Drawing up and processing of incoming and outgoing cash orders

Both PKO and RKO are cash documents that record the receipt and movement of funds at the cash desk. The cash desk, in turn, is understood as a whole system of all accounting operations within an enterprise.

PKO is filled out:

- At the time of depositing funds into the cash register. Sale of a product or service when the client pays the price according to the price list. In this case, the buyer receives a check, a receipt, and the seller keeps the corresponding completed document, which will become a reporting measure. But in most enterprises, each individual transaction is not subject to registration; only the total receipt at the end of the entire shift is recorded.

- To contribute finance to the authorized capital.

- To return unused issued funds.

- To fulfill debt obligations to the company.

Open a business account in SEA BANK and receive up to 6% on your account balance!.

The details of PKO and RKO are similar to each other, but with the help of an incoming cash order, the receipt of funds is recorded, and an outgoing cash order controls the issuance of money. Accordingly, the types of activities are used in radically opposite situations:

- When submitting the total proceeds to the bank at the end of a certain session, which is established by the regulations for the functioning of the enterprise.

- For the issuance of accountable funds. In fact, this is the transfer of finances to a company employee or a person representing its interests for a certain period of time to carry out management tasks. This procedure is strictly recorded in the documentation, where the name and surname, as well as the position (if any) of the accountable person are written down. The purpose of the funds received is also indicated there.

- If there is a need for any unplanned purchases, expenses, acquisitions on behalf of the enterprise itself.

- To issue compensations, bonuses, advances and other forms of employee incentives.

The corporate card of SEA BANK Visa Business is a convenient means of organizing and controlling entertainment and travel expenses for company employees.

Is it necessary to issue a cash receipt order?

In accordance with information from the Ministry of Finance No. PZ-10/2012, Russian organizations have the right not to use forms of accounting documents contained in albums of unified forms of relevant sources. One of the albums of this type is included in the structure of Resolution No. 88, and it reflects the KO-2 form.

At the same time, in accordance with the same source, forms of documents that are approved by authorized structures on the basis of federal laws remain mandatory. Thus, in accordance with clause 4.1 of the Bank of Russia Directive No. 3210-U dated March 11, 2014, cash transactions must be formalized by business entities using cash outgoing orders corresponding to number 031002 according to the OKUD classifier, that is, exactly those provided for by Resolution No. 88.

In accordance with Art. 34 of the Law “On the Central Bank of the Russian Federation” dated July 10, 2002 No. 86, the Bank of Russia has the right to establish the procedure for conducting cash transactions for legal entities in general, as well as a simplified procedure for individual entrepreneurs and small businesses. Therefore, all taxpayers with the status of legal entities, entrepreneurs and small businesses are required to follow the provisions of Directive No. 3210-U. Thus, the legislation requires Russian organizations to use exactly the form of cash receipt order that is established by Resolution No. 88.

However, individual entrepreneurs who, in accordance with the legislation of the Russian Federation on taxes and fees, keep records of income or income and expenses or physical indicators characterizing a certain type of business activity, may not draw up cash documents and a cash book (clauses 4.1, 4.6 of Directive No. 3210-U) . Thus, if an entrepreneur takes into account the movement of business funds in the books of income (and expenses), then he may not formalize cash settlements.

Read more about cash discipline here.

Journal of registration of expenditure and receipt documentation

Such a document can exist in both physical (paper) and electronic form. The law does not regulate a single mandatory form. But if the document at the enterprise is in paper form, then it is worth knowing a few key rules. Firstly, each page must be strictly numbered and signed by the responsible persons. And, secondly, all pages must be a single form, that is, be bound.

At the moment, the Tax Code and other legal acts (regulatory legal acts) do not oblige entrepreneurs to maintain such a journal. It serves for comfortable submission of reports, as well as quick search for necessary documents. The procedure prescribed by law for filling out the PKO and RKO also does not apply to the journal.

This means that each manager himself decides whether to keep such a journal or not.

Account book

An accounting book is a set of documentation that records all movements of funds within and outside the enterprise. Keeping a book is an easy way to combine all the information in one form. Unlike the previous magazine, this is a more general concept. You could say that the journal is included in the book and is not required. But you will need an account book in any case.

All monetary transactions are recorded on the basis of receipts or expenditures. Moreover, each is signed by the responsible person, has its own date in a single format, and is then entered into the book by hierarchical sorting.

We have clarified what operations are processed using PKO, RKO. But not only they act as content for this reporting document. This also includes cash receipts and expense documentation.

Control of operations that are carried out to deposit new funds into the company’s account or, on the contrary, manage outflows is an important point for any company. Without this form of reporting it is impossible to conduct normal business activities.

MARINE BANK offers to use trade acquiring services. Accept payments for goods and services by bank cards.

Filling rules

The accounting book is a set of standard sheets that are formed from orders. The completed PKO and RKO are sent here, stapled in paper form or copied electronically. The book also contains a table that records all receipts and expenses throughout the entire reporting period, which is equal to a calendar year. Based on the table, you can not only summarize the reporting results, but also conduct a kind of financial analysis.

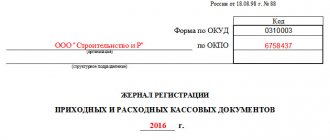

Traditionally, the first page of the documentation is the title page. It consists of:

- The full name of the legal entity on the basis of which the book is being filled out.

- OKPO - All-Russian Classifier of Enterprises and Organizations.

- Names of the division, branch or department. Often, reporting is carried out not for the entire company as a whole, but for its structural division. In this case, its name and number are also spelled out in full. If reporting goes throughout the entire enterprise, then you can safely skip this line.

- Date of. It is noteworthy that in this paragraph it is enough to attribute only the year. After all, according to the rules, the book opens at the beginning of the reporting period. And information stops being entered at the end of it. This means that there is no need to indicate any specific dates, only the year.

- The name and initials of the person who maintains this book. And this can only be one person, but it is permissible to delegate these powers without prejudice.

We know that PKO and RKO are issued based on the receipt or expenditure of funds. Accordingly, the main person who is involved in the collection of this kind of statements is the chief accountant. It is he who, according to the regulations, is required to keep the accounting book. But in practice, in almost all cases, he delegates powers to an assistant or other employees on the basis of a legal power of attorney or simply an order from the manager. This frees up the specialist’s working time, which he can effectively use for the benefit of the company. And routine moments are transferred to other workers.

Fines in case of improper storage or loss of the magazine

The responsible person is the chief accountant. But instead of him, any other accounting employee can also be appointed by order of the manager. The authorized employee bears personal financial responsibility. This aspect is fixed by a special act, an agreement concluded between him and the organization. The responsible employee is also required to ensure proper storage conditions for the journal. Filling out and maintaining incoming and outgoing cash orders is the responsibility of other persons: cashiers, managers, and accounting staff. The person responsible for the accounting book rarely personally fills out cash registers and cash registers.

General information about the storage periods for primary documents is contained in Art. 29 of the Federal Law of December 6, 2011 No. 402-FZ. This part of the legislation states that primary documentation must be stored for at least five years. Plus, if any conflict situation arises that is regulated by legal proceedings, then at the time the case is opened, the document must also be stored, even if the period of 5 years has already passed.

For the loss or modification of data, a fine is imposed: separately for the responsible person and for the entire organization as a whole. If an employee is required to pay only 5 or 6 thousand rubles, then the company will have to pay 40-50 thousand.

SEA BANK offers you to use a convenient banking system. Manage your business from anywhere in the world. Secure access to your accounts is always in your pocket.

Which sources of law provide a sample of filling out an expense cash order?

Filling out an expense cash order is not regulated by federal law. Resolution No. 88 provides brief instructions regarding the application and completion of the RKO form:

- the contents of the operation must be recorded in the “Base” line of the order;

- the “Attachment” line should reflect the list of attached documents.

Instruction No. 3210-U contains the following information on filling out cash receipts:

- The cashier checks for the signature of the chief accountant or accountant, and if they are absent, for the signature of the manager. When registering a cash settlement on paper, the signatures must match the sample.

- The correspondence of the cash amounts entered in figures with the amounts entered in words is checked.

- The cashier checks the presence of supporting documents listed in the cash register.

- Cash issuance is carried out by the cashier directly to the recipient specified in the cash settlement or power of attorney. The recipient is identified by an identification document, usually a passport. The cashier checks the information about the recipient of the money in the cash register with the information on the identity document.

- The recipient of the funds must sign the cash settlement; if the order is drawn up in electronic form, then it can be signed with an electronic signature.

Journal in form KO-3

It must necessarily reflect all orders reflecting information about the receipt and disbursement of funds. After all, PKO and RKO are primary documents; tax reporting is generated on their basis.

In addition to them, various bills for payment of expenses, expenses or reimbursements, compensations are also entered into the book. Accompanying documentation (checks or receipts) are not stored in the journal.

The magazine itself is usually divided into two parts. The first is designed to record all orders aimed at receiving funds. The second, as you might guess, reflects consumption. Both of them contain a table, as well as each of the designated orders separately.

Example of a completed journal

Form KO-3 is quite simple to fill out and usually does not cause any difficulties even for persons who have not previously dealt with it. The papers should be filled out strictly according to the model, because any changes will entail the complete destruction of the book and entering all the data from scratch. From the point of view of tax authorities, incorrect information deprives the document of legal force. Therefore, papers with corrections are treated as missing.

On each page you need to enter:

- The date on which a particular order was printed or written.

- Its number is in a serial value, which is assigned specifically in the journal.

- The full amount of money that was allocated or received at the cash desk.

- Reason or other additional information that will be important for further reporting. For example, for what needs were funds allocated, or on the basis of what transactions were received at the cash desk.

How to keep records and how much to store

Registration and accounting of the cash receipt order is carried out in the registration journal in the KO-3 form, as well as in the cash books (KO-4). The serial numbers of the RKO are entered into the journal. This must be done after they are signed by the chief accountant or director. The journal must be kept in the accounting department of the enterprise or with the director.

Journal KO-3 (form according to OKUD 0310003) is a cover in which the registration data of the institution and a loose leaf are filled out. Two tables are formed on the insert sheet: the left one displays information on PKO, and the right - on RKO.

Incoming and outgoing KOs are stored for 5 years according to the rules established by the head of the organization.

Assurance

Orders of both incoming and outgoing nature must be certified by signatures. The journal itself is not subject to signature by other employees, not counting the responsible person. If the journal was compiled by a cashier after a shift, then when handing over the proceeds, someone from the accounting department usually signs it. When these powers have not been delegated in advance, a person must be appointed by order. Without appointing a responsible person, it is permissible to leave orders, while signing in the accounting book or on the documents themselves only with a written transfer of authority.

Printing on orders

It is mandatory. Both a seal and a stamp are suitable, depending on what is used in the enterprise. The main feature is that the seal is placed simultaneously on the receipt accompanying the receipt and issue of funds, and on the order itself. And in such a way that the edge of the drawing touches both papers.

How to work with PKO and RKO

The procedure is simple:

- The transaction is completed and a receipt is sent.

- Formed in electronic or paper form.

- The date, amount, basis and subject (accountable person) are entered.

- Certified by the signature of an authorized employee.

- The documentation is submitted for inclusion in the book and the formation of primary financial statements.

SEA BANK (JSC) projects for salary transfer can be convenient and interesting for any enterprises and organizations, regardless of the number of employees working in them.

Electronic document management

Makes the accounting department's life much easier. It is worth remembering that in order to certify a document, it must be printed in a physical format. Regarding sending a document to the tax service, the document signed with an electronic key is already certified.

What is the penalty for missing cash documents?

For the lack of primary documentation, the tax service imposes serious fines. In some cases, subsidiary liability of employees is possible.

How to correct an error in a receipt or debit order

The algorithm is very simple. It is necessary to dispose of the existing document and create it again. Yes, this may seem like a time-consuming action, however, there is no alternative. Corrections or changes are not permitted in the primary documentation. If they exist, the documents lose their legal force, and the Federal Tax Service interprets the correction as a complete lack of reporting, imposing appropriate fines on the organization. For small individual entrepreneurs, an amount of 40-50 thousand rubles will become, although not critical, very unpleasant.

How to properly report money

When issuing cash to report on a cash receipt order, the accountant must adhere to certain rules established by the procedure for conducting cash transactions (clause 6 of the instruction of the Central Bank of the Russian Federation dated March 11, 2014 No. 3210-U).

Let's consider the main steps when issuing money:

- An application is accepted from the employee, which contains a request for the payment of a certain amount for a specified period, written in free form addressed to the manager. The manager's decision, signature and date are checked. Instead of an application, a completed administrative document (instruction/order) can be submitted to the accounting department. Such a statement (instruction/order) serves as the basis for issuing money for reporting.

ATTENTION! From November 30, 2020, an administrative document can be drawn up for several cash payments to one or more employees. In this case, you need to indicate the name, amount and period for which the money is issued for each employee.

You can learn about the new procedure for recording cash transactions from ConsultantPlus. Get trial access to the K+ system and proceed to the explanations for free.

IMPORTANT! From August 19, 2017, the absence of debt on accountable amounts is not a limitation for receiving a new advance (clause 1.3 of instruction No. 4416-U).

- Next, a cash receipt order is issued in a single copy. Signed by an accountant or manager (if there is no accountant and he (the manager) combines the position of accountant and manager).

- The completed RKO, together with the application, is handed over to the cashier, who checks all items of the consumables for correct filling, and checks them with the document - the grounds for issuance.

- The cashier prepares the money, verifies the identity of the accountant using the passport received from him, and hands him the cash register for signature.

- After the employee signs the cash order, the cashier issues the money and puts his signature in the cash register.

- An entry is then made in the cash book.

IMPORTANT! Individual entrepreneurs, in accordance with the instructions of the Central Bank of the Russian Federation No. 3210-U, from 06/01/2014 may, at their own discretion, not issue receipts and expenditure orders and not maintain a cash book.