How to draw up an Act on the Destruction of the Seal and Stamp in 2022

As for the design, there are no strict rules here. It is highly desirable that the document be compiled without errors or typos. In general, experts recommend adhering to the rules for filling out other official documents. This means there should be a “head”, a base and a final part.

Of course, no one forbids you to enter data by hand. But at the same time, you need to make sure that all information is readable. Although in practice you can see that almost all companies fill out such documents using a computer.

Usually the document is drawn up in one copy. Although if there is a need, their number can be increased.

Each enterprise has a special journal that records the movement of seals. This is where you need to check the appropriate box. The process of filling out the document can be considered step by step:

- The company at which the seal is being destroyed is indicated at the top.

- The name of the document is written down, and the number assigned by internal document flow is also indicated.

- Below you need to enter the date and place of filling.

- The following is the reason why the destruction occurs.

- The members of the commission, their names and positions are listed. A group chairman is also appointed.

- Below it is necessary to mention which method of destruction was chosen.

- It would be useful to mention that after destruction the seal cannot be used.

- If we are talking about several seals and stamps, you can use a table. Here the quantity is indicated and imprints are placed. In fact, this will be a sample of the seal being destroyed.

- In the final part, each member of the commission must sign the document.

After the document is fully executed, it must be certified by the director. To do this, the act is submitted to him for signature. Another employee whose authority allows him to sign documents of this kind can also certify.

How to take into account seals and stamps in the accounting of a budgetary organization

A seal is an object on which signs and symbols are depicted, made in a special way so that it is possible to put imprints of these images on paper or other objects (clay, wax, etc.) in order to give these objects a certain meaning and (or ) legal force.

A stamp is a type of seal that replaces a handwritten note and is used, as a rule, in paperwork. It has no legal force; its main purpose is to facilitate work and speed up the document flow process.

Purchase of seals and stamps

All existing seals are divided into three types: the seal of the organization, the seal of the structural unit of the organization, the seal indicating its intended purpose (for documents, etc.). In turn, the seals of organizations are divided into simple and official seals <*>.

Production of official seals is carried out in stamping and engraving workshops according to sketches of organizations. It should be taken into account that such a seal must be made in one copy. Additional official seals can be produced only with the permission of a higher authority. In this case, they must be indicated by the number “2” and subsequent <*>.

Structural divisions and branches of organizations are also allowed to produce official seals if this is provided for by their charter, regulations or order on their formation. In this case, the word “branch” or the name of the structural unit <*> is entered into the text of the seals.

There are no restrictions on the production of stamps. They are ordered (purchased) based on the real needs of the organization.

In general, seals and dies consist of two elements: equipment (body) and cliche. Moreover, often in shipping documents the components of the seal (stamp) are written down as separate items. We recommend combining them into a single accounting object, since they are not used separately.

Accounting for seals and stamps is not established by law. In this case, the budgetary organization has the right to determine it independently and reflect it in its accounting policies <*>.

Taking into account that the service life of seals and stamps, as a rule, is more than one year, and their cost is relatively small, we propose to take into account these accounting items as separate items in the composition of working capital (OP in SOS).

In this case, in accounting, transactions for the receipt of seals and stamps purchased from budget funds by bank transfer to the organization are reflected in the following entries <*>:

| Contents of operations | Debit | Credit |

| Budget funding was received for the production of seals and stamps | 100 | 140, 142 (230, 232) |

| Funds were transferred from the treasury account to the manufacturer of seals and stamps | 178 | 100 |

| The received seals and stamps were capitalized including VAT <*> | 070 | 178 |

| At the same time, budget expenses are reflected and the EP fund is increased in the SOS | 200, 202 | 260 |

In accounting, transactions for the acquisition of seals and stamps using extra-budgetary funds are generally reflected in the following entries <*>:

| Contents of operations | Debit | Credit |

| Payment was transferred to the manufacturer of seals and stamps from an off-budget settlement account | 178 | 111 |

| Received seals and stamps have been capitalized (excluding VAT) | 070 | 178 |

| The submitted VAT is reflected <*> | 175 | 178 |

| Accepted for VAT deduction <*> | 173 | 175 |

| At the same time, expenses for extra-budgetary activities are reflected and the EP fund in the SOS is increased | 211 (080, etc.) | 260 |

Attention! Costs for the production of seals and stamps are included in cost element 1 10 03 05 “Other consumables and supplies” of the economic budget classification <*>.

2. Issuance of seals (stamps) for operation

Currently, each organization establishes the procedure for recording, using and responsibility for storing seals and stamps independently. The organization also independently determines the list of documents on which the seal is affixed. These norms can be enshrined in the Regulations on the procedure for production, recording, storage, use and destruction of seals and stamps in an organization or other local regulatory legal act.

Note See the explanation of Ministry of Justice specialist I.V. Leus in the article “To affix a stamp in the documentation or not.”

When issuing seals and stamps worth up to 1 base value ( hereinafter referred to as BV), they should be written off from accounting. This produces the entry <*>:

| Contents of operations | Debit | Credit |

| Prints and stamps worth up to 1 BV per unit were issued for use according to the list of materials issued for the needs of the institution. | 260 | 070 |

In the future, accounting of seals and stamps is carried out by the accounting department and the persons to whom they were issued, only in quantitative terms in the operational (quantitative) accounting statements f. 412 or in the inventory book of material assets f. M-17 <*>.

Also, as a rule, records of seals and stamps are kept by persons responsible for their recording and storage in a registration journal. This could be, for example, a journal of seals and stamps. For some organizations its form is approved <*>. In other cases, organizations have the right to determine it independently.

Seals and stamps that cost more than 1 base value are not written off when released into service, but are assigned to subaccount 071 “Items in use” <*>:

| Contents of operations | Debit | Credit |

| Seals and stamps that cost more than 1 BV per unit were put into operation according to the invoice (request) | 071 | 070 |

Analytical accounting for subaccount 071 is maintained by the accounting department in quantitative and monetary terms in the book f. 296 (cards f. 296a), on loose-leaf sheets f. 402 to the inventory list (matching sheet) f. 401 <*>.

Persons responsible for the operation and safety of the OP in the SOS are required to take into account these items in quantitative terms in the inventory book of material assets f. M-17 or statement of operational (quantitative) accounting f. 412 <*>.

The procedure for carrying out the destruction procedure

Today, the state does not regulate in any way the procedure for either the production or destruction of seals, so organizations must independently develop a regulatory framework for these actions.

However, in general, the procedure for recycling cliches is approximately the same:

- First, the management of the enterprise makes a decision to destroy seals and stamps that have lost their relevance (this can be made in relation to one seal, several or even all).

- Then an order is issued, which is a catalyst for starting this process.

- Based on the order, a special commission is created, which carries out the destruction of stamped items.

- To record the fact of disposal, a detailed report is drawn up.

It should be said that in some cases, organizations do not destroy seals and stamps themselves, but transfer this right to third-party companies.

As for lost or stolen stamps, it is impossible to draw up a disposal report in relation to them - in such cases it is necessary to submit appropriate applications to the tax service and the police.

What is important to remember in order to properly destroy an old seal?

The company's management has the right to choose from 2 basic options for destroying the seal:

- carry out the destruction of the seal yourself;

- entrust the destruction of the seal to third parties (a company engaged in the production and destruction of seals).

Since destroying a seal does not require significant labor costs, most organizations choose the first method, that is, they do it on their own.

The algorithm of actions in this case will be as follows:

- The leader, by order, convenes a special commission, which will deal with the destruction of the seal.

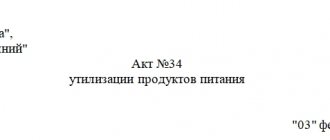

- After the old seals are destroyed (in the presence of the full commission), the company draws up a special act. The legislator has not established a single form for such an act, so it can be drawn up in free form. The main thing is that it should indicate for what reason it was decided to destroy the seals, what kind of seals they were (give their names and imprints). The act must be signed by all members of the commission.

If the company decides not to deal with the destruction of seals on its own, it can entrust this to a special organization that provides such services. Having chosen this method, you should remember that along with the seal of this organization you will need to provide documents confirming the legality of the actions to destroy the seal (decision of the head of the company, documents confirming his powers, etc.).

In addition, in some cases, a company, regardless of the chosen method of destroying a seal, will need to pay a state fee (for example, when removing a seal from the register).

Commission

The recycling commission must include at least two people . These can be any employees of the organization, but, as a rule, the following are appointed as such:

- director or any person close to the management of the company,

- employee responsible for the maintenance and storage of seals and stamps,

- HR specialist,

- lawyer,

- secretary.

Among them, the chairman of the commission and ordinary members should be highlighted.

The main task of the commission is to select stamps that have lost their relevance, directly carry out their destruction in any acceptable and most accessible way, and draw up an act about this.

For disposal, fairly simple methods are usually used:

- cutting cliches into small pieces with scissors (provided that they are made of polymers, rubber, caoutchouc and other soft materials),

- cutting using special tools (if the cliche is metal).

The main thing is that as a result of destruction, these products become completely unsuitable for further use.

Writing off seals and stamps

— the cost of printing is accepted for off-balance sheet accounting.

Also show material expenses in tax accounting. You can fully include the cost of printing without VAT as part of material costs. Moreover, at the very moment when you issue a stamp release with an act or a demand invoice. In other words, in tax accounting you will show the expense on the same day as in accounting. This conclusion follows from subparagraph 3 of paragraph 1 of Article 254 of the Tax Code of the Russian Federation. Accordingly, the accounting of seals in accounting and tax accounting will not differ.

A certificate of completion or a delivery note received from the seller will help confirm the costs of making the seal. And if the seal was received by a representative of your company by proxy and he also signed the confirmation form, attach it to the primary document as well.

The seal is destroyed by its own forces

The legislation does not regulate the procedure for the production and destruction of seals. Companies or individual entrepreneurs develop it independently.

Let's give an approximate recycling algorithm.

- The company's management decides to destroy seals and stamps that have lost their relevance. The decision can be made in relation to one seal, or several, or all at once.

- An order is issued to destroy the seals.

- Based on the order, a special commission is created, which carries out the destruction of stamped items.

- To record the fact of disposal, a report is drawn up.

The act of destruction of the seal includes the following information:

- composition of the commission;

- time and place of destruction of the seal;

- basis for destruction;

- name and imprint of the destroyed seal;

- method of destruction - complete destruction of the printing surface: rubber printing is cut into small pieces or burned, metal printing is sawed off with two cross lines;

- the commission's conclusion that the seal is unsuitable for use;

- signatures of the commission members.

The act is approved by the head of the enterprise (example 1). It is stored permanently to avoid disputes over documents certified by the old seal.

Attention! If the stamp is lost or stolen, then a corresponding application is submitted to the tax office and the police. In such a situation, a disposal report is not drawn up.

Basic options for destroying seals

- On your own, i.e. by the organization itself.

- By outside forces, i.e. by a special workshop (the same one that produces seals) or by the relevant body responsible for recording seals.

Destroying the seal on your own

In this case, the destruction of the seal is carried out by a commission appointed specifically for these purposes by the head of the organization. The created commission deals with the destruction of the seal and draws up an act for writing off seals and stamps, which is approved by the head of the organization.

What should be recorded in the write-off act:

- place and time of destruction;

- composition of the commission;

- the reasons why seals and stamps are written off;

- name of the seal and imprints;

- method of destruction. Typically, rubber products and photopolymer products are cut into pieces or burned.

When is a seal destruction certificate required? sample

Currently, federal laws do not require a seal

enterprises, but many companies use this attribute, the imprint of which confirms the authenticity and legal force of documents. The seal contains the mandatory details of the company, their composition depends on the specific purposes for which a particular seal is used. And since companies usually have a large number of stamp products in their arsenal, they must pay special attention to the issue of their accounting, storage and disposal.

The fact of disposal of the seal must be confirmed with a special document - an act.

It is the act of destruction of seals and stamps that is a sample document that confirms the establishment of a fact, an event that happened in the past or is taking place in the present. The main condition that a particular document is recognized as an act

- strict adherence to the order of its preparation and subsequent correct execution.

The organization needs to appoint an employee responsible for organizing work and storing seals and stamps. The order for his appointment is signed by the head of the company.

Situation. Replacing the seal

The organization plans to replace the round seal due to physical wear and tear and unclear image printing. The cost of printing is listed in accounting on account 10 “Materials”. The organization's accounting policy for 2016 stipulates that inventory, tools and household supplies are classified as inventories if the cost criterion does not exceed RUB 3,000,000. (excluding VAT) per unit and are written off as costs in the amount of 100% upon disposal due to the impossibility of further use.

The following questions arise:

1.1. What documents are required to complete this operation?

The procedure for destroying seals with the image of the State Emblem of the Republic of Belarus is established by the Instruction on the procedure for the production and destruction of seals with the image of the State Emblem of the Republic of Belarus, approved by Resolution of the Ministry of Internal Affairs of the Republic of Belarus dated June 12, 2009 No. 189.

The organization carries out the destruction of round seals without the image of the State Emblem of the Republic of Belarus independently, drawing up an act on the destruction of the seal. For this purpose, by order of the head, a commission is appointed to carry out this procedure. The act of destruction of the seal must contain an imprint of the seal being destroyed, be signed by members of the commission, and also approved by the head of the organization.

Typically, rubber printing cliches are cut into small pieces with scissors.

Let us remind you that all organizations, regardless of their form of ownership, must keep logs of the issuance (return) of seals (disposable sealing materials), stamps, seals, keys, numberers, cliches (clause 325 of the List of standard documents of the National Archival Fund of the Republic of Belarus generated in the process activities of government bodies, other organizations and individual entrepreneurs, indicating storage periods, approved by Resolution of the Ministry of Justice of the Republic of Belarus dated May 24, 2012 No. 140).

The forms of these documents are not established by law, therefore the organization has the right to independently develop and approve them reflecting the necessary information about seals and stamps.

1.2. How to reflect the replacement of a seal in accounting?

Tools, inventory and household supplies, which include the seal, are accounted for on account 10, subaccount 10-9 “Inventory and household supplies, tools” (clause 16 of the Instructions on the procedure for applying the standard chart of accounts, approved by the resolution of the Ministry of Finance of the Republic of Belarus dated 06/29/2011 No. 50).

The following second-order subaccounts can be opened in an organization:

10-9-1 “Inventory and household supplies, tools in the warehouse”;

10-9-2 “Inventory and household supplies, tools in operation.”

An organization’s accounting policy can provide for one of the following options for assigning the cost of individual items as part of funds in circulation to cost accounts:

– write off part of the cost at the time of transfer for operation (for example, 30%), and the rest (for example, 70%) when decommissioned due to the impossibility of further use;

– 100% of the cost is written off upon disposal due to the impossibility of further use.

For reference: the cost of individual items as part of funds in circulation is transferred to accounts accounting for production costs and sales costs in the following order:

– for special tools and special devices (tools and devices for special purposes, stamps, molds and similar items) – in accordance with standard rates, which are calculated based on the cost estimate for their production (purchase) and their useful life up to 2 years;

– the cost of special tools and special devices intended for individual orders is repaid at the time of their transfer to the production of this order;

– for other items – in accordance with the accounting policy of the organization (clause 107 of the Instructions for accounting of inventories, approved by Resolution of the Ministry of Finance of the Republic of Belarus dated November 12, 2010 No. 133) |*|.

* Commentary on individual norms of Instruction No. 133 is available for subscribers of the electronic “GB”

Thus, in the accounting records of an organization, when destroying a seal that has become unusable and acquiring a new seal, the following should be reflected:

D-t 60 – K-t 51 – prepayment was transferred to the supplier for the production of the seal;

D-t 26 – K-t 10-9-2 – the residual value of the destroyed seal is written off to cost accounts on the basis of the destruction act;

D-t 10-9-1 – K-t 60 – a new seal was received from the supplier based on the goods or delivery note, the prepayment was credited;

D-t 18 – K-t 60 or D-t 10-9-1 – K-t 60* – reflected VAT presented by the supplier;

D-t 68 – K-t 18 – accepted for deduction of VAT if it was not attributed to the increase in the cost of printing**;

D-t 10-9-2 – K-t 10-9-1 – the new seal was put into operation without transferring its cost (part of the cost) to cost accounts. __________________________ * VAT amounts presented when purchasing goods may be applied by payers to increase the cost of these goods (clause 4 of article 106 of the Tax Code of the Republic of Belarus).

** From July 1, 2016, it is possible to deduct VAT only on the basis of the ESCHF.

In the future, when decommissioned due to the impossibility of further use, the cost of printing will be charged to cost accounts in the amount of 100%.