Responsibilities of the income tax payer

The responsibilities of income tax payers are:

- calculation and payment of income tax (subclause 1, clause 1, Article 23, Articles 286 and 287 of the Tax Code of the Russian Federation) ( see also “What you need to know about the deadlines for paying taxes” );

- maintaining tax records (subclause 3, clause 1, article 23, article 313 of the Tax Code of the Russian Federation) ( see “How to independently develop tax registers for income tax?” );

- submission of tax returns based on the results of reporting and tax periods (subclause 4, clause 1, article 23, clause 1, article 289 of the Tax Code of the Russian Federation) ( see “What are the deadlines for filing income tax returns?” );

- submission of documents provided for by the norms of Chapter. 25 of the Tax Code of the Russian Federation (clause 6, clause 1, article 23 of the Tax Code of the Russian Federation);

- other general obligations of taxpayers (Article 23 of the Tax Code of the Russian Federation) ( see also “What are the fines for income tax (amounts and violations)?” ).

All information about income tax can be found in the Tax Guide from ConsultantPlus:

If you don't have access to the system, get a free trial online.

Subject of taxation

The subject of taxation refers to persons who are charged by the Tax Code of the Russian Federation with the obligation to pay a particular tax.

The main category of taxation subjects are taxpayers and fee payers. Taxpayers and payers of fees are organizations and individuals who, in accordance with the Tax Code of the Russian Federation, are obliged to pay taxes and (or) fees, respectively.

In accordance with the Tax Code of the Russian Federation, since January 1, 1999, branches and representative offices of Russian legal entities are not considered as participants in tax legal relations and do not have the status of taxpayers, tax agents and other obligated persons. Accordingly, branches and representative offices cannot be subject to taxation either. In addition, since January 1, 1999, responsibility for the fulfillment of all obligations to pay taxes, fees, penalties and fines lies with the legal entity that includes the corresponding branch (representative office).

In accordance with the procedure provided for by the Tax Code of the Russian Federation, branches and other separate divisions of Russian organizations fulfill the obligations of these organizations to pay taxes and fees at the location of these branches and other separate divisions.

The responsibility for calculating and paying taxes is not always assigned to direct taxpayers. In some cases, in particular when paying personal income tax, the responsibility for accrual and transfer of calculated tax amounts to the budget is assigned to other, according to the legislator, more competent persons, called tax agents.

Tax agents are persons who, in accordance with the Tax Code of the Russian Federation, are entrusted with the responsibility for calculating, withholding from the taxpayer and transferring taxes to the appropriate budget (extra-budgetary fund). This is discussed in more detail in Chap. VI “Tax legal relations”.

Who doesn't pay income tax

The Tax Code of the Russian Federation in 2022 provides 1 basis for non-payment of income tax: if it is exempt from it.

Those exempt from income tax include:

- organizations applying special tax regimes (Unified Agricultural Tax, UTII, STS), and gambling business organizations;

- participants of the “Innovative” project, subject to the conditions provided for in Art. 246.1 Tax Code of the Russian Federation.

Let's consider each of the cases in more detail.

See also “What corporate income tax benefits are established for 2019-2020?”

Temporary benefits for cultural and art organizations

Law No. 305-FZ established income tax benefits for cultural and art organizations. Such organizations:

- are exempt from the obligation to calculate and pay advance payments and submit income tax returns for the reporting periods 2022 and 2022;

- pay income tax for the tax periods 2022 and 2022. no later than March 28, 2022.

This applies to organizations carrying out:

- creative activities, activities in the field of art and entertainment (OKVED code 90);

- activities of libraries, archives, museums and other cultural objects (OKVED code 91).

The activities carried out by the organization are determined by the code of the main type of economic activity in accordance with OKVED, contained in the Unified State Register of Legal Entities as of December 31, 2020.

Corresponding changes have been made to Articles 286, 287, 289 of the Tax Code of the Russian Federation, which are in force from 08/02/2021 (clause 44, paragraph “b”, clause 46, clause 47 of Article 2, clause 2 of Article 10 of Law No. 305- Federal Law).

Please note that the tax amount for 2022 and advance payments for the first quarter and half of 2022 can be paid by the taxpayer. We believe that in this case he has the right to return these amounts from the budget or offset them against upcoming other payments to the budget (for example, for other taxes) according to the rules of Article 78 of the Tax Code of the Russian Federation.

Special regime as an exemption from income tax

Exemption from income tax is provided by:

- taxation system for agricultural producers (clause 3 of article 346.1, clause 10 of article 274 of the Tax Code of the Russian Federation);

- simplified taxation system (clause 2 of article 346.11, clause 10 of article 274 of the Tax Code of the Russian Federation);

- taxation system in the form of a single tax on imputed income for certain types of activities (clause 4 of article 346.26, clause 10 of article 274 of the Tax Code of the Russian Federation);

- tax on gambling business (clause 9 of article 274 of the Tax Code of the Russian Federation).

See also “How can an organization choose a taxation regime: OSN, simplified tax system or UTII?”

The first 2 regimes (Unified agricultural tax and simplified tax system) exempt the organization from paying income tax in relation to all its activities. However, such “special regimes” retain the obligation to pay income tax on income in the form of dividends and interest on state and municipal securities (clause 3 of Article 346.1, clause 2 of Article 346.11 of the Tax Code of the Russian Federation).

“Imputement” and the tax on the gambling business allow you not to pay income tax only in relation to those types of activities that fall under these special regimes (clause 4 of article 346.26, clause 9 of article 274 of the Tax Code of the Russian Federation). If an organization combines them with a “general regime” business, the tax on it is paid in the general manner on the basis of separate accounting of income and expenses ( see “How to organize separate accounting for UTII” ).

And of course, none of the specified special tax regimes provides exemption from paying income tax as a tax agent (clauses 3 and 6 of Article 275, clauses 4 and 5 of Article 286, Article 310, clause 4 of Art. 346.1, paragraph 5 of Article 346.11 of the Tax Code of the Russian Federation):

- on dividends ( see “How to correctly calculate income tax on dividends?” );

- for certain income paid to foreign organizations ( see “Tax agent for income tax when paying income to a foreign organization” ).

On confirmation of payment to a permanent representative office of a foreign organization

As is known, the duties of a tax agent for income tax when paying income to a foreign organization do not arise if this income relates to its permanent establishment. To confirm this, the source of income must have a copy of the certificate of registration of the recipient of income for tax registration in the Russian Federation, notarized no earlier than in the previous tax period (clause 1, clause 2, article 310 of the Tax Code of the Russian Federation).

From 08/02/2021, the tax agent only needs to have a copy of the above document. There is no need to notarize it (clause 49, article 2, clause 2, article 10 of Law No. 305-FZ).

We believe that now it must be certified by the recipient of the income (a foreign organization represented by its permanent representative office).

Freeing up to innovate

Organizations that have received the status of participants in a project to carry out research, development and commercialization of their results in accordance with Federal Law dated September 28, 2010 No. 244-FZ “On Innovation” can apply an exemption from the duties of income tax payers. The exemption is valid for 10 years from the date of receipt of project participant status. The procedure and conditions for applying the exemption are established by Art. 246.1 Tax Code of the Russian Federation.

The exemption can be used from the first day of the month following the month in which the status of a project participant was obtained (clause 4 of Article 246.1 of the Tax Code of the Russian Federation).

The tax authority must be notified of its use. To do this, no later than the 20th day of the month following the month from which the exemption is used, the following must be sent to the inspectorate at the place of registration (clauses 4, 7 of Article 246.1 of the Tax Code of the Russian Federation):

- written notification (in the form approved by order of the Ministry of Finance of Russia dated December 30, 2010 No. 196n, Appendix No. 1);

- documents confirming the status of a participant in the Skolkovo project;

- an extract from the book of income and expenses (financial performance report), confirming the annual volume of revenue from the sale of goods (work, services, property rights). The volume of revenue should not exceed 1 billion rubles (clause 2 of Article 246.1 of the Tax Code of the Russian Federation).

The same documents should be submitted to the inspectorate at the end of the tax period in which the exemption was used, along with a notice of extension of the use of the right to exemption for the next period or refusal of the exemption. The deadline for sending is no later than the 20th day of the month following the tax period in which the exemption was applied (clause 6 of Article 246.1 of the Tax Code of the Russian Federation).

If the documents are not sent or contain false information, you need to restore the income tax, pay it to the budget, and also transfer penalties. According to the Ministry of Finance, organizations that submit documents later than the deadline should do the same (letter of the Ministry of Finance of Russia dated June 20, 2012 No. 03-03-06/1/316).

See also “How to calculate and reflect penalties for income tax?”

The right to release can be lost for 2 reasons (clause 2 of article 246.1 of the Tax Code of the Russian Federation):

- in case of loss of the status of a project participant - from the first day of the tax period in which such status was lost;

- if the annual revenue exceeds 1 billion rubles - from the first day of the tax period in which the specified excess occurred.

The tax for the tax period in which the status of a project participant was lost or the total amount of profit received by a project participant exceeded 300 million rubles will have to be restored and paid to the budget with the corresponding penalties (clause 3 of Article 246.1 of the Tax Code of the Russian Federation).

Voluntary refusal of release is also possible (clause 5 of Article 246.1 of the Tax Code of the Russian Federation). To refuse it, you need to send to the inspectorate the notification provided for by Order of the Ministry of Finance of the Russian Federation dated December 30, 2010 No. 196n (Appendix No. 1). This should be done no later than the first day of the tax period from which the waiver of exemption is planned. However, it must be remembered that someone who has repeatedly refused it will no longer be able to obtain exemption.

In 2012-2018, certain categories of taxpayers were exempt from paying income tax. These included organizations associated with:

- holding the XXII Olympic and XI Paralympic Games 2014 in Sochi;

- holding the 2022 FIFA World Cup and the 2022 FIFA Confederations Cup in the Russian Federation.

Let's consider this point in more detail.

Defaulters - “Sochi residents”

This category of profit tax evaders includes organizations that are (clause 2 of Article 246 of the Tax Code of the Russian Federation):

- Foreign organizers of the XXII Olympic Winter Games and XI Paralympic Winter Games 2014 in Sochi, in accordance with Art. 3 of Federal Law No. 310-FZ of December 1, 2007 (the preference is valid in the period 2008–2016).

- Foreign marketing partners of the International Olympic Committee (IOC), in accordance with Art. 3.1 of Law No. 310 (in the period 2010–2016) - in relation to income received in connection with the organization and holding of the Olympic and Paralympic Games.

- Official broadcasting companies, in accordance with Art. 3.1 of Law No. 310, - in relation to income received under contracts concluded with the IOC or an organization authorized by it:

- from the production of media products during the organization of the games (from July 5, 2007 to December 31, 2016);

- from the production and distribution of media products (including official television and radio broadcasting, including digital and other communication channels) during the period of the Games (1 month before the start of the opening ceremony of the Olympic Games, the time of the Games and 1 month after the end of the closing ceremony Paralympic Games).

Clause 1 of Article 246 of the Tax Code of the Russian Federation

Taxpayers of corporate income tax (hereinafter in this chapter - taxpayers) are recognized as: (As amended by Federal Law No. 310-FZ of December 1, 2007)

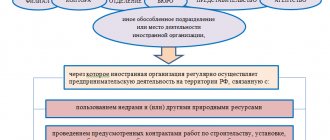

Russian organizations;

foreign organizations operating in the Russian Federation through permanent representative offices and (or) receiving income from sources in the Russian Federation.

Organizations that are responsible participants in a consolidated group of taxpayers are recognized as taxpayers with respect to corporate income tax for this consolidated group of taxpayers. (Paragraph introduced - Federal Law of November 16, 2011 No. 321-FZ)

Participants in a consolidated group of taxpayers perform the duties of corporate income tax taxpayers for the consolidated group of taxpayers to the extent necessary for its calculation by the responsible participant in this group. (Paragraph introduced - Federal Law of November 16, 2011 No. 321-FZ)

Defaulters - “football players”

In respect of income received in connection with the preparation and holding of the 2022 FIFA World Cup and the 2022 FIFA Confederations Cup, income tax is not paid:

- FIFA and its subsidiaries specified in Federal Law dated 06/07/2013 No. 108-FZ;

- confederation,

- national football associations,

- FIFA media producers,

- suppliers of goods (works, services) to FIFA, specified in Law No. 108 and being foreign organizations.

Clause 3 of Article 246 of the Tax Code of the Russian Federation

(Clause introduced - Federal Law dated September 28, 2010 No. 243-FZ; repealed - Federal Law dated November 28, 2011 No. 339-FZ)

4. UEFA (Union of European Football Associations) and subsidiaries of UEFA for the period up to December 31, 2022 inclusive, FIFA (Federation Internationale de Football Association) and subsidiaries of FIFA, defined by the Federal Law “On preparation and conduct in the Russian Federation”, are not recognized as taxpayers the 2022 FIFA World Cup, the 2022 FIFA Confederations Cup, the 2020 UEFA European Football Championship and amendments to certain legislative acts of the Russian Federation.”

Confederations, national football associations, producers of FIFA media information, suppliers of goods (works, services) of FIFA, commercial partners of UEFA, suppliers of goods (works, services) of UEFA and broadcasters of UEFA defined by the Federal Law “On the preparation and holding of the championship in the Russian Federation” are not recognized as taxpayers FIFA World Cup 2022, FIFA Confederations Cup 2022, UEFA European Football Championship 2022 and amendments to certain legislative acts of the Russian Federation" and being foreign organizations, in relation to the income received by them from activities related to the implementation of activities provided for specified by Federal Law.

(Clause introduced - Federal Law dated 06/07/2013 No. 108-FZ) (As amended by Federal Law dated 05/01/2019 No. 101-FZ)

Results

So, we found out that income tax payers are organizations and not individual entrepreneurs.

All Russian organizations must pay income tax, with the exception of those that:

- exempt from its payment due to the use of special tax regimes;

- use the Skolkovo exemption.

Also, some foreign organizations are payers, for some of which there are also a number of preferences.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.