Who submits simplified financial statements

The Law “On Accounting” dated December 6, 2011 No. 402-FZ provides for some organizations the right to use simplified methods of accounting, as well as to prepare simplified financial statements. In paragraph 4 of Art. 6 of this law lists the following subjects:

- organizations classified as small in terms of business volume;

- non-profit structures created in accordance with the Law “On Non-Profit Organizations” dated January 12, 1996 No. 7-FZ;

- participants of the Skolkovo project, subject to the Law “On Innovation dated September 28, 2010 No. 244-FZ.

To determine whether an organization is classified as small, you need to correlate its indicators with the requirements of the law “On the development of small and medium-sized businesses in the Russian Federation” dated July 24, 2007 No. 209-FZ.

About the criteria that must be met in order to call an organization a small enterprise, read the article “Small enterprise - designation criteria” .

In addition, those wishing to simplify their accounting should check whether they are subject to the restrictions established by clause 5 of Art. 6 of Law No. 402-FZ. This clause prohibits the use of simplified accounting and reporting, for example, by government organizations, entities subject to mandatory audit, and some legal structures.

Simplified balance sheet and balance sheet using the simplified tax system: what is the difference?

Companies using the simplified tax system (STS) must submit a balance sheet to the Federal Tax Service. The exceptions are individual entrepreneurs who conduct private practice and branches or representative offices of foreign organizations located on the territory of the Russian Federation.

Some legal entities using the simplified tax system are allowed to conduct reporting in a simplified manner:

- small business;

- NPO;

- organizations in the status of a participant in a project to carry out research and development with the subsequent commercialization of their results.

Simplified organizations that are not included in this list are deprived of this privilege. These are organizations with mandatory audit, housing cooperatives, credit consumer cooperatives, microfinance organizations, budgetary organizations, political parties, law offices and colleges, legal consultations, notary chambers and non-profit organizations from the register of organizations that perform the function of a foreign agent.

Thus, not all legal entities using the simplified tax system can apply the simplified accounting procedure, and the concepts themselves are not identical to each other.

Composition of simplified financial statements for 2021

Let's start with the fact that, by virtue of paragraph 1 of Art. 14 of Law No. 402-FZ, accounting consists of:

- from the balance sheet;

- financial results report;

- applications to them.

For a sample of a simplified balance sheet, see ConsultantPlus, having received trial demo access to the K+ system for free:

The annexes, in turn, are (clauses 2, 4 of order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n):

- statement of changes in equity;

- cash flow statement;

- report on the intended use of funds;

- explanations for reporting.

For information on preparing appendices to financial statements, see the material “Filling out Forms 3, 4 and 6 of the Balance Sheet.”

Note that for non-profit organizations, a report on the intended use of funds is designated as a form of mandatory annual accounting reporting along with a balance sheet (clause 2 of Article 14 of Law No. 402-FZ). Not only NPOs, but also other companies if they received targeted funds must fill out this report.

As for those who apply simplified rules, Order No. 66n contains special relaxations. In mandatory forms, you can indicate aggregated indicators, combined by groups. These forms are:

- balance;

- income statement;

- report on the intended use of funds.

For these three reports, legislators provided abbreviated forms in the mentioned order No. 66n; they can be found in Appendix 5. Those who have the right to simplify reporting have the opportunity to choose whether to use the forms given in the order or develop them themselves.

According to sub. “b” clause 6 of Order No. 66n in the appendices to the main forms it is necessary to indicate only those data that may influence the opinion of users of the reporting on the results of the organization’s work or its financial condition. Accordingly, if such important information is not available, then it is not necessary to fill out the applications. This is confirmed by paragraph 17 of the information of the Ministry of Finance of the Russian Federation No. PZ-3/2015.

Legal requirements for submitting accounting reports

Accounting statements are a set of documents of a certain content, compiled according to accounting data (clause 1, article 13 of the law “On Accounting” dated December 6, 2011 No. 402-FZ).

Keeping accounting records is not mandatory for individual entrepreneurs, private practitioners and divisions of foreign companies that keep records in accordance with the rules of Tax legislation (Clause 2 of Article 6 of Law No. 402-FZ). Accordingly, accounting is not mandatory for them. But the legal entity must prepare and submit it (subclause 5, clause 1, article 23 of the Tax Code of the Russian Federation). Today there are 2 options by which accounting records are formed (order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n):

- full;

- simplified, which can be used by legal entities that have the right to conduct accounting according to simplified rules.

Simplification of reporting implies the possibility of drawing up 3 forms of reporting in a reduced volume:

- balance sheet;

- financial results report;

- report on the intended use of the funds received.

Starting from 2022, reports must be submitted exclusively via electronic communication channels.

Read our article on how to submit documents to the tax office electronically.

If you have access to ConsultantPlus, check whether you are filling out simplified reporting correctly. If you don't have access, get a free trial of online legal access.

Changes in financial statements for 2022

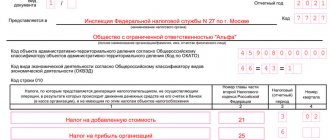

A small business has the right to submit simplified accounting reports using the KND form 0710096 (a single form that includes the balance sheet, form 2 and all appendices) or from Appendix 5 to the order of the Ministry of Finance dated July 2, 2010 No. 66n, by filling out a separate simplified balance sheet using the OKUD form 071001, a report on financial results - in the OKUD form 071002, as well as a report on the intended use of funds in the OKUD form 071003.

The KND form 0710096 has not changed in general. But the tax authorities made changes to the machine-readable form (see letter from the Federal Tax Service dated November 25, 2019 No. VD-4-1 / [email protected] ).

The forms from Appendix 5 have been amended since June 2022 by Order of the Ministry of Finance dated April 19, 2019 No. 61n. The changes were generally not significant:

- OKVED has been replaced by OKVED 2;

- The unit of measurement million rubles has been abolished, fill out the report only in thousands;

- OKI code has been corrected.

In the report on the intended use of funds, the OKUD code has also been changed.

You can download all 3 forms in excel format using the link below:

Where are financial statements submitted?

As a general rule, companies are required no later than three months after the end of 2022 to submit annual financial statements to the tax office at their location (clause 5, clause 1, article 23 of the Tax Code of the Russian Federation).

The annual accounting (financial) statements of a joint-stock company, subject to mandatory audit, are disclosed by publishing its text together with the auditor’s report on the Internet page no later than three days from the date of drawing up the audit report, but no later than three days from the date of expiration of the period established by the legislation of the Russian Federation for the submission of a mandatory a copy of the prepared annual accounting (financial) statements. A mandatory copy of the prepared annual accounting (financial) statements for 2022 is submitted no later than three months after the end of the reporting period (clause 10, article 13, clause 2, article 18 of Law No. 402-FZ, clause 71.3 and clause 71.4 of the Regulations No. 454-P).

In addition, the company is required to submit a legal copy of its annual financial statements to the state statistics body.

And if the reporting is subject to mandatory audit, then the organization is obliged to submit an audit report to the state statistics bodies (clause 2 of Article 18 of Law No. 402-FZ). The audit report is submitted to statistics together with the annual financial statements or no later than 10 business days from the day following the date of the audit report, but no later than December 31 of the year following the reporting year (clause 2 of article 18 of Law No. 402-FZ, Appendix to the Letter of the Ministry of Finance of the Russian Federation dated January 29, 2014 No. 07-04-18/01).

The audit report is not submitted to the tax authorities (Letters of the Ministry of Finance of the Russian Federation dated January 30, 2013 No. 03-02-07/1/1724, Federal Tax Service of the Russian Federation for Moscow dated March 31, 2014 No. 13-11/030545, dated January 20. 2014 No. 16-15/003855).

In addition, companies are required to submit financial statements to other addresses provided for by the legislation of the Russian Federation, the constituent documents of the organization, decisions of the relevant management bodies of the organization (clause 44 of PBU 4/99, Information of the Ministry of Finance of the Russian Federation No. PZ-10/2012).

Features of preparing simplified reporting

To address some issues related to the topic of our article, the Ministry of Finance of the Russian Federation issued information message No. PZ-3/2015. This message contains the main concessions for those using simplified reporting:

- The decision to disclose any information should be based on the materiality of the data to users (including the identification of individual items from groups of items in reporting forms).

- You don't have to write down the information:

- about related parties;

- segments;

- for discontinued activities.

- Events after the reporting date are shown in financial statements only if it makes rational sense.

- When changes are made to accounting policies, the significant consequences of this fact can be reflected in the financial statements prospectively.

- Significant errors from previous years can be corrected by affecting other income or expenses of the current period, without adjusting retained earnings/loss.

Recommendations on the use of simplified accounting methods provided by the Institute of Professional Accountants will help you avoid making mistakes when preparing reports. Get free trial access to ConsultantPlus and go to the material.

Filling out simplified reporting forms

A simplified balance sheet has enlarged items that include several accounting objects. The table below shows what is included in each balance line.

| Line title | Explanation |

| Assets | |

| Tangible non-current assets | Fixed assets, unfinished capital investments in them |

| Intangible, financial and other non-current assets | Intangible assets, results of research and development, investments in intangible assets, research and development, long-term financial investments (issued loans, bills, bonds), etc. |

| Reserves | Materials, goods, work in progress, finished products |

| Cash and cash equivalents | Cash in various currencies, converted into rubles, in the bank and at the cash desk. Their equivalents are highly liquid investments that can be quickly exchanged for cash without significant risk of loss, such as demand deposits |

| Financial and other current assets | Accounts receivable, advances issued, short-term financial investments, other immaterial current assets |

| Passive | |

| Capital and reserves | Authorized capital, additional capital, reserve capital, retained earnings. NPOs include in this line target funds, a fund of real estate and especially valuable movable property and other target funds |

| Long-term borrowed funds | Credits and borrowings for a period of more than a year and interest on them |

| Other long-term liabilities | Lender and targeted financing for a period of more than a year, reserves for upcoming expenses for a period of more than a year, etc. |

| Short-term borrowed funds | Credits and borrowings for a period of less than a year and interest on them |

| Accounts payable | Creditor to counterparties, personnel, budget, founders, advances received, etc. |

| Other current liabilities | Reserves for future expenses, targeted financing, deferred income with a period of less than a year, etc. |

The simplified statement of financial results does not highlight the types of expenses for core activities and some other indicators that detail its data when prepared in the usual form. The table below shows the components of this report.

| Line title | Explanation |

| Revenue | Revenue net of VAT and excise taxes |

| Expenses for ordinary activities | Cost, commercial, administrative expenses |

| Percentage to be paid | Interest on received loans and borrowings |

| Other income | Income not related to ordinary activities |

| other expenses | Other expenses less interest payable |

| Profit taxes (income) | Current income tax |

| Net income (loss) | Resulting string = 1 – 2 – 3 + 4 – 5 – 6 |

A form and sample for filling out the balance sheet for 2021 can be downloaded in the article “Accounting statements for 2021.”

Starting from 2022, financial statements must be submitted to the tax office only in electronic form. This applies to all business entities and there are no exceptions for anyone.

For information on existing methods of submitting reports via the Internet, read the article “Procedure for submitting tax reports via the Internet” .

Results

Small enterprises have the right to prepare accounting reports in both regular (full) and simplified (abbreviated) form. Simplification is expressed in a reduction in the number of reports themselves, as well as in the consolidation of data on the information reflected in them. However, it should be borne in mind that indicators that are significant and may influence the opinion of users of the statements must be disclosed either as separate lines in the reporting forms or in appendices to them.

For information on changes in accounting reporting effective from 2022, read the article “The procedure for submitting financial statements has been changed.”

Sources:

- Tax Code of the Russian Federation

- Federal Law of December 6, 2011 No. 402-FZ

- Letter of the Federal Tax Service of Russia dated November 25, 2019 No. VD-4-1/ [email protected]

- Letter of the Federal Tax Service of Russia dated July 16, 2018 No. PA-4-6/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

conclusions

Economic entities officially classified as small businesses, non-profit structures and some other organizations have the right to generate and submit annual reports either in abbreviated form or in standard form.

The possibility of such a choice is clearly provided for by specific provisions of current legislation.

Simplification of reporting consists in the fact that the number of completed reports is reduced, and the information reflected in these documents is noticeably generalized (enlarged).

In some cases, however, it may be necessary to clarify some reporting data by properly detailing the compiled forms or filling out appropriate annexes to the main documents.

The deadlines for submitting simplified financial statements and their required recipients do not differ from the deadlines/addressees typical for submitting standard reporting forms.