What is BSO

Strict reporting forms (SRF) include a variety of documents on the provision of various services to the population. These include railway, bus and air tickets, various receipts, vouchers, repair orders, subscriptions, coupons and the like. Article 11 of Federal Law No. 54-FZ of May 22, 2003 “On the use of cash register equipment when making cash payments and (or) payments using payment cards” states what a strict reporting form is formally:

BSO is a primary accounting document, equivalent to a cash receipt, generated in electronic form and (or) printed using an automated system for BSO at the time of payment between the user and the client for services rendered, containing information about the calculation, confirming the fact of its implementation and meeting the requirements of the law Russian Federation on the use of CCP.

But the use of strict reporting forms is strictly regulated and limited. They are issued not only when paying in cash or with a plastic bank card, if it is impossible to use an online cash register, but also by duplicating it. Strict reporting lies in the order of production of such forms and the requirements for their execution and storage.

Who has the right to use strict reporting forms

The provisions of Article 7 of Federal Law 290-FZ of 07/03/2016 determine that it is no longer possible to use printed forms of receipts or tickets instead of cash register receipts (the final ban came into force on 07/01/2019). The corresponding changes were adopted on behalf of the President of Russia. And the Ministry of Finance recalled this in its letter dated May 22, 2019 No. 03-07-07/3670. Individual entrepreneurs not related to trade and public catering, who do not have employees, were allowed to work without using online cash registers until 07/01/2021. Until this date, BSO for individual entrepreneurs is allowed to be printed using a printing method, without the use of cash registers.

A sample version of a receipt for the provision of services by an entrepreneur looks like this:

All other categories of business are required to use exclusively cash registers with the ability to generate and transmit checks to the fiscal authorities in electronic form. If they fall into the exceptions, they will have to use new BSO forms, the requirements for which have changed significantly.

Receipt cash order (form KO-1)

Home / Cash discipline

| Table of contents: 1. Procedure and methods for registering PQS 2. Instructions for filling out a receipt order 3. Sample of filling out RKO 4. Fines for the absence and storage periods of PKO | PKO in excel or word format Download samples of PKO: Founder’s contribution, Return of account, Compensation for damage, Money from the bank for salary, LLC loan from the founder, According to the contract from the legal entity. persons, Retail revenue from individual entrepreneurs, LLC trading revenue |

A receipt order is a unified form that is filled out upon receipt of cash at the cash desk of an organization (IP).

The company is obliged to issue a PKO in the following cases:

- Contribution of funds to the authorized capital;

- Return of unused amounts of accountable funds;

- Compensation for damage by an employee;

- Sale of property owned by the company;

- Return or receipt of borrowed funds;

- Receipt of money from the company account;

- Receipt of cash revenue from business activities (at the end of the working day, one PQR is filled in for the entire amount of revenue).

Individual entrepreneurs are not required to draw up PKO, as well as other cash discipline forms (for example: cash register, cash book, etc.), but can use such documents on their own initiative for the purpose of accounting and control over the movement and expenditure of cash.

Procedure and methods of registration of PKO

The unified order form (No. KO-1) was approved by Resolution of the State Statistics Committee of Russia dated August 18, 1998 No. 88.

The document consists of two parts: a cash receipt order and a receipt for the PKO.

The order is issued in one copy. Numbering is carried out in order in chronological sequence, the reference date is January 1 of each new year.

The person whose responsibilities include filling out the receipt order may be:

- an employee of the organization (cashier, accountant, etc.), appointed by order of the head of the company;

- Chief Accountant;

- manager (if the company does not have a chief accountant or accountant on staff).

The PKO is signed by: the chief accountant (accountant or director) and the cashier.

If the head of the organization (IP) single-handedly carries out cash transactions and draws up primary documentation, only the signature of the head (IP) is placed on the PKO.

The form is completed:

1) Manually.

2) On a computer with subsequent printing:

- in a text or spreadsheet editor;

- using specialized programs and online services.

3) In electronic form. With this method of document management, cash forms must be certified by a qualified electronic signature.

Corrections and blots when filling out the PQS are strictly not allowed!

The receipt for the order is filled out simultaneously with the PKO, signed and sealed.

To affix a seal impression the following can be used:

1) The main round seal of the organization.

It should be noted that since the entry into force of the law dated 04/06/2015 No. 82-FZ, organizations have the right to refuse to use a round seal.

2) Simple (auxiliary) seals and stamps kept by company employees responsible for their safety and use.

The seal impression should be located entirely on the receipt and not go onto the receipt order itself.

The cashier who receives the completed form from the accounting department is obliged to:

- check all order data;

- check the document for erasures and corrections;

- verify the authenticity of the signature of the chief accountant (or other responsible person);

- check the availability of the specified applications.

If all the rules are followed, the cashier accepts the money. The documents attached to the order should be stamped or handwritten: “Received” (“Paid”) with the date.

The executed PKO remains in the organization and is filed with the cashier’s report (the second copy of the cash book sheet), and the receipt is handed over to the person who deposited the cash.

Information about the order is entered into the order registration journal (No. KO-3). A record of received funds is reflected in the company's cash book.

Instructions: how to fill out a cash receipt order

The unified form is filled out as follows:

- In the “Organization” field, the full name of the company is indicated in accordance with the constituent documents.

- In the “according to OKPO” window, the corresponding code is indicated according to the Rosstat notification.

- The line “Structural division” is filled in if the company has divisions and only in situations where money is handed over by an employee of the representative office.

- Next, fill in the serial number of the form and the current date.

- The “Debit” and “Credit” cells indicate accounting account numbers or codes (if the company uses coding).

Individual entrepreneurs do not fill out these cells.

Transactions on the receipt of cash into the organization are reflected in the debit of account 50 (you should also indicate a subaccount in accordance with the company’s working chart of accounts).

For a loan, a corresponding account is recorded - the source of cash inflow, for example:

- 51 (52) – receipt of cash from the company’s bank account;

- 60 – the supplier returned the advance;

- 62 (76) – money received from customers and buyers;

- 66 (67) – borrowed funds received;

- 73-1 (2) – the employee compensated for material damage;

- 75-1 – the owner contributed a share to the authorized capital;

- 90-1 – revenue was received from the sale of products (services, works).

- “Structural unit code” is filled in if the unit for which the order is issued has a code.

- “Analytical accounting code” – enter the analytics code of the corresponding account (if such codes are provided in the organization).

- The amount of cash received in numerical terms is recorded in the “Amount” cell.

- The “Purpose Code” cell is filled in if the company uses a coding system.

- Full name is entered in the “Accepted from” line. company employee. When making payments between counterparties, the company name and full name are indicated. the employee who handed over the money, using the preposition “through”. For example: Meridian LLC through K.M. Ivanov.

- The content of the operation is entered in the “Base” line.

- In the “Amount” line, the amount of funds received is deciphered in words, with kopecks indicated in numbers.

- The “Including” line records the VAT rate and amount. If the transaction is not subject to VAT, it is indicated: “Without VAT”.

- The “Attachment” field lists the names, numbers and dates of the attached documents.

When filling out printed forms by hand, you should put dashes in the empty cells. Also, after entering the amount in words, be sure to cross out the empty space on the line to avoid falsification of the document.

The PKO receipt contains information identical to the data on the receipt order.

Sample of filling out a cash receipt order 2022

Contribution of the founder to the authorized capital

Return of accountable funds

Compensation for damage by the guilty party

Receiving money from the bank to pay salaries

LLC loan from the founder

Payment under an agreement from a legal entity

Retail revenue from individual entrepreneurs

LLC trading revenue

Penalties for the absence of PKO and storage periods for the form

For the lack of primary documents (gross violation of accounting rules), inspectors may fine the company under Art. 120 Tax Code of the Russian Federation:

- For 10,000 – 30,000 rubles;

- Or 20% of the unpaid amount if the tax base is understated, but not less than 40,000 rubles.

There are no sanctions for incorrect execution of the PKO, but a form filled out with errors can be equated to the absence of a document.

The absence of a PKO receipt from the counterparty may lead to the inspectors’ refusal to recognize expenses taken into account when calculating income tax (single tax under the simplified tax system). In such a situation, the counterparty will incur additional costs for paying taxes, fines and penalties.

The organization is obliged to store primary documentation, which includes the cash receipt order, for 5 years after the end of the reporting year.

Read in more detail: Form KO-1

Did you like the article? Share on social media networks:

- Related Posts

- Cash payment limit in 2022

- Sample of filling out form T-51

- Cash limit for LLCs and individual entrepreneurs in 2022

- Cash book (form KO-4)

- Order on accountable persons

- Sample of filling out form T-53

- Advance report (form AO-1)

- Payroll (form T-53)

Discussion: there is 1 comment

- Victor:

01/03/2020 at 08:31The PKO is filled out as follows: - organization (above) - one name (not related to the operation) - seal - another organization - There is no order itself - The receipt is filled out after the seal has been affixed (the handwriting of the second person) To whom should I appeal about the nullity of this document?

Answer

Leave a comment Cancel reply

Strict reporting form: sample and required details

Legally, BSOs are equivalent in meaning to a cash receipt with all the ensuing consequences. This means that if the client to whom the service was provided did not receive such a form, the organization or individual entrepreneur is liable for failure to provide a cash receipt. BSO, like cash receipts, are in electronic format and are sent to the client’s mobile network number or email address.

Organizations and individual entrepreneurs have the right to independently decide which forms of SSO to use. But ordering forms from a printing house is prohibited. They are generated only by a special automated system, which largely replicates cash register equipment. All requirements imposed by law on cash registers apply to it, namely: such systems must be registered with the tax authorities and comply with the requirements for their use.

IMPORTANT!

Currently, BSO is formed only with the help of cash register systems (including using an automated system for BSO), with the exception of individual entrepreneurs without employees until 07/01/2021.

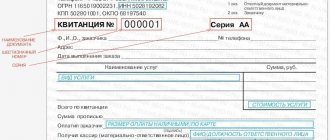

A sample of a new automated BSO looks like this:

The installed automated system can not only generate a form designed specifically for the provision of this service, but also transmit fiscal documents to the Federal Tax Service through a data operator, store information about them and print them on paper, that is, perform all the operations that online cash registers do. An automated system cannot replace cash registers, since its use is permitted only for payments for services, but not for goods sold. But some CCP models are universal: their manufacturers inform about this before inclusion in the register. Moreover, now in the application for registering a cash register with the tax authority, its owner must indicate that a specific unit is intended exclusively for payments for services and the formation of BSO.

Article 4.7 of Federal Law No. 54-FZ approved a strict reporting form for individual entrepreneurs and organizations. It contains 20 mandatory details. They are identical to the mandatory details of a cash receipt, which are regulated by the same article:

- Title of the document;

- series of the form and its six-digit number;

- name of the legal entity or surname, first name, patronymic of the individual entrepreneur;

- organization address;

- TIN;

- type of service provided;

- service cost;

- the amount of payment made in cash or by bank card;

- date of payment;

- FULL NAME. and the position of the person who accepted the money and issued the document.

The BSO, which must be issued by bank payment agents, contains additional details, as provided for in paragraphs 3 and 4 of the above article. One of the additional details that, by order of the government of the Russian Federation, every strict reporting form must have is a product nomenclature code and a special two-dimensional QR code. The latter, in fact, contains all the other data specified in the document:

- date of operation;

- time of settlement with the client;

- BSO serial number;

- established sign of calculation;

- payment amount;

- fiscal document number;

- serial number of the fiscal drive.

All strict reporting forms contain such a barcode; it is located in a specially designated place. Even if the paper itself on which the forms are printed has an original design, the document cannot be printed in a printing house and filled out manually or on a regular printer. If an organization or entrepreneur needs this, a separate cash register receipt or an automatically generated BSO is attached to such a ticket or receipt.

IMPORTANT!

Businessmen have the right to add additional details to the document if the specifics of their activity require it.

Legislators made the transition to compliance with all new requirements for these settlement documents smooth. Some of them, for example, the names and number of services provided, will remain optional when carrying out the types of activities listed in paragraph 2 of Article 346.26 of the Tax Code of the Russian Federation by entrepreneurs and legal entities using preferential tax systems (STS, PSN and Unified National Economic Tax) until 12/31/2021. But such a relaxation does not apply to businessmen who trade in excisable goods and at the same time provide services to the population; they will have to indicate the entire range.

Form of receipt for payment of services

Unlike the invoice form, you cannot print the BSO yourself on a printer. You can purchase receipts for payment for services at a printing house that uses special automated equipment. An entrepreneur has the right to independently develop a form in any text editor, but he can order printing of the document only from a specialized company.

See also: How to write a letter of guarantee for payment - sample

Features of the new BSO

The issuance of forms confirming the fact of payment for services rendered is now allowed not only to the population and individual entrepreneurs, but also to legal entities. Whereas in the previous version of the law on cash register equipment, the scope of BSO recipients was limited only to individuals. Now the legislation does not provide for such restrictions. When making payments using electronic means of payment, receipts are issued. Tax authorities include not only plastic payment cards, but also electronic wallets used for payments on the Internet. The electronic form of the receipt is legally equal to its printed counterpart.

Since a strict reporting form cannot be used instead of a cash register receipt, when paying for goods it is necessary to issue a receipt of the established form, generated on a cash register. But the law does not prohibit the opposite situation. If the same businessman simultaneously trades and provides services to the public, he has the right not to establish a separate system and issue cash receipts to all clients in the manner prescribed by law. This is only prohibited when working on the Internet; in this case, you will have to install a separate cash register and automated system.