Purpose of the document

The act certifies that the OS group has retired and is written off. Starting from the new month, accounting will stop calculating depreciation and property taxes for companies. In addition, after the destruction of fixed assets, materials may remain that can be useful in the company’s work, for example, precious metals, parts, scrap metal. Based on the act, the accounting department receives them at the price of potential use.

For your information! The acceptance of materials is recorded in the invoice according to form M-11. Information about write-off is indicated in the inventory card in the OS-6a form or in the book in the OS-6b form. The latter is used for small organizations.

Why do you need an act of write-off of fixed assets?

The act of write-off of fixed assets is a primary document that details the process of disposal of fixed assets.

Based on the information presented in the act, the following actions are taken:

- entries are made in the inventory card of the OS being written off;

- The following entries are generated in accounting:

- on write-off of OS;

- reflecting expenses associated with the disposal of fixed assets;

- capitalization of inventories remaining from the disposed fixed assets;

- non-operating income (expenses) are reflected in tax accounting (clause 13 of article 250 of the Tax Code of the Russian Federation, subclause 8 of clause 1 of article 265 of the Tax Code of the Russian Federation).

Read more about how to reflect the write-off of fixed assets in tax accounting in the Ready-made solution from ConsultantPlus. Trial full access to the system can be obtained for free.

There are unified forms of such acts (approved by Resolution of the State Statistics Committee of the Russian Federation dated January 21, 2003 No. 7). They differ in their scope of application:

- OS-4 – for fixed assets, except for vehicles and fixed assets group;

- OS-4a – for vehicles;

- OS-4b – for the OS group.

To generate an act of write-off of fixed assets, an organization has the right to use forms of its own design indicating all the required information (clauses 2–4 of Article 9 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ).

Whether it is necessary to restore VAT when writing off a fixed asset, find out from the ConsultantPlus experts. Get trial access to K+ for free and go to the Ready-made solution.

We will tell you in further examples how to correctly draw up a sample form for the write-off of fixed assets.

Samples of the act and conclusion of the commission on write-off of fixed assets

The act of writing off fixed assets, in essence, represents the conclusion of the competent commission on the possibility of writing off one or more objects. In this case, the act form first indicates information about the object and information about the events preceding the write-off. Let's give an example.

Based on the results of the inspection of the structure for storing inventory belonging to the Warehouse division of Mir Proizvodstvo LLC and registered as part of the OS, it was revealed that it was unsuitable for further use due to physical wear and tear and a defective statement was drawn up for write-off of the OS dated June 20, 2018 No. 3 .

By order of the executive director of World of Production LLC O. M. Mitin dated February 21, 2020 No. 26, a decision was made to dismantle the structure.

Information from the inventory card of the wooden structure:

- The employee responsible for its safety is Commandant A. A. Golovlev (account number - 000165).

- Inventory number - 0001596SK.

- Release (construction) date: 07/20/2008.

- The start date of operation is 07/21/2008.

- Useful life - 168 months.

- The actual service life is 131 months.

- Operating period - from 07/21/2008 to 02/21/2020 (139 months).

- Initial cost - 364,268 rubles.

- The amount of depreciation written off is RUB 284,042.

- Residual value - 80,226 rubles. (364 268 – 284 042).

The dismantling of the structure was carried out by a full-time worker, whose labor was paid according to agreement No. 1 dated 02/21/2020 to the employment contract. Labor costs amounted to RUB 10,640. (including insurance payments of 2,455 rubles). The structure was dismantled in 1 day (02/22/2020).

After dismantling the structure, boards (50 pcs.) with a market value of 120 rubles/piece. left for household needs.

Reinforcing metal structures (5 pcs.) costing RUB 1,130/pc. kept for sale as scrap metal.

ATTENTION! The material assets remaining after the dismantling of buildings and structures must be reflected in accounting and tax accounting. The primary document in this case is Form M-35 “Act on the Capitalization of Material Assets”.

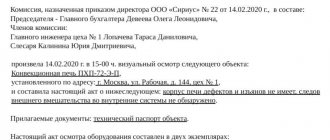

Based on the results of the dismantling of the structure, a decommissioning act was drawn up dated 02/25/2020 No. 4 (approved by the director on 02/29/2020).

An example of filling out a vehicle write-off report

After inspecting the passenger car damaged in the accident, assigned to the Office division of World of Production LLC, the commission made a decision on the financial impracticality of restoration (defective act dated 02/25/2020 No. 2).

By order of the director dated February 26, 2020 No. 14, a decision was made to dismantle the car, sell scrap metal and place working parts in the warehouse.

The car was handed over to the contractor for disassembly. Parts that are in working condition are registered as spare parts. The scrap metal was transferred to a warehouse for sale.

Vehicle write-off report No. 3 dated 02/27/2020 was completed on the basis of:

- vehicle inventory card;

- defective act dated 02/25/2020 No. 2;

- certificates of deregistration with the traffic police;

- certificate of services rendered by the contractor dated February 27, 2020 No. 145;

- act for the receipt of materials from car disassembly dated 02/27/2020 No. 1 (form No. M-35).

A completed sample act is presented below:

An example of filling out an act for writing off groups of fixed assets

On March 29, 2020, the inventory commission found unused printers in the Office division of Mir Production LLC (replaced with new high-performance MFPs).

By order of the director dated April 1, 2020 No. 5, it was decided to sell the discovered printers.

Act on write-off of fixed assets (group of printers) dated 04/05/2020 No. 2 was drawn up on the basis of:

- inventory cards for printers;

- inventory act dated March 29, 2020;

- act of purchase and sale of printers dated 04/05/2020 No. 12.

The completed sample act is posted below:

General information

Write-off begins after the issuance of the manager’s order on the procedure, as well as an act of a specially created commission on the impossibility of further use of the OS. The form is used for all OS objects, except transport. The OS-4a form is intended for it. For operating systems whose objects do not form a group, OS-4 is used.

The form is filled out by the employee responsible for recording and storing this group of OS objects. It is necessary to make 2 copies of the document: one for the above-mentioned employee, the second for the accounting department.

Filling out OS-4b

The form has a front and back side. Both must be filled out.

Front side of OS-4b

When filling out the header, you must indicate: the name of the organization, the name of the structural unit, OKUD and OKPO, the date when the object was written off from accounting, the full name and personnel number of the responsible person.

Next, note the number and date of preparation of the document to be filled out. Nearby there are fields for approval by the manager of the write-off. They are filled in at the very end.

Then the main part begins - on the front page it consists of a table with information about the state of OS objects. What you need to indicate in columns 1 to 8:

- Record number in order. Only one row in the table should be allocated for each object.

- OS object name.

- Inventory number.

- The actual operating life of the OS object.

- Initial or replacement cost.

- The amount of accrued depreciation.

- Residual value. It is calculated by finding the difference between the indicators in columns 5 and 6.

- Reason for write-off. This could be a breakdown, moral or physical wear and tear, or theft.

If the OS object contains precious metals, then fill out columns 9 to 13: indicate the name, item number, units of measurement, quantity and weight of raw materials.

Reverse side of OS-4b

Here the commission that conducted the inspection must write a conclusion. The chairman and members of the commission must sign, confirming the accuracy of the specified data.

Then there is a table with information about what material assets the company received from the write-off of fixed assets. This part is filled out in the accounting department. You must enter the following information:

- A document on the sale of valuables remaining from the OS object and its details.

- Name, item number, unit of measurement, quantity, cost of materiel.

- Correspondence of accounts.

- Serial number in the materials accounting card according to form M-17.

At the end of the table, the cost of all materiel values is summed up. Then indicate the results of the write-off, and write in words the amount of proceeds from the sale.

After this, the document is signed by the chief accountant and approved by the manager.

Instructions for filling out an act for write-off of fixed assets

The form has three sections. Each of them is designed to display specific information. An accounting employee is responsible for filling out the document. This can also be done by an employee who is responsible for the safety of fixed assets. In addition, a special commission is created that is directly involved in drawing up the act. Filling is carried out in four stages:

- Title page . Designed to indicate the company name. If the property belongs to a specific department or division, it is also indicated. The write-off is carried out on the basis of an order, therefore the date of its preparation and number are indicated on the title page. The date of direct write-off of the property is also indicated. Here you can see a column intended to indicate the reason for the write-off. This may be wear and tear, inappropriate repair, or physical aging.

- First table . Information and characteristics of the OS are entered here. The name of the product being written off, its serial and inventory numbers, the date of issue and registration with the organization must be indicated here. The relevant columns indicate the actual service life of the object, its initial cost and wear and tear costs.

- Second table . Additional data about the means is indicated here, for example, the materials that make up the OS. This table is filled out by members of the commission, confirming that the property is truly unsuitable for further use. The commission also gives its conclusion and detailed reason for the write-off. Each participant signs the document.

- Third table . Filled out by an accounting employee who calculates finances associated with the property being written off. If dismantling the OS required monetary costs, this must also be indicated in the document.

The document is completed in two copies. One of them remains with the employee who was financially responsible for this object. The second copy is transferred to the accounting department, where the official write-off is carried out.

Is it possible not to draw up an act?

When an object or equipment registered with an enterprise is written off, a corresponding mark is made on the inventory card. This is what the company's accounting department does. However, the basis for performing this procedure is the executed act of write-off of the fixed assets. It is also necessary for accounting purposes aimed at write-offs. Thus, without drawing up an act, it will not be possible to officially write off the property on the balance sheet of the enterprise.

Like other valid documents, the write-off act must be kept in the accounting department. After the expiration date, the document is sent to the organization’s archive for storage. He has been here for at least three years. There may also be a longer storage of the act, if this is provided for by the standards established by the organization.

When drawing up the act, try to avoid questionable wording of the reason for the write-off. The commission's conclusion should not raise additional questions for the inspection authorities. There are often situations when an accountant is accused of illegally writing off property, which may result in a fine. However, this employee only displays the write-off of the fixed assets in accounting. Although the accountant’s responsibilities do not include checking the commission’s conclusion and the grounds for write-off, it is still recommended to do so. The accountant must ensure that the commission's decision is as convincing as possible.

What are fixed assets

Fixed assets include any property of an enterprise used to carry out its activities: these can be materials, machinery, instruments, equipment, etc., in other words, everything that is involved in the labor process.

It should be noted that any inventory items acquired by an organization for work must be listed on its balance sheet. Once materials, equipment or machinery become unusable, they must be written off.

Reasons for write-off

As a rule, the reasons for write-off are physical wear and tear, obsolescence, irreparable breakdown, manufacturing defects, etc., that is, in fact, any irreversible defects in property that prevent its use .

Procedure

In order to write off fixed assets, it is necessary to first establish their unsuitability for further use. For this purpose, the company creates a special commission, the main task of which is to certify the fact of a defect, wear, etc.

The commission must include at least three people, including the financially responsible person.

Most often, only full-time employees of the enterprise are included in the commission, but in some cases, these may also be third-party experts who have the necessary knowledge and skills to determine irreparable failure, for example, of particularly complex equipment.

After the property is declared completely faulty, the commission draws up a special act, on the basis of which the organization writes an order to write off fixed assets. This order, in turn, serves as the basis for drawing up a write-off act.

Who writes the act

The same commission that recognized the inventory items as unfit for use is responsible for drawing up the write-off act. After the form is filled out, the act must be handed over to the head of the enterprise, without whose signature the document will not gain legal force.

How to draw up an act correctly

Today, the act of writing off fixed assets can be written in any form, however, most enterprise employees, in the old fashioned way, prefer to use previously generally applicable mandatory forms in their work. Their advantage is obvious: there is no need to rack your brains over the structure and content of the document, since all the necessary positions are indicated in it. Such unified forms also include form OS-4. This act can be filled out both when writing off one object or several at once.