Transport tax rates in St. Petersburg

For a year

| Name of taxable object | Rate (RUB) for 2022 |

| Passenger cars | |

| up to 100 hp (up to 73.55 kW) inclusive | 24 |

| over 100 hp up to 150 hp (over 73.55 kW to 110.33 kW) inclusive | 35 |

| over 150 hp up to 200 hp (over 110.33 kW to 147.1 kW) inclusive | 50 |

| over 200 hp up to 250 hp (over 147.1 kW to 183.9 kW) inclusive | 75 |

| over 250 hp (over 183.9 kW) | 150 |

| Motorcycles and scooters | |

| up to 20 hp (up to 14.7 kW) inclusive | 10 |

| over 20 hp up to 35 hp (over 14.7 kW to 25.74 kW) inclusive | 20 |

| over 35 hp up to 90 hp (over 25.74 kW to 66.20 kW) inclusive | 30 |

| over 90 hp (over 66.20 kW) | 50 |

| Buses | |

| up to 200 hp (up to 147.1 kW) inclusive | 50 |

| over 200 hp (over 147.1 kW) | 65 |

| Trucks, from the year of manufacture of which up to 3 years have passed inclusive | |

| up to 100 hp (up to 73.55 kW) inclusive | 25 |

| over 100 hp up to 150 hp (over 73.55 kW to 110.33 kW) inclusive | 40 |

| over 150 hp up to 200 hp (over 110.33 kW to 147.1 kW) inclusive | 50 |

| over 200 hp up to 250 hp (over 147.1 kW to 183.9 kW) inclusive | 55 |

| over 250 hp (over 183.9 kW) | 45 |

| Trucks, from the year of manufacture of which 3 to 5 years have passed inclusive | |

| up to 100 hp (up to 73.55 kW) inclusive | 25 |

| over 100 hp up to 150 hp (over 73.55 kW to 110.33 kW) inclusive | 40 |

| over 150 hp up to 200 hp (over 110.33 kW to 147.1 kW) inclusive | 50 |

| over 200 hp up to 250 hp (over 147.1 kW to 183.9 kW) inclusive | 55 |

| over 250 hp (over 183.9 kW) | 65 |

| Trucks that are more than 5 years old from their production year | |

| up to 100 hp (up to 73.55 kW) inclusive | 25 |

| over 100 hp up to 150 hp (over 73.55 kW to 110.33 kW) inclusive | 40 |

| over 150 hp up to 200 hp (over 110.33 kW to 147.1 kW) inclusive | 50 |

| over 200 hp up to 250 hp (over 147.1 kW to 183.9 kW) inclusive | 55 |

| over 250 hp (over 183.9 kW) | 85 |

| Other self-propelled vehicles, pneumatic and tracked machines and mechanisms | 25 |

| Snowmobiles, motor sleighs | |

| up to 50 hp (up to 36.77 kW) inclusive | 25 |

| over 50 hp (over 36.77 kW) | 50 |

| Boats, motor boats and other water vehicles | |

| up to 100 hp (up to 73.55 kW) inclusive | 50 |

| over 100 hp (over 73.55 kW) | 200 |

| Yachts and other motor-sailing vessels | |

| up to 100 hp (up to 73.55 kW) inclusive | 100 |

| over 100 hp (over 73.55 kW) | 400 |

| Jet skis | |

| up to 100 hp (up to 73.55 kW) inclusive | 250 |

| over 100 hp (over 73.55 kW) | 500 |

| Non-self-propelled (towed) ships for which gross tonnage is determined (from each registered ton of gross tonnage) | 200 |

| Airplanes, helicopters and other aircraft with engines (per horsepower) | 250 |

| Airplanes with jet engines (per kilogram of thrust) | 200 |

| Other water and air vehicles without engines (per vehicle unit) | 1000 |

FILES

Note to the table: the values are given in St. Petersburg for 2016, 2022, 2022, 2022, 2022, 2022, 2022. To select rates for a specific year, use the selector.

According to the Federal Tax Service, 2.18 million vehicles are registered in St. Petersburg. Owners of this equipment, data on which are obtained from the registration authorities, are required to pay transport tax. In the northern capital, rates and payment procedures are fixed by law dated November 4, 2002 No. 487-53.

Useful links on the topic “Transport tax rates in St. Petersburg in 2022 - 2022”

- Personal income tax 15%. Progressive scale

- Tax on interest on deposits

- Tax control of accounts

- Why are benefits declarative in nature?

- Personal income tax on inheritance

- Tax liability for failure to submit documents

- Minimum wage in St. Petersburg

- Living wage in St. Petersburg

- Property tax rates in St. Petersburg

- Property tax benefits in St. Petersburg

- Transport tax rates in the Leningrad region

- Transport tax benefits in the Leningrad region

- Transport tax rates in St. Petersburg

- Transport tax benefits in St. Petersburg

- Child benefits in St. Petersburg

- Where to get a compulsory medical insurance policy in St. Petersburg

- Passport offices of St. Petersburg

- Addresses, telephone numbers, websites of tax inspectorates of St. Petersburg

- District courts of the Leningrad region

- District courts of St. Petersburg

- Territorial jurisdiction of district courts of St. Petersburg

- Court districts of magistrates of the Leningrad region

- Territorial jurisdiction of justices of the peace of the Leningrad region

- Judicial areas of justices of the peace in St. Petersburg

- Territorial jurisdiction of justices of the peace in St. Petersburg

- Reference and legal information for the city of St. Petersburg and Leningrad. region

- The procedure for obtaining confirmation of the status of a tax resident of the Russian Federation

- When and what to report to the Federal Tax Service

- Convention on the International Exchange of Tax Information

- Taxpayer personal account

- Tax benefits for pensioners - procedure for provision and sample application

- How to pay taxes online

- Should children pay taxes?

- How to get a deferment (installment plan) for paying taxes

- Tax audits

- What should a complaint to the tax inspectorate contain?

Tax return

- Complete list (list) of persons who are required to file a tax return

- Sample of filling out the 3-NDFL tax return for 2022:

- title page, sections 1, 2

- income from sources in the Russian Federation (Appendix 1);

- calculation of property tax deduction for expenses on the purchase of real estate (Appendix 7)

- calculation of property tax deductions for income from the sale of property (Appendix 6);

- calculation of social tax deductions established by subparagraphs 4 and 5 of paragraph 1 of Article 219 of the Tax Code (calculation to Appendix 5);

- calculation of standard, social, investment tax deductions (Appendix 5);

Taxes

- UTII

- Land tax

- Personal income tax (NDFL)

- Income not subject to taxation

- Who are tax residents and non-residents

- Sale of an apartment by a tax non-resident of the Russian Federation

- The procedure for calculating and paying personal income tax upon the sale of a share in the authorized capital of an LLC, shares of an OJSC, securities

- Personal income tax on payments by court decision

- Tax on the sale of currency and income on Forex

- How to reduce personal income tax when buying and selling a car

- How to reduce personal income tax when selling and buying a home

- Procedure for paying personal income tax if an employee is on a business trip abroad

Tax deductions

- Property tax deductions

- How to get a property deduction when buying a home on credit

- How to get a deduction for improving housing conditions

- When can you get a deduction of 2,000,000 rubles when purchasing a room or a share of an apartment?

- Is a non-working pensioner entitled to receive a property tax deduction in connection with the purchase of an apartment?

- List of medicines for which social tax deduction is provided

- List of expensive types of treatment for which a social tax deduction is provided (approved by Decree of the Government of the Russian Federation of March 19, 2001 No. 201)

Tax liability for:

- failure to provide documents

- failure to provide tax reporting;

- incomplete payment of taxes;

- failure to appear when called to the tax authorities

Tax calculation and payment deadlines for organizations

Legal entities registered in St. Petersburg must make advance payments.

Advance refers to the amounts transferred by a legal entity to the treasury during the tax year. They are paid three times: for the previous quarter no later than April 30, July 31 and October 31. Advances are calculated based on the estimated tax amount for the year. Interim contributions equal to 25% of the total payment.

The portion of obligations remaining unpaid after the transfer of advances must be received by February 10.

Deadline for payment of transport tax for legal entities in 2022:

- for 2022 - no later than March 1, 2022

- for the 1st quarter of 2022 - no later than May 2, 2022

- for the 2nd quarter of 2022 (6 months) - no later than August 1, 2022

- for the 3rd quarter of 2022 (9 months) - no later than October 31, 2022

- for the 4th quarter and the entire year 2022 - no later than March 1, 2023

How to correctly calculate transport tax in St. Petersburg

For individuals, the amount of the transport fee is calculated by tax authorities. However, vehicle owners can independently check the accuracy of the accrual, and if an error is detected, challenge the amount presented for payment. The easiest way to calculate transport tax is to use the calculator available on the Federal Tax Service website.

When filling out the fields of the electronic form, the following information is entered:

- Vehicle release date.

- Type of equipment - truck, motorcycle, etc.

- Engine power installed in the PTS.

- Length of time you owned the car in the previous tax year.

After filling out all the fields, click the “ Next ” button, and the calculator provides the required information.

Another way to calculate is using a simple formula:

N = Bs x Md , where N is the required tax amount, Bs is the base tax rate, Md is the vehicle engine power.

Also, when calculating, you need to take into account the increasing factor if your car is a luxury item, that is, it costs over 3 million rubles . For some categories of citizens, full and partial exemption from transport tax is provided. Therefore, you should find out from the regional branch of the Federal Tax Service whether the owner of the vehicle belongs to a preferential category.

Rules and deadlines for paying taxes for individuals

Every citizen who has registered a vehicle that belongs to him must pay tax on the basis of a notification that will be sent to him from the Federal Tax Service. This document is sent on the basis of information received by the Federal Tax Service over the past year. It displays information on tax objects, applied rates and benefits. A notification is sent to your residential address.

If all the data in it is true, individuals must make payment no later than the nearest December 1st. In case of delay in payment, a fine equal to 1/300 of the refinancing rate accepted in the Russian Federation is charged daily for the entire amount of the debt.

Deadline for payment of transport tax for individuals in 2022:

- for 2022 - no later than December 1, 2022

- for 2022 - no later than December 1, 2023

Please take into account: in accordance with paragraph 7 of Art. 6.1. Tax Code of the Russian Federation, if the last day of the period falls on a weekend, then the day of expiration of the period is considered to be the next working day following it.

Deadline for transferring transport tax to the treasury

Payment of car tax, which is a regional tax, is made for each vehicle registered with the organization. The timing of its payment to the regional budget is independently regulated by local officials. The date of payment of the transport fee varies in different regions.

What remains the same is that, unlike an individual who pays a fee in the form of tax using a receipt from the tax office, the company reports on the payment of the vehicle tax fee by submitting a declaration to the Federal Tax Service. Declarations of legal entities are submitted to tax inspectors no later than February 1 of the year following the reporting year.

Tax deductions for vehicles are paid by transferring quarterly advance payments, the amounts of which are taken into account at the end of the tax period when determining the amount and payment of transport tax. The advance tax payment must be paid by February 10 of the year following the expired tax period.

Benefits for individuals

In St. Petersburg, an extensive list of tax benefits has been introduced for citizens who own transport. Here is a list of groups of city residents who have the right to use a reduced rate or exemption from the need to pay:

- Holders of the star of the Hero of the USSR or the Russian Federation, full holders of the Order of Glory or Labor Glory, Heroes of Labor or Socialist Labor;

- veterans and disabled combat veterans;

- disabled people (groups I, II);

- radiation victims in Chernobyl, at Mayak Production Association;

- guardians of disabled children;

- owners of cars and motorcycles manufactured in the USSR before 1990;

- citizens aged 60 or 55 years (men and women, respectively);

- spouses of those killed while performing the duties of employees of fire protection or internal affairs and state security agencies;

- guardians in large families.

FILESOpen the table of transport tax benefits in St. Petersburg

Tax benefits for paying taxes for legal entities

When determining the auto tax, the organization’s vehicle should be checked to see if the vehicle is subject to exceptions that are not subject to taxation in accordance with paragraph 2 of Article 358 of the Tax Code.

The state at the federal level decides which categories of taxpayers will pay auto tax, calculates and recommends its maximum amount, and determines benefits. Regional officials are authorized to approve additional benefits for companies and residents registered in this region.

The transport tax for 2022 in St. Petersburg has been abolished for vehicles using natural gas as motor fuel. The limitation of this law is the amount of wages of employees in the organization on whose balance sheet the vehicle is recorded.

Companies registered in St. Petersburg are exempt from paying tax in relation to vehicles (except air and water vehicles) on which an electric motor with a power of up to 150 hp is installed. With.

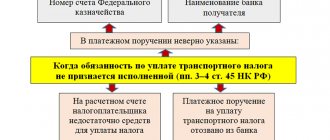

Responsibility for non-payment of transport tax

If an individual fails to pay the transport tax for trucks, he will be charged a fine of 20% of the arrears. And for each day of delay, a penalty of 0.003–0.006% “drips” (Tax Code of the Russian Federation, clause 4, article 75 “Penya”, No. 146-FZ), depending on the period of non-payment. First the minimum, then the maximum.

For malicious evasion of tax obligations, the sanction is increased to 40% of the amount of the fee (TK, Art. 122, No. 146-FZ “Non-payment or incomplete payment of tax amounts”). At the same time, the violator may be prohibited from registering actions with property (movable and immovable). And the accounts will be blocked by the bank or bailiffs by court order until the debt, penalties and fines are fully repaid.