What payments are due upon dismissal?

The Labor Code of the Russian Federation establishes three ways to terminate employment contracts: at the request of the employee, at the initiative of the employer and by agreement of the parties. For each of them, the manager is obliged to transfer the following payments to the resigning person no later than the last working day:

- compensation for unused vacation;

- salary for the period worked.

If the dismissal is due to staff reduction, severance pay is transferred. It may also be provided for by agreement of the parties.

If the dismissed person was in the position of a manager, his deputy or chief accountant, he is also entitled to compensation payments.

How to deal with income tax

It is not always possible to offset compensation amounts as expenses that reduce the taxable base for income tax. Such payments must meet the following conditions:

- These amounts are fixed in the local documents of the institution. For example, they are specified in a collective or labor agreement. Either they are indicated in the additional agreement to the employment contract, or in the agreement on termination of the employment contract itself.

- The amount of compensation must be economically justified and documented.

If it is problematic to meet these conditions, then it is better not to include these expenses. Tax authorities pay special attention to such calculations.

From what payments is personal income tax withheld upon dismissal?

Personal income tax stands for personal income tax. They are subject to most of the payments, including compensation upon dismissal. For residents of the Russian Federation, its value is 13%, for non-residents – 30%.

Compensation for unused vacation is transferred regardless of the reason for the employment contract. Taxation of personal income tax is a priority: only after the tax has been calculated, alimony and other payments are withheld from the amount received.

Personal income tax is also transferred from the following income:

- salary, bonuses, allowances;

- temporary disability benefits.

The employing organization is a tax agent, therefore the obligation to transfer personal income tax rests with it. Violation of this rule is subject to administrative liability in the form of a fine, so it is very important to comply with the deadlines and procedure for calculating the tax.

Filling out the 2-NDFL certificate

Personal income tax is withheld from severance pay in a preferential regime due to the fact that they are compensation payments, the amount and procedure for payment of which is regulated by current legislation, as well as federal and municipal regulations.

Thus, VP that does not exceed 3 times the amount of average earnings in general cases or 6 times the size of the SZ in areas with a “northern” allowance or territories equivalent to them is not reflected in the 2-NDFL certificate (Letter of the Ministry of Finance of Russia No. 03-04 -06/8-118 dated 04/18/2012). Severance pay is indicated in the 2-NDFL certificate if it exceeds the above norms of the Tax Code of the Russian Federation. When filling out the certificate in the VP part, code 4800 “Other income” is used.

Income not subject to taxation

The list of income from which personal income tax is not withheld is determined by Art. 217 Tax Code of the Russian Federation. This includes the following:

- monthly payments in connection with the birth of children;

- compensation for harm to health;

- payment of allowances in kind;

- severance pay not exceeding three times the average monthly salary, for residents of the North - six times the amount;

- daily allowance up to 700 rubles. while on a business trip.

Expert commentary

Kamensky Yuri

Lawyer

Thus, if on the date of dismissal an employee is due to receive compensation for vacation time and severance pay, these payments will not be taxed. If an employee terminates an employment contract during illness, temporary disability benefits are paid no later than 10 days from the date of receipt of sick leave, while the tax is withheld on the day the benefits are transferred and paid to the Federal Tax Service no later than the last day of the month.

In what situations are severance pay paid?

Before finding out the issues of taxation of personnel income, let’s figure out what payments fall under the designation of severance pay. The reason for calculating this payment is the termination of the employment contract:

- something that happened at the initiative of the employer, but does not allow the employee to work in the future. For example, the contract with him was signed contrary to existing legislation, i.e. the employee cannot hold the position due to lack of qualifications, education, medical reasons or a court decision;

- as a consequence of the liquidation of the company or staff reduction;

- due to conscription into the ranks of the Armed Forces;

- due to the employee’s disagreement with being transferred to another location for further work.

We have listed the cases of dismissal established by labor legislation when severance pay must be paid. This list is not closed, therefore, through collective agreements or industry agreements, it can be expanded and supplemented with other, significant from the point of view of the company management, grounds for paying this compensation.

How is compensation for unused vacation calculated?

The minimum duration of annual paid leave for citizens working under employment contracts is 28 calendar days. For some categories of persons, additional days of rest are provided.

How compensation is calculated:

- The number of days of non-vacation is established. To do this, the personnel officer determines the product of the number of days of rest due to the employee for each month worked and subtracts the days already used.

- The resulting number of vacation days is multiplied by the citizen’s average daily earnings.

For example, if a quitter is entitled to 14 days of vacation, and the average daily earnings are 1,500 rubles, the calculation will be carried out as follows: 14 x 1,500 = 21,000 rubles. – the total amount from which personal income tax will be withheld.

21,000 x 13% = 2,730 rub. – personal income tax amount.

21,000 – 2,730 = 18,270 rubles. - the total is in the hands of the employee.

18,270 x 22% = 4,019.4 rubles. – the amount of contribution to the insurance part of the pension paid by the employer.

18,270 x 5.1% = 931.77 rubles. – the amount of payment to the Compulsory Medical Insurance Fund from the employer’s funds.

Amount of compensation provided

To calculate the amount of compensation payment, the following steps are performed:

- The number of vacation days that the employee did not take off is determined. The Labor Code stipulates that he must be compensated for all vacation days, regardless of the length of the period when he was not on vacation (3, 5, 7 years). The standard amount of leave an employee is entitled to in one year is 28 days. For some employees (for example, those working in hazardous industries, without limiting the length of the working day, minors working in the northern regions), additional leaves are provided, also subject to monetary compensation, in case of non-use.

Note. If an employee has not taken vacation for less than a full year, the compensation payment is calculated in proportion to the period worked.

- For example, a worker (who does not have additional preferential leave) has not completed 1 year and 4 months of leave. For each month he is entitled to (28/12) 2.33 vacation days. In total, the employee is accrued CCW for 37 days (2.33 x 4 days + 28).

- If the resigning employee worked for less than half a month, this period is not taken into account.

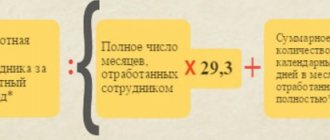

- The average earnings of 1 day are determined for the 12 calendar months worked preceding the payment (periods of temporary disability are excluded) on the basis of Regulation 922.

- The total amount of compensation accrual is determined.

- Calculation of personal income tax and insurance contributions from vacation compensation is carried out.

To simplify the calculation procedure and check it correctly, you can use an electronic calculator from the Internet.

How to withhold personal income tax from compensation upon dismissal: step-by-step instructions

To understand this issue, you must first study the features of the dismissal procedure:

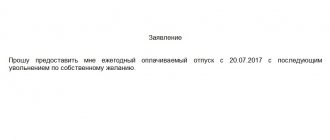

- The employee submits his resignation. If necessary, the employer has the right to assign mandatory work of 2 weeks.

- The manager issues a dismissal order indicating a specific date. The person leaving gets acquainted with it against signature, then the document is transferred to the personnel department and accounting department. It is the accountant who makes all the deductions, but this can only be done if there is a reason - an order.

- The accountant calculates wages, compensation for unused vacation and other payments minus personal income tax, contributions to the Social Insurance Fund and pension contributions.

- On the last working day, the employee is transferred or given cash. He must also be issued with education documents, a salary certificate, 2-NDFL, and information about the status of his personal account with the Pension Fund.

Important! All charges must be reflected in the documentation. The accountant deals with them, and he also draws up the postings.

Results

In the article, we talked about a situation where an employee did not have time to take all the vacation days allotted to him before being fired. In this case, the employer, regardless of the reasons for dismissal, must pay the employee monetary compensation on the day of dismissal. We have indicated all the necessary indicators for calculating compensation upon dismissal for unused vacation and examined them with an example. For violation of payment terms, the employer bears various legally established types of liability - from financial to criminal. In addition, he is obliged to withhold personal income tax on the day of actual payment of compensation upon dismissal, transfer personal income tax to the budget, and also charge insurance premiums for the entire amount of compensation.

Firmmaker, November 2022 (monitor the relevance) Irina Bazyleva When using the material, a link is required

Transfer deadline

The deadline for transferring tax to the budget depends on the method of receiving compensation:

| Cash in the bank | No later than the day of issue |

| To the employee's bank account (non-cash transfer) | No later than the day of transfer |

| Cash from the company's cash desk | No later than the day following the date of issue |

Important! If compensation is paid not upon dismissal, but during the citizen’s work, it must be transferred on payday. Payment according to the Labor Code of the Russian Federation is made every 15 calendar days. If the payment date falls on a weekend, the money must be transferred on the previous weekday.

For example, when an organization pays salaries on the 15th and the date falls on a Sunday, the money must be issued on Friday.

Transfer of funds on the next business day is not allowed, because this will already be considered a delay in wages, and the employer undertakes to pay a penalty for each day of delay.

Calculation and accounting entries

As mentioned earlier, the tax rate on employment contracts for residents of the Russian Federation is 13%. Non-residents are subject to an increased tax of 30%. If citizens have applied for tax deductions or other social benefits, they must be deducted from their salaries, and personal income tax will be withheld from the final amount.

Let's look at practical examples:

A citizen has been working at the company for 3 years. Previously, he received a tax deduction, according to which 1,000 rubles are deducted from the tax amount every month. In May 2022, he decided to quit. The salary for the period worked was 30,000 rubles, compensation for several days of unused vacation was 15,000 rubles. In total, an amount of 45,000 rubles is used to calculate personal income tax and other contributions. How personal income tax is calculated:

45,000 x 13% = 5,850 rub.

After withholding personal income tax, 39,150 rubles remain. Insurance premiums and payments to the Compulsory Medical Insurance Fund must be paid from this amount. They are transferred by the employer from the enterprise budget.

39,150 x 22% = 8,613 rubles. – the amount of contributions to pension insurance.

39,150 x 5.1% = 1,996.65 rubles. – payment to the Compulsory Medical Insurance Fund.

The second example is the payment of state contributions for a non-resident of the Russian Federation:

A foreign citizen works at the enterprise for 2 months, i.e. less than 183 days. This alone does not give him the right to be considered a resident. The decision to resign was made by him in November 2022. He does not yet have the right to leave, so no compensation will be paid. Only wages for the period worked are subject to transfer. In a month, a citizen earned 50,000 rubles. From this money, the employer must withhold 30% of personal income tax - the tax is paid from the employee’s funds. Also, 22% is withheld for the insurance part of the pension, and 5.1% for the Compulsory Medical Insurance Fund. The last two payments are made from the organization's budget.

50,000 x 30% = 15,000 rub.

50,000 – 15,000 = 35,000 rub. – the foreigner finally received it.

35,000 x 22% = 7,700 rub. – transferred by the company towards pension contributions.

35,000 x 5.1% = 1,785 rubles. – the amount of contributions to the Compulsory Medical Insurance Fund.

Accounting entries

In the postings, the accountant reflects all payments as follows:

| DT 44 Kt 70 “F.I.O. employee" | Payroll |

| DT 70 (full name of the employee) Kt 68 Personal Income Tax | Tax withholding |

| DT 70 (full name of employee) Kt 50 (51) | Issuance of wages |

| DT 68 Personal income tax Kt 51 | Transfer of tax to the budget |

Responsibility for non-payment of personal income tax

The employing organization is a tax agent, and the obligation to remit personal income tax rests entirely with it.

The agent's responsibility for untimely transfer is assigned to Art. 123 Tax Code of the Russian Federation. It all depends on the specific situation:

| The tax was withheld from the employee, but was not transferred to the budget | Arrears of 20% of the unpaid amount will be charged. An additional penalty will be charged for each day of delay. |

| The tax is not transferred to the budget and is not withheld | According to the Tax Code of the Russian Federation, personal income tax is always withheld only from employee salaries. Collection of tax from the employer for personnel is not allowed (clause 9 of Article 226 of the Tax Code of the Russian Federation). If the arrears cannot be recovered, no penalty will be charged. |

How much do they pay?

VP is paid to employees in the amount of two weeks SZ upon termination of an employment contract in the following situations:

- if you do not want to be transferred to another workplace based on medical indications;

- when conscripted for military service;

- in case of refusal to move to another area together with the employer;

- with complete inability to work, confirmed by medical reports;

- in case of a significant deviation of the new terms of the employment contract from the previous ones and refusal to continue working.

When compensation is not taxable

In all cases, compensation for unused vacation is subject to taxation. The exception is when relatives of a deceased employee apply for it: in such a situation, there is no need to withhold personal income tax.

To receive compensation and other salary payments for a deceased relative, you must do the following:

- Guided by Art. 141 of the Labor Code of the Russian Federation, according to which relatives of the deceased employee are entitled to payments, draw up an application and collect the necessary package of documents for the employer. This must be done within 4 months from the date of death of the citizen.

- Submit a package of documentation to the organization. Money must be transferred no later than 1 week from the date of application.

Along with the application, the employer is provided with a death certificate, passport and a document confirming the relationship of the citizen with the deceased employee.

Important! If wages are paid into staff bank accounts, the employer must not transfer funds upon learning of the employee's death, otherwise it will no longer be considered a legal payment. The money must be given to close relatives. If they do not apply within 4 months, the amount is included in the inheritance mass, and only the heirs can apply for it after six months.

In addition to compensation for unpaid vacation, the employer must give relatives the amount of salary for the period worked, as well as other payments due to the employee during his lifetime. There are no taxes or insurance contributions, since a citizen’s tax obligations cease due to death.

Compensation for unused vacation and other payments upon dismissal are subject to personal income tax without fail, with the exception of the death of the employee: in this case, his relatives receive the amount without withholding tax.

If personal income tax is not paid on time, the tax agent may oblige the Federal Tax Service to pay arrears and penalties, so it is very important to comply with the deadlines for the transfer and know the specifics of accounting entries.

Taxation of personal income tax on severance pay upon dismissal by agreement of the parties

The legal uncertainty that arises at the intersection of the branches of labor and tax law in the issue of withholding personal income tax from the amount of severance pay (compensation payment) upon dismissal by agreement of the parties is considered. It seems that during a crisis, this problem has not only legal, but also social significance, since it affects the rights and legitimate interests of such a category as dismissed workers.

Let us give two examples of clauses in additional agreements to the employment contract concerning the conditions for withholding personal income tax from severance pay (compensation payment).

Extract from the additional agreement.

Extract from the additional agreement.

The agreements were drawn up by companies that are approximately equivalent in the market with the same category of workers. At first glance, the only difference is in the more explicit wording regarding the withheld personal income tax of company A, although both agreements contain references to current Russian legislation.

But it turned out that company B withholds the entire amount of personal income tax from the severance pay.

To explain its position, Company B provided the following conclusion: “We believe that, taking into account the ambiguous position of the Ministry of Finance, if the employer applies the provisions of clause 3 of Art. 217 of the Tax Code of the Russian Federation to payments that are made upon termination of an employment contract by agreement of the parties, there is a high risk of claims from the tax authorities and, as a result, there is a high probability that the taxpayer will have to prove the legitimacy of his position in court, the result of which is currently difficult to predict.” The conclusion was given in 2022; at that time there was truly contradictory practice on this issue.

In 2022, the Ruling of the Supreme Court of the Russian Federation dated June 16, 2017 N 307-KG16-19781 appeared, which, it would seem, should have put an end to it. In the case under consideration based on the results of an on-site tax audit in relation to PJSC “Murmansk Trawling Fleet” (hereinafter referred to as the “Company”), the Interdistrict Inspectorate of the Federal Tax Service of the Murmansk Region, in its act, among other things, proposed to transfer to the budget 393,838 rubles of unwithheld personal income tax as a result of dismissals by agreement of the parties. The company filed a claim, the court of first instance supported the conclusions of the tax inspectorate, but the Thirteenth Arbitration Court of Appeal did not agree with the indicated position of the court of first instance, based on the fact that the Labor Code of the Russian Federation does not contain a prohibition on establishing in an employment or collective agreement the size and conditions for payment of severance pay, paragraph 3 of Article 217 of the Tax Code of the Russian Federation applies regardless of the grounds for dismissal and the position held by the employee. The cassation court, in turn, did not agree with this, which considered that paragraph 3 of Article 217 of the Tax Code of the Russian Federation provides for exemption from taxation only for those payments that are established by law, which does not include dismissal by agreement of the parties.

The ruling of the Supreme Court of the Russian Federation contained the following provisions: “According to paragraph 1 of Article 3 of the Tax Code, legislation on taxes and fees is based on the recognition of the universality and equality of taxation. When establishing taxes, the actual ability of the taxpayer to pay the tax is taken into account.<..> As the Constitutional Court of the Russian Federation has repeatedly noted, in taxation equality is understood primarily as the uniformity, neutrality and fairness of taxation. Taxpayers, especially if they are personal income tax payers, with equal solvency must bear an equal burden of taxation: ensuring informal equality of citizens requires taking into account the actual ability of a citizen (depending on his earnings, income) to pay public legal mandatory payments in the appropriate amount (resolutions of 30.11. 2016 N 27-P, dated 03/13/2008 N 5-P and dated 02/24/1998 N 7-P). Therefore, the interpretation of the provisions of Chapter 23 of the Tax Code should not lead to the imposition of an arbitrary tax burden on individuals who belong to the same category of taxpayers, including taking into account their equal actual ability to pay tax when receiving the corresponding income<..> Severance pay as a separate type of compensation in the sphere of labor is established by law (Article 178 of the Labor Code) and performs the social function of protecting the employee from temporary loss of income upon dismissal <..> The need for this protection is not excluded when using the grounds for termination of employment relations provided for in Article 78 of the Labor Code (termination of employment agreement by agreement of the parties), presupposing the will of the employer to dismiss the employee and, as a rule, leaving for the dismissed person a limited opportunity to agree on the terms of termination of the employment contract.”

However, after such premises, the Supreme Court makes a conclusion, the ambiguous legal technique of which, as it later turned out, did not remove legal uncertainty from judicial practice: “Consequently, the determination of specific cases of payment of severance pay as a result of an agreement reached between the employer and the employee does not exclude these compensatory payments are within the scope of legislative establishment and, taking into account the provisions of paragraph 1 of Article 3 of the Tax Code, does not mean that these compensations are not subject to the tax exemption provided for in paragraph 3 of Article 217 of the Tax Code for such a category of taxpayers as dismissed employees.”

The Federal Tax Service spoke out more definitely and sent a letter dated June 29, 2017 N SA-4-7/ [email protected] , where, referring to the decision of the Supreme Court, it writes: “One-time payments made in favor of employees upon termination of employment contracts by agreement of the parties , paid within the limits established by paragraph 3 of Article 217 of the Tax Code of the Russian Federation, are not subject to personal income tax.”

After this, in general, court decisions began to be made in favor of workers. Courts began to directly or indirectly refer to the decision of the Supreme Court, for example:

- Decision of the Shchelkovo City Court of the Moscow Region dated July 19, 2017 in case No. 2-2452/2017 ~ M-1700/2017: “In this regard, the interpretation of the norms of Chapter 23 of the Tax Code of the Russian Federation, including the provisions of Article 217 of the Tax Code of the Russian Federation, should not lead to the imposition arbitrary tax burden on individuals who belong to the same category of taxpayers, including taking into account their equal actual ability to pay tax when receiving the corresponding income. This conclusion corresponds to the position of the Supreme Court of the Russian Federation, set out in Determination No. 307-KG16-19781 dated June 16, 2017 in case A42-7562/2015.”

- Determination of the Supreme Court of the Republic of Tatarstan dated October 22, 2018 in case No. 33-15544/2018: “...payment of severance pay as a result of an agreement reached between the employer and employee does not exclude these compensation payments from the scope of legislative establishment and, taking into account the provisions of paragraph 1 of Article 3 of the Tax Code of the Russian Federation does not mean that these compensations are not subject to the tax exemption provided for in paragraph 3 of Article 217 of this Code for such a category of taxpayers as employees dismissed on appropriate grounds.”

The position of the Moscow City Court deserves attention. Already a month after the ruling of the Supreme Court of the Russian Federation, all decisions began to be made against employees demanding that personal income tax be deducted in accordance with clause 3. Article 217 of the Tax Code of the Russian Federation:

- Appeal ruling of the Moscow City Court dated July 14, 2017 in case No. 33-26760/2017;

- Appeal ruling of the Moscow City Court dated November 22, 2017 in case No. 33-47163/2017;

- Appeal ruling of the Moscow City Court dated May 14, 2018 in case No. 33-17194/2018;

- Appeal ruling of the Moscow City Court dated January 30, 2018 in case No. 33-3840/2018;

- Appeal ruling of the Moscow City Court dated February 20, 2019 N 33-5979/2019;

- Appeal ruling of the Moscow City Court dated May 10, 2018 in case No. 33-8807/2018.

The conclusion is again used that dismissal by agreement of the parties is not provided as a basis for payment of severance pay, and the provisions of Art. 217 of the Tax Code do not provide for employment contracts and additional agreements thereto as grounds for tax exemption.

In terms of the opposite position, the conclusion of the Belgorod court, which directly rejected the plaintiff’s reference to the decision of the Supreme Court, is interesting. The decision of the Oktyabrsky District Court of Belgorod dated January 18, 2017 in case No. 2-226/2018 reads: “The plaintiff’s reference to the position of the Supreme Court of the Russian Federation in the Ruling dated June 16, 2017 No. 307 KG16-19781 in case No. A42-7562/2015 is not justified. Indeed, when using the grounds for termination of employment relations provided for in clause 1, part 1 of article 77 and article 78 of the Labor Code of the Russian Federation (termination of an employment contract by agreement of the parties), it is not excluded by law from exempting the dismissed employee from taxation paid on the amount of severance pay, on the basis of paragraph 3 of article 217 Tax Code of the Russian Federation. At the same time, severance pay upon dismissal must be provided for in collective or labor agreements, which equates it to payments established by the legislation of the Russian Federation.”

There is an opinion that if the collective (employment) agreement does not contain an explicit provision that severance pay is not subject to personal income tax in the amount specified in clause 3. Article 217 of the Tax Code (example of the agreement of company A), then the courts lawfully rule in favor of the employers.

But this raises objections based on the following arguments:

- The Tax Code of the Russian Federation, Article 3 defines: “..2. It is not allowed to establish differentiated rates of taxes and fees, tax benefits depending on the form of ownership, citizenship of individuals or place of origin of capital.

<…> 6. All irremovable doubts, contradictions and ambiguities in acts of legislation on taxes and fees are interpreted in favor of the taxpayer (fee payer, insurance premium payer, tax agent).

- It seems strange that subjects of the same category of workers (with the same labor relations, grounds for dismissal, etc.) can pay different taxes, depending on the “terms of a collective or labor agreement,” which, in principle, do not relate to public law. It turns out that contractual provisions (using the example of company A) can change the mandatory rules of tax legislation?

In conclusion, two solutions can be given:

1) Appeal ruling of the Moscow Regional Court dated November 1, 2017 in case No. 33-33572/2017

2) Appeal ruling of the Moscow City Court dated January 30, 2018 in case No. 33-3840/2018

In both cases, there is one defendant, one subject of the claim - the withholding of excess personal income tax from severance pay (compensation payment) upon dismissal by agreement of the parties. At the same time, directly opposite court decisions were made, which confirms the legal uncertainty in the issue under consideration, which exists even after the decision of the Supreme Court.