For a whole year now, tax authorities have been operating a scheme according to which, if a taxpayer detects signs of fictitiousness, they cancel (nullify) the VAT and income tax returns. The actions of the tax office in this case are not regulated by legislative acts; they apply exclusively to internal departmental rules. However, many taxpayers have already encountered this problem and the proceedings are even going to court. In this article we will consider whether the tax office can reset the VAT and income tax returns and what to do if this happens.

Can the tax office reset the VAT return?

On July 10, 2022, the Tax Service issued a letter on the issue of preventing violations of tax legislation, where it was proposed to determine in advance those companies and entrepreneurs who submit VAT and income tax returns signed by fictitious directors.

Let's figure out whether the actions of the tax authorities are legal. Such a procedure as refusal to accept a declaration signed by an unidentified person is not enshrined in any legislative act. However, tax authorities have been using it for about a year. In addition, they also nullify (cancel) VAT returns if they detect tax discrepancies between counterparties. That is, they simply do not recognize the information contained in the declaration. In this case, the taxpayer can only contact the tax office to find out the reasons for what happened. The consequence of canceling the declaration will be the loss of time to prove that you are right, or the obligation to pay additional tax to the budget. This practice will have to come from tax authorities quarterly and annually, respectively, for VAT and income tax (

List of control ratios

Control ratios are a reconciliation of VAT tax return indicators for compliance with the total amounts for the sections of the declaration. See them in the table from the Federal Tax Service.

Please note the abbreviations in the “Control ratios” column of the table:

- "R." - chapter;

- "st." - line;

- "gr." – graph;

- "adj." - application;

- “VAT” – VAT declaration.

Control ratios of the indicators of the tax return for value added tax, indicating a violation of the procedure for filling it out, in terms of implementing the provisions of paragraph 5.3 of Article 174 of the Tax Code of the Russian Federation

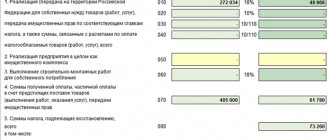

| No. | Control ratio | Description of Control Ratio |

| 1 | R. 3. art. 200 gr. 3 = r. 3. art. 118 gr. 5 - Art. 190 gr. 3 | Comparison of indicators within Section 3 of the Value Added Tax Declaration (hereinafter referred to as the Declaration) The amount of tax payable to the budget under Section 3 is equal to the difference in the total amount of tax calculated taking into account the restored tax amounts under Section 3 and the total amount of tax subject to deduction under Section 3 |

| 2 | Art. 040 rub. 1 = (Art. 200 R. 3 + Art. 130 R. 4 + Art. 160 R. 6) - (Art. 210 R. 3 + Art. 120 R. 4 + Art. 080 R. 5 + Art. 090 RUR 5 + RUR 170 6) | Comparison of the indicators of Section 1 of the Declaration with Sections 3, 4, 5, 6 of the Declaration The amount of tax payable to the budget in accordance with paragraph 1 of Article 173 of the Tax Code of the Russian Federation in Section 1 of the Declaration is equal to the total reflected for payment under Sections 3, 4, 5 , 6 Declarations |

| 3 | gr. 5 tbsp. 118 rub. 3 + amount of art. 050 and 130 rub. 6 amount art. 060 for all sheets of the river. 2 + amount of art. 050 rub. 4 + art. 080 rub. 4 = [st. 260 + art. 265 + art. 270] p. 9 + [st. 340 adj. 1 to r. 9 dVAT + art. 345 adj. 1 to r. 9 dVAT + art. 350 adj. 1 to r. 9 dVAT - Art. 050 adj. 1 to r. 9 - Art. 055 adj. 1 to r. 9 dVAT - Art. 060 adj. 1 to r. 9 dVAT] | Comparison of indicators of the total value of Sections 2, 3, 4, 6 and 9 of the Declaration The total amount of calculated tax for Sections 2, 3, 4, 6 of the Declaration is equal to the total amount of tax for Section 9 of the Declaration, taking into account the Appendix to Section 9 of the Declaration |

| 4 | Art. 190 rub. 3 + amount line 030 and 040 rub. 4 + art. 080 and 090 rub. 5 + art. 060 rub. 6 + art. 090 rub. 6 + art. 150 rub. 6 = st. 190 rub. 8 + [st. 190 adj. 1 to r. 8 - Art. 005 adj. 1 to r. 8] | Comparison of indicators of the total value of Sections 3, 4, 5, 6 and 8 of the Declaration The total amount of deductions for Sections 3, 4, 5, 6 of the Declaration is equal to the total amount of deductions for Section 8 of the Declaration, taking into account the Appendix to Section 8 of the Declaration |

| 5 | amount art. 180 rub. 8 = st. 190 on the last page p. 8 | Identification of inconsistencies in Section 8 of the Declaration The sum of all deductions line by line under Section 8 of the Declaration is equal to the total amount of deductions under Section 8 |

| 6 | page 005 adj. 1 to r. 8 dVAT + amount art. 180 adj. 1 to r. 8 dVAT = art. 190 on the last page adj. 1 to r. 8 dVAT | Identification of inconsistencies in Appendix 1 to Section 8 of the Declaration Addition of the total tax amount according to the purchase book of Appendix 1 to Section 8 and the tax amount on the invoice, the difference in the tax amount on the adjustment invoice accepted for deduction is equal to the total tax amount according to Appendix 1 to Section 8 Declarations |

| 7 | amount art. 200 rub. 9 = st. 260 rub. 9 on last page | Identification of inconsistencies in information in Section 9 The amount of tax on the invoice, at a rate of 20% of Section 9 of the Declaration, is equal to the amount of tax according to the sales book at a rate of 20% of Section 9 of the Declaration on the last page |

| 8 | amount art. 210 rub. 9 = st. 270 rub. 9 on last page | Identification of inconsistencies in information in Section 9 The amount of tax on the invoice, at a rate of 10% of Section 9 of the Declaration, is equal to the amount of tax according to the sales book at a rate of 10% of Section 9 of the Declaration on the last page |

| 9 | amount art. 205 rub. 9 = st. 265 rub. 9 on last page | Identification of inconsistencies in information in Section 9 The amount of tax on the invoice, at a rate of 18% of Section 9 of the Declaration, is equal to the amount of tax according to the sales book at a rate of 18% of Section 9 of the Declaration on the last page |

| 10 | Art. 050 adj. 1 to r. 9 dVAT + amount art. 280 adj. 1 to r. 9 dVAT = art. 340 adj. 1 to r. 9 dVAT | Identification of inconsistencies in information in Appendix 1 to Section 9 Addition of the total tax amount according to the sales book at a rate of 20% of Appendix 1 to Section 9 of the Declaration is equal to the amount of tax according to Appendix 1 to Section 9 of the Declaration at a rate of 20% |

| 11 | Art. 060 adj. 1 to r. 9 dVAT + amount art. 290 adj. 1 to r. 9 dVAT = art. 350 adj. 1 to r. 9 dVAT | Identification of inconsistencies in information in Appendix 1 to Section 9 Addition of the total tax amount according to the sales book at a rate of 10% of Appendix 1 to Section 9 of the Declaration is equal to the amount of tax according to Appendix 1 to Section 9 of the Declaration at a rate of 10% |

| 12 | Art. 055 adj. 1 to r. 9 dVAT + amount art. 285 adj. 1 to r. 9 dVAT = art. 345 adj. 1 to r. 9 dVAT | Identification of inconsistencies in information in Appendix 1 to Section 9 Addition of the total tax amount according to the sales book at the rate of 18% of Appendix 1 to Section 9 of the Declaration is equal to the amount of tax according to Appendix 1 to Section 9 of the Declaration at the rate of 18% |

Who can have their reporting canceled?

Returning to the above letter, we can conclude that the actions of the tax authorities are directed against shell companies, including companies in which the signatories are nominee directors. The letter contains 22 signs confirming fictitious directors, fictitious companies and, accordingly, fictitious transactions and reporting. For example, some of them:

- submission of an updated declaration that contains an incorrect serial number of the adjustment;

- evasion of interrogations by heads of organizations or entrepreneurs (more than two refusals);

- interrogation of company managers or entrepreneurs in the presence of a lawyer (other representative);

- the manager and entrepreneur do not live at the place of registration;

- representatives of taxpayers' interests are registered in other constituent entities of the Russian Federation;

- newly created organization in 2022;

- for previous tax periods, organizations or individual entrepreneurs submitted zero declarations;

- income indicated in the tax return is as close as possible to expenses (VAT deductions are more than 98%);

- the actual location of the organization differs from the place of registration;

- the organization or individual entrepreneur has not entered into a rental agreement with the owner of the premises;

- the average number of employees in the organization is 1 person or less;

- the head of the company has no income in his company;

- organizations or individual entrepreneurs change their place of registration;

- information about the change of manager was entered immediately before reporting;

- the organization did not open a current account within 3 months after registration;

- taxpayer's current accounts are closed;

- The taxpayer has more than 10 current accounts opened;

- the fact of cashing out funds has been established;

- the head of the organization is a non-resident of the Russian Federation.

Important! If the tax authorities detect one or more of the above signs, the tax authorities will conduct an audit.

They cannot immediately cancel the reporting. In order to collect the necessary evidence, tax officials conduct interrogations, inspect the premises of the taxpayer at the legal address, examine documents, request the necessary documents from banks and certification centers.

If the suspicions of the tax authorities are confirmed, they can cancel the received VAT or income tax return.

What should you be wary of?

As a rule, most entrepreneurs are now most often called to the tax office to provide explanations on their activities or to a “commission.” Tax audits are not ordered immediately after a “gap” is discovered, as this is too costly and ineffective. And the general policy in the field of tax administration is aimed at reducing audits. That is why you will first go to a commission at the Federal Tax Service of the Russian Federation.

At the same time, such calls indicate the risk of an audit. Therefore, as soon as the Federal Tax Service becomes interested in you, you must immediately begin preparation. And already at this stage you need to seek professional help from a lawyer who specializes in resolving such issues.

In particular, if you have received a Notice to appear at the tax authority to provide explanations on the company’s activities, or a Request to provide documents and information on a particular counterparty for a quarter or more, then our tax lawyers will help you navigate and correctly build a dialogue with the Federal Tax Service. We will tell you what documents need to be submitted to the Federal Tax Service, including in addition to those requested.

Reasons for canceling a VAT return

Based on the above, the following reasons for canceling the declaration can be identified:

- The director of the organization admitted that he does not participate in the company’s activities, did not submit a declaration, and also did not issue a power of attorney for its presentation.

- The leader was disqualified.

- The declaration was submitted by a company or individual entrepreneur that has already been excluded from the register;

- The director of the organization or entrepreneur has died or is declared missing;

- The head of the company is in prison.

Cancellation of a declaration is possible only after approval of the Federal Tax Service. After its cancellation, the reporting will be entered into the “Register of Declarations Not Subject to Processing”. After this, an automatic message is generated using a special program. This notification is new; tax authorities have not previously used this form of notification.

Important! A notice of cancellation of a VAT tax return is issued by the tax authorities within 5 working days.

How reporting is canceled

Resetting of reporting occurs during a desk audit, often automatically. The Tax Code of the Russian Federation specifies the period during which the tax office can nullify a VAT or profit return - the period for a desk audit is 3 months, during which at any time the tax authorities have the right to identify a discrepancy that will lead to a refusal to accept the report and its cancellation.

If during the desk audit the reporting does not pass the test for compliance with at least one of the criteria, the tax authorities will refuse to accept it and cancel it. The payer will be sent a notice of refusal to accept the report on the same or the next day after the grounds are identified. The form of notice of cancellation was approved by Order of the Federal Tax Service No. ED-7-2/488 dated May 17, 2021. After this, the document will be included in the register of declarations that cannot be processed, and it will be assigned a special encoding. The taxpayer is given time for corrections (clauses 5.3, 5.4 of Article 174 of the Tax Code of the Russian Federation) when the Federal Tax Service resets VAT returns for 2022 - 5 days from the date of receipt of the notification.

Procedure for canceling a VAT return

Thus, the procedure for canceling a VAT return, as well as an income tax return, will be as follows:

- First of all, tax authorities must find signs (one or more of 22 signs) of fictitiousness in the taxpayer.

- They conduct interrogations, examinations, interrogations and other tax control activities;

- Submission of a declaration by the taxpayer to the tax office;

- Cancellation of the declaration for one of 5 reasons.

- Notification of the taxpayer about the cancellation of the declaration within 5 days.

After the cancellation process is completed, the declaration is considered unsubmitted, and information about the cancellation will be transferred to the VAT ASK.

Can the Federal Tax Service cancel an accepted taxpayer report?

In July 2022, amendments to the Tax Code of the Russian Federation, introduced by Federal Law No. 374-FZ of November 23, 2020, on recognizing declarations as not submitted, came into effect. From this date, employees of the Federal Tax Service of Russia have the right to reset tax reporting - to recognize it as not submitted if, during a desk audit, a discrepancy in the declaration is discovered. The procedure is established by order of the Federal Tax Service No. ED-7-15/519 dated May 25, 2021. This measure currently applies only to tax reports:

- according to VAT;

- on income tax.

Previously, the Federal Tax Service Inspectorate reported on such a measure of influence on negligent taxpayers as cancellation of a VAT return in letter No. ED-4-15/ [email protected] as a preventive measure against tax offenses. But then the norms of the Tax Code of the Russian Federation did not provide for the possibility of canceling any reporting submitted by the taxpayer and accepted by the inspection. Now tax officials have such an opportunity. The new procedure applies to VAT returns filed from 07/01/2021.

What to do if your VAT return has been canceled

First of all, it should be remembered that the cancellation of a declaration by tax authorities occurs solely according to internal instructions, that is, regarding tax legislation, the nullification of a declaration by tax authorities is not considered . However, this does not eliminate problems with the tax authorities. In order to prevent the consequences of cancellation, the taxpayer should protect himself in advance. To do this, he can personally meet with the counterparty before completing the transaction, and also request his documents. That is, the taxpayer should personally make sure that the counterparty with whom he enters into a transaction is not a shell company, and that its manager is a nominee director.

Important! It should be remembered that the VAT return is processed quarterly, which means you need to receive information about the taxpayer regularly and constantly update it.

If, in the opinion of the taxpayer, the cancellation of the declaration is unfounded, he has the right to go to court. By the way, similar claims have already taken place and they had a positive result (decision of the court of the Tomsk region No. 67-8529/2017 dated January 23, 2022).

How will they prove

To revoke a declaration, it is necessary to prove that one of the grounds mentioned above exists. To do this, inspectorates must select taxpayers whose reports are suspicious . And then carry out control measures against them.

The letter lists a fairly large list of signs that may indicate that declarations are signed by unidentified or unauthorized persons. Many of these signs are well known:

- zero reporting for several periods;

- exceeding the safe percentage of VAT deductions;

- cash withdrawal;

- income equals expenses;

- frequent migrations between tax authorities;

- not being at the place of registration;

- inaccurate information in the register;

- lack of staff;

- lack of a lease agreement;

- violations related to accounts - transit transfers, a large number or, conversely, absence of accounts, location of banks in other regions;

- suspicious behavior of the manager - working without wages, living outside the place of registration or even in another region, failure to appear for questioning.

What’s new: tax authorities should be suspicious primarily of organizations registered in 2022 and later. Another suspicious fact is that the director or individual entrepreneur comes for questioning with a lawyer.

Each of these signs separately cannot be regarded as independent evidence of the mentioned violations. However, if there are several such signs, tax authorities may classify a business entity as one-day. However, the letter does not indicate exactly how many signs a suspicious taxpayer should have.

What to do if the counterparty’s declarations are canceled

A company or individual entrepreneur may encounter such a situation when the counterparty’s declaration has been canceled. In this case, information about the exception will be reflected in the VAT ASC, which is quite dangerous. In this case, the tax authorities will be asked to provide explanations and also pay additional VAT.

To begin with, the taxpayer can request information from his counterparty and find out the reason for rejecting the return. If the cancellation is due to the fictitiousness of the director, then he can be asked to change the information about the director and resubmit the report. Or you will have to delete all deductions for this counterparty.

What happens if negative signs are detected?

If a company meets a number of negative criteria, it is scheduled for inspection. In particular, these events are carried out:

- Summoning the director or entrepreneur for questioning. During the process, the manager will be asked to explain any oddities found.

- Inspection of premises. During the process, they can verify, for example, the authenticity of the registration address.

- Sending requests to the bank. The tax office has the right to send a request to the bank about who exactly uses banking services. In particular, whoever opens the account withdraws money.

- Sending a request to a certification center. This center issues keys for electronic signatures. The tax office asks him for documents confirming who exactly interacts with the institution.

Verification is required to confirm that the company is a shell company.