As part of the implementation of the main directions of the budget, tax and customs tariff policy of Russia, Federal Law No. 374-FZ dated November 23, 2020 was adopted with numerous additions and changes to the Tax Code of the Russian Federation, which came into force on November 23, December 23, 2022, some from 2022 or during it. We tell you what changes in tax legislation now need to be taken into account in the work of accountants, lawyers and other specialists.

Large package of amendments to the Tax Code 2020-2021

Law No. 374-FZ was adopted in pursuance of the Main Directions of Budget, Tax and Customs Tariff Policy for 2022 and for the planning period of 2022 and 2023, approved by the Ministry of Finance of Russia.

It provides for the improvement of tax administration (control), as well as clarification of certain provisions of the Tax Code of the Russian Federation, affecting the issues of value added tax (VAT), excise taxes, personal income tax (PIT), corporate income tax, state duty, land tax, personal property tax and insurance premiums.

Next, we will consider the corresponding changes in the Tax Code of the Russian Federation for each of these elements.

Concept and list of local taxes and fees

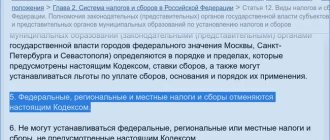

The very concept of “local taxes and fees” is given in paragraph 4 of Article 12 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code). In accordance with this norm , taxes established by the Tax Code of the Russian Federation and regulatory legal acts of representative bodies of municipalities on taxes are recognized as local and are obligatory for payment in the territories of the corresponding municipalities .

Federal Law No. 382-FZ of November 29, 2014 “On Amendments to Parts One and Two of the Tax Code of the Russian Federation”, Part 4 of Article 12 of the Tax Code is stated as follows:

Local taxes and fees are taxes and fees that are established by this Code and regulatory legal acts of representative bodies of municipalities on taxes and fees and are obligatory for payment in the territories of the relevant municipalities, unless otherwise provided by this paragraph and paragraph 7 of this article.

Local taxes and fees are introduced and cease to operate on the territories of municipalities in accordance with this Code and the regulatory legal acts of the representative bodies of municipalities on taxes and fees.

Local taxes and fees are established by this Code and regulatory legal acts of representative bodies of settlements (municipal districts), city districts (intra-city districts) on taxes and fees and are obligatory for payment in the territories of the corresponding settlements (inter-settlement territories), city districts (intra-city districts), if otherwise not provided for in paragraph 7 of this article. Local taxes and fees are introduced and cease to operate in the territories of settlements (inter-settlement territories), city districts (intra-city districts) in accordance with this Code and regulatory legal acts of representative bodies of settlements (municipal districts), city districts (intra-city districts) on taxes and fees

In an urban district with intracity division, the powers of representative bodies of municipalities to establish, enact and terminate local taxes in the territories of intracity districts are exercised by representative bodies of the urban district with intracity division or representative bodies of the corresponding intracity districts in accordance with the law of the constituent entity of the Russian Federation on the division of powers between bodies local government of an urban district with intracity division and local government bodies of intracity areas.

Local taxes and fees in the federal cities of Moscow, St. Petersburg and Sevastopol are established by this Code and the laws of the specified constituent entities of the Russian Federation on taxes and fees, and are obligatory for payment in the territories of these constituent entities of the Russian Federation, unless otherwise provided by paragraph 7 of this article. Local taxes and fees are introduced and cease to operate in the territories of the federal cities of Moscow, St. Petersburg and Sevastopol in accordance with this Code and the laws of these constituent entities of the Russian Federation.

When establishing local taxes, the representative bodies of municipalities (legislative (representative) bodies of state power of the federal cities of Moscow, St. Petersburg and Sevastopol) determine in the manner and within the limits provided for by this Code the following elements of taxation: tax rates, procedure and deadlines for paying taxes , if these elements of taxation are not established by this Code. Other elements of taxation for local taxes and taxpayers are determined by this Code.

Representative bodies of municipal formations (legislative (representative) bodies of state power of federal cities of Moscow, St. Petersburg and Sevastopol) in the manner and within the limits provided for by this Code may establish the specifics of determining the tax base, tax benefits, grounds and procedure for their application.

When establishing local fees, the representative bodies of municipalities (legislative (representative) bodies of state power of the federal cities of Moscow, St. Petersburg and Sevastopol) determine the rates of fees in the manner and within the limits provided for by this Code, and may also establish benefits for the payment of fees, grounds and procedure for their application.

Article 15 of the Tax Code of the Russian Federation (as amended by Federal Law No. 382-FZ of November 29, 2014) classifies taxes according to the level of government responsible for establishing the tax and establishes the following local taxes:

- Land tax;

- Property tax for individuals;

- Trade fee.

The procedure for introducing and collecting local taxes and fees

When establishing local taxes and fees, the legislative (representative) bodies of state power of the constituent entities of the Russian Federation are determined in the manner and within the limits provided for by the Tax Code, the following elements of taxation:

- tax rates;

- procedure and terms of payment.

Other elements of taxation for regional taxes and taxpayers are determined by the Tax Code of the Russian Federation.

According to Article 4 of Federal Law No. 382-FZ of November 29, 2014, a trade tax can be introduced in Moscow, St. Petersburg and Sevastopol no earlier than July 1, 2015, and in other municipalities - only after the adoption of the corresponding federal law.

Changes in tax administration

Regarding the organization of tax control, Law No. 374-FZ:

- introduced corresponding changes to the Tax Code of the Russian Federation in connection with the introduction of treasury services and a treasury payment system in 2021;

- determined the powers of local representative bodies to establish their taxes and fees to form their budgets for 2021-2023 (amendment to Article 12 of the Tax Code of the Russian Federation);

- introduced the opportunity to use an electronic power of attorney , signed with an enhanced qualified electronic signature, or a notarized (including equivalent) power of attorney (see more about this later in the article);

- increased the threshold amount of taxes, fees, insurance premiums, penalties and fines from 3,000 to 10,000 rubles for tax authorities to apply to the courts for their collection from individuals who are not individual entrepreneurs (changes in Article 48 of the Tax Code of the Russian Federation);

- from December 23, 2020, established uniform 1 year for individuals and organizations for sending demands for payment of arrears and arrears of penalties and fines, if the amount of arrears does not exceed 3,000 rubles (amendments to Article 70 of the Tax Code of the Russian Federation);

- clarified the rules on the return of overpaid (collected, subject to reimbursement) taxes to bank accounts, information about the opening of which was received by tax authorities in accordance with clause 1.1 of Art. 86 of the Tax Code of the Russian Federation, including regarding the timing of decisions on the collection of arrears and debts on penalties and fines and the offset of taxes subject to reimbursement, regardless of the type of tax (added to Art. , , , , , , 176, 176.1, 203.1 Tax Code of the Russian Federation);

- from December 23, 2020, established general rules according to which interest accrued by the Federal Tax Service on the date of the decision to return an overpaid payment is subject to payment to the payer on the basis of such a decision without a corresponding application (in other cases, an application is required), and additional opportunities for making changes to tax returns (calculations) without applying the current procedure based on the Federal Tax Service's request from payers for explanations and supporting documents;

- excluded the peculiarities of making decisions on conducting on-site inspections in relation to organizations from Skolkovo or participants in innovative scientific and technological centers (Article 89 of the Tax Code of the Russian Federation);

- introduced the obligation of the Pension Fund to report to the Federal Tax Service about combat veterans from the Unified State Information System of Social Security (USISSO) (new provisions of Article 85 of the Tax Code of the Russian Federation);

- in relation to information received from tax authorities to another government authority about taxpayers, payers of insurance premiums that constitute tax secrets, from 01/01/2021, a regime of prohibition of disclosure, requirements for a special regime of storage and access, liability for the loss of documents containing the specified information, or for disclosure (amendments to Article 102 of the Tax Code of the Russian Federation);

- from 01/01/2021, the submission by the tax authority to the operator of the “One Window” system of relevant information in the field of foreign economic activity (new clause 2.2 of Article 102 of the Tax Code of the Russian Federation) does not constitute a disclosure of tax secrets.

Concept and composition of tax legislation

Tax legislation is an integral part of the Russian legislative system, and therefore it is subject to the general principles of its construction. From this point of view, tax legislation forms a unified system (subsystem) of regulatory legal acts of varying legal force. However, the features of tax legislation should, first of all, include: a) subject composition; b) the sphere of regulation of public relations; c) applied methods (techniques, methods) of legal regulation.

The legislation on taxes and fees consists of the Tax Code of the Russian Federation and the federal laws on taxes and fees adopted in accordance with it (clause 1 of Article 1). But unlike civil legislation, which includes the Civil Code of the Russian Federation and federal laws (clause 2, article 3), tax legislation also includes the legislation of the constituent entities of the Russian Federation and regulatory legal acts of representative bodies of local government on local taxes and fees (clause 4, 5 Article 1 of the Tax Code of the Russian Federation). This provision corresponds to the constitutional and legal principle of division of tax powers, taking into account the different levels of competence of public authorities.

We emphasize that at the federal and regional levels, taxes and fees are established by laws, and at the local level - by regulatory legal acts of representative bodies of local government.

The Constitution of the Russian Federation does not allow the collection of taxes and fees on the basis of decrees of the President of the Russian Federation, resolutions of the Government of the Russian Federation, and departmental legal acts.

Thus, acts

§ 1. Concept and composition of tax legislation

executive authorities are not included in the tax legislation.

In addition, federal laws on taxes and fees must comply with the Tax Code of the Russian Federation. It is reasonable to ask: how to evaluate those laws that were adopted before the Code came into force? Further, should such laws be understood only as those laws whose adoption is expressly provided for or permitted by the Tax Code?

Since the entry into force of part two of the Tax Code of the Russian Federation, which establishes a system of federal and regional taxes and fees, the first issue has been largely resolved. The tax laws that were previously in force for the transition period (before the entry into force of part two of the Tax Code of the Russian Federation) have lost their legal force. At the same time, laws containing tax rules (for example, certain elements of tax regulation) are still in force. And although some of the laws were adopted before the entry into force of parts one and two of the Tax Code of the Russian Federation, such laws must be included in the legislation on taxes and fees. In this case, the main condition is their compliance with the requirements of the Tax Code of the Russian Federation.

A difficult question is the criteria for compliance (non-compliance) of the so-called “industry laws” containing the norms of tax law and the Tax Code of the Russian Federation. The fact is that, by virtue of paragraphs 1 and 2 of Art. 6 of the Code, verification of non-compliance is carried out only for regulatory legal acts on taxes and fees. On the other hand, the Tax Code of the Russian Federation does not contain direct indications that when taxing, only the norms (rules) of the legislation on taxes and fees are applied, and the norms of “sectoral” laws are applied after they are included in the acts of legislation on taxes and fees1. This problem has caused great resonance in practice. Thus, tax authorities began to be guided by the instructions of the State Tax Service of Russia (currently the Federal Tax Service) on the non-application of tax

1 See: Commentary on the Tax Code of the Russian Federation, part one (item-by-item) / Comp. and ed. comment S. D. Shatalov.

M., 1999. S. 19-23.

Chapter 5. Sources of tax law

new rules contained in “non-tax legislation”. In turn, the Supreme Court of the Russian Federation and the Supreme Arbitration Court of the Russian Federation in certain cases also shared a similar position1. For example, the decision of the Supreme Arbitration Court of the Russian Federation in case No. K4-N-7/850 dated December 24, 1994 recognized that the income tax benefit for individuals established by Decree of the President of the Russian Federation of December 24, 1993 No. 2284 “On the state program privatization of state and municipal enterprises in the Russian Federation" (clause 5.15.3) should not be applied, since it is not included in the Law on Income Tax.

We consider it necessary to formulate the following conclusions.

1. The Tax Code of the Russian Federation is a federal law, and therefore, from the point of view of the Constitution of the Russian Federation, it does not have any priority over other laws. Therefore, in cases where the norms of two laws conflict with each other, as a general rule

the norms of the law that was adopted most recently must be applied (the principle of

lex posterior derogat priori).

However, under some circumstances, the priority of the Tax Code of the Russian Federation may be justified by the constitutional and legal requirement of certainty of taxation2.

2. Attention should be paid to the danger of a situation when certain changes are made to the tax system through the adoption of non-tax laws. This practice in itself is dangerous. Such (destructive) trends are to some extent counteracted by the rule of paragraph 5 of Art. 3 of the Tax Code of the Russian Federation, according to which federal laws and fees are established, amended or repealed only by the Tax Code. We must recognize the emergence of “industry” laws containing norms as anomalous.

1 See: Gadzhiev G. A., Pepelyaev S. G.

Entrepreneur. Taxpayer. State (legal positions of the Constitutional Court of the Russian Federation). pp. 270-271.

2 See: Vinnitsky D.V.

Russian tax law: problems of theory and practice. pp. 338-339.

§ 2. Other sources of tax law

We are tax law. From the point of view of the sectoral affiliation of a particular act, it is important to avoid the adoption of such laws. The idea of comprehensiveness of legal acts does not work in this situation. Although in legal reality a complex element is present in any branch of legislation1.

Tax legislation is an integral part of the Russian legislative system, and therefore it is subject to the general principles of its construction. From this point of view, tax legislation forms a unified system (subsystem) of regulatory legal acts of varying legal force. However, the features of tax legislation should, first of all, include: a) subject composition; b) the sphere of regulation of public relations; c) applied methods (techniques, methods) of legal regulation.

The legislation on taxes and fees consists of the Tax Code of the Russian Federation and the federal laws on taxes and fees adopted in accordance with it (clause 1 of Article 1). But unlike civil legislation, which includes the Civil Code of the Russian Federation and federal laws (clause 2, article 3), tax legislation also includes the legislation of the constituent entities of the Russian Federation and regulatory legal acts of representative bodies of local government on local taxes and fees (clause 4, 5 Article 1 of the Tax Code of the Russian Federation). This provision corresponds to the constitutional and legal principle of division of tax powers, taking into account the different levels of competence of public authorities.

We emphasize that at the federal and regional levels, taxes and fees are established by laws, and at the local level - by regulatory legal acts of representative bodies of local government.

The Constitution of the Russian Federation does not allow the collection of taxes and fees on the basis of decrees of the President of the Russian Federation, resolutions of the Government of the Russian Federation, and departmental legal acts.

Thus, acts

§ 1. Concept and composition of tax legislation

executive authorities are not included in the tax legislation.

In addition, federal laws on taxes and fees must comply with the Tax Code of the Russian Federation. It is reasonable to ask: how to evaluate those laws that were adopted before the Code came into force? Further, should such laws be understood only as those laws whose adoption is expressly provided for or permitted by the Tax Code?

Since the entry into force of part two of the Tax Code of the Russian Federation, which establishes a system of federal and regional taxes and fees, the first issue has been largely resolved. The tax laws that were previously in force for the transition period (before the entry into force of part two of the Tax Code of the Russian Federation) have lost their legal force. At the same time, laws containing tax rules (for example, certain elements of tax regulation) are still in force. And although some of the laws were adopted before the entry into force of parts one and two of the Tax Code of the Russian Federation, such laws must be included in the legislation on taxes and fees. In this case, the main condition is their compliance with the requirements of the Tax Code of the Russian Federation.

A difficult question is the criteria for compliance (non-compliance) of the so-called “industry laws” containing the norms of tax law and the Tax Code of the Russian Federation. The fact is that, by virtue of paragraphs 1 and 2 of Art. 6 of the Code, verification of non-compliance is carried out only for regulatory legal acts on taxes and fees. On the other hand, the Tax Code of the Russian Federation does not contain direct indications that when taxing, only the norms (rules) of the legislation on taxes and fees are applied, and the norms of “sectoral” laws are applied after they are included in the acts of legislation on taxes and fees1. This problem has caused great resonance in practice. Thus, tax authorities began to be guided by the instructions of the State Tax Service of Russia (currently the Federal Tax Service) on the non-application of tax

1 See: Commentary on the Tax Code of the Russian Federation, part one (item-by-item) / Comp. and ed. comment S. D. Shatalov.

M., 1999. S. 19-23.

Chapter 5. Sources of tax law

new rules contained in “non-tax legislation”. In turn, the Supreme Court of the Russian Federation and the Supreme Arbitration Court of the Russian Federation in certain cases also shared a similar position1. For example, the decision of the Supreme Arbitration Court of the Russian Federation in case No. K4-N-7/850 dated December 24, 1994 recognized that the income tax benefit for individuals established by Decree of the President of the Russian Federation of December 24, 1993 No. 2284 “On the state program privatization of state and municipal enterprises in the Russian Federation" (clause 5.15.3) should not be applied, since it is not included in the Law on Income Tax.

We consider it necessary to formulate the following conclusions.

1. The Tax Code of the Russian Federation is a federal law, and therefore, from the point of view of the Constitution of the Russian Federation, it does not have any priority over other laws. Therefore, in cases where the norms of two laws conflict with each other, as a general rule

the norms of the law that was adopted most recently must be applied (the principle of

lex posterior derogat priori).

However, under some circumstances, the priority of the Tax Code of the Russian Federation may be justified by the constitutional and legal requirement of certainty of taxation2.

2. Attention should be paid to the danger of a situation when certain changes are made to the tax system through the adoption of non-tax laws. This practice in itself is dangerous. Such (destructive) trends are to some extent counteracted by the rule of paragraph 5 of Art. 3 of the Tax Code of the Russian Federation, according to which federal laws and fees are established, amended or repealed only by the Tax Code. We must recognize the emergence of “industry” laws containing norms as anomalous.

1 See: Gadzhiev G. A., Pepelyaev S. G.

Entrepreneur. Taxpayer. State (legal positions of the Constitutional Court of the Russian Federation). pp. 270-271.

2 See: Vinnitsky D.V.

Russian tax law: problems of theory and practice. pp. 338-339.

§ 2. Other sources of tax law

We are tax law. From the point of view of the sectoral affiliation of a particular act, it is important to avoid the adoption of such laws. The idea of comprehensiveness of legal acts does not work in this situation. Although in legal reality a complex element is present in any branch of legislation1.

A new approach to power of attorney

As mentioned above, the opportunity has been introduced to use an electronic power of attorney signed with an enhanced qualified electronic signature, or a notarized power of attorney (including equivalent according to the norms of the Civil Code of the Russian Federation) in tax legal relations.

The Federal Tax Service of Russia will approve:

- electronic format of a power of attorney confirming the authority of the taxpayer’s representative to sign reports;

- procedure for sending an electronic power of attorney via TKS (from 07/01/2021).

As of December 23, 2022, an authorized representative of an individual entrepreneur or an individual not registered as an individual entrepreneur can act under an electronic power of attorney with an electronic signature.

The very rule regarding the power of attorney issued by an individual taxpayer (clause 3 of Article 29 of the Tax Code of the Russian Federation) was also corrected. As of December 23, 2020, it is explicitly stated here that the same individual entrepreneurs and ordinary citizens (previously there was no clarification about individual entrepreneurs).

Changes in reporting

Law No. 374-FZ established in the Tax Code of the Russian Federation, from July 1, 2022, a closed (exhaustive) list of circumstances under which a declaration or calculation is considered not submitted.

These are new clauses 4.1 and 4.2 of Art. 80. The list includes 6 circumstances :

- during tax control activities, the fact of signing a tax return (calculation) by an unauthorized person was established;

- an individual who has the right to act without a power of attorney on behalf of the taxpayer (fee payer, insurance premium payer, tax agent) and who signed the declaration (calculation) is disqualified on the basis of a decision on disqualification that has entered into force in a case of an administrative offense and the period of disqualification has not expired before the date of filing reporting;

- the date of death of an individual occurred earlier than the date of signing the declaration (calculation) with his enhanced qualified electronic signature (information about the death is available in the Unified State Register of Civil Status Records);

- in relation to a person who has the right to act without a power of attorney on behalf of the taxpayer (payer of fees/insurance contributions, tax agent) and who signed the declaration (calculation), an entry was made in the Unified State Register of Legal Entities about the unreliability of information about him earlier than the date of submission of the report;

- in relation to the organization, an entry was made in the Unified State Register of Legal Entities about the termination of the legal entity (reorganization/liquidation/exclusion by decision of the registering authority) earlier than the date of submission of the reports;

- the VAT declaration does not correspond to the control ratios (clause 5.3 of Article 174 of the Tax Code of the Russian Federation) or there are errors in the calculation of contributions (for example, indicators for individuals do not coincide with the total amount) (clause 7 of Article 431 of the Tax Code of the Russian Federation).

If at least one of these circumstances is established, he will notify the relevant tax return (calculation) not submitted 5 days This means that the desk inspection will be stopped on the day the notification is sent.

If the updated declaration (calculation) is considered not submitted, then the previous reporting will continue to be verified. In this case, the period of the terminated cameral is not taken into account.

Changes in the calculation and payment of VAT

Law No. 374-FZ granted the right to a zero rate to payers selling to foreign buyers:

- goods in the form of aquatic biological resources obtained in the exclusive economic zone of the Russian Federation;

- and/or goods produced from them.

Accordingly, the right to VAT deductions is stipulated.

Article 147 of the Tax Code of the Russian Federation was supplemented with a clause according to which the place of sale of these goods is the territory of Russia, if at the time of the start of shipment and transportation they are located in the exclusive economic zone of the Russian Federation.

An exemption from VAT has also been introduced for a number of services provided by the operator of the financial platform.

Changes in excise taxes

Law No. 374-FZ obligated the publication of information about certificates of registration of an organization carrying out transactions with ethyl alcohol (with denatured ethyl alcohol) in electronic digital form in the public information system of the Federal Tax Service of Russia.

From 01/01/2021, according to the rules for calculating interest for late returns (new clause 10 of Article 78 of the Tax Code of the Russian Federation), it is necessary to calculate interest on refunds of VAT and excise taxes.

Changes in personal income tax

Law No. 374-FZ:

- clarified the list of compensation and other payments exempt from income tax;

- determined the specifics of exemption from personal income tax for income from the sale of real estate acquired under shared construction agreements;

- clarified the procedure for calculating the minimum maximum period of ownership of residential premises in the event of its sale (clause 2 of Article 217.1 of the Tax Code of the Russian Federation was added);

- clarified the procedure for taxation of personal income tax on dividends that a Russian company paid to a foreign one and which the individual recognized in the declaration (new subclause 1.1 clause 1 of Article 208 of the Tax Code of the Russian Federation from 2022);

- exempted from taxation income in kind when providing temporary use of residential premises and/or food to employees of medical organizations and social service organizations, if such persons perform their duties in isolation for the period of introduction of restrictive measures in connection with coronavirus infection;

- from 01/01/2021, the exemption from personal income tax for vacation travel and baggage transportation for workers from the Far North and equivalent areas was brought into line with the norms for insurance premiums. So, if you are on vacation abroad, the cost of travel to the border checkpoint, including the international airport, should be exempt.

From January 1, 2022, reimbursement of expenses for housing, rather than its free provision, should not be subject to personal income tax. We are talking about compensation that is established by law or decisions of local authorities.

The essence of law enforcement Art. 6 Tax Code of the Russian Federation

The provisions of this article apply to both laws and regulations. The first paragraph of the above contains a list of grounds for recognizing a normative act as contrary to the Code with all the ensuing consequences. It is open; if necessary, it can be expanded through the adoption of Federal Laws that edit the content of the Code. Nor is it exhaustive. The opportunity to challenge the provisions of regulations on grounds other than those set out in this article remains.

In Art. 6 of the Tax Code of the Russian Federation establishes the most significant and indisputable reasons. Those regulations that are subject to repeal are:

- derogate from the rights of one of the participants in legal transactions - taxpayers, representatives of authorized bodies and all other persons - tax agents, customs officials and others;

- contradict the articles of the Tax Code - they allow what is prohibited in the articles of the Code or prohibit what is permitted in them, etc.;

- introduce responsibilities or change the content of existing relationships between the participants.

Thus Art. 6 of the Tax Code of the Russian Federation does not establish completely original rules, but logically continues and details Art. 1 of the Tax Code of the Russian Federation, which declares the priority of the Code over all other regulations.

Changes regarding the avoidance of double taxation

Law No. 374-FZ defined in the Tax Code of the Russian Federation:

- the procedure for taxing the income of foreign organizations - shareholders from the trust management of property constituting a mutual fund, on investment shares belonging to them in proportion to the share in the right of common ownership of the fund’s property; namely, he equated this type of income to dividends;

- Income of foreign companies from sources in the Russian Federation includes income from the sale (including redemption) of investment shares of closed mutual funds, belonging not only to the categories of rental funds and real estate funds, but also to combined and other funds, more than 50% of the assets of which are direct or indirectly consists of real estate located in Russia.

Division of regulations into categories

According to the Constitution of the Russian Federation (Article 72), the establishment of taxation principles is one of the subjects that are under the joint jurisdiction of the center and the subjects of the federation. In addition, the Tax Code includes legislative acts adopted by representative bodies at all levels, including local government.

The following documents are accepted:

- at the level of the Russian Federation - in the form of amendments and additions to the tax code;

- at the level of federal subjects - in the form of its laws;

- at the local government level - in the form of decisions or regulations.

Documents of a regional and local nature must comply with the norms of the Tax Code of the Russian Federation and are accepted exclusively within the framework provided for by it. An example is the legislation on transport tax. The basic rates of this payment and a number of elements are established in the Tax Code of the Russian Federation, but the issue of its final amount is decided by the authorities of the constituent entities.

The general rule regarding the establishment of legal grounds for levying taxes is that they must be established by representative authorities.

However, the question arises about what to do with numerous by-laws both at the level of the Russian Federation and at the level of its constituent entities and local self-government? The Tax Code in Article 4 singled them out into a separate category and established the rules for the acceptance and validity of such documents. The concept contained in it implies regulatory legal acts on taxes and fees, with the exception of legislative ones.

Changes in corporate income tax

Law No. 374-FZ introduced the following amendments to the Tax Code of the Russian Federation:

- clarified the rules for applying the zero rate on dividends paid by Russian organizations to foreign companies, the actual right to which is held by organizations that are tax residents of the Russian Federation;

- clarified the rules for forming the tax base of non-profit organizations, taking into account the problems of their distribution of expenses between statutory and paid activities, and also clarified the list of types of income not subject to taxation;

- clarified the procedure for calculating the indicator for determining the tax base for income from equity participation in other organizations;

- established the procedure for the formation of the residual value of intangible assets by analogy with the procedure for fixed assets;

- established the procedure for forming a reserve for the payment of remuneration based on the results of the year;

- excluded provisions allowing to bypass the ban on the application of a “zero” rate to profits from the sale of shares of companies whose assets are more than 50% represented by real estate in the Russian Federation;

- clarified the procedure for recognizing non-operating income using the accrual method (new subclause 15, clause 4, article 271 of the Tax Code of the Russian Federation);

- gave regions the right to establish an investment tax deduction for expenses on research and development (R&D, intangible assets) (as an additional opportunity to stimulate their innovation activities).

An organization should not include as income not only property received free of charge from an organization or individual with a share of at least 50% (previously more than 50%), but also similar property rights . This applies to legal relations arising from January 1, 2020 .

Acts of legislation on taxes and fees as the main source of NP. Action of acts in space

Law is a normative legal act adopted by the highest government body or directly by the people, which has the highest legal force. This definition contains an indication of two essential features of the law: 1) a normative legal act is adopted by the highest body of state power that has the ability to express the will of the state, 2) the law has the highest legal force .

1. The Constitution of the Russian Federation , adopted in a referendum on December 12, 1993, as a basic regulatory legal act, contains the fundamental rules necessary for the further regulation of tax relations.

The articles of the Constitution containing norms of tax law include:

-Article 57, according to which “everyone is obliged to pay legally established taxes and fees. Laws establishing new taxes or worsening the situation of taxpayers do not have retroactive effect”;

- paragraph “h” of Art. 71 , according to which the Russian Federation is responsible for federal taxes and fees;

— subparagraph “i” of Part 1 of Art. 72 , according to which the establishment of general principles of taxation and fees in the Russian Federation falls within the general competence of the Russian Federation and the constituent entities of the Russian Federation;

- part 3 art. 75 , according to which the system of taxes levied into the federal budget and the general principles of taxation and fees in the Russian Federation are established by federal law;

- part 3 art. 104 , stipulating that bills on the introduction or abolition of taxes can only be introduced if there is a conclusion from the Government of the Russian Federation;

— Article 106 , which establishes that federal laws on federal taxes and fees adopted by the State Duma are subject to mandatory consideration in the Federation Council;

— Article 132 , according to which local self-government bodies independently establish local taxes and fees.

2. Federal Laws are adopted on issues provided for by the Constitution of the Russian Federation. Although the Constitution does not provide for federal constitutional laws specifically devoted to the regulation of tax relations, some norms of this group of laws regulate taxation issues and, therefore, can be classified as sources of tax law. For example, Federal Law No. 5-FKZ dated June 28, 2004 “On the referendum of the Russian Federation” prohibits the submission to a referendum of questions on the introduction, amendment and abolition of federal taxes and fees, as well as on exemption from their payment (Article 6) <1 >, and the Federal Constitutional Law of December 17, 1997 N 2-FKZ “On the Government of the Russian Federation” (as amended on June 19, 2004) establishes the obligation of the Government of the Russian Federation to give written opinions on bills on the introduction or abolition of taxes, on exemption from their payment (Article 36)

3. Federal laws . Acts of legislation on taxes and fees are the main sources of tax law, and among these acts the primary role is given to the Tax Code of the Russian Federation adopted in 1998 . Part one of the Tax Code of the Russian Federation is devoted to the general principles of taxation and establishes the general principles of the functioning of the tax system in Russia, the rights and obligations of participants in tax legal relations, the basic categories of taxation, forms of tax control and responsibility for committing tax offenses. Article 1 of the Tax Code of the Russian Federation formulates the concept of legislation on taxes and fees, according to which the legislation on taxes and fees includes acts of three levels:

— legislation of the Russian Federation on taxes and fees;

— legislation of the constituent entities of the Russian Federation on taxes and fees;

— regulatory legal acts of municipalities.

The Tax Code of the Russian Federation is a regulatory legal act, one of the federal laws, designed to systematize tax and legal norms. In the system of legislation on taxes and fees, the Tax Code of the Russian Federation is the main regulatory legal act , on the basis of which the entire system of legal regulation of tax relations is built. Therefore, all tax and legal norms, regardless of which acts they are enshrined in, must comply with the requirements of the norms contained in the Tax Code of the Russian Federation. At the same time, despite the fact that the Tax Code of the Russian Federation undoubtedly occupies a dominant position in the system of legislation on taxes and fees, even at the federal level it does not have a monopoly right to regulate tax relations .

Clause 1 of Art. 1 includes among the federal acts included in the system of legislation on taxes and fees other federal laws adopted in accordance with the Tax Code of the Russian Federation. According to the legislator, the attribute “adopted in accordance with it” was supposed to mean that federal laws would only be included in the system of legislation on taxes and fees of the Russian Federation when they were directly or indirectly mentioned in the text of the Tax Code. However, the use of the term “adopted in accordance” may well be interpreted as “not contradicting” the Tax Code of the Russian Federation.

It is precisely this reading of this norm that probably allowed the Plenum of the Supreme Arbitration Court of the Russian Federation to indicate in its Resolution that “until the entry into force of the relevant chapters of part two of the Tax Code of the Russian Federation, courts must apply the norms of law regarding tax benefits adopted in the prescribed manner, regardless of whether in what legislative act are they included: related or not generally related to taxation issues.” In other words, the Plenum of the Supreme Arbitra issues of application of part one of the Tax Code of the Russian Federation" // Bulletin of the Supreme Arbitration Court of the Russian Federation. 2001. N 7)

4. Clause 4 of Art. is devoted to the legislation of the constituent entities of the Russian Federation on taxes and fees. 1 Tax Code of the Russian Federation. The named point, following the norm of Art. 76 of the Constitution of the Russian Federation, determines that the legislation of the constituent entities of the Russian Federation on taxes and fees consists of laws on taxes and fees of the constituent entities of the Russian Federation, adopted in accordance with the Tax Code of the Russian Federation.

5. System of legal acts regulating taxation issues at the local level . Clause 5 Art. 1 indicates only that these acts of municipalities must be adopted by representative authorities. Despite the fact that the wording “acts on local taxes and fees” is used as a qualifying feature of an act of municipal bodies authorized to regulate taxation issues, this feature has no practical meaning, since the Tax Code of the Russian Federation does not define “acts on taxes and fees”, and therefore, any legal acts of a municipal entity that in one way or another affect taxation issues can be classified as acts of legislation on taxes and fees. ACCORDINGLY – ACTION IN SPACE – ACTION IN A CERTAIN AREA FOR SPECIFIC GUYS.

Law is a normative legal act adopted by the highest government body or directly by the people, which has the highest legal force. This definition contains an indication of two essential features of the law: 1) a normative legal act is adopted by the highest body of state power that has the ability to express the will of the state, 2) the law has the highest legal force .

1. The Constitution of the Russian Federation , adopted in a referendum on December 12, 1993, as a basic regulatory legal act, contains the fundamental rules necessary for the further regulation of tax relations.

The articles of the Constitution containing norms of tax law include:

-Article 57, according to which “everyone is obliged to pay legally established taxes and fees. Laws establishing new taxes or worsening the situation of taxpayers do not have retroactive effect”;

- paragraph “h” of Art. 71 , according to which the Russian Federation is responsible for federal taxes and fees;

— subparagraph “i” of Part 1 of Art. 72 , according to which the establishment of general principles of taxation and fees in the Russian Federation falls within the general competence of the Russian Federation and the constituent entities of the Russian Federation;

- part 3 art. 75 , according to which the system of taxes levied into the federal budget and the general principles of taxation and fees in the Russian Federation are established by federal law;

- part 3 art. 104 , stipulating that bills on the introduction or abolition of taxes can only be introduced if there is a conclusion from the Government of the Russian Federation;

— Article 106 , which establishes that federal laws on federal taxes and fees adopted by the State Duma are subject to mandatory consideration in the Federation Council;

— Article 132 , according to which local self-government bodies independently establish local taxes and fees.

2. Federal Laws are adopted on issues provided for by the Constitution of the Russian Federation. Although the Constitution does not provide for federal constitutional laws specifically devoted to the regulation of tax relations, some norms of this group of laws regulate taxation issues and, therefore, can be classified as sources of tax law. For example, Federal Law No. 5-FKZ dated June 28, 2004 “On the referendum of the Russian Federation” prohibits the submission to a referendum of questions on the introduction, amendment and abolition of federal taxes and fees, as well as on exemption from their payment (Article 6) <1 >, and the Federal Constitutional Law of December 17, 1997 N 2-FKZ “On the Government of the Russian Federation” (as amended on June 19, 2004) establishes the obligation of the Government of the Russian Federation to give written opinions on bills on the introduction or abolition of taxes, on exemption from their payment (Article 36)

3. Federal laws . Acts of legislation on taxes and fees are the main sources of tax law, and among these acts the primary role is given to the Tax Code of the Russian Federation adopted in 1998 . Part one of the Tax Code of the Russian Federation is devoted to the general principles of taxation and establishes the general principles of the functioning of the tax system in Russia, the rights and obligations of participants in tax legal relations, the basic categories of taxation, forms of tax control and responsibility for committing tax offenses. Article 1 of the Tax Code of the Russian Federation formulates the concept of legislation on taxes and fees, according to which the legislation on taxes and fees includes acts of three levels:

— legislation of the Russian Federation on taxes and fees;

— legislation of the constituent entities of the Russian Federation on taxes and fees;

— regulatory legal acts of municipalities.

The Tax Code of the Russian Federation is a regulatory legal act, one of the federal laws, designed to systematize tax and legal norms. In the system of legislation on taxes and fees, the Tax Code of the Russian Federation is the main regulatory legal act , on the basis of which the entire system of legal regulation of tax relations is built. Therefore, all tax and legal norms, regardless of which acts they are enshrined in, must comply with the requirements of the norms contained in the Tax Code of the Russian Federation. At the same time, despite the fact that the Tax Code of the Russian Federation undoubtedly occupies a dominant position in the system of legislation on taxes and fees, even at the federal level it does not have a monopoly right to regulate tax relations .

Clause 1 of Art. 1 includes among the federal acts included in the system of legislation on taxes and fees other federal laws adopted in accordance with the Tax Code of the Russian Federation. According to the legislator, the attribute “adopted in accordance with it” was supposed to mean that federal laws would only be included in the system of legislation on taxes and fees of the Russian Federation when they were directly or indirectly mentioned in the text of the Tax Code. However, the use of the term “adopted in accordance” may well be interpreted as “not contradicting” the Tax Code of the Russian Federation.

It is precisely this reading of this norm that probably allowed the Plenum of the Supreme Arbitration Court of the Russian Federation to indicate in its Resolution that “until the entry into force of the relevant chapters of part two of the Tax Code of the Russian Federation, courts must apply the norms of law regarding tax benefits adopted in the prescribed manner, regardless of whether in what legislative act are they included: related or not generally related to taxation issues.” In other words, the Plenum of the Supreme Arbitra issues of application of part one of the Tax Code of the Russian Federation" // Bulletin of the Supreme Arbitration Court of the Russian Federation. 2001. N 7)

4. Clause 4 of Art. is devoted to the legislation of the constituent entities of the Russian Federation on taxes and fees. 1 Tax Code of the Russian Federation. The named point, following the norm of Art. 76 of the Constitution of the Russian Federation, determines that the legislation of the constituent entities of the Russian Federation on taxes and fees consists of laws on taxes and fees of the constituent entities of the Russian Federation, adopted in accordance with the Tax Code of the Russian Federation.

5. System of legal acts regulating taxation issues at the local level . Clause 5 Art. 1 indicates only that these acts of municipalities must be adopted by representative authorities. Despite the fact that the wording “acts on local taxes and fees” is used as a qualifying feature of an act of municipal bodies authorized to regulate taxation issues, this feature has no practical meaning, since the Tax Code of the Russian Federation does not define “acts on taxes and fees”, and therefore, any legal acts of a municipal entity that in one way or another affect taxation issues can be classified as acts of legislation on taxes and fees. ACCORDINGLY – ACTION IN SPACE – ACTION IN A CERTAIN AREA FOR SPECIFIC GUYS.

Changes in payment of state duty

Law No. 374-FZ added the following provisions:

- established a state fee for issuing a license for the production of ethyl alcohol for the production of the pharmaceutical substance ethyl alcohol (ethanol) in connection with the establishment of a new type of activity subject to licensing in accordance with the Law of November 22, 1995 No. 171-FZ “On state regulation of the production and turnover of ethyl alcohol, alcohol and alcohol-containing products and on limiting the consumption (drinking) of alcoholic products”;

- to encourage rights holders of real estate to register rights that arose before the entry into force of the Law of July 21, 1997 No. 122-FZ “On state registration of rights to real estate and transactions with it”, they were exempted from paying state fees when applying for legally significant actions related to with state registration of long-established rights to real estate;

- To reduce the financial burden on citizens affected by the emergency, they were exempted from paying state fees for registering ownership of residential premises or shares in them acquired by individuals in connection with the implementation of social support measures to replace the housing they lost as a result of the emergency.

For entering information about a legal entity into the register of financial platform operators, the state duty is set at 35,000 rubles.

Changes to the mineral extraction tax (MET)

Law No. 374-FZ established:

- assessment of the cost of precious metals based on the taxpayer’s current sales prices for precious stones in the corresponding tax period (and in their absence, in the nearest previous tax period) excluding VAT, reduced by his expenses for their delivery;

- responsibilities for taxpayers - participants in regional investment projects to restore unpaid amounts of mineral extraction tax not transferred due to the application of reduced tax rates, in the event of termination of participant status - on the grounds provided for by the Tax Code of the Russian Federation.

Characteristics of regulations on taxes and fees

The legislation of the Russian Federation does not contain a definition of a normative act on taxes and fees. However, the general principles of its application, as well as the signs, will help to formulate a suitable concept.

What characterizes the normative act on taxes and fees in the Russian Federation:

- these are decisions establishing responsibilities associated with the transition of private finance into the public sphere;

- any of the entities accepting them must have the appropriate powers;

- they must have the characteristics of a document, including the date of adoption, the accepting authority, the place of approval, and the number;

- such acts must clearly occupy their place in the legal hierarchy and not contradict documents that have greater legal force;

- execution requires publication. Taxation subjects must be provided with such information. This can be either a newspaper or another publication, for example, “Bulletin of normative acts of federal executive bodies”;

- such regulations, if they relate to legislation, must contain all elements of taxation. These include objects, base, tax periods, tax rates, calculation procedure, as well as the procedure and terms of payment.

Based on these characteristics, the following definition is obtained. A tax regulatory act is a document adopted by an authorized body, establishing obligations to make mandatory payments to the treasury, not contradicting acts of greater legal force, published in the prescribed manner and containing all elements of taxation.

Changes in property taxes

In terms of land, transport and property taxes, Law No. 374-FZ made the following changes to the Tax Code:

- the non-declaration procedure for providing tax benefits on property taxes has been extended to combat veterans ;

- the list of documents submitted to the tax authorities by individuals through the MFC (“My Documents”) has been expanded;

This:

- notification of the availability of real estate and/or vehicles recognized as objects of taxation for individuals;

- statement about the loss or destruction of an object for transport tax.

- the procedure for reviewing documents received from payers - individuals and organizations by tax authorities has been improved;

- from 01/01/2021, a procedure for taxation of destroyed vehicles , which provides for the termination of the calculation of transport tax not from the moment the vehicle is deregistered, but from the 1st day of the month in which the vehicle was destroyed (new clause 3.1 of Article 362 of the Tax Code of the Russian Federation) ;

In order for the tax office to stop calculating tax, you need to submit an application on the Federal Tax Service form, where you indicate the month of the accident with the car. You can attach documents confirming the death or destruction of the vehicle. If there are no documents, the Federal Tax Service itself will request information from the authorities and persons who have it.

After reviewing the application, she will notify that the tax is no longer charged. Or that there is no reason to stop accrual.

- the procedure for interaction between tax authorities and authorized bodies has been determined for the purpose of administering land tax in relation to lands withdrawn from circulation and limited in circulation, provided to ensure defense, security and customs needs;

- a reduction factor has been established when calculating property tax for individuals in relation to newly formed real estate;

- New rules have been introduced for the recalculation of previously calculated property taxes for individuals.

According to the Federal Tax Service, if a citizen has a tax benefit that was not previously taken into account when sending him a tax notice, from November 23, 2020 it will be applied from the period in which the taxpayer became entitled to this benefit. In this case, the tax authority will carry out a recalculation, reducing tax payments by the amount of such a benefit. These are amendments to paragraph 3 of Art. 361.1, paragraph 10 of Art. 396, paragraph 6 of Art. 407 of the Tax Code of the Russian Federation.

From 2022, it is also possible to recalculate land tax or property tax for individuals for previous tax periods if it is associated with a decrease in the cadastral value of the taxable object. Corresponding amendments have been made to clause 1.1 of Art. 391 and paragraph 2 of Art. 403 of the Tax Code of the Russian Federation. For example, if the cadastral value has decreased due to:

- introducing amendments to the act on approval of the results of its determination;

- bug fix;

- establishing the cadastral value of real estate in the amount of its market value.

In addition, from July 1, 2021 , in paragraph 2.1 of Art. 52 of the Tax Code of the Russian Federation, a rule will appear stating that an individual does not recalculate the transport tax if it (regardless of the grounds) entails an increase in the previously paid tax. That is, it worsens the situation of the taxpayer. This innovation is aimed at respecting the legitimate interests of bona fide car owners who have paid the transport tax on time according to the received tax notice (a similar restriction on recalculations is already applied to land tax and property tax for individuals).

Also, Law No. 374-FZ made changes regarding the calculation of taxes according to the cadastre from 2022.

Now there are only 2 exceptions , when changes in the cadastral value of a land plot or other real estate are taken into account in the current and previous periods:

| SITUATION | EXPLANATION |

| The cadastral value is set at the market value | To calculate taxes, market value is used with start date of application variable cadastral value (previously, recalculation of taxes at market value was possible from January 1 of the year in which the payer applied). Until 2022, this only applied to situations where the value of a plot or other real estate was disputed in a commission or court. By 2023, in all regions, disputes (cases) regarding the establishment of cadastral value in the amount of market value will be considered by special budget institutions involved in cadastral valuation, and not by commissions under Rosreestr. |

| Current or retrospective application of the changed cadastral value is provided for by the Law on Cadastral Valuation dated July 3, 2016 No. 237-FZ | For example, when the real estate index has decreased by more than 30%, the reduced cadastral value is applied from the beginning of the year for which the index is calculated. If the value of real estate included in the regional list (shopping and office centers, premises in them, offices, catering facilities, consumer services) has not been determined at the beginning of the year, according to the new rules, tax must be , but at the average annual cost (previously the Ministry of Finance believed that not necessary at all). |

In the property tax return for 2022, organizations need to include information on the average annual value of movable property, which the legal entity reflects in accounting as a fixed asset . The relevant amendments to the declaration form will be approved by the Federal Tax Service.

According to the Main Directions of Tax Policy, it is possible that taxes will be levied on movable property again, and the marginal rate will be reduced. This will make it possible not to increase the tax burden and eliminate disputes about classifying the property as real estate.

Starting from 2022, the tax office was obliged to consider the notification of the transition to a single declaration for non-retail real estate within 30 days , and then report on the results of the organization (new provisions of paragraph 1 of Article 386 of the Tax Code of the Russian Federation).

All rules on calculating property tax for individuals based on inventory value have been excluded: Art. 402 of the Tax Code of the Russian Federation has lost force since 2021.

Who can adopt by-laws in the tax sphere

In Part 1 of Art. 4 of the Tax Code of the Russian Federation lists the bodies that have the right to issue such norms. In some cases, the place of specific subjects, the law contains only general formulations, since the structure and names of the elements of executive power can change regularly.

The important point is that they cannot supplement or change the legislation on taxes and fees.

1. Government of Russia.

The Government of Russia is the highest executive body that determines the foundations of state policy in key areas. And in a number of cases, the law delegates to him the rights to resolve private issues that do not affect the basis of regulation.

An example is Part 2. Art. 149 of the Tax Code of the Russian Federation, which exempts cases of sale of certain goods from VAT. Their list is determined by the relevant decree of the Russian Government.

It is assumed that the text of the law cannot take into account the development of medical technologies, and the government act can be quickly adopted. In addition, its publication serves as a manifestation of both stimulating economic measures and a manifestation of policies aimed at maintaining the social sphere.

2. Executive authorities of Russia.

Art. 4 provides such rights to the bodies responsible for developing state policy in the field of taxes and duties, as well as in customs matters. Currently, both of these functions are combined within the Ministry of Finance.

Examples of regulatory legal acts of this body are numerous accounting provisions, according to which the base for many taxes and fees is calculated.

They are also specific in nature.

Structural divisions of the Ministry of Finance can issue acts establishing the forms of certain documents related to the requirements of legislation on taxes and fees, as well as in customs affairs. These include the Federal Customs Service and the Federal Tax Service. Examples of acts are orders approving declaration forms.

At the same time, control authorities related to the collection of mandatory and customs payments and their territorial divisions do not have the right to issue such acts.

3. Regional executive authorities.

The executive authorities of the constituent entities of Russia also have the right to issue regulations on taxes and fees. Their powers must be provided for by the legislative act (it talks about the authorized body) and not go beyond the scope of the competence provided for by the regulations on them. As a rule, these include regional governments.

An example is the establishment of various technical indicators that affect the size of the final payments of taxable subjects.

4. Local executive bodies.

Decisions of executive bodies of local self-government can also play a significant role.

A number of mandatory payments require a difficult to calculate base, which depends on local conditions. If they are of a non-permanent nature, then the possibility of adoption of a number of acts by local authorities contributes to the most effective application of the law.

At the same time, the body issuing this decision must have the appropriate competence defined by the regulations on it.

Changes in insurance premiums

Law No. 374-FZ:

- added to the list of periods for which individual entrepreneurs do not pay insurance premiums for themselves - periods of being in custody and serving a sentence in places of deprivation of liberty;

- synchronized the list of payments from the employer in favor of employees and not subject to insurance contributions (Article 422 of the Tax Code of the Russian Federation) with the list of similar payments not subject to personal income tax (Article 217 of the Tax Code of the Russian Federation);

- The criteria for the share of income of IT companies have been clarified in order to apply reduced contribution rates.

Exemption from contributions for compensation of expenses to the contractor under a civil contract (GPD, GPC) was fixed from 01/01/2021 in a separate new sub-clause. 16 clause 1 art. 422 of the Tax Code of the Russian Federation. This:

“Amounts paid by the payer to reimburse actually incurred and documented expenses of an individual related to the performance of work, provision of services under civil contracts, as well as payment by the payer of such expenses.”

The wording has become clearer: payment for such expenses has also been added.

Changes in controlled debt

For 2022 and 2022, special intervals have been established (clause 1.2 of Article 269 of the Tax Code of the Russian Federation) for interest rates on controlled debt. Thus, for a debt obligation in rubles from a transaction recognized as controlled, the range is from 0% to 180% of the Central Bank key rate (previously - from 75% to 125%).

These amendments can be applied taking into account the specifics of determining the amount of debt and equity in legal relations that arose from January 1, 2020 .

A new approach to calculating the tax base

The law changed the procedure for determining the tax base for personal income tax when an individual receives income in the form of interest accrued on deposits (account balances) in banks located on the territory of the Russian Federation.

The amount of the deposit itself is not subject to new tax, only the interest on it!

The tax base in this case is the excess of interest received during the tax period (calendar year) on all deposits (account balances) in banks, over interest calculated as the product of 1 million rubles and the key rate of the Central Bank on the 1st day of the tax period .

Simply put, 1 million rubles multiplied by the key rate of the Central Bank is the so-called non-taxable minimum for deposits. You must pay income tax on all amounts above.

Although the following incomes are not taken into account when determining the tax base:

- in the form of interest on ruble deposits, the interest rate on which during the entire tax period does not exceed 1% per annum (on demand, etc.);

- on escrow accounts (property set aside to fulfill another obligation).

Income in foreign currency is converted into rubles at the official exchange rate of the Bank of Russia on the date of actual receipt of income on deposits.

Ruble revaluation of foreign currency deposits is not subject to the new tax.

Salary accounts in banks are not subject to the new tax on interest on deposits!