When making a calculation, the user is obliged to issue a cash receipt or a strict reporting form (SRF) on paper and (or) if the buyer (client) provides the user with a subscriber number or email address before the calculation, send a cash receipt or a strict reporting form in electronic form to the buyer (client) to the provided subscriber number or email address (if it is technically possible to transfer information to the buyer (client) in electronic form to the email address), unless otherwise established by the Federal Law of May 22, 2003 N 54-FZ “On the Application of Control - cash register equipment when making payments in the Russian Federation" (hereinafter referred to as Law No. 54-FZ) (clause 2 of Article 1.2 of Law No. 54-FZ).

Basic rules for storing strict reporting forms

The traditional way to produce BSO is to go to a printing house. The legislation of the Russian Federation requires the issuance of forms when using automated systems.

According to the law “On the use of cash register equipment,” all individual entrepreneurs and LLCs are required to record information about payments through a fiscal drive (including in the form of a cash receipt or BSO), transfer such information to the tax authority (including through a fiscal data operator) and subsequent storage of the fiscal drive. Other responsibilities in 2022, for example, for storing cash register receipts or BSO (including counterfoils) on paper, maintaining a BSO accounting log or rules for their destruction by analogy with documents confirming payment in hard-to-reach areas (clause 4 of article 2 Law No. 54-FZ, Decree of the Government of the Russian Federation of March 15, 2017 No. 296), in our opinion, the legislation of the Russian Federation does not establish the use of cash register equipment.

Until July 1, 2021, printing BSOs have the right to use only individual entrepreneurs without hired employees. After this date, all individual entrepreneurs are required to use online cash register, incl. for registration of BSO.

Let's consider the rules according to which Russian taxpayers were required to store BSO earlier, before the provisions on the mandatory use of cash registers came into force.

See also “What applies to strict reporting forms (requirements)”.

As for BSOs produced by printing methods, they should have been placed in safes or in special premises of the enterprise, where the safety of the forms was guaranteed. Every day, the place where the BSO was stored was subject to sealing or sealing (clause 16 of the Regulations).

The functions of ensuring the safety of strict reporting forms must be performed by a financially responsible person (hereinafter referred to as the MOL) - an employee of the organization, with whom the employer must sign an agreement on full financial responsibility (clause 14 of the Regulations).

The MOL begins to perform its functions from the moment the BSO becomes available to the organization (for example, from a printing house). His tasks at the time of receipt of the forms are to:

- check the number of forms, their series and numbers with the data specified in the accompanying documents;

- issue an act of acceptance of forms;

- enter information about the accepted forms into the book of strict reporting forms.

All three actions of the MOL must be carried out in the presence of a commission, which is created on the basis of an order from the head of the company (clause 15 of the Regulations).

As a BSO accounting book (or the basis for its creation), commercial companies can use a form corresponding to number 0504045 according to OKUD. For state and municipal organizations, its use is mandatory (Order of the Ministry of Finance of the Russian Federation No. 52n dated March 30, 2015).

The acceptance certificate (a little later we will look at the basis on which form it should be drawn up) must be signed by all members of the commission. It must also be approved by the supervisor. The book of records of strict reporting forms should be stitched and numbered. It must be signed by the head of the company, the chief accountant, and also sealed.

You can learn about filling out the book from the article “How to fill out the book of strict reporting forms.”

About the employee responsible for old BSOs

Before writing off the SSO, you need to select the employee responsible for the SSO. An agreement on full financial liability is concluded with him (clause 14, article 244 of the Labor Code of the Russian Federation). The employee will receive BSO, keep records in the book, be responsible for the safety of forms, fill them out or give them to employees who receive cash as payment for services.

An employee is required to accept purchased BSOs with a commission created by the manager. They must check the number of forms, series and numbers with the data in the invoice from the printing house where the old BSO was printed. Based on the results of acceptance, the commission draws up an act of acceptance of the forms in any form, and the responsible employee records their arrival in the BSO accounting book.

When transferring the BSO to the employee who will pay clients, the person responsible for the forms indicates in the accounting book the expense and balance of the forms. Damaged forms cannot be thrown away; they must be crossed out and attached to the BSO accounting book.

Storing forms using automated systems

The “innovative” scenario for manufacturing BSO - using automated systems (AS) - significantly simplifies the task of organizing the storage of forms for the company’s management. If the corresponding system meets the criteria contained in clause 11 of the Regulations (is protected from unauthorized access, identifies and records transactions with BSO for five years or more, stores data on the form in memory), then there is no need to carry out the above procedures, because:

- BSO from a third party is not accepted;

- copies of the BSO remain in the memory of the computer and other devices as part of the system;

- Suppliers of modern AS for organizing the circulation of BSO, as a rule, include in the software package solutions that allow you to maintain a book of records of strict reporting forms in electronic form.

At the same time, once printed using AS, but for one reason or another damaged, BSOs should, like those created by printing, be stored in the organization’s safes or in other safe places.

The functions of the MOL in the case of using an automated system are most often assigned to an accountant trained in working with the appropriate software, and less often to a system administrator managing the automated system.

Attention! In connection with the transition to online cash registers, the taxpayer is obliged from 07/01/2018, and in some situations from 07/01/2019, to form a BSO using automated systems for strict reporting forms capable of transmitting information about mutual settlements to the Federal Tax Service online. For more details, see the material “Law on online cash registers - how to apply BSO (nuances)” . The BSO is issued to the buyer on paper or sent by email or to the client’s phone number.

Tax authorities control the completeness of revenue accounting. Find out what rights they have when checking the cash balance in the cash register, the BSO machine and generated forms from the materials of ConsultantPlus experts by getting trial access. It's free.

Document retention periods

6.2. Primary documents, accounting registers, accounting reports and balance sheets, before transferring them to the archives of an enterprise or institution, must be stored in the accounting department in special rooms or locked cabinets under the responsibility of persons authorized by the chief accountant.

Strict reporting forms must be stored in safes, metal cabinets or special rooms to ensure their safety.

6.3. The procedure for storing primary and output documents on machine-readable media is determined in the relevant regulatory documents regulating the maintenance of accounting in the conditions of its mechanization (automation).

6.4. Manually processed primary documents of the current month related to a specific accounting register are completed in chronological order and accompanied by a certificate for the archive.

Cash orders, advance reports, bank statements with related documents must be collected in chronological order and bound.

Certain types of documents (work orders, shift reports) can be stored unbound, but filed in folders to avoid their loss or misuse.

6.5. The storage period for primary documents, accounting registers, accounting reports and balance sheets in the archives of an enterprise or institution is determined in accordance with the List of standard documentary materials generated in the activities of ministries and other institutions, organizations and enterprises, indicating the storage periods for materials, approved by the Main Archival Directorate under the Council of Ministers of the USSR .

6.6. The safety of primary documents, accounting registers, accounting reports and balance sheets, their execution and transfer to the archive is ensured by the chief accountant of the enterprise or institution.

The issuance of primary documents, accounting registers, accounting reports and balance sheets from the accounting department and from the archives of the enterprise or institution to employees of other structural divisions of the enterprise or institution is, as a rule, not allowed, and in some cases can only be done by order of the chief accountant.

6.7. Seizure of primary documents, accounting registers, accounting reports and balance sheets from enterprises and institutions can only be carried out by the bodies of inquiry, preliminary investigation, prosecutor's office and courts on the basis of decisions of these bodies in accordance with the current criminal procedural legislation of the USSR and union republics. The seizure is documented in a protocol, a copy of which is handed over against receipt to the relevant official of the enterprise or institution.

With the permission and in the presence of representatives of the authorities carrying out the seizure, the relevant officials of the enterprise or institution may make copies of the seized documents indicating the grounds and date of their seizure.

If unfinished volumes of documents are seized (not filed, not numbered, etc.), then with the permission and in the presence of representatives of the authorities making the seizure, the relevant officials of the enterprise or institution can complete these volumes (make an inventory, number the sheets, lace them, seal them , certify with your signature and seal).

6.8. In the event of loss or destruction of primary documents, the head of an enterprise or institution appoints by order a commission to investigate the causes of the loss or death.

Where necessary, representatives of investigative authorities, security and state fire supervision are invited to participate in the work of the commission.

The results of the commission’s work are documented in an act, which is approved by the head of the enterprise or institution. A copy of the act is sent to a higher organization.

Transfer of forms to the organization's employees

If the calculations in which the BSO is used are carried out not by the MOL, but by another employee of the company, then the transfer of the relevant forms to his disposal is carried out by the financially responsible person on the basis of a written application. Data on issued BSOs are entered by the MOL in the book of records of strict reporting forms.

Copies of the BSO issued to the organization's clients, or the counterfoils of the forms (depending on which specific form of the BSO is used) are transferred by the employees to the financially responsible person. Data about this is also recorded in the BSO accounting book. If any of the previously issued forms is damaged, it is crossed out and then attached to the accounting book.

How long should BSO forms be kept?

Hello, Ekaterina!

One of the important conditions for using BSO is to ensure their safety and maintain correct records.

Depending on the manufacturing method, forms need to be taken into account differently.

Forms produced in the printing house must be accepted by the employee responsible for their storage, recording and issuance (or the manager himself or the individual entrepreneur).

A liability agreement must be concluded with this employee.

When accepting the BSO, it is necessary to check the compliance of the actual number of forms, as well as their series and numbers with the data specified in the accompanying documents from the printing house. After this, you need to draw up a BSO acceptance certificate.

The act must be signed by the head of the organization (IP) and members of the commission for accepting strict reporting forms. The composition of the commission is approved by the relevant order.

Forms must be stored in metal cabinets, safes or in specially equipped rooms under conditions that prevent their damage and theft.

The forms are kept in the BSO accounting book. There is no approved form for the journal, so you have the right to develop your own version. The sheets of the book must be numbered, laced and signed by the manager and the chief accountant (or individual entrepreneur) and sealed.

At the time of receiving money from the client, the authorized employee fills out the BSO. He must hand over the main part of the form to the client, and keep the tear-off spine (or a copy) for himself. A cash receipt order is issued for the amount of money received (the counterfoil or copy of the BSO will serve as a document confirming the receipt of money).

The counterfoils (copies) of the forms must be packed in bags, sealed and stored for 5 years. At the end of this period, the documents are disposed of and a report on the write-off of the BSO is drawn up (using the same report, damaged and defective forms are disposed of).

Monitoring compliance with the rules for using strict reporting forms is carried out by employees of the Federal Tax Service.

In the event of an inspection, you will need to provide the inspectors with the BSO accounting book for inspection.

For identifying violations related to the use of strict reporting forms, as well as for failure to issue BSO to clients, a fine is provided under Article 14.5 of the Code of Administrative Offenses of the Russian Federation for individual entrepreneurs and officials of the organization (manager) - from 3,000 to 4,000 rubles;

Also, for non-compliance with the procedure and terms of storage of strict reporting forms, a fine of 2,000 to 3,000 rubles is provided for individual entrepreneurs and officials of organizations (Article 15.11 of the Code of Administrative Offenses of the Russian Federation).

In addition, for the absence of a BSO (as a primary document), liability is provided under Article 120 of the Tax Code of the Russian Federation.

Do GMEC protocols have legal force?

Some provisions of the legislation regulating the circulation of BSO are contained in the minutes of the meeting of the State Interdepartmental Expert Commission (GMEC) No. 4/63-2001 dated June 29, 2001. Do they have legal force that applies to all Russian organizations?

Despite the fact that GMEC ceased to exist on 08/09/2004, its decisions, which were made during the period when this institution exercised its powers, are generally binding (letter of the Federal Tax Service of the Russian Federation No. ED-18-2/947 dated 06/17/2014).

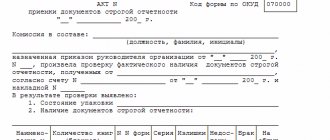

So, with regard to the form of the BSO acceptance certificate, you should use the form that corresponds to number 070000 according to OKUD. The order to use this form includes clause 18 of the GMEC protocol No. 4/63-2001.

Similarly, other provisions of the GMEC Protocol No. 4/63-2001 retain legal force. In particular, those that regulate BSO accounting.

Accounting for strict reporting forms

BSO turnover is recorded in off-balance sheet account 006, which is called “Strict Reporting Forms”. BSO accounting is carried out through entries reflecting the amount of costs for the production of forms (clause 22 of the minutes of the GMEC meeting No. 4/63-2001). As a rule, these are the postings:

- Dt account 26 “General business expenses”;

- Kt account 60 “Settlements with suppliers and contractors.”

In some cases, BSO accounting involves the creation of subaccounts for account 006. This is possible if the forms capitalized by the accounting department are subsequently issued to other employees who actually manage the BSO (we examined a similar scenario above). In this case, subaccount 006-1 “BSO in accounting”, as well as subaccount 006-2 “BSO from executors” can be formed.

How to correctly write off BSO in accounting and what documents to prepare? The answer to this question was given by 2nd class State Civil Service Advisor I. O. Gorchilina. Get free trial access to the ConsultantPlus system and get acquainted with the official’s point of view.

Criteria for correct numbering of strict reporting forms

An important criterion characterizing the accounting and storage of BSO is the correct numbering of the relevant forms.

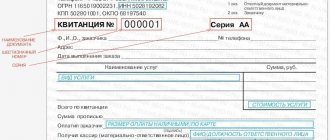

The main requirement for a BSO is the presence of a unique 6-digit serial number and a series consisting of 2 letters. At the level of federal legislation, the noted criteria are not fixed, but they are regularly found in departmental legal acts regulating the production of BSO (for example, in the letter of the Ministry of Culture of the Russian Federation No. 2344-01-39/03-E4 dated April 13, 2009). These provisions can be applied by subjects of legal relations in other industries on the principle of legal analogy.

The relevant details of the forms - series, number - will need to be recorded in the marked forms (BSO acceptance certificate, BSO accounting book).

As we noted at the beginning of the article, BSOs must be produced using the printing method or using automated systems. In the first case, the organization, as a rule, orders the production of forms from a third-party contractor who has the necessary printing equipment. If such an order is being made for the first time, then you can start producing BSO with series AA and number 000001. But in subsequent orders, printed forms must begin with the number following the one that was present on the last BSO of the previous edition.

The use of automated systems for issuing forms assumes that the correct numbering of the BSO (in correlation with entering the necessary information into the system registers) will be carried out automatically by the corresponding software.

Inventory and write-off of BSO

The tasks that the process of storing strict reporting forms includes includes inventory. This procedure involves reconciling existing copies of the BSO, as well as their counterfoils, with the data contained in the book of strict reporting forms. The inventory of BSO must be carried out simultaneously with a similar procedure established in relation to cash at the cash desk (clause 17 of the Regulations).

After five years of storage of forms (including damaged or incomplete ones) in the organization, it is necessary to write off the BSO. This procedure is carried out by drawing up a separate act (you can use the form corresponding to OKUD number 0504816, and for state and municipal structures its use is mandatory). This document is drawn up with the participation of a commission created on the basis of an order from the head of the company.

For more information about the act, see “Act on the write-off of strict reporting forms - sample.”

The structure of modern automated systems, as a rule, contains solutions that make it possible to issue the necessary acts on inventory and write-off of BSO in electronic form. Also, the corresponding systems provide algorithms for excluding decommissioned digital BSOs from hardware registers.

For more information about other types of inventory provided for by the legislation of the Russian Federation, read the article “How to conduct an inventory before annual reporting.”

Write-off of BSO

The government, in the Regulations on Cash Payments, indicated the possibility of destroying damaged or incomplete BSO forms.

Required condition for writing off BSO:

- Storage of documents for at least 5 years.

- Participation in the procedure for the destruction of BSO members of the commission.

- Drawing up an act on the write-off of damaged strict reporting forms.

When drawing up the described act of writing off BSO, you need to use the official sample of the act of writing off BSO. Commercial organizations and entrepreneurs can use the official sample or approve their own BSO write-off form. The correct act must indicate:

- company name, address, tax identification number, telephone number, full name of management,

- an indication of the financially responsible employee, members of the commission and details of the relevant order,

- a list of strict reporting forms to be destroyed,

- signatures of all persons involved,

- date of manufacture of the form.

Results

BSO are equivalent to cash receipts and must be generated using automated systems capable of transmitting information to the Federal Tax Service online. In this case, the forms are also recorded using such systems. Some taxpayers are legally allowed to switch to using online devices from 07/01/2019, and individual entrepreneurs without employees in some cases - from 07/01/2021. Before this, they have the right to use printed forms. The purchase of such forms is carried out on cost accounting accounts (25, 26, 44 - depending on the department), and subsequent accounting is carried out using balance sheet account 006.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.