Why do you need a card for individual accounting of accrued payments?

In accordance with law 125-FZ and art. 431 of the Tax Code of the Russian Federation, employers must keep records of transactions on insurance premiums. The accounting card plays a special role in this matter. This document is not mandatory and is only a recommendation. That is, employers have the right to use their own form of the document. Moreover, any form that will be used by the company must be approved in the accounting policy. All information that is reflected in the document must be entered in accordance with the accounting data for account 69. Such cards can be used by tax authorities. In the absence of such cards, penalties in the amount of 200 rubles will be assessed for each such missing document.

Important! Each organization is required to keep cards for individual accounting of the amounts of accrued insurance premiums. These cards may be requested by tax authorities and if they are missing, the company will face a fine of 200 rubles for each missing card.

Which form to use

The current tax legislation does not establish a registration card form. Therefore, each company must develop and approve it independently. The Federal Tax Service recommends using the form approved by the Pension Fund as a basis.

Until 2022, insurance premiums were administered by extra-budgetary funds: the Pension Fund and the Social Insurance Fund. The rules for calculating insurance premiums were set out in Federal Law No. 212-FZ of July 24, 2009.

It was these two organizations that, in a joint letter, developed and recommended the form of an individual accounting card for the amounts of accrued payments and other remunerations and the amounts of accrued social contributions (PFR Letter No. AD-30-26/16030 and FSS PF No. 17-03-10/08/47380 dated 09.12 .2014).

Pension Fund and Social Insurance Fund form

Card contents

The individual accounting card has a fairly simple structure. However, there is a certain set of information that must be indicated in this document. These include:

- name of the insured, his TIN, KPP;

- Full name of the insured employee, as well as his citizenship, disability, details of the employment contract, employee status;

- the amount of payments to the insured employee, and the amounts subject to and non-taxable by insurance contributions are separately indicated;

- data for calculating insurance premiums for compulsory health insurance, compulsory medical insurance and social insurance;

- amounts of contributions to be paid;

- expenses for compulsory health insurance, information about paid benefits for temporary disability, social security and occupational diseases.

The final data in the map is marked both for the month and as a cumulative total. If it is necessary to reflect additional contributions, the second page of the card is used (

What does the card consist of?

The accounting card consists of three pages.

- Card recording all payments and amounts of insurance premiums accrued to the employee.

- Card for recording payments, other remunerations and amounts of accrued insurance premiums for persons working in harmful or dangerous working conditions.

- Card for recording amounts for compulsory social insurance.

All policyholders must complete page 1. And pages 2 and 3 are completed if necessary.

Policyholders do not have to use the specified card form when keeping records of insurance premiums. You can develop your own form.

A separate card is issued for each employee for the calendar year. The amounts on the card are reflected in rubles and kopecks on a monthly basis and on a cumulative basis from the beginning of the year.

If the policyholder develops its own accounting form, it must reflect the following information:

- name, tax identification number, checkpoint of the organization;

- employee data: full name, INN, SNILS, citizenship, disability, type of concluded contract, its details;

- tariffs at which insurance premiums are calculated from payments to this employee, as well as the tariff code;

- payments to the employee, including those not subject to contributions;

- amounts of assessed contributions;

- the amount of benefits (payments) transferred at the expense of the Social Insurance Fund.

If the policyholder does not keep records of insurance premiums, the Federal Tax Service may hold him accountable.

Article 120 of the Tax Code of the Russian Federation establishes liability for violations of the rules for accounting for taxable items. Under this article, the policyholder may be held liable in the form of a fine.

There is no officially approved form of registration card. Policyholders need to develop it themselves.

A sample of filling out an insurance premium registration card can be downloaded in the attachments to the article.

How to fill out the card

Most employers, when filling out a card, will only have to enter information on the first page. In the upper right corner, tariff codes for compulsory medical insurance, compulsory medical insurance and social insurance, as well as key rates, are indicated. In addition, indicate information about the payer and recipient of payments. When creating such a card in 1C, all information is entered automatically. After this, a table is formed that reflects all monthly accruals on an accrual basis. If any payments are not subject to insurance premiums, they are indicated separately. At the bottom, the bases are indicated, as well as the total amounts of contributions for each area.

The second page is filled out only for employees employed in hazardous industries. The table is compiled for additional payments in amounts individually for hazardous areas. The sheet with expenses indicates all insurance cases necessary for payment from the budget. Each line reflects the total values, amounts from the budget, as well as the number of payments. Each section must contain the signature of the chief accountant (

Report “Calculation of insurance premiums”: guidelines for creating in 1C: ZUP 8.3.1.

All companies with at least one employee on staff are required to submit insurance premium calculations to the Federal Tax Service. This information is necessary to track the number and income level of employees. Many people have difficulty generating this report, so we have prepared practical material on the features of creating calculations for insurance premiums in the 1C: ZUP 8.3.1 program.

Stage I. Preparatory

Accrual of income to employees in 1C programs is the basis for generating the “Calculation of insurance premiums” report. An employee's income may include the following accruals:

- wage;

- monthly bonuses;

- quarterly;

- annual;

- temporary disability benefits;

- vacation pay;

- and so on.

In the program "1C: ZUP 8.3.1." accounting is carried out according to accrual documents. Elements of the directory “Methods of reflecting salaries in accounting” (section Settings → Reflecting salaries in accounting) are synchronized with the same elements of the directory in the program “1C: BP 8.3.0.”

In order to correctly reflect and generate insurance premiums in the program, you should make the appropriate tariff settings (section Salary → See also → Types of insurance premium tariffs). Rice. 1.

The calculation of the base for calculating insurance premiums is the document “Calculation of salaries and contributions” (section Salary → Calculation of salaries and contributions). Rice. 2.

Click on the “Create” button to create a document and indicate the period for calculating salaries and contributions. Then click the “Fill” button to reflect the employees for whom “Salaries and contributions are calculated.” To obtain information about the base for calculating insurance premiums, you can use the “Analysis of contributions to funds” report (section Taxes and contributions → Reports on taxes and contributions → Analysis of contributions to funds). Rice. 3.

The generated salary accruals and insurance premiums are reflected in the document “Reflection of salaries in accounting.” It displays accrued income and insurance premiums for each employee for the month of accrual.

To correctly reflect insurance premiums in the “Calculation of Insurance Premiums” report, you must correctly indicate the status of the insured person (section Personnel → Employees → Insurance link or in the “Individuals” directory). In the personal card of an employee or individual, you must indicate the date of change of status.

Stage II. Generating a report

After we performed in the program “1C: ZUP 8.3.1.” After all the necessary settings and charges, you need to proceed to generating the “Calculation of insurance premiums” report. It is filled out in the section Reporting → Certificates-1C reporting. Click the “Create” button to select the “Calculation of insurance premiums” report and indicate the period for generating the report. The document consists of a title page and sections for reflecting information on the calculation of insurance premiums. Section 1 contains data on the obligations of insurance premium payers. It is filled out according to the ten Appendices that relate to it. This section should reflect the total data on insurance premiums required for payment to the budget. More detailed data on the assignment of contributions is provided in the appendices to this section.

Section 2 “Calculations for insurance premiums” is intended for peasant (farm) farms (peasant farms). Section 3 contains personalized information about individuals, that is, a list of personal data about individuals. So, in addition to the full name and SNILS, the TIN, date of birth, citizenship of the employee, information about the employee’s identity document are provided. The data in this section is compiled based on the results of the last three months of the reporting year.

Cases when section 3 of the report “Calculation of insurance premiums” is completed:

- If payments are made to employees under employment or civil law contracts.

- When an employee is on leave without pay.

- When an employee goes on maternity leave, in the calculation of insurance premiums in Section 3 for an employee on maternity leave, a report is generated without filling out subsection 3.2 on payments.

- If the organization has only one employee, including the director, who is the founder.

- If in the accounting quarter accruals and payments were made for dismissed employees.

The title page, Section 1, Subsections 1.1 and 1.2, Appendix 1, Appendix 2 and Section 3 are made up of all organizations and individual entrepreneurs, payers of insurance premiums, making payments to individuals. Rice. 4.

The remaining sections and applications are formed as necessary, if there is information to fill out.

In the program "1C:ZUP 8.3.1." The “Calculation of insurance premiums” report is generated automatically, subject to the conditions for the correct and timely formation of salaries in the program.

To correctly generate the “Calculation of Insurance Premiums” report, you need to update the program to the current version. Since January 2017, the Federal Tax Service Inspectorate has introduced new conditions for accepting reports: personal data of individuals must completely match the data in the Federal Tax Service Inspectorate database. If the data on employees does not match the data in the Federal Tax Service Inspectorate database, the report will not be accepted by the Federal Tax Service Inspectorate.

In this article, we have highlighted the main points that you should pay attention to when generating the “Calculation of insurance premiums” report. To summarize, I would like to note that correct accounting of the accrual and payment of wages and other charges is an advantage for the correct formation of this document. We wish you successful completion of your annual reporting!

Dear readers, submit your reports without any problems! Our consultants have extensive experience in 1C programs and are ready to help you with the generation of any report. Book a consultation here.

If you liked the article, like it and share it with your colleagues.

Work in 1C with pleasure!

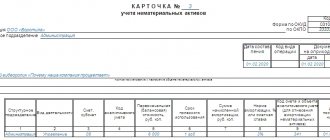

Sample card for individual accounting of accrued payments

The classic card form is contained in Excel format. The accounting card acts as an accounting certificate. This document is primary and mandatory for completion for each policyholder. Materials are contributed based on accrued insurance premiums, as well as expenses for insured events. In addition, separate data is provided for employees who are employed in hazardous industries. Completing these documents is mandatory for each organization. Even if the form in which accounting is carried out is subject to change, the company is obliged to approve it each time in the accounting policy.

Sample insurance payment card

Reporting

To analyze insurance premiums accrued to an employee, use the “Insurance Premium Accounting Card” report.

Menu: Salary – Accounting for personal income tax and taxes (contributions) from the payroll – Accounting card for insurance contributions

Tab: Salary – Insurance contribution card

The card displays taxable and non-taxable payments to the employee, the base for calculating contributions, and the amount of contributions:

Regulated reports to the Pension Fund and the Social Insurance Fund are entered through the “Regulated and financial reporting” form.

Menu: Reports – Regulated reports

In this form, in the “Reporting to funds” section, you must select the appropriate report:

First, the period selection form opens, where you need to specify the period for generating reports. After this, the report form itself opens. Sections are located on separate tabs. By clicking the “Fill” button, automatic filling occurs, and all sections of the report are filled in. In some cases, it may be necessary to manually enter data in certain sections (for example, information about a document confirming an employee’s disability, to apply a reduced tariff, etc.).

Section 1 of the RSV-1 form provided to the Pension Fund. Accruals and payments are reflected (since the document “Calculations for insurance premiums” was introduced):

Section 1 of Form 4-FSS provided to the FSS. Reflects accruals, payments, expenses for the purposes of mandatory social services. insurance:

Regulated reports are saved in the program. Each report can be printed (the “Print” button), as well as a file can be generated for transmission to the Social Insurance Fund or Pension Fund (the “Upload” button).

The procedure for filling out a personal T-2 card

The employee’s personal card T-2 has the following features:

- Filled out exclusively based on information confirmed by documents.

- Code ciphers for data to be encoded are taken from the corresponding all-Russian classifiers.

- Contains personal information that is not subject to disclosure by HR employees.

- It is certified by several signatures of the employee to whom it is dedicated.

You will find a line-by-line algorithm for filling out a personal card in the HR Guide from ConsultantPlus, having received free access to the system.

The card is filled out during the entire period of work of the employee with whom it is associated with the employer who issued this document. Some information is entered when hiring, and then supplemented with data that arose during work, and completed with the details of the dismissal document.

For more information on drawing up a dismissal order, read the article “Drawing up a dismissal order (form, form, sample)” .

Results

The T-2 personal card, issued separately for each hired employee, contains all personal information about him: both that arose before he joined the employer, and that was formed during the period of work with him.

Sources:

- Information from the Ministry of Finance of Russia N PZ-10/2012

- Resolution of the State Statistics Committee of the Russian Federation dated January 5, 2004 N 1

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.