Who is entitled to a deduction and in what amount?

The child deduction is a standard deduction, and paragraph 1 of Article 218 of the Tax Code of the Russian Federation is devoted to it.

The “children’s” deduction is due to the following persons who support the child: a parent (including an adopted one), his or her spouse, an adoptive parent, a guardian and a trustee. Calculate salary and personal income tax with standard deductions in the web service

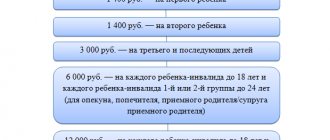

The “children’s” deduction is provided for all children, without exception, under the age of 18, as well as for full-time students, graduate students, residents, interns, students and cadets under the age of 24. The amount of the deduction depends on the type of child in the family. For the first and second child, the deduction amount is 1,400 rubles each. per month. For the third and each subsequent child - 3,000 rubles. per month. When establishing the priority, it is necessary to take into account children from previous marriages, if they live in a new family, or alimony is transferred to them (see “When providing a “children’s” deduction, the total number of children, including the children of the spouse from the first marriage”). Let us add that the indicated deduction values are the same for everyone who is entitled to them. Comments on some “atypical” situations are given in Table 1.

Table 1

Explanations from officials on “children’s” deductions in unusual situations

| Situation | Comment from the Russian Ministry of Finance |

| The father has a child from his first marriage who is over 18 years old and lives with his mother | When determining the total number of children, a child from his first marriage is taken into account by the father, but not taken into account by his new wife (letter dated January 21, 2016 No. 03-04-05/1999) |

| Husband pays child support from first marriage | The current spouse has the right to receive a deduction for this child (letter dated 03/18/15 No. 03-04-05/14392) |

| The deduction for the first and second child is not provided due to their age | The deduction for the third child is 3,000 rubles. (letter dated 04/17/14 No. 03-04-05/17619) |

| A full-time student under the age of 24 got married | The parent loses the right to deduction (letter dated 03/31/14 No. 03-04-06/14217) |

| The child is registered at an address different from the parents' address | The right to deduction remains (letter dated 05/11/12 No. 03-04-05/8-629) |

| Twins were born into the family | Their order can be determined in any order (letter dated 12/21/11 No. 03-04-05/8-1075) |

| The wife's children from her first marriage live with their mother and her new husband, who did not adopt them | The current husband has the right to receive a deduction for these children (letter dated 09/05/12 No. 03-04-05/8-1064) |

In addition, a separate deduction is provided for a disabled child. It is provided for children with disabilities under the age of 18. It is also provided for full-time students, graduate students, residents, interns and students under the age of 24, if they are disabled people of group I or II. The size of the deduction depends on who receives it. If this is a parent, his spouse, or an adoptive parent, then the deduction is 12,000 rubles. per month for one child. For an adoptive parent, his or her spouse, caregiver and guardian, the deduction is RUB 6,000. per month.

Is it necessary to give two deductions at once for a disabled child?

From the text of Article 218 of the Tax Code of the Russian Federation, we can conclude that a disabled child is entitled to two “children’s” deductions at once. The first - as for any other child (1,400 rubles or 3,000 rubles, depending on the order of birth), the second - as for a disabled person (6,000 rubles or 12,000 rubles, depending on who receives). However, there is no direct answer to the question of whether it is necessary to give both deductions at the same time.

Specialists from the Ministry of Finance of Russia agree with this position (letter dated November 7, 2019 No. 03-04-05/85821; see “One of the children in the family is disabled: how to calculate the standard deduction for personal income tax?”).

The judges are of the same opinion. The review released by the Presidium of the Supreme Court of the Russian Federation on October 21, 2015 states that the amount of deductions for a disabled child is being added (read more about this in the article “The Supreme Court of the Russian Federation summarized the practice on disputes about personal income tax: what court conclusions should accountants and employees know about” ). This means that if a child with a disability is, for example, the second in the family, then his parent has the right to receive a monthly deduction in the amount of 13,400 rubles (1,400 + 12,000).

What standard tax deductions are established by Art. 218 of the Tax Code of the Russian Federation for 2022

The procedure for providing standard tax deductions is regulated by Art.

218 Tax Code of the Russian Federation. I would like to immediately note that the main difference between standard tax deductions and other personal income tax deductions is not the presence of specific expenses on the part of the taxpayer, but his direct membership in certain groups of persons. So, what are the standard tax deductions today?

- For certain categories of citizens, standard tax deductions can be 3,000 or 500 rubles.

- All citizens with children can be provided with a so-called child deduction.

For what period should the “children’s” deduction be provided?

The Tax Code clearly states that “children’s” deductions are provided up to the month in which the employee’s income, calculated cumulatively from the beginning of the year, exceeded 350,000 rubles. Please note that income does not include dividends, as well as payments exempt from personal income tax (letter of the Ministry of Finance of Russia dated March 21, 2013 No. 03-04-06/8872, see “When determining the maximum amount of income in respect of which a child deduction is granted , payments exempt from personal income tax are not taken into account"). Also, daily allowances, amounts of financial assistance and additional contributions to a funded pension are not taken into account (letter of the Federal Tax Service dated 08/09/19 No. SD-4-11 / [email protected] ; see “Standard deductions for personal income tax “for children”: are daily allowances and financial assistance taken into account when calculating the employee’s income limit?”).

Starting from the month in which the milestone is 350,000 rubles. passed, deductions for the child are canceled.

Let's give an example. Let’s say the monthly salary of an employee with children is 55,000 rubles. Then in the first half of the year his income will be equal to 330,000 rubles (55,000 rubles × 6 months). This means that in the period from January to June inclusive, the accountant will provide him with “children’s” deductions. In July, income will reach 385,000 rubles (55,000 rubles × 7 months). Therefore, in July and subsequent months of the year, deductions for children will not be provided.

Another reason for canceling the deduction is when the child reaches the age of 18. For older children in full-time education, there are two reasons: either completing their studies or reaching the age of 24. Experts from the Ministry of Finance explained: the right to deduction remains until the end of the year in which the child turns 18 years old. For full-time students, the same rule sounds like this: the right to deduction remains until the end of the year in which the child turns 24 years old, if training has not yet been completed. As soon as studies are completed, regardless of age, deductions stop (letter dated October 22, 2014 No. 03-04-05/53291; “The Ministry of Finance explained for what period the standard personal income tax deduction for children is provided”).

The question may also arise: for what period should a child deduction be provided if the employee applies for it in the middle of the year? Simply put, is it necessary to give a deduction for January and February if the employee applied for a deduction in March? The answer is contained in Article 218 of the Tax Code of the Russian Federation. It says that the deduction is due from the month of birth of the child, or from the month in which the adoption took place, guardianship (trusteeship) was established, or the child was placed in foster care. There are no additional conditions regarding the moment of applying for a deduction in the Code. Therefore, in case of a late application, the accountant must give a deduction retroactively. The Federal Tax Service for Moscow also agrees with this approach (letter dated December 26, 2017 No. 20-15 / [email protected] ; “Standard deduction for a child: what documents should an employee provide?”).

Is it necessary to give a deduction for “non-income” months?

There is no clear answer to the question of whether a “children’s” deduction should be provided for months in which the employee did not have income subject to personal income tax at a rate of 13%. The Russian Ministry of Finance believes that everything depends on whether income has resumed this year. If resumed, then deductions for “non-income” months can be provided. If there is no income until December 31 inclusive, then there will be no deductions this year (letter dated October 30, 2018 No. 03-04-05/78020. See “The employee will have no income until the end of the year: is he entitled to a standard deduction according to personal income tax?").

The Federal Tax Service thinks differently. The letter dated 05.29.15 No. BS-19-11/112 states that deductions for a child for months in which there was no income are due in any case (see “Federal Tax Service: standard tax deductions for children can also be received for those months , during which the individual did not have taxable income"). A similar point of view is set out in the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated July 14, 2009 No. 4431/09. In our opinion, this approach is correct, and thanks to the court’s position, it is completely safe.

Calculate “complex” wages under different remuneration systems

Child tax credit

Parents have the right to take advantage of deductions for children. At the same time, the Tax Code of the Russian Federation allows this application for each type of tax deduction for a child:

- standard child deduction;

- social deduction for a child.

NOTE! The spouse of the child's parent has the right to receive a tax deduction provided that the marriage with the child's father (mother) is officially registered.

See here for details.

What documents are needed for the “children’s” deduction?

Article 218 of the Tax Code of the Russian Federation stipulates that deductions for children are provided on the basis of a written application and documents confirming the right to deduction. But legislators did not provide a list of specific documents and did not indicate how often the employee must write a statement. Specialists from the Russian Ministry of Finance reported: it is enough to submit the application once, there is no need to update the application annually (letter dated 02/26/13 No. 03-04-05/8-131; see “The application for a standard tax deduction is submitted to the tax agent only once” ). A repeated application will be needed only if the employee’s circumstances for receiving the deduction have changed (letter from the Federal Tax Service of Russia for Moscow dated December 26, 2017 No. 20-15 / [email protected] ; see “Standard deduction for a child: what documents must the employee provide ?).

We have provided a list of required documents, compiled on the basis of explanations from officials, in Table 2.

table 2

What documents are needed to provide a “children’s” deduction in various situations?

| Situation | Documentation | Comment from the Russian Ministry of Finance |

| In any situation |

| letter dated 09.18.13 No. 03-04-05/38670 |

| Parents are divorced |

| letter dated 05/30/11 No. 03-04-06/1-125 |

| The parent lives with the child, but is registered at a different address | certificate from the housing and communal services about the joint residence of the child with the parent | letter dated 09.18.13 No. 03-04-05/38670 |

| A child under the age of 24 studies full-time (including at a paid university) | a certificate from the educational institution stating that the student is studying full-time | letter dated 10/02/15 No. 03-04-05/56445 |

| A child under 24 years of age is studying abroad | a certificate from the educational institution stating that the student is studying full-time, translated into Russian | letter dated 10.27.11 No. 03-04-06/8-289 |

| The wife's children from her first marriage live with their mother and her new husband, who did not adopt them | a statement from the mother stating that the children are jointly dependent on the spouses | letter dated 09/05/12 No. 03-04-05/8-1064 |

| The child is being raised by adoptive parents |

| letter dated 04/06/12 No. 03-04-05/8-465 |

Who is entitled to a deduction of 500 rubles.

These are persons awarded state awards, participants of the Great Patriotic War, former prisoners of concentration camps, disabled people of the 1st and 2nd groups and others. The full list can be found in sub. 2 p. 1 art. 218 Tax Code of the Russian Federation.

IMPORTANT! In the case where the taxpayer falls into both categories, the deductions are not summed up, but the maximum of them is provided. The taxpayer's income limit for receiving such deductions is not established by law.

If you have access to ConsultantPlus, check whether you have correctly determined the amount of the standard “for yourself” deduction. If you don't have access, get trial of online legal access.

Is it possible to provide a deduction without an application and other documents?

If the employee has not written an application and brought supporting documents, the employer cannot provide him with a “children’s” deduction. But this does not mean that the right to deduction is lost forever. At the end of the year, the employee should submit a declaration to the Federal Tax Service in Form 3-NDFL and attach the necessary documents to it. Then the inspectors will recalculate the taxable base for personal income tax and transfer the money to the employee’s account. This option was proposed by the Ministry of Finance of Russia in letter No. 03-04-08/8-230 dated December 23, 2011 (see “If the employee has not provided the employer with documents confirming the right to a “children’s” deduction, then you will have to contact the inspectorate to receive it”) .

The procedure for providing standard deductions for personal income tax

Standard tax deductions are provided to the taxpayer at his choice by one of the employers based on an application and supporting documents, which include:

- child’s birth certificate - when receiving a deduction for the 3rd and subsequent children, certificates are needed for all the employee’s children, regardless of their age and whether a deduction is provided for them or not (letter of the Ministry of Finance of Russia dated February 10, 2012 No. 03-04 -05/8-146, Federal Tax Service of the Russian Federation dated January 24, 2012 No. ED-4-3/ [email protected] );

- document on adoption, establishment of guardianship;

- certificate of disability;

- certificate from an educational institution.

To learn about what documents are needed to receive a tax deduction for education, read the material “What documents are needed for a tax deduction for education?” .

If an employee does not start work from the beginning of the year, the question arises: is a certificate of his income from his previous place of work required for deduction? Today there are 2 opposing opinions:

- provision of deductions is possible without a certificate from the previous place of work (letter of the Federal Tax Service of Russia dated July 30, 2009 No. 3-5-04 / [email protected] , resolution of the Federal Antimonopoly Service of the North Caucasus District dated April 14, 2010 in case No. A32-19847/2008-33/ 333);

- the employer does not have the right to provide a deduction without such a certificate (resolution of the Federal Antimonopoly Service of the North Caucasus District dated June 17, 2014 in case No. A32-11484/2012).

Therefore, if the employee has income from his previous place of work in the current year, it is advisable to still have a 2-NDFL certificate in order to avoid claims from controllers.

If the employer has not provided the taxpayer with a standard tax deduction, then the latter has the right to receive it from the Federal Tax Service at his place of residence. To do this, at the end of the year you need to submit a personal income tax return and documents confirming your right to deduction. By virtue of clause 7 of Art. 78 of the Tax Code of the Russian Federation, this can be done within 3 years. It is advisable to attach a 2-NDFL certificate to the declaration, which will speed up receipt of the deduction and refund.

For information on how to obtain a certificate, read the article “Where can I get (get) a 2-NDFL certificate?” .

Double deduction for a single parent (guardian, trustee, adoptive parent)

According to the Tax Code, the amount of the “children’s” deduction is doubled if the parent (including adopted), guardian, adoptive parent or trustee is the only one. In practice, this rule gives rise to many questions, since Chapter 23 of the Tax Code of the Russian Federation does not provide a clear definition of the concept of “single”. But there are many official comments that accountants are guided by.

Thus, according to officials, a parent is considered a single parent if the second parent is absent due to death. In addition, the parent is considered the only one if there is a court decision recognizing the second parent as missing (letter of the Ministry of Finance of Russia dated April 13, 2012 No. 03-04-05/8-503; see “The child’s parent has the right to receive a double “children’s” deduction for the reason recognition of the second parent as missing"). Finally, the child's mother is the only parent in cases where paternity has not been legally established. In particular, if information about the father is included in the birth certificate according to the mother (letter of the Ministry of Finance of Russia dated 02.02.16 No. 03-04-05/4973; see “The only parent of a disabled child may be provided with a “children’s” deduction in the amount of 24 000 rubles per month").

Officials also outlined situations in which a parent is not considered the only one and cannot claim a deduction (see Table 3).

Table 3

Situations in which a parent does not have the right to claim a double “children’s” deduction

| Situation | Officials' comments |

| One of the parents does not pay child support | letter of the Ministry of Finance of Russia dated November 2, 2012 No. 03-04-05/8-1246 |

| One of the spouses is deprived of parental rights | letter of the Federal Tax Service of Russia dated 09/02/15 No. BS-3-11/3340 |

| Both mother and father are indicated on the child's birth certificate, although the parents were not officially married | letter of the Ministry of Finance of Russia dated November 25, 2008 No. 03-04-05-01/443 |

| The parents listed on the child's birth certificate are divorced | letter of the Ministry of Finance of Russia dated November 25, 2008 No. 03-04-05-01/443 |

| One of the parents does not have income taxed at the rate of 13% | letter of the Ministry of Finance dated December 14, 2018 No. 03-04-05/91182 |

| Mother is on maternity leave | letter of the Ministry of Finance dated April 20, 2017 No. 03-04-05/23946 |

Be that as it may, the right to double deduction remains only until the single parent marries. Starting from the month following the month of the wedding, the “children’s” deduction becomes single. This is directly stated in the Tax Code, and the Ministry of Finance of Russia regularly reminds about this (see, for example, letter dated 04/11/13 No. 03-04-05/8-372.; “After marriage, the only parent loses the right to receive “children’s "double deduction").

As for the guardian, he can receive a double deduction based on a certificate issued by the guardianship and trusteeship authorities. This document must indicate that the citizen is appointed as the sole guardian of the child. Such clarifications are given in the letter of the Ministry of Finance of Russia dated December 14, 2015 No. 03-04-05/72969 (see “The Ministry of Finance clarified the procedure for providing a standard “children’s” deduction in double amount to the only guardian”).

Prepare all documents for the transition to electronic work books Try for free

Voluntary waiver of deduction in favor of the second parent

The Tax Code allows one of the parents (including adopted ones) to refuse the “children’s” deduction in favor of the second parent. To do this, you need to write an application, and the other parent will receive a double deduction. But there are a number of nuances that an accountant should be aware of.

Firstly, only a person who has this right can transfer his right to deduction. If a citizen does not receive income subject to personal income tax at a rate of 13% (for example, is on parental leave), then there is nothing to transfer to him. This means that the other parent is not entitled to a double deduction. The Russian Ministry of Finance recalled this in letter dated November 27, 2014 No. 03-04-05/60389 (see “A parent who does not have income taxed at a rate of 13 percent cannot refuse the standard deduction for a child in favor of a spouse”).

Secondly, it is possible that the income of the parent receiving a double deduction will exceed 350,000 rubles, and the income of the other parent will be less than this amount. Under such circumstances, the first parent loses the right not only to a double, but also to a single deduction. The low level of earnings of the “refusing” spouse does not matter (letter from the Ministry of Finance of Russia dated December 22, 2014 No. 03-04-06/66307; “The Ministry of Finance explained how to provide a standard deduction for a child in double the amount when the income limit is exceeded”).

Thirdly, during the inspection, inspectors will most likely require monthly certificates from the place of work of the “refusing” parent. These documents must prove that the income of the second spouse did not exceed 350,000 rubles, and his right to the deduction has not been lost. The Ministry of Finance of Russia is convinced that without such certificates a double deduction cannot be provided (letter dated 03/06/13 No. 03-04-05/8-178; “When providing a tax deduction for a child to one of the parents in double amount, a certificate of income of the other parent is needed submit monthly").

Fourthly, according to officials from the Federal Tax Service of Russia, an application to waive the deduction is not enough. A parent claiming a double deduction will also have to write a statement and bring it to his accounting department. This document must indicate the employee’s full name, address, TIN and details of the child’s birth certificate. The absence of such an application is a reason for refusing to provide a double deduction (letter No. ED-3-3/3636 dated November 3, 2011, see “To receive a double “children’s” deduction, both parents must submit applications to the tax agent of the person who will receive deduction").