From October 1, 2016, on the basis of Part 6 of Art. 5 of the Federal Law “On Auditing Activities”, the customer of a mandatory audit (the audited entity) is obliged to enter information about the results of such an audit into the Unified Federal Register of legally significant information about the facts of the activities of legal entities, individual entrepreneurs and other economic entities. The exception is cases when such information constitutes a state or commercial secret, as well as other cases established by federal laws.

Please note that the mandatory audit is carried out in relation to annual reporting, therefore information from the audit report at the end of the year is subject to mandatory reporting of the results of the audit.

The Unified Federal Register is located on the website https://fedresurs.ru and the following information about the results of the mandatory audit should be reflected there:

— data identifying the audited person (TIN, OGRN, SNILS, if available);

— data identifying the audit organization (individual auditor) (TIN, OGRN, SNILS, if available);

— a list of the accounting (financial) statements of the audited entity in respect of which a mandatory audit was carried out, the period for which these statements were compiled;

— date of the auditor’s report on the accounting (financial) statements of the audited entity;

— the opinion of the auditing organization ( individual auditor) on the reliability of the accounting (financial) statements of the audited entity, indicating the circumstances that have or may have a significant impact on the reliability of such statements.

The procedure for maintaining the Unified Federal Register and publishing the information contained in it is established by the Federal Law “On State Registration of Legal Entities and Individual Entrepreneurs.”

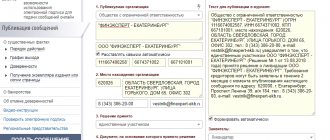

An example of disclosure of information about a mandatory audit on the Unified Federal Register portal

Information about the audit can be posted either by the organization itself in which the mandatory audit was carried out, or by a notary.

Information about the mandatory audit conducted must be placed in the Unified Federal Register no later than 3 business days from the date of signing the audit report .

ALGORITHM FOR POSTING INFORMATION ON THE PORTAL:

— obtain an electronic signature for working on the fedresurs portal from a special operator (please note that an electronic signature is not suitable for submitting reports to the Federal Tax Service);

— log into the portal with digital signature, install software if necessary;

— issue an invoice and pay it at ZAO INTERFAX (as a rule, funds are available the next day);

From July 1, 2022, the Operator will charge a fee of 902 rubles for entering and posting information 51 kopecks for each message (until 07/01/2021 - 860 rubles 35 kopecks, including VAT 20% (143 rubles 39 kopecks).

- if there is an advance payment - publish information about the mandatory audit on the portal (you can attach a scan of the audit report - not a mandatory requirement);

— sign the act and invoice for the publication and receive them with digital signature from your personal account.

Penalties for late posting of information

Article 14.25 of the Code of Administrative Offenses of the Russian Federation establishes administrative liability (parts 6-8 are introduced into Article 14.25 by Federal Law dated December 29, 2015 N 391-FZ) for late submission of information, as well as for failure to provide or submission of unreliable or knowingly false information to the Unified Federal Register of Information on Facts activities of legal entities.

Article 14.25. Violation of legislation on state registration of legal entities and individual entrepreneurs

6. Failure to timely submit information about a legal entity or an individual entrepreneur to the Unified Federal Register of information on the facts of the activities of legal entities in cases where such submission is provided for by law -

entails a warning to officials or the imposition of an administrative fine on officials in the amount of 5,000 rubles.

7. Failure to submit or submission of false information about a legal entity or an individual entrepreneur to the Unified Federal Register of information on the facts of the activities of legal entities in cases where such entry is provided for by law -

shall entail the imposition of an administrative fine on officials in the amount of 5,000 to 10,000 rubles.

8. Repeated commission of an administrative offense provided for in Part 7 of this article, or the entry into the Unified Federal Register of information about the facts of the activities of legal entities of knowingly false information -

shall entail the imposition of an administrative fine on officials in the amount of 10,000 to 50,000 rubles or disqualification for a period of one to three years.

Legislation on accounting documentation

More recently, until January 2013, issues of maintaining financial documents affected only some entrepreneurs. Only organizations that were on the general taxation system were required to keep books. Those on the simplified system may not have documented their activities as thoroughly.

Since January 2013, the requirements of Order No. 402 of the Ministry of Finance of December 6, 2011 came into force, according to which all enterprises are required not only to maintain accounting documentation, but also to annually report on it to regulatory authorities.

True, with the tightening of measures, there was also a relaxation: entrepreneurs were relieved of the need to submit interim reports. Now only a very small number of organizations, whose activities are regulated by special federal laws, submit reports not only once a year, but also once every three, six and nine months.

On the one hand, this made life easier not only for entrepreneurs, but also for tax officials. On the other hand, the burden on the tax office at the beginning of the reporting period increases enormously.

However, it is worth noting that the Russian accounting system is systematically moving towards international standards and a more simplified scheme, therefore, at the moment, far from the latest innovations and changes have been introduced. The process of searching for optimal forms of documents and their execution will continue and we should expect other innovations in the new year.

Back to contents

Special procedure for individual organizations

A special procedure for presenting annual financial statements has been defined:

- for organizations whose annual financial statements contain information classified as state secrets in accordance with the legislation of the Russian Federation;

- for organizations in cases established by the Government of the Russian Federation.

The annual financial statements of such organizations are not included in the GIRBO. However, these organizations are still required to submit one copy of their annual accounting reports:

- to the tax authority;

- to the state statistics body.

The submission deadline is no later than three months after the end of the reporting period, i.e.

no later than March 31 of the year following the reporting year. These regulations come into force on January 1, 2022.

Why are financial statements necessary?

Any organization, even with the smallest staff, even with the smallest production, deals with finances, assets and some kind of business operations.

Once you have become a legally registered business and designated a statutory fund, all the money spent on and received from the business becomes profit and loss, assets and liabilities. And most of the actions performed for the development, stable operation of the enterprise, satisfaction of partners or clients - that is, performed within the framework of the work process - fall into the category of economic, property or financial transactions.

According to the law, all this must be recorded either on paper or in electronic form: timely, accurately, reliably and without distortion, both at the time of recording and in the future.

Accounting documents reflect all of the above: the movement of tangible and intangible assets, the state of assets, repaid and outstanding liabilities, and so on. Based on the primary accounting documentation, if necessary, final reports are drawn up, which contain the same information, but in a more concise and convenient form for study.

Back to contents

Responsibility

For the absence (non-submission, non-publication) of an audit report on the Fedresource, the legislation provides for administrative liability : clauses 6-8 of Art. 14.25 of the Code of Administrative Offenses of the Russian Federation in the form of a fine in the amount of 5,000 to 50,000 rubles, and in case of a repeated offense - disqualification of the official from 1 to 3 years.

Consequences of failure to conduct a mandatory audit (fines)

1. Fines from tax authorities, executive authorities exercising control and supervision functions in the financial and budgetary sphere, the Accounts Chamber of the Russian Federation and control and accounting bodies of constituent entities of the Russian Federation (Article 28.3 of the Administrative Code).

For failure to provide an audit report to the tax authority, liability is not established (Article 14 of Law No. 402-FZ; subparagraph 5, paragraph 1, Article 23 of the Tax Code of the Russian Federation), however, the tax authority, having established during the inspection that the person being inspected does not have an audit report , has the right to draw up a protocol on an administrative offense.

Article 15.11 of the Code of Administrative Offenses of the Russian Federation provides for fines for gross violations of accounting and reporting rules, including for the lack of an auditor’s report on the accounting (financial) statements (if an audit of the accounting (financial) statements is mandatory). The amount of the fine for a manager for lack of a conclusion ranges from 5,000 to 10,000 rubles, and for a repeated violation - from 10,000 to 20,000 rubles, or the manager faces disqualification for a period of 1 to 2 years.

We also note that in accordance with paragraph 3 of Article 52 of Federal Law No. 208-FZ “On Joint Stock Companies”, information (materials) to be provided to persons entitled to participate in the general meeting of shareholders in preparation for the general meeting of shareholders of the company include , including the annual report of the company and the conclusion of the audit commission (auditor) of the company based on the results of its audit, annual accounting (financial) statements, auditor's report and the conclusion of the audit commission (auditor) of the company based on the results of the audit of such statements.

Thus, the absence of an audit report is a violation of the requirements of the law on the procedure for preparing and holding general meetings of shareholders, participants in limited (additional) liability companies and owners of investment shares of closed mutual investment funds, liability for which is provided for in Part 2 of Article 15.23.1 of the Code of Administrative Offenses of the Russian Federation and entails entails a fine:

— for citizens in the amount of 2 to 4 thousand rubles;

- for officials - from 20 to 30 thousand rubles or disqualification for up to one year;

- for legal entities - from 500 thousand to 700 thousand rubles.

2. Fines from the Bank of Russia

The most serious sanctions may be imposed by the Bank of Russia.

A public JSC is obliged to disclose an annual report and annual accounting (financial) statements (Article 92 of the Federal Law of December 26, 1995 No. 208-FZ “On Joint-Stock Companies”, hereinafter referred to as Law No. 208-FZ). Requirements for the content of the annual report of joint-stock companies are established in the Regulations on the disclosure of information by issuers of equity securities, approved. Bank of the Russian Federation dated December 30, 2014 No. 454-P

Failure by a joint-stock company an audit report on its website on the Internet , as well as failure to submit to shareholders, an audit report within the prescribed period is a violation of legal requirements regarding the presentation and disclosure of information on financial markets. Disclosure of information not in full (accounting statements must be disclosed together with the auditor's report), and (or) unreliable information, and (or) misleading information entails the imposition of an administrative fine:

- for officials - from 30,000 to 50,000 rubles. or disqualification for a period of 1 to 2 years;

— for legal entities — from 700,000 to 1,000,000 rubles. (clause 2 of article 15.19 of the Code of Administrative Offenses of the Russian Federation).

3. Fines from Rosstat

For failure to provide an audit report to a set of financial statements submitted to Rosstat (in the case of a mandatory audit), the organization and its official may face an administrative fine (Article 19.7 of the Code of Administrative Offenses of the Russian Federation):

— from 300 to 500 rubles (for officials);

— from 3 thousand to 5 thousand rubles (for legal entities).

At the same time, the imposition of a fine does not relieve the organization from the obligation to submit an audit report to the statistical authorities (clause 4 of article 4.1 of the Code of Administrative Offenses of the Russian Federation).

Let us note that the storage period of the auditor's report on the accounting (financial) statements is not limited (Part 1, Article 29 of Federal Law No. 402-FZ; Article 408 of the List, approved by Order of the Ministry of Culture of August 25, 2010 No. 558).

The statute of limitations for bringing to administrative liability for violation of accounting legislation is 2 years from the date of commission of the administrative offense (Article 4.5 of the Code of Administrative Offenses of the Russian Federation).

Users of accounting documentation and reporting

From the title it may seem that the main users of the above documents are accountants, and that’s all. But this is not true at all. Since the main purpose of financial or accounting documentation is an accurate reflection of the state of the enterprise in measurable indicators and figures, virtually anyone can be a user of the reporting.

There are internal and external users.

Internal ones include:

- heads of enterprises, structural divisions, departments - those people who are on the staff of the enterprise and use documentation to analyze the current situation and make the necessary management decisions;

- chief accountants of the enterprise and financiers - again, people on staff who study and maintain these documents to perform their immediate job responsibilities;

- internal auditors are people on staff and appointed by management directly to conduct reporting audits.

External users include:

- auditors - representatives of third-party organizations who are not directly interested in the activities of the enterprise, but study the papers in order to give an accurate assessment of the activities;

- shareholders and investors who are persons interested in the activities of the enterprise, but do not directly participate in its work. Such people study the documentation in order to determine whether the investment is worthwhile;

- representatives of tax and other government services who study reporting in order to check the activities of the enterprise and maintain documentation for compliance with legal requirements;

- clients and potential clients who, based on documentation, draw conclusions about the profitability and stability of the enterprise and make decisions, for example, about the start of service.

Most external users gain access to an enterprise's financial statements due to their public nature.

Back to contents

GIRBO

State Information Resource of Accounting Reports (GIRBO) is a set of financial statements of organizations required to prepare such reports, as well as audit reports on them in cases where the financial statements are subject to mandatory audit.

Accounting reporting is not included in GIRBO:

- public sector organizations;

- Bank of Russia;

- religious organizations;

- organizations whose annual financial statements contain information classified as state secrets in accordance with the legislation of the Russian Federation;

- organizations in cases established by the Government of the Russian Federation.

In addition, the GIRBO does not include the latest accounting records of reorganized and liquidated legal entities.

GIBO is formed and maintained by the federal executive body authorized for control and supervision in the field of taxes and fees, i.e. Federal Tax Service.

GIRBO is formed from:

1) mandatory copies of reports submitted by organizations to the tax authorities;

2) annual financial statements of organizations submitted to the Central Bank. The Bank of Russia transmits to GIRBO information in electronic form containing the annual accounting records of organizations supervised by it, as well as audit reports on it.

All interested parties will have access to the information contained in the GIRBO.

Moreover, we are talking about access to a full set of annual accounting reports and the auditor’s report on it. The rules for using GIRBO will be approved by the Federal Tax Service of Russia.

Access to the information contained in GIRBO will be provided free of charge.

However, in cases determined by the Government of the Russian Federation, a fee will be charged .

Such cases may include, for example, providing a copy of the annual accounting records of a specific organization on paper. The amount and procedure for collecting such fees are established by the Government of the Russian Federation.

The provisions of the law dedicated to GIRBO come into force on January 1, 2022. From this date, the Federal Tax Service begins, and Rosstat ceases, to exercise the authority to form and maintain the GIRBO.

In particular, Rosstat will stop collecting legal copies of financial statements, including revised ones, as well as audit reports on them for the reporting period of 2022 and reporting periods that expired before January 1, 2022.

The first reporting included in GIRBO will be the annual financial statements of organizations for 2022. In this regard, the Federal Tax Service will not provide access to the financial statements of organizations for reporting periods that expired before January 1, 2019.

Interested parties will be able to access the annual financial statements of organizations for 2014 - 2022 as before in Rosstat. Rosstat will provide this service until the expiration of the storage period for the specified accounting records, i.e. at least 5 years after the reporting year. In other words, access to the annual financial statements of organizations for 2014 - 2022 will be provided by Rosstat until the end of 2023.

What does publicity mean?

According to the Law “On Accounting” (clause 16), some enterprises are required to make information from their financial statements publicly available so that anyone can familiarize themselves with them.

Back to contents

Who is required to publish reports?

According to the law, individual enterprises whose activities are directly related to finance, investment, and the like are required to annually provide their accounting data for review to any interested party.

Such enterprises include:

- banks;

- credit organizations;

- exchanges;

- Insurance companies;

- open joint stock companies;

- investment funds;

- funds created from private, public and government funds;

- limited liability companies that have placed their bonds or other securities publicly.

Back to contents

When should reports be published?

Since the organization must initially prepare all the information, carefully double-check it, and also submit it to regulatory authorities - otherwise it will be forced to pay a large fine - publication of documents in the public domain is carried out only after all these operations have been completed. But it must be carried out no later than the first of July of the year following the reporting year. That is, information for 2022 must be published no later than July 1, 2022.

Each enterprise establishes the procedure for disclosing information independently. By law, two basic requirements must be met: accessibility to any interested party (in the case of, for example, an insurance company or a bank) and compliance with publication deadlines. The method of bringing data to the attention of users can be any:

- publication in certain printed publications - newspapers or magazines;

- placement on the official website of the enterprise;

- publishing special brochures or booklets and distributing them among users.

Back to contents

Taking into account expenses

In accounting, the costs of publishing the statements in question are expenses for ordinary activities (clauses 5, 7 of PBU 10/99 “Expenses of an organization”, approved by order of the Ministry of Finance of Russia dated May 6, 1999 No. 33n). Moreover, expenses associated with the publication of financial statements, including expenses for the preparation, publication and mailing of a special brochure or booklet with accounting records, are included in the cost of products (works, services) as costs associated with production management.

But the amounts reimbursed for the costs of copying and sending reports received from interested users are credited to the profit and loss account.

The costs of publishing financial statements reduce taxable profit only if the obligation of such an event is imposed on the company by law. In this case, expenses are written off as other on the basis of subparagraph 20 of paragraph 1 of Article 264 of the Tax Code.

Audit and publicity

According to legal requirements, all enterprises whose financial statements are subject to publication in the public domain must undergo an annual audit.

Previously, the inspectors’ conclusions had to be submitted along with the company’s documents to the regulatory authorities; since 2013, this rule is no longer in effect, but for public reports all the previous requirements have been preserved.

The inspection must be carried out by third-party organizations with appropriate permission and trained specialists.

During the audit we study:

- content and composition of financial reporting forms;

- correspondence of various indicators from various documents to each other;

- interconnection of indicators;

- correctness of evaluation of reporting items;

- correct formation of consolidated reporting.

Without a signed audit report, the company's documents are considered invalid. The audit is carried out completely: for the entire enterprise as a whole, for the entire reporting period.

In addition to independent verification, some companies are also required to hold a shareholders meeting before publication, at which information is approved for release to the public.

Back to contents

Regular organizations

All organizations required to prepare financial statements, with the exception of religious, credit and non-credit financial organizations, submit one copy of their prepared annual financial statements to the tax authority at their location.

Let us remind you that previously reports were submitted to Rosstat (with the exception of public sector organizations and the Central Bank) and the tax authority.

How to submit reports now:

- presentation form - in the form of an electronic document (previously - on paper or in the form of an electronic document);

- submission method - via TKS through an electronic document management operator, which is a Russian organization and meets the requirements approved by the Federal Tax Service;

- submission deadline - no later than three months after the end of the reporting period, i.e. no later than March 31 of the year following the reporting year. The annual financial statements of the Central Bank as part of the annual balance sheet and financial results statement are submitted no later than May 15 of the year following the reporting year;

- presentation formats are approved by the Federal Tax Service;

- the procedure for submission is approved by the Federal Tax Service (previously it was approved by Rosstat).

If the organization's annual financial statements are subject to mandatory audit, then an auditor's report on it is submitted to the tax authority along with a copy of such statements. It appears:

- in the form of an electronic document (previously - on paper or in the form of an electronic document);

- together with a copy of the financial statements or within 10 working days from the day following the date of the auditor's report, but no later than December 31 of the year following the reporting year.

The new procedure for presenting accounting reports comes into force starting with the annual financial statements for 2022. At the same time, small businesses are required to submit accounting records in electronic form starting with the annual financial statements for 2020; Such entities can submit reporting for 2022 on paper or in the form of an electronic document of their choice.

Mandatory Public Reporting Requirements

The documents that the organization will provide to interested users must comply with all the requirements imposed on them by law.

Back to contents

General requirements

The main documentation requirements are:

- completeness – all data must be reflected in full;

- timeliness - every fact, every operation should be reflected as immediately as possible, as soon as it was completed;

- prudence - it is unacceptable to create hidden reserves, record premature income, and so on;

- consistency - analytical accounting data must be identical to the accounting data for turnover and balances on the last day of each reporting period;

- priority of content over form - economic activity should be taken into account according to its economic content, not its legal content;

- rationality - documentation must be maintained on production volumes and conditions of economic activity of the enterprise;

- reliability - documents should reflect the true state of affairs at the enterprise as fully as possible;

- neutrality - only facts should be reflected, without propaganda information, advertising or the like;

- integrity - data should be reflected as much as possible, taking into account the activities of all branches, if any;

- sequence - information must be submitted in chronological order;

- materiality - reporting should contain only those information that are important for a correct assessment of the enterprise;

- Comparability – all data provided must be comparable with the same data for other periods.

In addition, reporting must be prepared in Russian and indicators must be entered in national currency, even if some transactions were carried out in foreign currency.

Back to contents

Content requirements

Since the publicity of financial statements means that anyone can read them at any time, some measures have been taken to protect enterprises and facilitate the preparation of documents: it is allowed to publish abbreviated forms of reports containing only the totals for the necessary sections.

For example, you may not include intermediate results; It is permitted not to include in documents information that constitutes a commercial or other secret of the enterprise.

Reports that are posted publicly must contain:

- full name of the organization and its legal form;

- reporting date and reporting period;

- clear indication of the currency and format of the presented numerical indicators;

- last name, first name, patronymic and full position of the persons who signed the reports;

- date of approval of documents at the general meeting;

- the address where you can review the report data and receive a copy of the documents;

- information about the branch of the State Statistics Committee to which the enterprise submitted its annual financial statements.

In addition, it is necessary to annually comply with the once accepted publication form and provide data for the previous period along with new data.

Back to contents

When does an audit become mandatory?

Certain types of organizations are subject to mandatory audit, regardless of their legal form. Such organizations include, in particular:

— joint-stock companies (including closed joint-stock companies) ;

— organizations whose securities are admitted to trading at stock exchanges and (or) other organizers of trading on the securities market;

— housing savings cooperatives (Article 54 Federal Law of December 30, 2004 No. 215-FZ “On Housing Savings Cooperatives”);

— developers (Article 18 of the Federal Law of December 30, 2004 No. 214-FZ);

— an organization that is a professional participant in the securities market;

— non-state pension or other fund;

A complete list of organizations that are required to conduct an audit is published on the website of the Ministry of Finance of the Russian Federation.

In addition, in general, an audit is required if the financial performance of the organization has reached the following values:

— revenue exceeds 400 million rubles;

and/or

— the balance sheet currency exceeds 60 million rubles.

Financial indicators are taken for the year preceding the reporting year. That is, the need to conduct an audit for 2022 is determined based on the results of an analysis of financial indicators for 2022.

Examples of cases of acceptable limitation of the volume of disclosed information

| THE AMOUNT OF DISCLOSURE INFORMATION PROVIDED FOR BY PBU | ACCEPTABLE LIMITATION OF THIS VOLUME |

| Income of the organization | |

With respect to revenue received from the execution of contracts providing for the fulfillment of obligations (payment) in non-monetary means, at least the following information is subject to disclosure:

| They do not provide information about the organizations that account for the bulk of the revenue received under contracts providing for the fulfillment of obligations (payment) in non-cash. Provides reasons why more detailed information is not disclosed. |

| Related Party Information | |

If, during the reporting period, the organization preparing the accounting reports carried out transactions with related parties, at least the following information is disclosed in the reporting for each related party:

Indicators that reflect similar relationships and transactions with related parties can be grouped. An exception is cases where separate disclosure is necessary to understand the impact of transactions with related parties on the accounting statements of the entity that makes it up. | They do not disclose information on each related party to the extent provided for by PBU 11/2008. Information to the extent provided for by PBU 11/2008 is disclosed for a group of related parties, and also indicates the reasons why more detailed information is not disclosed. |

| Construction contracts | |

In the financial statements, organizations disclose the following information for each contract not completed at the reporting date:

| They do not disclose information on each construction contract to the extent provided for by PBU 2/2008. Information to the extent provided for by PBU 2/2008 is disclosed for the totality of contracts not completed as of the reporting date, and also indicates the reasons why more detailed information is not disclosed. |

| Segment Information | |

The organization discloses the following information about buyers (customers), the sales revenue for which is at least 10% of the total revenue from sales to buyers (customers):

| They do not disclose information on each buyer (customer) to the extent provided for by PBU 12/2010. Provides reasons why more detailed information is not disclosed. |

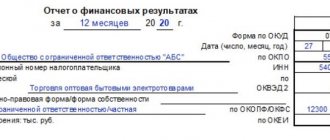

Profit and loss reporting

The financial statements of profit and loss that are published must necessarily contain the following indicators:

- gross profit;

- business expenses;

- administrative expenses;

- proceeds from sales (services, goods, works, etc.);

- cost of sales.

It is mandatory to publish information on the distribution of profits and coverage of losses (for the reporting year).

Publication of reporting occurs in thousands of rubles (or millions of rubles).