Rules for drawing up a document

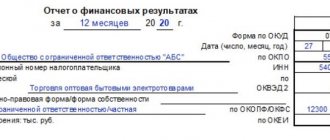

The financial results report has two unified forms:

- regular (includes extended information),

- simplified (the information in it is more compressed).

Regardless of which form the company uses, the report contains the following mandatory data:

- company details,

- date of document preparation,

- profit and loss indicators,

- total values.

You should be very careful when filling out the document, since mistakes, and even more so entering unreliable or deliberately false information into it, are fraught with unpleasant consequences.

If any inaccuracies or corrections were made during the process of filling out the document, it is best to print out a new form and fill it out again.

DDS or cash flow

Everyone wants to avoid mistakes - receive payment on time, avoid tax penalties and avoid cash gaps. All these tasks are solved by the cash flow statement or DDS.

Nikolay M.’s company repairs non-residential premises - teams work simultaneously on 5 objects. The business is new, in order to attract clients, Nikolai has to give a delay. He records income and expenses, so he knows exactly when a cash gap arises and the company needs additional financing.

A financial statement of cash flows contains all the receipts and expenditures of a company's funds for a period.

DDS shows how much money a company received and how much it paid, how much it had and how much it had left. Each operation is entered into it - income or expense; note who was paid and where they received the money from; divide fund movements into categories.

Rules for preparing financial reports

All information on the form can be entered either handwritten or printed. The main condition is that it contains the original signature of the head of the enterprise or an employee authorized to act on his behalf.

Starting from 2016, it is not necessary to put a stamp on the report, since legal entities are legally exempt from the need to endorse their documents using seals and stamps.

The financial results report is prepared in two copies :

- one is transferred to the tax office,

- the second remains in the organization.

After losing its relevance, this document is transferred for storage to the archive of the enterprise, where it is kept for the entire period established for this type of paper.

Statement of comprehensive income IFRS

This report is only partially included in the set of financial statements under IFRS. The statement of comprehensive income is a document that shows the amount of profit and loss and changes in other comprehensive income for a particular reporting period. Its preparation is also governed by IFRS 1.

The report consists of two sections:

- Gains and losses report

- Statement of other comprehensive income (items that affect retained earnings but are not reflected in the income statement, for example, changes in the revaluation reserve, declared dividends, etc.).

Expenses in the statement of comprehensive income are classified according to their nature and function. In either option, earnings and comprehensive income are allocated separately, attributable to the parent and separately to non-controlling shareholders. IAS 1 contains a minimum list of items of income and expenses that must be reflected in the statement of comprehensive income. The enterprise is obliged to decipher these items if necessary to understand the financial results. IFRS allows the above information to be provided in one form, as well as in two documents: the “Income Statement” and a document with data on retained earnings/losses, as well as other comprehensive income lines.

Example of Statement of Comprehensive Income

| PJSC "LYE" Statement of comprehensive income for the year ended December 31, 2016 | ||

| (in rubles) | ||

| 2011 | 2010 | |

| Revenues from sales | 89 795 229 | 79 306 979 |

| Cost of sales | (42 115 606) | (34 161 877) |

| Gross profit (loss) | 47 679 623 | 45 145 102 |

| Other income | 163 622 | 75 551 |

| Sales costs | (23 752 001) | (18 551 647) |

| Administrative expenses | (2 439 445) | (2 429 000) |

| other expenses | (10 709) | (551 231) |

| Profit (loss) from operating activities | 21 641 090 | 23 688 775 |

| Financial income | 1 319 017 | 1 269 192 |

| Financial expenses | (788 173) | (712 991) |

| Net financial profit (loss) | 530 844 | 556 201 |

| Share of profit (loss) from investments accounted for using the equity method | 29 193 | (57 629) |

| Profit (loss) before tax | 22 201 127 | 24 187 347 |

| Income tax | (4 487 947) | (5 016 165) |

| Net income (loss) | 17 713 180 | 19 171 182 |

| Other comprehensive income | ||

| Exchange differences associated with the translation of foreign transactions into reporting currency | 268 023 | 62 340 |

| Total total income for the year | 17 981 203 | 19 233 522 |

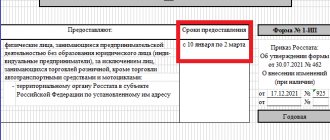

How to submit an income statement

Today, a document can be submitted to the tax service in three main ways.

- First : by going to the tax office in person. In this case, the report can be given either directly by the head of the company or by a proxy acting on his behalf (but then you must have a power of attorney certified by a notary).

- The second option: send the financial results report via electronic means of communication: however, here you need to keep in mind that the company must have a registered electronic signature.

- The third way to submit a report: sending it via Russian Post by registered mail with acknowledgment of delivery.

Balance sheet

To make management decisions, a business owner needs information. It is useful for him to see the business as a whole - to evaluate and understand all the details. This is what the Balance Sheet or Balance Sheet is for.

Andrey buys selfie sticks in China and sells them through retail outlets in large shopping centers. The balance helps him understand how much of the money is now “in goods” - he will not be able to quickly pull it out and direct it to the spinners that are gaining popularity. To play on demand, Andrey will have to take a loan from a partner or go to the bank for a loan.

A balance sheet is a summary: a snapshot of a company at a specific point in time.

The Balance Sheet summarizes all the company's assets - what it owns; and liabilities - those funds on which he lives. That is, on the one hand, this is equipment, raw materials and goods in stock, and on the other hand, loans and borrowings, investments in authorized capital and retained earnings. The assets and liabilities of the balance sheet are always equal to each other - nothing in the world arises from emptiness.

Money has several aggregate states in its assets. Equipment is difficult to sell, but money in the account is easy to use. The easier it is to release investments, the higher the liquidity of the asset. On the other hand, each liability has its own degree of urgency - something needs to be returned quickly, something may be with the company all the time. The balance sheet helps you see the current state of the money and correlate liquidity and urgency.

ANALYSIS OF BALANCE SHEET ITEMS

Analysis of balance sheet items shows:

- volume of assets, their ratio, sources of financing;

- items that change at a rapid pace, and how this affects the structure of the balance sheet;

- share of inventories and receivables;

- the amount of equity, the degree of dependence of the company on borrowed resources;

- distribution of loans by repayment period (long-term and short-term);

- level of debt to the budget, banks and employees.

There are several analysis methods:

- horizontal;

- vertical;

- trendy;

- factorial;

- financial ratios.

Horizontal analysis

Horizontal (time or dynamic) analysis reflects changes in indicators compared to the previous period. In horizontal analysis, the following is determined:

- absolute changes in indicators;

- relative deviations.

Absolute indicators

Absolute indicators characterize the number, volume (size) of the process being studied. They have a value (monetary) value on the balance sheet.

The calculated absolute indicator is the absolute deviation - the difference between two absolute indicators of the same name.

EXAMPLE 1

The amount of cash on line 1250 of the balance sheet in 2017 amounted to 2800 thousand rubles, in 2016 - 2400 thousand rubles. Let us find the absolute deviation of the amount of funds. 2017 will be the reporting year, 2016 will be the base year.

In the reporting period, compared to the base period, the amount of cash in absolute terms increased by 400 thousand rubles. (2800 thousand rubles – 2400 thousand rubles).

Composition of financial statements under IFRS and Russian legislation in 2022

Currently, more than 100 countries have officially prescribed or permitted the use of IFRS. The structure of international reporting differs from the Russian one in that it does not directly have a single approved or recommended chart of accounts; each company preparing reports under IFRS develops its own chart of accounts based on the specifics of the activity and the required detail of financial information. Let's compare the composition of financial statements that organizations must provide in accordance with IFRS and Russian legislation.

| IFRS | IFRS Russian legislation |

| Balance sheet | Balance sheet (form No. 1) |

| Report on the financial results of the organization's activities | Report on the financial results of the organization (form No. 2) |

| Statement of capital flows | Statement of changes in capital (form No. 3) |

| Cash flow statement | Cash flow statement (form No. 4) |

| — | Appendix to the balance sheet (form No. 5) |

| — | Report on the intended use of funds received (form No. 6) |

| Accounting policies and explanatory notes | Explanatory note |

| — | An audit report confirming the reliability of financial statements if they are subject to mandatory audit. |

Basic rules for preparing reports under IFRS and RAS:

Reporting period

– in it the company can prepare financial statements for the year ending on any date (clause 36 of IAS 1).

For example, the reporting year of company N... begins on October 1 and ends on September 30. If we look at paragraph 37 of IAS 1, we will see that companies are allowed to prepare financial statements for a period of 52 weeks (that is, 364 days). After all, the calendar year contains a non-integer number of weeks (approximately 52.14 weeks), and it is inconvenient for some companies to prepare reports for this period.

Chart of accounts and reporting forms -

As we know, there is no single approved or recommended chart of accounts. Each company reporting under IFRS develops its own chart of accounts based on the specifics of its activities and the required detail of financial information. At the same time, a company can use the Chart of Accounts of Russian accounting for IFRS purposes if it prepares international reporting using the transformation method. There are also no approved forms of financial reporting in IFRS. Instead, IAS 1 Presentation of Financial Statements provides general guidance on the structure of financial statements and minimum requirements for their content.

Composition of financial statements

— in IFRS the same as in RAS. Only the names of some forms differ, for example, the Russian balance sheet in IFRS corresponds to the statement of financial position, and the statement of financial results corresponds to the statement of comprehensive income. The statement of changes in equity and the statement of cash flows (CDFS) in IFRS are called the same as in Russian accounting. The composition of reporting under Russian legislation is presented in accordance with the regulations of the Ministry of Finance of the Russian Federation. It should be noted that the Federal Law “On Accounting” provides for the following composition of financial statements: balance sheet; income statement; appendices to them provided for by regulations; an auditor's report confirming the reliability of the organization's financial statements, if they are subject to mandatory audit in accordance with federal laws; explanatory note. Consequently, federal law considers the statement of changes in equity and the statement of cash flows as part of the schedules to the balance sheet and income statement. It is interesting that the audit report was included in the reporting according to Russian standards. Many experts emphasize the incorrectness of such inclusion, since it turns out that the audit report must contain an opinion, including about itself.

Difference in terminology:

International standards are financial reporting standards, while in Russian practice reporting is called accounting.

The issue of compliance with IFRS reporting requires special attention. Financial statements comply with IFRS if

they are prepared in accordance with all standards and interpretations, as appropriate. Compliance with IFRSs must be reflected in the financial statements, compliance with IFRSs means that the statements satisfy all the requirements of each applicable standard, and if the financial statements cannot be characterized as complying with IFRSs, there are any material departures from the standards and their interpretations in relation to accounting and disclosure of information. The presence of national standards that contradict IFRS, as well as the disclosure of accounting policies and the inclusion of relevant explanations in the financial statements, are not considered to justify deviations from the requirements of IFRS.

In exceptional situations

A departure from IFRS may be necessary. Such situations arise when the application of international standards may lead to distortion of information about individual business transactions. In this case, the financial statements must contain: the opinion of the company’s management on the need for deviations from IFRS; a detailed explanation of why the application of these standards may lead to misstatements; a description of the rule prescribed by IFRS and the accounting scheme actually used; assessment of the impact of this deviation on the amount of assets, liabilities, capital, profit (loss) and cash flows for each period presented in the statements. Knowledge of all facts of deviations from IFRS allows the user to form his own opinion on the statements and calculate the amount of amendments necessary to bring the statements into compliance with IFRS. An important role of the rule belongs to auditors, who are required to express an opinion on whether the statements are truly prepared in accordance with IFRS, i.e. verify and confirm that the reporting meets all the requirements of each individual standard. IFRS establish a fairly strict approach to the choice of accounting policies. In this process, the company must focus on the rules prescribed by IFRS; in the absence of those for individual transactions, the company’s management develops an accounting policy, using which the financial statements will contain complete and unbiased information necessary for users to make decisions that reliably reflect the results of operations and position of the company, and the economic content of transactions (rather than their legal form). In the absence of specific requirements for individual transactions, it is necessary to focus on the requirements adopted for similar transactions and the general principles of the IFRS system. It is also possible to use industry accounting rules and standards issued by other authorities, but only to the extent that their requirements do not contradict IFRS, which makes it possible to apply US GAAP, since the latter contains detailed accounting rules for many complex transactions.

Thus,

The IFRS approach is designed to eliminate overly broad interpretations of the standards, as well as situations where published financial statements purport to be prepared in accordance with IFRS when, in fact, not all of the requirements of the standards have been met. Most often, such situations arise in relation to disclosure requirements (related party transactions, geographic and operating segments).

Next week we will create a “Balance Sheet (Form No. 1) taking into account the Formation Features under IFRS.”