An inventory list in the INV-16 form is used when checking securities and strict reporting documents. They, just like other objects and assets of the company, must be subject to inventory. The form is filled out by a specially created commission based on the results of the procedure. It displays data on the actual availability of securities and BSO in the organization and compares it with accounting information. We’ll figure out how to fill out such a form in the article.

- Form and sample

- Online viewing

- Free download

- Safely

FILES

Legislative regulation

The inventory procedure is regulated by a document such as the Guidelines for Inventory of Property and Financial Obligations. They are an annex to the Order of the Ministry of Finance of the Russian Federation No. 49 of June 13, 1995.

As for the use of the INV-16 form, the law does not indicate anywhere that it is mandatory. On the contrary, Information of the Ministry of Finance of Russia No. PZ-10/2012 indicates that since 2013, all unified forms have become only recommended for use. Companies have the right to develop their own forms, not forgetting that a number of details must be on the document.

Important! The decision on which forms to use in work must be recorded in the accounting policies of the company.

Many business entities use unified forms out of habit, as well as being guided by their convenience and the absence of complaints from officials from inspection departments. INV-16 is no exception.

Comment on the rating

Thank you, your rating has been taken into account. You can also leave a comment on your rating.

Is the sample document useful?

If the document “Form No. inv-16 inventory of valuables and forms of strict reporting documents” was useful for you, we ask you to leave a review about it.

Remember just 2 words:

Contract-Lawyer

And add Contract-Yurist.Ru to your bookmarks (Ctrl+D).

You will still need it!

Briefly about inventory

Procedure required:

- once a year before preparing annual reports;

- when there is a change of the financially responsible person;

- after cases of theft of company property;

- after natural disasters, man-made accidents, etc.;

- during the company reorganization procedure.

The inventory algorithm is standard:

- The manager issues an order in the INV-22 form to conduct an inventory. It should indicate the reasons for the procedure, timing, and other details.

- The commission carries out the inventory within the time limits specified in the order. Based on the results, he fills out an inventory list and submits it to the accounting department.

- After checking by an accountant, the paper is sent to management.

- Next, the manager decides what to do with the surplus or shortage.

- The accountant, based on the decision of the manager, reflects the necessary transactions in accounting.

Attention! The commission is created on an ongoing basis. The leader decides who will be part of it and issues an order. As a rule, employees of the directorate, accounting, legal department, and heads of structural divisions are appointed members of the commission. Financially responsible persons are not included in the composition, but are required to attend the inventory.

Why is a securities inventory necessary?

Organizations that invest in various market instruments that generate income need to periodically check the actual cost of securities, as well as the correctness of their completion. Strict reporting forms (SRF) are also subject to inventory, if they are used at the enterprise.

The objectives of the audit may include the following:

- identifying suspected discrepancies between actual data and accounting information;

- change of financially responsible persons.

The procedure for conducting an inventory of financial investments is similar to the algorithm for other asset checks. Includes the following steps:

- Formation of an inventory commission, determination of its participants. Establishing the timing of the inventory and the reasons for justification.

- Checking the existence of securities, identifying possible inaccuracies when filling them out. Comparison of the information received with current accounting data.

- Documentation of inventory results. Drawing up an inventory of INV 16 in accordance with the results of the work performed.

General information about the INV-16 form

The form was approved by the Post. Goskomstat of Russia No. 88 dated August 18, 1998.

The form must be filled out by members of the commission and signed by the following persons:

- Members of the commission and its chairman. Their signatures indicate that all data was entered correctly. All employees included in the commission must sign the document, otherwise the document will not be considered valid.

- Financially responsible employee (there may be several of them). The signature is placed as a sign that the employee was present during the inventory, confirms the correctness of the information entered and the absence of claims against the members of the commission.

- Accountant. This employee confirms that he has checked all the information on the form.

- Head of the organization. He puts his signature last. With it, he confirms his decision on how to deal with the identified surpluses or shortages discovered as a result of the inventory.

How BSO is taken into account: features of the procedure

Strict reporting forms include various settlement documents that replace, in their purpose, cash (fiscal) checks generated through cash registers.

These may be payment receipts, tickets, identification forms, subscription forms, certificates, certificates, invitation papers, receipt/check books and other forms of this kind.

Business entities have the right to develop their own BSO forms or use their standard templates.

Such forms must meet the following requirements:

- availability of required details;

- required level of protection;

- six-digit machine readable numbering;

- typographic method of printing.

The consumption of strict reporting forms printed on paper is carefully controlled by responsible employees by name (standard varieties), as well as series/numbers.

BSO are accounted for in accounting account 006, which is off-balance sheet. Such forms are reflected according to their conditional valuation.

Records should be kept for individual types and places of safekeeping of strict reporting forms.

BSO are promptly registered in a special accounting journal, subject to lacing and numbering. Such a register must be certified by the signatures of the manager and chief accountant of the business entity.

If an organization/entrepreneur uses a seal (stamp), the corresponding imprint is affixed. There is a recommended form for such a journal. A business entity can develop and apply its own template. BSO is stored in safe conditions.

When is the audit carried out?

Inventory of existing BSO is an important aspect of their operation and accounting.

The audit is carried out by responsible employees in the following typical situations:

- the employees responsible for the safety of strict reporting forms have changed;

- the organization is facing liquidation/reorganization;

- natural disasters or other emergency situations occurred, as a result of which the forms were damaged (destroyed);

- facts of theft and deliberate destruction of BSO have been established;

- regulated inventory of BSO, carried out before drawing up the final reports for the year.

Order of conduct

To carry out an inventory of strict reporting forms, you must follow the procedure provided for by special guidelines drawn up and approved by the Ministry of Finance of the Russian Federation (Order No. 49 of June 13, 1995).

We are talking about inventory rules regulated by this official department for the audit of the assets and financial liabilities of a business entity.

The procedure for conducting a BSO inventory provides for the sequential implementation of the following stages:

- Management issues a special administrative act (order) to conduct the next BSO inspection (the reason and timing are specified). The same order regulates the formation of the inventory commission (its composition, powers).

- The commission recalculates the existing strict reporting forms, taking into account their numbering. The actual quantity and species composition of BSO are verified with accounting data. The inventory (audit) list is filled out by making the appropriate entries.

- If deviations of real information from accounting information are detected, a comparison (reconciliation) statement is drawn up.

- If it is possible to identify the entities responsible for the shortage/surplus of BSO, an appropriate penalty is imposed. This decision must be formalized in writing by the management of the business entity.

The audit committee must consist of at least 3 people. The specific composition of the commission is approved by the above-mentioned management order.

It may include not only full-time employees of the business entity (employees of the administration, accounting department, internal audit), but also independent experts from external structures.

The legitimacy of the results of the audit is achieved and approved if all members of the commission, the composition of which was appointed by the head, as well as the subjects responsible for the safety and security of the BSO, were present at this audit.

All these persons - commission members and responsible entities - must sign in the drawn up inventory act. This confirms the required quorum.

It should also be noted that this check is performed for each individual entity that is personally responsible for certain strict reporting forms.

A specific list of documents to be checked is given in the inventory documentation (inventory, act). One column indicates accounting information, the other indicates actual availability.

BSOs are calculated and verified with accounting information for each individual variety. Their starting/ending numbers are taken into account.

In addition, each storage location is taken into account.

Inventory allows you to successfully solve the following problems:

- check the accuracy of current accounting information;

- identify errors made in accounting;

- find and capitalize unaccounted for forms;

- control the safety and security of documents subject to strict records.

What documents are prepared?

Documentation of the BSO inventory is of great importance for the subsequent legalization of its results. The organization can record the results of the audit performed using independently developed document forms.

However, he has a convenient alternative - to use standard templates for this, approved back in 1998 by the normative act of the State Statistics Committee (Resolution No. 88).

As a rule, we are talking about the preparation of the following standard papers:

- order regulating the inventory (reason, timing, composition of the commission);

- inventory list for BSO;

- act of inventory of available documents;

- statement of comparison (reconciliation) of the results of the performed check (filled out if inconsistencies are detected between the fact and the accounting).

If a company uses its own template forms, it should make sure that these documents contain a number of mandatory details, the composition of which is regulated by 402-FZ of December 6, 2011 (accounting law).

In addition, independently developed templates must be approved by the manager. The results of the audit are documented in standard documentation, usually drawn up in 2-3 copies.

How to prepare an inventory list?

The BSO inventory list must contain the following mandatory information:

- general information about the strict reporting document being checked (name, type, category);

- code of the document being checked according to the OKEI classifier;

- the unit of measurement used;

- series/form number (form numbers);

- nominal (conditional) value of a document unit;

- the actual quantity and total cost of all BSOs of this type;

- accounting quantity and total cost of all BSO of this type;

- audit results (information about missing/excess forms - series, numbers, unit cost, total quantity, total cost).

forms INV-16 and 0504086

Download the inventory list IVN-16 for strict reporting forms and valuable documents – excel.

BSO comparative inventory form 050486 – excel.

Filling out INV-16

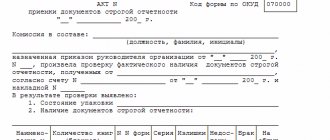

Form INV-16 has 4 pages. They all need to be filled out. You can enter data on a computer or by hand. When choosing the second method, there should be no blots.

Page 1

The document begins with a header. It must contain the following information:

- name of the economic entity and structural unit;

- OKPO and OKVED codes;

- basis for the procedure: here you need to select the type of document;

- details of this document: number and date of preparation;

- timing of the procedure;

- number and date of compilation of the current inventory list.

Then follows a receipt, where the financially responsible person confirms that all the necessary papers under his control have been handed over to the members of the commission.

At the end of the page they put the date of the inventory.

Page 2

This is where the table starts. Members of the commission enter information about inventory items into it:

- Column 1. Record number in order.

- Columns 2-4. The name of the inventory object (BSO or security), its number and code.

- Columns 5-6. The name of the unit of measurement and its OKEI code.

- Columns 7-12. Data on the actual availability of documents is indicated here. Enter numbers, series, face value data, quantity and total amount.

At the end of the table, the columns with quantity and amount are summed up.

Page 3

The table continues on this page:

- Columns 13-18. Here the accounting data for the documents is indicated. Record numbers, series, face value, quantity and total amount.

- Columns 19-26. These columns reflect the inventory results: identified surpluses and shortages. They also indicate the numbers, quantity, and amount.

At the end of the table, similar to the previous page, sum up the quantities and amounts.

Page 4

At the beginning of the page, the inventory is summarized (data must be entered in words): the number of serial numbers, units of documents, the total amount.

Next, the members of the commission and its chairman sign. Then follows a receipt stating that all inventory items were checked in the presence of the financially responsible person and he has no claims against the commission. And the financially responsible employee puts his signature and date. Then the accountant who checked the calculations signs. Next, the financially responsible employee indicates the reasons for the identified surpluses and shortages. And he puts his signature again.

At the end of the page (and document), the head of the company indicates his decision regarding the identified inconsistencies and signs and dates it.

For your information! Based on this inventory, the accountant must adjust the accounting data. If previously unaccounted for securities were discovered, then use the posting DT 58/KD 91. If shortages or damage are identified - DT 94/KD 58 (reduces the actual number of securities). If it comes to BSO, then to correct it, the accountant must use off-balance sheet account 006. Surpluses - according to DT, shortages - according to CD.

Leave a comment on the document

Do you think the document is incorrect? Leave a comment and we will correct the shortcomings. Without a comment, the rating will not be taken into account!

Thank you, your rating has been taken into account. The quality of documents will increase from your activity.

| Here you can leave a comment on the document “Form No. inv-16 inventory of valuables and forms of strict reporting documents”, as well as ask questions associated with it. If you would like to leave a comment with a rating , then you need to rate the document at the top of the page Reply for |