Reasons for writing a letter of absence of activity

Throughout their business activities, companies may encounter various financial problems. In this case, companies suspend their activities and send a message to certain authorities about the lack of commercial activity. The notification is drawn up in the form of a letter along with reporting and sent to the Pension Fund and the tax office to the Social Insurance Fund. The most common reasons for issuing this notice include the following:

- economic crisis;

- suspension of activities;

- Liquidation of company.

The letter is drawn up as a certificate, the form of which is not provided for by law. This document is of a notification nature, informing government authorities that the company does not have commercial, financial and economic activities . Such a certificate is submitted along with monthly documentation. In the absence of this letter, the tax office has the right to forcibly liquidate the company (Read also article ⇒ Zero reporting of the simplified tax system).

Important! A certificate of absence of company activity is submitted to the Federal Tax Service, Social Insurance Fund and the Pension Fund of the Russian Federation. In some cases, a certificate may be required by other authorities, for example, the prosecutor's office when conducting scheduled inspections. In this case, at the oral request of the prosecutor's office, the company is obliged to provide this document.

Items that are subject to tax

Objects that are subject to value added tax are items subject to the sale of products or execution of a contract in Russia, including elements of collateral, and the transfer of products (results of executed contracts) under an agreement to provide an alternative option and change of material rights. In this case, the change of ownership of the results, products:

- services performed on a gratuitous basis are still considered a sale;

- transportation of products on the territory of Russia (execution of a contract) for one’s own needs, the costs of which are not deductible when calculating the income tax of institutions, including depreciation charges;

- performance of installation and construction services for your own consumption;

- import of products to the border territory of Russia.

At the same time, the Russian Tax Code identifies a list of transactions that are not considered a sale:

- carrying out operations that are related to the circulation of foreign or Russian currency (except for philately);

- transfer of the main fund, intangible assets and other property of the institution to its successor in law (successors) during its reformatting;

- transfer of fixed assets, intangible assets and other property to non-profit organizations for the conduct of main activities that are not related to the work of the private enterprise;

- separation of property when this transfer is in the nature of contributions (for example, investments in the fixed capital of business entities, investments under an ordinary partnership agreement (agreement on common work), relative investments in cooperative funds);

- transfer of property within the boundaries of the original investment to a participant in an economic company or partnership (his successor) upon exclusion from the economic company and upon division of the property of a liquidated economic company between members;

- transportation of property within the boundaries of the original investment to a member of an ordinary company agreement (agreement on common work) or his successor when allocating his percentage from the property that is common to the members of the agreement, or dividing this property;

- issuance of residential buildings to individuals in state or municipal buildings upon conversion to private property; taking away property through weaning, inheriting property and turning abandoned and ownerless items and animals into the property of other persons, discovery of treasures in accordance with the standards of the Civil Code of Russia; issuance on a free basis of inhabited premises, kindergartens, sanatoriums, clubs and other elements of socio-cultural and municipal purposes and highways, electrical networks, substations, gas pipelines, water intake buildings and other such elements to representatives of state power and representatives of local independence (or, at the choice of these bodies, special institutions that use or maintain these objects for their intended purpose);

- issuance of property of state and municipal institutions, redeemable as transfer to private ownership;

- execution of a contract by bodies included in the bodies of state power and local independence, within the boundaries of the execution of unique assignments assigned to them in a specific area in a situation where the need to execute this contract is regulated by the laws of Russia, its constituent entities, and acts of representatives of local independence.

Suspension of activities

If there is a need to suspend activities in a company, then a certain procedure will be required.

| Algorithm of actions in case of suspension of activity | More details |

| Decision-making | The basis for suspension is the decision of the founders or the manager (if, according to the company’s charter, he has the right to do so) |

| Issuance of an order | The manager issues an order to suspend the financial and economic activities of the company. |

| Cancellation of contracts | For transactions for which operations have not yet begun, cancellation occurs. Current transactions that can be unilaterally canceled are also terminated. |

| Fulfillment of existing obligations | If there are existing obligations, they must be fulfilled |

| Release of employees from their positions | All employees are relieved of their positions in accordance with Articles 180 and 157 of the Labor Code of the Russian Federation |

| Notification to government agencies | A certificate of absence of company activity is submitted to the Federal Tax Service, Social Insurance Fund and the Pension Fund of the Russian Federation. |

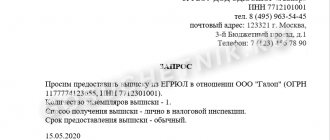

Letter of absence of activity to the Federal Tax Service

As noted above, a letter about the lack of activity of a legal entity is drawn up in free form, since the legislation does not provide for a special form. However, when compiling it, some requirements should be taken into account. So, when drawing up a certificate, the following is indicated:

- full name of the tax office;

- complete information about the legal entity, including contacts;

- name of the document (“Certificate of absence of activities and objects of taxation”);

- This is followed by the notification part, which lists the reasons for the suspension of activities, as well as documentary evidence of the current situation;

- date and signature of the head of the company, stamp if available.

When drawing up the notification part of the letter, it should be taken into account that it should contain the following information:

- information about the period of time during which the company’s financial and economic activities were not carried out (documents certified by the manager are attached, confirming the actual absence of activity);

- list of taxes for which there is no tax base.

Sample tax certificate

Ways to send a letter to the tax authority

There are several ways to send a letter to the tax office:

- By mail. In this case, an inventory of the attachments is compiled for the letter and it is sent as registered mail with acknowledgment of receipt.

- Personally to the tax office. Having appeared at the tax authority in person, the certificate is handed over to an authorized employee. In this case, 2 copies of a covering letter should be prepared for the certificate, one of which will remain with the tax office, and the second will be returned to the representative of the organization with a mark of receipt.

- Via courier service.

- By email through the tax website. This method of sending is considered official if the letter is certified by an electronic signature.

Check list. What to check and how to act

Step 1. Make sure that the request is sent to you

Open the electronic request and read it. Make sure that, firstly, the electronic document is opened, the file is not “broken” and is readable, and secondly, that the request is not sent incorrectly and to your company.

Step 2. Assessing legality and legality

The rules of tax law make it possible for tax authorities to request documents from a company or individual entrepreneur both within the framework of tax audits and outside the scope of audits.

Assess under what control procedure the requirement was raised.

Both in relation to your company and in relation to counterparties, documents can be requested:

1) directly during the audit, 2) during additional activities, 3) outside the framework of the tax audit. At the same time, documents or information on a specific transaction may be requested outside the framework of a tax audit .

The deadline for submitting documents depends on the type of control procedure:

Step 3: Find out who's under attack

Specify in relation to whom the tax office carries out tax control - in relation to your company or your counterparty (counter audit).

In the event of a counter inspection, you will receive a request from your inspection (at the place of registration of your company) with a copy of the order from the counterparty's inspection, which indicates the reason for the request with a list of documents. This procedure is defined by clauses 3, 4 of Article 93.1 of the Tax Code: someone else’s inspectorate must send an order to the Federal Tax Service Inspectorate at the place of registration of your company to request documents, and your Federal Tax Service Inspectorate will send you a request with a copy of the order.

During a counter-check, be sure to contact the counterparty, clarify the details and discuss actions. It is important! You can learn a lot of unexpected and useful things.

If you do not have the documents or information requested regarding the counterparty or transaction, no later than the next day after receiving the request, send a notification about this to your inspectorate.

Step 4. Explanation or documents

Specify what is required of you - explanation or presentation of documents. Perhaps both. But if the requirement does not indicate a list of documents, then explanations are sufficient.

Explanations are required, as a rule, as part of a desk audit when errors or contradictions are discovered in reporting. In this case, the requirement should indicate those errors and inconsistencies that you need to clarify. A special procedure for explanations has been established for VAT.

Generate a receipt and send it to the tax office.

The deadline for confirmation that you have received the request is 6 business days from the date the tax authority sent the request. If you do not do this, your account may be blocked.

The date of receipt of a request sent by registered mail is considered to be the sixth day from the date of sending the specified letter.

Step 6. Assess the “scale of the disaster”

Determine the composition and volume of the requested documents. This is important to determine the real possibility of submitting them to the tax office on time and how to respond.

Letter of absence of activity in the Pension Fund of Russia

As in the case of tax notification, there is also no approved form of document for notification of the absence of activity of the Pension Fund. Therefore, the company has the right to develop it independently. When preparing a certificate for the Pension Fund, be sure to indicate the following information:

- the period of time during which employees were accrued but not paid (that is, insurance contributions to the Pension Fund were also not transferred);

- a list of company employees with whom employment and other contracts have been concluded, under which monetary remuneration must be paid (the full names of the employees, their passport details, registration and actual residence addresses are indicated);

- the reason why employees are not paid;

- list of employees released from work due to layoff procedures or being idle.

The document is signed by the head of the company, as well as the chief accountant (

In a stream of disturbing news. Preparing a response to a request from the tax office

Requests from the tax office are no longer news, but, unfortunately, a familiar process.

In fact, it’s not even a surprise anymore. And some kind of indifferent fatigue, grief and anger. Well, how much can you do? (( Once again, the entire accounting department will have to spend at least a week running around groaning photocopiers or pushing tons of documents into exhausted scanners. It’s infuriating.

So, the request, alas, has been received.

Letter about lack of activity in the Social Insurance Fund

In addition to sending a letter to the tax office and the Pension Fund of the Russian Federation, the FSS will also need to notify the lack of activity. When writing a letter, you will need to indicate the following:

- name of the FSS body;

- name, details and contact details of the organization;

- information about the lack of activity, as well as the calculation and payment of social insurance contributions.

Important! This document is needed so that the Social Insurance Fund is informed that the organization did not work for a specific period of time. There is also no special form provided for this document, so the company has the right to develop it independently. The certificate should be accompanied by a bank statement confirming the fact that there were no funds in the account for a certain period of time.

How to submit an explanation to the tax office about the failure to provide 6-NDFL

When filling out explanations about failure to submit 6-NDFL, you must remember that:

- It is better to hand them over to the tax authorities during the period allotted to tax agents for providing 6-NDFL (1 month from the end of the reporting period);

- in the head part of the explanations, it is necessary to indicate the details of the merchant and the Federal Tax Service, to which the corresponding 6-NDFL should have been received;

- explanations are formulated in a laconic form (without excessive detail), but indicating all the necessary nuances;

- The manager or authorized representative must sign the explanations (in this case, attach a copy of the power of attorney to the explanations);

- explanations must be recorded in the outgoing correspondence journal.

The listed conditions are not requirements established by the Tax Code of the Russian Federation for explanations addressed to tax authorities in the event of a merchant’s failure to submit 6-NDFL. However, compliance by a merchant with these rules will allow tax authorities to:

- clearly identify the reasons and motives for non-submission of 6-NDFL;

- avoid the negative consequences of such failure to submit (fine and (or) suspension of account transactions).

And a merchant who provides clearly formulated explanations in a timely manner will avoid sudden blocking of his accounts and hasty issuance of additional explanations to controllers.

For one of the options for explaining to the tax office about failure to submit 6-NDFL, see the article “Filling out an explanation to the tax office regarding 6-NDFL - sample .

Answers to common questions

Question: Is there a fine for failure to notify the tax authority of the lack of activity?

Answer: No, there is no penalty for failure to notify. But the company will also have to submit reports and pay mandatory fees.

Question: How can you confirm that the company did not conduct financial and economic activities?

Answer: To do this, you will need to obtain a statement from the bank confirming that there are no movements on the current account. This will confirm that there were no movements on the account with the participation of the company.

What if it goes to court?

The judicial authorities attribute the assessment of circumstances, decisions on the timing and volume of required documents exclusively to the competence of the tax inspectorate conducting the audit . Like this.

It is clear that each company, based on its own situation and analysis of possible risks, makes its own decision on how to respond to the received demand and whether it is worth initiating legal proceedings.

Perhaps, given the wild decisions and millions of fines for failure to submit documents, it is worth going to court and defending your position.