Drawing up and processing of incoming and outgoing cash orders

Both PKO and RKO are cash documents that record the receipt and movement of funds at the cash desk. The cash desk, in turn, is understood as a whole system of all accounting operations within an enterprise.

PKO is filled out:

- At the time of depositing funds into the cash register. Sale of a product or service when the client pays the price according to the price list. In this case, the buyer receives a check, a receipt, and the seller keeps the corresponding completed document, which will become a reporting measure. But in most enterprises, each individual transaction is not subject to registration; only the total receipt at the end of the entire shift is recorded.

- To contribute finance to the authorized capital.

- To return unused issued funds.

- To fulfill debt obligations to the company.

Open a business account in SEA BANK and receive up to 6% on your account balance!.

The details of PKO and RKO are similar to each other, but with the help of an incoming cash order, the receipt of funds is recorded, and an outgoing cash order controls the issuance of money. Accordingly, the types of activities are used in radically opposite situations:

- When submitting the total proceeds to the bank at the end of a certain session, which is established by the regulations for the functioning of the enterprise.

- For the issuance of accountable funds. In fact, this is the transfer of finances to a company employee or a person representing its interests for a certain period of time to carry out management tasks. This procedure is strictly recorded in the documentation, where the name and surname, as well as the position (if any) of the accountable person are written down. The purpose of the funds received is also indicated there.

- If there is a need for any unplanned purchases, expenses, acquisitions on behalf of the enterprise itself.

- To issue compensations, bonuses, advances and other forms of employee incentives.

The corporate card of SEA BANK Visa Business is a convenient means of organizing and controlling entertainment and travel expenses for company employees.

The concepts of “cash register” and “cash register”: essence and differences

First, a little theory. Let’s start our discussion with the concepts of “cash register” and “cash register”. Most mistakes and misconceptions are due precisely to the fact that their meaning is often confused.

So, the cash desk is all transactions of an individual entrepreneur (or organization) carried out in cash. These can be either income transactions (receipt of income) or expenditure transactions (spending funds for various purposes). All cash transactions must be recorded on cash register. In fact, all individual entrepreneurs and organizations have a cash register; exceptions are very rare: even if all transactions are carried out by bank transfer, you can withdraw money for some business expenses, for example, for the purchase of office supplies.

“Cashier” is a kind of imaginary “wallet” where money comes in and where it comes from for expenses. For organizations, the concept of “cash” looks easier to understand, since in accounting according to the chart of accounts there is a special account 50 “Cash”, which records all cash transactions.

Cash register is a cash register equipment necessary for making cash payments for goods (or services) sold to a client, that is, the machine itself, which issues a check.

The definition from the law generally goes like this:

Cash register equipment - electronic computers, other computer devices and their complexes that provide recording and storage of fiscal data in fiscal drives, generate fiscal documents, ensure the transfer of fiscal data and print fiscal documents on paper in accordance with the rules established by the legislation of the Russian Federation on application of CCT.

Let's immediately note the important differences:

- According to the cash register, only cash received from customers for goods or services purchased from you is recorded; at the cash register, all cash receipts are considered receipts - revenue from the cash register for the day, withdrawals of money from the current account, and so on.

- You cannot spend money from the cash register - there is no expense part, money for expenses can be issued exclusively from the cash register.

Conclusion: cash register is not equivalent to cash register - these are different concepts that mean different things. Cash desk is all cash transactions of an entrepreneur or organization (a kind of “big wallet”), cash register is the actual machine for accepting money from a client and issuing a check. The connection between the two concepts can be easily shown: at the end of the day, the store’s revenue from the cash register is handed over to the cash register of the individual entrepreneur (organization), the transaction is formalized by the receipt.

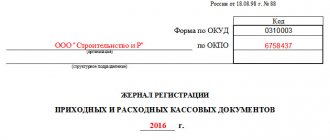

Journal of registration of expenditure and receipt documentation

Such a document can exist in both physical (paper) and electronic form. The law does not regulate a single mandatory form. But if the document at the enterprise is in paper form, then it is worth knowing a few key rules. Firstly, each page must be strictly numbered and signed by the responsible persons. And, secondly, all pages must be a single form, that is, be bound.

At the moment, the Tax Code and other legal acts (regulatory legal acts) do not oblige entrepreneurs to maintain such a journal. It serves for comfortable submission of reports, as well as quick search for necessary documents. The procedure prescribed by law for filling out the PKO and RKO also does not apply to the journal.

This means that each manager himself decides whether to keep such a journal or not.

Important information

The vast majority of parcels to Russia come from China. Obviously, the lion's share comes from purchases on special Internet sites.

It is also worth noting that the services of MR LC Vnukovo are often used by government agencies and other legal entities of the Russian Federation, including financial institutions, commercial and non-profit companies.

In this case, the shipment can contain both simple printed correspondence and a weighty parcel post - you can clarify this point on the notice itself, where the weight of the shipment is indicated. Therefore, if the document states up to 25-30 grams, then it is a simple envelope.

It should also be noted that another abbreviation is quite often assigned to the MR LC Vnukovo - DTI or additional technological index.

Account book

An accounting book is a set of documentation that records all movements of funds within and outside the enterprise. Keeping a book is an easy way to combine all the information in one form. Unlike the previous magazine, this is a more general concept. You could say that the journal is included in the book and is not required. But you will need an account book in any case.

All monetary transactions are recorded on the basis of receipts or expenditures. Moreover, each is signed by the responsible person, has its own date in a single format, and is then entered into the book by hierarchical sorting.

We have clarified what operations are processed using PKO, RKO. But not only they act as content for this reporting document. This also includes cash receipts and expense documentation.

Control of operations that are carried out to deposit new funds into the company’s account or, on the contrary, manage outflows is an important point for any company. Without this form of reporting it is impossible to conduct normal business activities.

MARINE BANK offers to use trade acquiring services. Accept payments for goods and services by bank cards.

What do we have in the source data?

- Cash register systems should be used by organizations and individual entrepreneurs if they make payments in cash, bank cards, or electronic means of payment;

- if all your sales go through a current account (non-cash payment), cash register is not used, as it is simply not needed;

- There are exceptions to the general rule when cash registers may still not be used: provision of services to the public (they may not use cash registers until 07/01/2021);

- specifics of activity or location;

- payment of tax on imputation or patent.

- We have already talked about all the exceptions in the previous article.

- Each of the exceptions to the CCP Law is accompanied by some condition, the fulfillment of which is mandatory (what must be issued instead of a check and how this document must be drawn up).

Conclusion: the main document that serves as confirmation of payment by the client for goods and services is a cash receipt. If the Cash Register Law obliges you to use a cash register, you are required to issue a check; if you may not use a cash register, but you have one (you fall under an exception, but do not use it) – you are required to issue a check.

It turns out that the presence of a cash register obliges the individual entrepreneur to issue the buyer a check, and not some other document. Let's talk about a few more situations:

- you must use a cash register, you have it, but you don’t knock out a check;

- you have the right not to use cash register, but you have it (you don’t use this right) and you don’t knock out a check;

- you must have a cash register, but you don’t have it, and therefore you cannot issue a check.

All these cases are classified as violations of the law. Failure to use cash registers and failure to punch a check are considered violations and will ensure that you are held accountable even when you do issue some document to the buyer (a certain form, a receipt from the PKO, and so on).

Everything is pretty clear here. Now let's get back to exceptions. Each of the exceptions to the CCP Law is accompanied by special requirements. These requirements are as follows:

- in a situation with the provision of services to the public (that is, individuals), cash register systems may not be used, but only on the condition that each client receives a completed BSO from the entrepreneur;

- when using UTII or a patent, you can do without a cash register, but issue a sales receipt or other document at the client’s request. These documents must contain all the details established by law;

- if the activity or location is specific, it is allowed not to issue anything at all.

Conclusion: what can be given to the buyer instead of a cash register receipt if there is no obligation to use a cash register? There are only three options:

- BSO;

- sales receipt or other document, but with a mandatory set of details;

- don't give anything away.

Filling rules

The accounting book is a set of standard sheets that are formed from orders. The completed PKO and RKO are sent here, stapled in paper form or copied electronically. The book also contains a table that records all receipts and expenses throughout the entire reporting period, which is equal to a calendar year. Based on the table, you can not only summarize the reporting results, but also conduct a kind of financial analysis.

Traditionally, the first page of the documentation is the title page. It consists of:

- The full name of the legal entity on the basis of which the book is being filled out.

- OKPO - All-Russian Classifier of Enterprises and Organizations.

- Names of the division, branch or department. Often, reporting is carried out not for the entire company as a whole, but for its structural division. In this case, its name and number are also spelled out in full. If reporting goes throughout the entire enterprise, then you can safely skip this line.

- Date of. It is noteworthy that in this paragraph it is enough to attribute only the year. After all, according to the rules, the book opens at the beginning of the reporting period. And information stops being entered at the end of it. This means that there is no need to indicate any specific dates, only the year.

- The name and initials of the person who maintains this book. And this can only be one person, but it is permissible to delegate these powers without prejudice.

We know that PKO and RKO are issued based on the receipt or expenditure of funds. Accordingly, the main person who is involved in the collection of this kind of statements is the chief accountant. It is he who, according to the regulations, is required to keep the accounting book. But in practice, in almost all cases, he delegates powers to an assistant or other employees on the basis of a legal power of attorney or simply an order from the manager. This frees up the specialist’s working time, which he can effectively use for the benefit of the company. And routine moments are transferred to other workers.

Where else is PKO FM available?

There are similar points in almost all major cities of the country. For example:

- Index 200961 corresponds to the St. Petersburg ASC post office;

- 660075 – Krasnoyarsk;

- 650000 – Kemerovo;

- 102961 – OPS MR LC Vnukovo;

- 603094 – Nizhny Novgorod;

- 140961 – Moscow region.

Note! All notifications contain a cut-off coupon in which you can indicate what data was entered inaccurately; if in doubt, you can call your tax office’s phone number.

Fines in case of improper storage or loss of the magazine

The responsible person is the chief accountant. But instead of him, any other accounting employee can also be appointed by order of the manager. The authorized employee bears personal financial responsibility. This aspect is fixed by a special act, an agreement concluded between him and the organization. The responsible employee is also required to ensure proper storage conditions for the journal. Filling out and maintaining incoming and outgoing cash orders is the responsibility of other persons: cashiers, managers, and accounting staff. The person responsible for the accounting book rarely personally fills out cash registers and cash registers.

General information about the storage periods for primary documents is contained in Art. 29 of the Federal Law of December 6, 2011 No. 402-FZ. This part of the legislation states that primary documentation must be stored for at least five years. Plus, if any conflict situation arises that is regulated by legal proceedings, then at the time the case is opened, the document must also be stored, even if the period of 5 years has already passed.

For the loss or modification of data, a fine is imposed: separately for the responsible person and for the entire organization as a whole. If an employee is required to pay only 5 or 6 thousand rubles, then the company will have to pay 40-50 thousand.

SEA BANK offers you to use a convenient banking system. Manage your business from anywhere in the world. Secure access to your accounts is always in your pocket.

Journal in form KO-3

It must necessarily reflect all orders reflecting information about the receipt and disbursement of funds. After all, PKO and RKO are primary documents; tax reporting is generated on their basis.

In addition to them, various bills for payment of expenses, expenses or reimbursements, compensations are also entered into the book. Accompanying documentation (checks or receipts) are not stored in the journal.

The magazine itself is usually divided into two parts. The first is designed to record all orders aimed at receiving funds. The second, as you might guess, reflects consumption. Both of them contain a table, as well as each of the designated orders separately.

Example of a completed journal

Form KO-3 is quite simple to fill out and usually does not cause any difficulties even for persons who have not previously dealt with it. The papers should be filled out strictly according to the model, because any changes will entail the complete destruction of the book and entering all the data from scratch. From the point of view of tax authorities, incorrect information deprives the document of legal force. Therefore, papers with corrections are treated as missing.

On each page you need to enter:

- The date on which a particular order was printed or written.

- Its number is in a serial value, which is assigned specifically in the journal.

- The full amount of money that was allocated or received at the cash desk.

- Reason or other additional information that will be important for further reporting. For example, for what needs were funds allocated, or on the basis of what transactions were received at the cash desk.

Assurance

Orders of both incoming and outgoing nature must be certified by signatures. The journal itself is not subject to signature by other employees, not counting the responsible person. If the journal was compiled by a cashier after a shift, then when handing over the proceeds, someone from the accounting department usually signs it. When these powers have not been delegated in advance, a person must be appointed by order. Without appointing a responsible person, it is permissible to leave orders, while signing in the accounting book or on the documents themselves only with a written transfer of authority.

Printing on orders

It is mandatory. Both a seal and a stamp are suitable, depending on what is used in the enterprise. The main feature is that the seal is placed simultaneously on the receipt accompanying the receipt and issue of funds, and on the order itself. And in such a way that the edge of the drawing touches both papers.

How to work with PKO and RKO

The procedure is simple:

- The transaction is completed and a receipt is sent.

- Formed in electronic or paper form.

- The date, amount, basis and subject (accountable person) are entered.

- Certified by the signature of an authorized employee.

- The documentation is submitted for inclusion in the book and the formation of primary financial statements.

SEA BANK (JSC) projects for salary transfer can be convenient and interesting for any enterprises and organizations, regardless of the number of employees working in them.

Electronic document management

Makes the accounting department's life much easier. It is worth remembering that in order to certify a document, it must be printed in a physical format. Regarding sending a document to the tax service, the document signed with an electronic key is already certified.

What is the penalty for missing cash documents?

For the lack of primary documentation, the tax service imposes serious fines. In some cases, subsidiary liability of employees is possible.

How to correct an error in a receipt or debit order

The algorithm is very simple. It is necessary to dispose of the existing document and create it again. Yes, this may seem like a time-consuming action, however, there is no alternative. Corrections or changes are not permitted in the primary documentation. If they exist, the documents lose their legal force, and the Federal Tax Service interprets the correction as a complete lack of reporting, imposing appropriate fines on the organization. For small individual entrepreneurs, an amount of 40-50 thousand rubles will become, although not critical, very unpleasant.

Decoding PKO FM

In this case, there is no need to doubt. Explanation of PKO FM – Collective Service Point for Franking Machine. But this doesn’t mean much to many of us. To put it simply, this is a separate division of the Russian Post, which facilitates the accelerated mailing of letters. Since tax notices are sent by mail, this item helps make all processes faster, so that each payer receives his due on time, and therefore has time to pay for it.

Note! There is no technical capability and the required amount of human resources to send payment receipts on behalf of each territorial tax office.

Actually, the service point is something like a transshipment point for hundreds of thousands of notifications. All calculations regarding the volume to be paid are carried out by the inspectors based on the declaration and other data available to them.