the design of cash receipts and BSO.

From 07/01/2019, the cash register receipt or BSO issued instead includes information about the name of the buyer (organization or individual entrepreneur) and his tax identification number. When preparing documents using the new reporting templates from August 19, 2017, remember:

1. If the accountable person has been given a power of attorney to purchase goods and services in the interests of the organization and he has presented it to the seller, then the seller is obliged to reflect this data in the issued cash receipt.

2. If the seller is not able to reliably establish that an individual is acting in the interests of a certain organization, then he is not obliged to comply with this requirement for issuing a check. In this case, the buyer for the seller is the individual himself. And the cashier's check is issued in the usual manner.

We are changing the regulations on conducting cash transactions

Since adjustments have been made to the procedure for issuing money, changes to accountable amounts in 2022 also affected documentation.

Enterprises should update their regulations on working with imprest amounts. Employees have the right to receive accountable funds in cash at the enterprise cash desk. It is also allowed for the company to issue money to a bank card, including to the employee’s salary card (see instruction No. 3073-U, letter of the Ministry of Finance of Russia dated July 25, 2014 No. 03-11-11/42288). To make this possible, the procedure for settlements with reporting employees should be recorded in the company's accounting policies.

Money is issued through the cash desk in accordance with the following requirements:

1. When preparing cash documents, the accountant must be guided by the provisions of instructions No. 3210-U.

2. Money is issued to an accountable person on the basis of an order (or other administrative document) or upon his written application. As stated in the letter of the Central Bank of the Russian Federation dated September 6, 2017 No. 29-1-1-OE/2064, the order is signed by the director, indicating the date and registration number.

3. The period for which accountable funds are issued is established in the administrative document for their issuance. The report period (paragraph 2, clause 6.3 of instructions No. 3210-U) is 3 days. During this time, the accountable is obliged to report or return the money to the organization.

4. The issuance of money for reporting from the cash register is formalized by an expense order. Return of balances of accountable amounts - receipt orders. Money can also be issued for reporting by transferring it to the applicant’s bank card (letter of the Ministry of Finance dated August 25, 2014 No. 03-11-11/42288). It is allowed to return the money to the accountable by transferring funds to the company's current account. The possibility of non-cash accountable payments is fixed in the accounting policy.

5. There is no limit on the amounts that can be reported. The enterprise has the right to issue money to the accountable person in any amount. The settlement limit (RUB 100,000 per agreement) must be taken into account only when making payments between enterprises. In this regard, there have been no changes for accountable persons.

6. Issuing money on account to a person who has a debt on accountable amounts is not a violation of the law from 08/19/2017.

7. Organizations and individual entrepreneurs have the right to issue money on account not only to those employees who work on the basis of a permanent employment contract, but also to those who are in civil legal relations with the enterprise (letter of the Central Bank of the Russian Federation dated October 2, 2014 No. 29-1-1 -6/7859).

8. Issue from the cash register to the account is documented by posting Dt 71 Kt 50. When transferring funds to a card - posting Dt 71 Kt 51.

Changes from 11/30/2020

The new instruction of the Bank of Russia No. 5587-U dated 10/05/2020 came into force on 11/30/2020. The financial regulator has established a new procedure for issuing and spending accountable amounts in 2022 and approved new requirements for cash transactions in organizations and individual entrepreneurs. Now cash transactions are allowed to be carried out using devices that operate automatically without the participation of employees. Cashiers have the right not to require an identification document from recipients of money, although they are required to make sure that the person indicated in the debit order is in front of them.

Cashiers were prohibited from issuing banknotes with damage: contamination of the surface of the front or back sides, leading to a decrease in the brightness of the image by 8% or more, with extraneous inscriptions or drawings consisting of two or more characters or symbols, with stamp impressions or stains with a diameter of 5 mm and more. If the banknote contains one or more of these damages, as well as others specified in clause 2.9 of Bank of Russia Regulation No. 630-P dated January 29, 2018, it is subject to mandatory delivery to the bank. It is prohibited to accept cash from other persons who have been declared insolvent; this is stipulated by the new rules for working with accountants.

In the application of the accountable person for the issuance of money, it is no longer necessary to record the amount and the period for which the cash is issued. It is not necessary for the manager to sign the application. Organizations have the right to issue one order for several procedures for issuing cash to one or more accountable persons. The document must indicate:

- surnames and initials of cash recipients;

- amounts of cash;

- the period for which funds were issued for the report.

The requirement for a mandatory advance report within three days has been abolished. Now organizations and individual entrepreneurs independently set the period after which the accountable person must report and return the remaining money to the cash desk. This period is approved by the head of the organization or individual entrepreneur by a separate order and indicates it in the regulations on the issuance of money on account.

Use free instructions from ConsultantPlus experts to correctly issue money and account for it.

to read.

Main rules

Let's summarize what has been said:

1. Any amount is issued for the report.

2. From August 19, 2017, in order for an employee to receive an accountable payment, an order from the head of the company is sufficient. It is not necessary to write an application.

3. Previously, before submitting a report for the previous amount, an employee could not receive an accountable amount; now the answer to the question: is it possible to issue money for an accountable amount if the employee has not accounted for the previous one? Yes, it is possible.

4. Accountable amounts may be transferred to bank cards.

5. As of August 19, 2017, local acts on settlements with accountable persons have been updated.

Responsibility

It is important for organizations and individual entrepreneurs to follow the procedure for conducting cash transactions. Violation of this order will result in a fine (Part 1 of Article 15.1 of the Code of Administrative Offenses of the Russian Federation):

- for an organization - from 40,000 rubles. up to 50,000 rubles;

- for its officials and individual entrepreneurs - from 4,000 rubles. up to 5000 rub.

Hello Guest! Offer from "Clerk"

Online professional retraining “Accountant on the simplified tax system” with a diploma for 250 academic hours . Learn everything new to avoid mistakes. Online training for 2 months, the stream starts on March 1.

Sign up