It is worth starting with the interpretation of the concept of depreciation. This term is interpreted as a gradual transfer of the amount spent on the acquisition of fixed assets to manufactured products (services).

There are tax consequences of adjusting the amount of depreciation deductions calculated according to the norms established by law. The amount of depreciation accumulation, which is set as a percentage of the existing book value of fixed assets, is otherwise referred to as the depreciation rate of fixed assets.

Basic Concepts

Depreciation is the process of gradual loss of consumer value from an asset. It is divided into physical and moral. In the first case, we are talking about a decrease in consumer value due to wear of parts, the negative influence of aggressive environments, and natural factors. In the second - a decrease in value regardless of physical wear and tear.

It is customary to distinguish between obsolescence of the 1st type (loss of the 1st initial value due to an increase in labor productivity in the industry where the operating systems are manufactured) and the 2nd type (the development of more progressive, economical equipment, as a result of which there is a decrease in the relative usefulness of outdated operating systems).

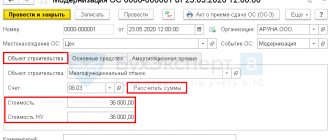

Objects of depreciation are fixed assets that are in the company either on the basis of ownership, or operational management, or economic management.

Useful life is the average service life of objects of a particular type.

The depreciation rate is the annual percentage of reimbursement of the cost of fixed assets, established by the state. In our country, uniform depreciation standards are used. This indicator is defined for each type of OS.

Economic meaning of depreciation

There are several versions, namely:

- Through the depreciation mechanism, cash flows are generated, which are subsequently directed to the reproduction of the PF.

- In accordance with the accrual principle, this is a way of splitting large investments in fixed assets into periods.

The depreciation rate for fixed assets is expressed as a percentage of the existing book value of classification groups of non-current assets. At the same time, the standards are widely differentiated by types of equipment, machines, as well as by the types of work where they are used, and by existing industries.

Increasing and decreasing coefficients

Businesses can use different ratios that speed up or slow down the depreciation process. The choice of indicators provided for in the Tax Code of the Russian Federation is reflected by the company in its accounting policies.

For equipment used in aggressive atmospheres or under extensive operating conditions, increasing factors are applicable. When calculating depreciation of fixed assets using the calculation formula, increasing factors are applied in amounts approved by law.

The organization, by decision of the manager, can also apply reducing coefficients. According to the Tax Code of the Russian Federation, special efficiency factors are applied to cars received or leased. For example, minibuses intended for passenger transportation, with a purchase price of more than 400 thousand rubles, are depreciated with k = 1/2.

All changes regarding the application of additional coefficients are fixed in the accounting policy of the enterprise and are valid throughout the entire tax period. Recalculation of depreciation of fixed assets using the calculation formula during the reporting period is not allowed.

Depreciation methodology

There are only five payment methods:

- Linear. In this option, the annual value of joint stock company is established on the basis of the initial cost of the fixed asset element and the depreciation rate. During the reporting period, deductions must be made every month in the amount of 1/12 of the total annual amount. The rate of linear depreciation is determined according to the previously presented second version of the formula.

- Reducing balance. Here, the annual value of joint stock company is based on the residual value of fixed assets at the beginning of the year (reporting), the depreciation rate, and a special acceleration factor (it should not be more than 3). The depreciation rate (formula 2) is calculated based on the service life.

- Cumulative. The annual size of the joint stock company is established on the basis of the 1st initial cost (when revaluing the replacement value), the ratio of the number of years remaining until the end of the service life to the sum of the numbers of years of the entire service life.

- Write-offs are proportional to the volume of manufactured products. When applying this method, accrual of joint stock is carried out on the basis of the natural indicator of the reporting period of the produced volume of products, the ratio of the 1-initial cost of the fixed assets to the expected volume of production for the entire service life of the fixed assets.

- Accelerated method (increase in deductions determined by the linear method). Full transfer of the cost of fixed assets (balance sheet) to production costs.

Method 1. Linear method

The straight-line depreciation method is the most common. During all periods, depreciation charges are the same. Accumulated wear increases evenly. Straight-line depreciation should be used when the asset is expected to provide equal value over its useful life and the asset's remaining usefulness declines evenly.

With the linear method, the annual amount of depreciation is determined by the formula (see clause 19 of PBU 6/01, paragraph “a” of clause 54 of the Methodological Instructions, approved by Order of the Ministry of Finance of October 13, 2003 N 91n):

SAgod = PS / N,

where SAgod is the annual amount of depreciation; PS - the initial cost of the fixed asset; N is the useful life, i.e. the number of years during which the organization plans to use this object (annual depreciation rate = 100%/N).

Below are 4 calculations created based on examples from the Guidelines.

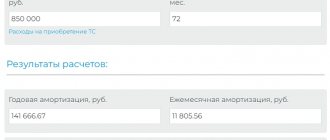

Example 1.1 . An item of fixed assets worth 120 thousand rubles was purchased. with a useful life of 5 years (annual depreciation rate - 20 percent (100% / 5 years)). The deadline for accepting fixed assets for accounting is December 30, 2013. Determine the annual amount of depreciation and the amount of monthly deductions. Solution. The annual amount of depreciation charges will be 24 thousand rubles. (120,000 x 20% / 100%) (see example file, sheet Annual amount of joint-stock company). For a fixed asset, depreciation begins to accrue in the month following the month the object was accepted for accounting, i.e. from January 2014. Therefore, the annual amount of depreciation for all 5 years will be the same = 24 thousand rubles. Monthly deduction amount = 1/12*24 thousand rubles = 2 thousand rubles.

Note : The solution to Example 1.1 can be obtained using the function APL(initial_cost; remaining_cost; operation_time) = APL(120000;0;5) .

Now consider the case when depreciation is calculated not from January, but again an entire number of years. We read PBU 6/01: If an object of fixed assets is accepted for accounting during the reporting year, the annual amount of depreciation is considered to be the amount determined from the first day of the month following the month of acceptance of this object for accounting until the reporting date of the annual financial statements.

Example 1.2 . In April of the reporting year, a fixed asset item with an initial cost of 20 thousand rubles was accepted for accounting; useful life is 4 years or 48 months (the organization uses the straight-line method). Solution. The annual amount of depreciation charges in the first year of use will be (20,000 rubles x 8 months / 48 months) = 3.33 thousand rubles, in subsequent years it will be (20,000 rubles / 4 years) = 5 thousand rubles, in the last year (20,000 rubles x (12 months - 8 months) / 48 months) = 1.67 thousand rubles. The amount of monthly deduction in any year is the same = 20 thousand rubles / 4 years / 12 months = 416.67 rubles.

Now let's look at an example where the Useful Life is NOT expressed in a whole number of years, for example: 2 years and 3 months (=27 months).

Example 1.3 . In May of the reporting year, a fixed asset item with an initial cost of 20 thousand rubles was accepted for accounting; useful life is 27 months. Solution. The annual amount of depreciation charges in the first year of use will be (20,000 rubles x 8 months / 27 months) = 3.33 thousand rubles, in subsequent years it will be (20,000 rubles / 4 years) = 5 thousand rubles, in the last year (20,000 rubles x (12 months - 8 months) / 48 months) = 1.67 thousand rubles.

Here the calculations become a little more complicated (see example file, sheet Linear. Annual amount of joint stock company, example 1.3).

To close the topic with the Linear method, the Linear sheet of the example file shows the calculation of the Residual value at the beginning and end of the month, as well as accumulated depreciation.

Example 1.4 . In March of the reporting year, a fixed asset item with an initial cost of 390 thousand rubles was accepted for accounting; useful life is 27 months. The method of calculating depreciation is linear. Determine the amount of accrued depreciation for the month and the residual value at the end of each month until the end of the service life. Amount of monthly deduction = 390 thousand rubles/27 months = 14,444.44 rubles.

The solution is given in the example file on the Linear sheet.

Because Since depreciation does not begin to accrue at the beginning of the year, the annual amount of depreciation charges will be different for different years.

Note : The graph was created based on ideas from the article Stepped Graph.

To calculate the amount of depreciation accrued per month, you can use the APL() function, i.e. =APL(390000;;27)

Depreciation rate: calculation formula

For accounting purposes, this indicator is calculated using 2 formulas. In the first case, the annual depreciation rate is determined as follows:

Us = (Pst - Lst): (Ap · Pst) · 100%, where

Pst – 1-initial cost of fixed assets, in rubles;

Lst – liquidation value of fixed assets, in rubles;

Ap – depreciation period, in years.

In the second option, the required indicator is established based on the service life of a specific OS object, expressed in years (T):

Us = (1 : T) · 100%.

This formula is used in both accounting and taxation. Directly for the last area, the 3rd formula for calculating the depreciation rate is applied:

Us = (2 : Tm) 100%, where

Тм – service life of a specific OS object, in months.

Important points ↑

In the process of use, the main assets of an enterprise invariably wear out and lose part of their value. In this case, wear and tear can be moral or physical.

Obsolescence of equipment due to the emergence of more advanced models leads to obsolescence. That is, existing objects fall in price, even if they remain in perfect condition.

Moreover, this can happen long before physical wear and tear, which is caused by natural use. Depreciation is always charged on long-lived assets.

The only exception is land and intangible assets used by the enterprise. Depreciation amounts are included in operating costs.

Depreciation continues throughout the useful life of the depreciable asset. In all cases of accrual of depreciation amounts, depreciation rates are determined.

These are regulated by the state, which exercises control over the speed of reproduction and growth rates in each individual economic sector.

For this purpose, ten main depreciation groups have been established. Each of them has its own depreciation rate. This average rate is used for tax accounting purposes.

In accounting, the rate of depreciation of an object is established based on the period of useful use determined for this property.

In this case, the useful life period of an organization can be established either independently or by belonging to a certain depreciation group.

What it is

Depreciation is the gradual process of transferring the cost parameters of an object to production costs. The depreciation rate is the part of the cost characteristic of an asset expressed as a percentage.

The indicator shows the ratio of the annual depreciation amount and the original cost of the property. The depreciation rate is the reciprocal of the useful life of an object.

The depreciation rate determines what proportion of fixed assets should be written off during the year. The level of depreciation rate is determined by the period of useful use of the object.

The depreciation rate depends on many factors - production capabilities, the ratio of resources and needs, the pace of technical progress, etc.

For each individual object or group, its own depreciation rate is established. The depreciation rate is calculated based on the initial cost of the objects, their standard service life and salvage value.

Various methods are used to calculate the annual depreciation rate. In particular:

- linear;

- reducing balance method;

- method of writing off value by the sum of the numbers of years of the useful life period;

- a method of writing off cost in proportion to the volume of production.

For what purpose is the indicator calculated?

The main objective of depreciation is the accumulation of capital necessary for the subsequent reimbursement of fixed assets or the costs of their repair.

In each case of sale of manufactured products, part of the funds included in the amount of transferred cost is sent to the depreciation fund.

Here, funds accumulate before the cost of the object is paid off. After this, the accumulated resources are used to purchase a new object. That is, an update (renovation) of production is taking place.

The sinking fund plays a central role in achieving designated goals and fulfilling depreciation standards in the future period.

The main functions of this fund should be considered:

| Renewal of production equipment | After its absolute wear and tear and disposal |

| Intense stimulation | Core Asset Updates |

| Accumulating the necessary amounts of money | For subsequent renovation of production facilities |

The main task of introducing depreciation standards into the cost parameters of fixed assets is economic compensation for physical and moral wear and tear, which is inevitable in the business process.

Simply put, with the help of depreciation rates, the cost of objects is smoothly transferred to manufactured products. It is the depreciation rate that allows you to monitor the rate of depreciation of an object and the rate of its restoration.

Current standards

Assets accepted for accounting are recognized as fixed assets if they comply with the requirements established by PBU 6/01 “Accounting for Fixed Assets”, adopted by Order of the Ministry of Finance of the Russian Federation No. 26n dated March 30, 2001 and “Methodological guidelines for fixed assets accounting”, ratified by Order of the Ministry of Finance of the Russian Federation No. 91n dated 13.10. 2003.

The property must be used for production purposes for a period of more than twelve months, must provide economic benefit and not be intended for subsequent resale.

The useful life refers to the period during which an object brings profit to the organization.

The term is set by the entity independently, based on operational characteristics and taking into account the “Classification of fixed assets”.

According to this, depreciable property objects are divided into depreciation groups according to their useful periods.

Depreciation is calculated in accordance with Order of the Ministry of Finance No. 147n dated December 12, 2005 for fixed assets, the list of which is given in clause 17 of PBU 6/01.

Depreciation rates are determined depending on membership in depreciation groups or on the period of useful use.

Useful life: basis for determination

This indicator is established based on the following:

- its expected value depending on performance, power;

- expected physical wear, which is influenced by the operating mode (number of shifts), aggressive environment, natural conditions, systems for carrying out the repair procedure;

- restrictions on the operation of this facility (regulatory and other, for example, lease term).

It is important to note that in the event of an increase in the initial standard indicators due to reconstruction or modernization, the company is obliged to review the service life of the improved facility.

This indicator is established based on the existing requirements of the OS Classification, which are included in special depreciation groups.

Shock absorption groups

For clarity, it is better to present the data in table form:

| Service life of depreciable assets, in years | Depreciation group |

| 1 — 2 | 1 |

| more than 2, but up to 3 | 2 |

| more than 3, but up to 5 | 3 |

| more than 5, but up to 7 | 4 |

| more than 7, but up to 10 | 5 |

| more than 10, but up to 15 | 6 |

| more than 15, but up to 20 | 7 |

| more than 20, but up to 25 | 8 |

| more than 25, but up to 30 | 9 |

| over 30 | 10 |

Based on the service lives presented above, depreciation rates are determined for each asset element. In other words, the volume of resources that are removed from taxation is established, as a result of which the financial base for the reproduction of public funds is formed.

Equipment subject to depreciation

This is something that is owned by the company and has an initial cost starting from 10 thousand rubles.

In accordance with current regulations, the following equipment is not subject to this procedure:

- if it has been preserved for more than 3 months;

- if it has been under reconstruction (modernization) for more than a year;

- if it was given free of charge.

Depreciation rates for equipment that is operated in aggressive conditions are calculated using a special coefficient established by the enterprise.

Monetary expression of PF depreciation

These are depreciation charges, which are included in the cost of manufactured products for subsequent investment. As mentioned earlier, their standards are set as a percentage of the existing book value of the PF. Depreciation is calculated every month. It stops accruing in relation to disposed objects from the 1st day of the following month.

The accumulation of depreciation charges and their expenditure are not reflected separately in accounting. They go to finance capital investments, long-term investments. Depreciation charges are spent on full (partial) restoration.

In the case of a complete overhaul, they must cover both physical and moral wear and tear due to the fact that technically outdated operating systems are not economically viable for operation even if they are physically suitable.

General information

Funds accrued for depreciation are included in the cost of manufactured products. That is, after the sale of goods, part of the proceeds goes to the depreciation fund. They are calculated taking into account the initial cost of assets, their depreciation period and use in the production process.

Not all property can be considered depreciable. Such, according to Art. 256 of the Tax Code of the Russian Federation, property is considered to be:

- is the property of the taxpayer;

- used by him to make a profit;

- compensated by depreciation charges.

The following are not subject to depreciation:

- property received for free use from third parties,

- housing facilities, unless they are used to generate income;

- immutable and irreplaceable types of fixed assets: land, forests.

Main functions of depreciation means:

- restoration of completely worn out or unusable equipment;

- gradual renewal of funds;

- acquisition of new equipment and facilities.

The accrual of depreciation amounts begins from the date of capitalization; the last period for accrual of depreciation will be the moment the means of production are removed from the balance sheet. Charges are not made during repairs, reconstruction or conservation for a period of at least three years.

Depreciation charges as an instrument of state policy in the field of industrial investment

Achieving significant structural changes is carried out primarily through depreciation rates. With the help of the production development fund, the accrued funds from joint stock companies are used to restore the capital fund in full. This takes the form of capital investments, through which the circulation of the previously advanced cost ends, and additional investments of funds are made due to the expansion of production and the improvement of its material and technical base.

It is impossible to ensure expanded reproduction only through joint stock companies, since they are intended primarily for simple reproduction. In this regard, a significant part of capital investments is provided by national income, while capital costs are reinvested primarily with the enterprise’s own funds. Also, share capital, share capital, credit resources, and sometimes funds from extra-budgetary funds and budgetary allocations are sent there.

Profit occupies an important place in the composition of enterprise funds used as capital investments. Today, one can observe a tendency to increase the share and absolute amount of profit in the sources of capital investment.

Finally, it is worth recalling that the article discussed such concepts as wear and tear, depreciation, depreciation rate, service life, etc.

Application of the wear and tear coefficient of fixed assets in financial analysis

OSes play an important role in the life of an enterprise. Financiers use various techniques for a comprehensive analysis of fixed assets and the dynamics of their movement.

You will learn about methods of analyzing the balance sheet from the material “Methodology for analyzing the balance sheet of an enterprise.”

KAOS refers to indicators of the state of the OS. Most often, it is considered along with the OS serviceability coefficient (CGOS), which characterizes the technical condition of the OS and is expressed by the ratio of the residual value of the OS to the primary value. The higher the CGOS, the better the technical condition of the OS.

It is calculated according to the formula

KGOS = Co/Sp,

Where:

Co - residual (final) cost of fixed assets;

Sp - initial cost.

This indicator, like KAOS, depends on the depreciation method used and is conditional. In this regard, it is more advisable to compare the values of these indicators with the data of competitors or with the average value in the industry.

More details about the KGOS can be found in the article “Formula for calculating the serviceability coefficient of fixed assets.”

In addition to the above indicators, do not forget about the moral and physical indicators of the OS condition.

Obsolescence is the depreciation of assets due to technical and technological progress.

Physical wear and tear - material wear and tear under the influence of climatic conditions or during labor. This depreciation is subject to accounting and can be determined in 2 ways:

- by useful life (expected) use (depreciation);

- during a technical inspection of an OS facility.

The analysis must be carried out in dynamics. Based on the results, a conclusion is drawn about the degree of suitability and wear of the OS.