Which companies are required to pay transport tax?

Tax legislation establishes that all legal entities that own vehicles are required to pay tax.

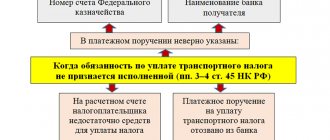

Termination of obligation is possible only if the vehicle is deregistered or destroyed. But both of these facts need to be documented , otherwise the Federal Tax Service will not take them into account.

That is, the fee will still have to be paid, even if the organization has not used the equipment for a long time, has leased it or contributed it to the authorized capital of another company.

But there is one exception - a company is exempt from paying transport tax if the equipment was sold due to enforcement proceedings.

The fee applies to most shipping, water and air vehicles. But some legal entities have the opportunity to save money. For example, the law exempts owners of offshore platforms, special equipment for agricultural activities, and fishing vessels from payment.

Article 358. Object of taxation

1. The objects of taxation are cars, motorcycles, scooters, buses and other self-propelled machines and mechanisms on pneumatic and caterpillar tracks, airplanes, helicopters, motor ships, yachts, sailing ships, boats, snowmobiles, motor sleighs, motor boats, jet skis, non-self-propelled (towed vessels) ) and other water and air vehicles (hereinafter in this chapter - vehicles) registered in the prescribed manner in accordance with the legislation of the Russian Federation.

2. The following are not subject to taxation: 1) rowing boats, as well as motor boats with an engine power of no more than 5 horsepower; 2) passenger cars specially equipped for use by disabled people, as well as passenger cars with an engine power of up to 100 horsepower (up to 73.55 kW), received (purchased) through social welfare authorities in the manner prescribed by law; 3) fishing sea and river vessels; 4) passenger and cargo sea, river and aircraft owned (by the right of economic management or operational management) of organizations and individual entrepreneurs whose main activity is passenger and (or) cargo transportation; 5) tractors, self-propelled combines of all brands, special vehicles (milk tankers, livestock trucks, special vehicles for transporting poultry, machines for transporting and applying mineral fertilizers, veterinary care, maintenance), registered to agricultural producers and used in agricultural work for the production of agricultural products ; 6) vehicles owned by the right of operational management to federal executive authorities, where military and (or) equivalent service is legally provided for; 7) vehicles that are wanted, subject to confirmation of the fact of their theft (theft) by a document issued by the authorized body; airplanes and helicopters of air ambulance and medical services; 9) ships registered in the Russian International Register of Ships.

Instructions on how to calculate transport tax

Transport tax is calculated using the formula:

TN = NB x NS , where:

- NB – tax base

- TS – tax rate current at the time of payment

The formula becomes more complicated if the company:

- makes advance payments

- wants to take advantage of tax benefits

- applies different coefficients

If all three conditions above are met, the calculation looks like this:

TN = NB x NS x Kv x Kp - NL - AP , where:

- Kv – vehicle ownership coefficient

- Кп – increasing coefficient

- AP – advance payments

- NL - benefits to which the payer is entitled

This is the complete formula, but it may vary depending on the situation.

Features of transport tax for legal entities

Transport tax for legal entities, as well as for individuals, is calculated using a simple formula:

Tax base × tax rate.

In addition, decreasing/increasing coefficients can also be added to this formula, and the tax rate in the region can be reduced or increased in relation to the basic values specified in paragraph 1 of Art. 361 Tax Code of the Russian Federation. But the tax rates established in the constituent entities of the federation cannot differ from the base ones by more than 10 times - such a limitation is specified in paragraph 2 of Art. 361 Tax Code of the Russian Federation.

Read more about the procedure for calculating transport tax for cars in our article “How to calculate transport tax for a car?” .

For expensive cars, the cost of which exceeds 3 million rubles, an increasing factor is applied. This coefficient can be found in paragraph 2 of Art. 362 of the Tax Code of the Russian Federation. Its value depends not only on the cost of the car, but also on the period of its use after release. Prices for luxury cars are updated annually and are available for viewing on the official website of the Ministry of Industry and Trade.

Taxpayers who are legal entities, unlike individuals, must calculate their taxes independently. Despite the fact that tax returns for 2020 have been canceled for organizations, and the Federal Tax Service must send them messages with the amount already calculated, legal entities must still calculate the tax themselves. First, they must know the amount in order to make advance payments throughout the year (if they are established in the region). And secondly, the message from the tax office is more of an informational nature, so that the company can compare its accruals with those made according to the tax authorities. After all, she will receive it after the deadline for paying advances (see, for example, letter of the Ministry of Finance dated June 19, 2019 No. 03-05-05-02/44672).

The message from the Federal Tax Service will indicate the object of taxation, tax base, tax period, rate and amount of calculated tax.

Important! Recommendation from ConsultantPlus Compare the amount of tax calculated by the inspectorate with the amount you calculated and paid yourself. If they are equal, then the tax was calculated and paid correctly. If the amounts differ, check:... What to check and what to do in case of an error (yours or the tax authorities), see K+. Trial access to the system can be obtained for free.

ATTENTION! If you do not receive the notification, you are required to independently inform the tax authorities about your taxable property. Read about the nuances in the material “Organizations will have to report transport and land plots to the tax authorities.”

Main meanings of the formula

The main parameters for calculating tax are the tax base and tax rate . They are not excluded from the formula in any case. Other indicators complement it, if necessary in a specific situation.

The NB value can be found in the registration certificate or other documents for the vehicle. The base becomes engine power, gross tonnage or vehicle unit.

Please note that the engine power indicated in kW must be recalculated in horsepower: the number of kW must be multiplied by 1.35962 (this is a constant value). The resulting result must be rounded to 2 decimal places.

As for the tax rate, it is set by regional authorities and depends on:

- tax bases

- age of technology

- vehicle categories

- environmental class

If the LSG body has not determined the rates, companies have the right to use the basic indicators prescribed in Art. 361 Tax Code of the Russian Federation .

To find out the tax authorities in a specific region, you can use the Federal Tax Service help service:

- Specify region.

- Enter “About transport tax” into the search. The system will automatically display the law that is in force in the desired subject of the Russian Federation.

- Click "More details".

- Go to the “Bets” tab.

- Check the box next to “Legal Entity”.

- Click the “Show” button.

The service will display rates for TN in the selected region.

Calculation example

The calculation, made with only the basic values, is very simple. For example, during 2022, the company owned a passenger car with a power of 145 hp, which is the tax base. The tax rate in the region is 35 rubles.

We multiply the two indicators and get the amount of transport tax:

145*35 = 5 075 rubles

This is how much the organization needs to pay without taking into account advance payments, benefits and coefficients.

Advance payments and final technical specification

The frequency of advance payments depends on whether the regional authorities have established reporting periods or not. If yes, then you need to pay quarterly, if not, then at the end of the year.

Advance payments are made in equal installments. The formula used to calculate them is as follows:

AP = ¼ x TN

At the end of the year, TN is calculated minus advance payments:

TN = NB x NS – AP

Calculation example

Throughout 2022, the company owned a passenger car with an engine power of 150 hp, which is considered the tax base. The regional rate is 10 rubles.

First, the tax amount is calculated:

150*10=1500 rubles

Then the advance payment is determined from it:

¼*1500=375 rubles

The final transport tax, taking into account advances made every quarter (that is, 3 times), is calculated as follows:

1500- (375*3)=375 rubles

Accounting for vehicle ownership coefficient

An organization applies a ownership coefficient (Q) when equipment is not registered for it for the entire reporting year or quarter. If the vehicle is owned for a full year, then the coefficient is 1 and does not affect the final amount of the TN. Therefore it is not taken into account.

The coefficient is calculated using a separate formula:

Kv = number of full months of vehicle ownership/number of months in the reporting period

How is an incomplete month of vehicle ownership taken into account?

As mentioned above, if a legal entity owns a vehicle for an incomplete period, it is necessary to apply the ownership coefficient. Let's look at how all this is taken into account using an example.

The company on March 10 , 2022. (this is NB). The tax rate in the region is 10 rubles. How, in this case, to calculate the advance for the first quarter and the transport tax at the end of the year?

Please note that there is a "15th" rule :

- the car was registered in the period from the 1st to the 15th of the month (inclusive)

- the car was deregistered from the 16th to the 30th (31st) day of the month (for February from the 16th to the 28th/29th)

In this case, this rule works exactly. The car was registered on March 15, which means that this month is taken into account in full for calculating tax.

First we calculate the ownership coefficients:

- first quarter – 0.3333 (1 month of ownership/3 months of the reporting period)

- at the end of the year – 0.8333 (10 months/12 months)

Then we move on to advance payments:

- first quarter – ¼*150*10*0.3333=125 rubles

- second – ¼*150*10=375 rubles

- third – ¼*150*10=375 rubles

Finally, we calculate the total amount of transport tax:

150*10*0,8333 — (125+375+375)=375 rubles

We must not forget that the TN amount is rounded to the nearest ruble if it comes out to more than 50 kopecks.

Procedure for calculating tax and advance payments

Transport tax is calculated separately for each vehicle. Organizations independently determine the amount of transport tax. Individuals do not need to calculate tax: the inspectorate will send them a request to pay transport tax. To calculate the amount of transport tax that needs to be paid to the budget, multiply the tax base by the tax rate. If you own the vehicle for less than a year (for example, a few months), then the tax is paid only for those months. To calculate transport tax for several months, you need to determine the coefficient:

| Number of full months during which the car is registered to the company | : | 12 months | = | Correction factor |

The tax amount is calculated as follows: the tax base is multiplied by the tax rate and by the correction factor. In this case, the month of registration of the vehicle, as well as the month of deregistration of the vehicle, are taken as a full month. In case of registration and deregistration of a vehicle within one calendar month, this month is taken as one full month.

At the end of each reporting period (Q1, Q2 and Q3), firms pay advance payments for transport tax. They are calculated as follows: the total amount of transport tax (the product of the tax base and the tax rate, taking into account the correction factor) is divided by 4.

And at the end of the tax period (year), the difference between the annual tax amount and the amount of advance payments transferred during the year is transferred to the budget.

Regional authorities may exempt certain categories of firms from paying advance payments for transport tax. In this case, Osvobozhdeniye residents will have to remit tax only at the end of the year.

What is a multiplying factor?

Tax legislation requires the use of an increasing coefficient (Kp) if the company owns a high-value passenger car. This value depends on the average price and age of the car.

The list of cars for which the KP must be applied when calculating tax is published on the official website of the Ministry of Industry and Trade. This list is updated every year. The new version can be viewed no later than March 1 .

Calculation of TN taking into account KP is carried out according to the following formula:

TN=NB*NS*Kp – AP

Advance is calculated as follows:

AP = ¼*NB*NS*Kp

Calculation example

Throughout 2022, the company owned a BMW 340i xDrive Gran Turismo passenger car with a power of 326 hp (HP), costing 3,200,000 rubles. The tax rate in the region is 150 rubles. In accordance with the list of the Ministry of Industry and Trade, the increasing coefficient for such a machine is 1.1.

Prepaid expense:

¼*326*150*1,1=13 448 rubles

Final transport tax:

(326*150*1,1) – (3*13 448)=13 446 rubles

Tax period of transport tax

The tax period is the period of time after which the tax is calculated and paid into the budget (Clause 1, Article 55 of the Tax Code of the Russian Federation).

In accordance with paragraph 1 of Art. 360 of the Tax Code of the Russian Federation, the tax period for transport tax is 1 year.

For all owners of cars, motorcycles and other vehicles, this time period is the same. It does not depend on the brand of vehicle, engine power or other characteristics.

There is also no difference in the length of the tax period in relation to the transport of a businessman and a similar vehicle of an ordinary person who is far from business activity. For all these persons, the tax period for transport tax is a calendar year.

You will learn about the features associated with the payment and calculation of TN from this article.

The duration of the tax period for the specified tax does not depend on the location (registration) of transport, although tax legislation grants greater powers to the regions in matters of technical tax (to determine tax rates, etc.). We will talk about the features of regional legislation related to the calculation and payment of transport tax in the next section.

IMPORTANT! Starting with the reporting campaign for 2022, organizations do not need to report on transport to the Federal Tax Service. The tax authorities will calculate the tax amount themselves. The payment deadline also changed and became uniform throughout the country: March 1 of the year following the reporting year. The deadline for paying advances was also postponed and made uniform throughout the country: the last day of the month following the reporting quarter.

ConsultantPlus experts spoke in more detail about changes in the procedure for calculating and paying property taxes. Get free demo access to K+ and go to the review material to learn all aspects of the innovations.

Who is eligible for tax breaks?

Article 358 of the Tax Code of the Russian Federation contains a list of vehicles for which legal entities are not required to pay tax. But regional authorities have the right to establish additional benefits.

For example, in the capital, companies that transport passengers on public transport do not pay the fee. In St. Petersburg, companies that own floating docks pay 50% less tax.

You can find out if there are benefits in your region by contacting the tax office.

When calculating, the amount of the benefit is deducted from the amount of the transport tax. The resulting amount must be paid to the Federal Tax Service.

Is a tax declaration required?

A transport tax return is no longer required . Federal Tax Service employees independently request information from the State Traffic Safety Inspectorate and Rostechnadzor about which equipment is registered to a legal entity. As a reminder, the inspectorate sends the payer a notice of the tax amount.

If a citizen has calculated the fee himself, and his result differs from the Federal Tax Service, he can defend his position if it is correct. You will need to justify the correctness of your independent calculations with documentation. The tax service allows 10 days from the date of receipt of notification of the amount of transport tax.

Article 363.1. Tax return

1. Taxpayers who are organizations, after the expiration of the tax period, submit a tax return on the tax to the tax authority at the location of the vehicles.

2. Lost force on January 1, 2011. — Federal Law of July 27, 2010 N 229-FZ.

3. Tax returns are submitted by taxpayers who are organizations no later than February 1 of the year following the expired tax period.

4. Taxpayers, in accordance with Article 83 of this Code, classified as the largest taxpayers, submit tax returns to the tax authority at the place of registration as the largest taxpayers.