When do unearned vacation pay appear?

The following example will help you understand the mechanism by which unearned vacation pay appears.

Technical University graduate P. N. Ptichkin got a job at a helicopter plant on July 1, 2020, and in January 2022 he received the right to go on vacation (paragraph 2 of Article 122 of the Labor Code of the Russian Federation) and took advantage of this opportunity. The duration of his vacation was 28 calendar days (Article 115 of the Labor Code of the Russian Federation).

Find out more about the provision of leave and its duration from the article “Annual paid leave under the Labor Code (nuances).”

During his vacation, he received a more lucrative job offer and immediately after returning from vacation, he quit the plant.

Thus, by the time of his dismissal, P.N. Ptichkin had earned only half of his legal leave: 14 days (6 months × 28 days / 12 months), and used all 28 days. There were 14 vacation days unworked at the time of dismissal (28 – 14).

Since the employee received the full amount of vacation pay before going on vacation, by the time of dismissal he had a debt to the company for the 14 days of vacation paid in advance.

IMPORTANT! The right to vacation for the first working year arises after six months of work in the organization (Article 122 of the Labor Code of the Russian Federation). Subsequent vacations are issued according to the approved schedule.

What the lack of a vacation schedule in a company can lead to, see the material “Unified Form No. T-7 - Vacation Schedule” .

"Vacation" rights and obligations

Upon termination of the employment relationship, the employer must perform many mandatory actions regulated by labor legislation. Among them is the obligation to give the employee everything he earned by the time of dismissal.

Vacation payments are one of the elements of the final settlement with a resigning employee. Their composition depends on how many vacation days have been accumulated and whether the employee has exercised his right to vacation in the current period (Article 127 of the Labor Code of the Russian Federation).

For information on the circumstances affecting the calculation of vacation days upon termination of an employment contract, see the material “How to calculate the number of vacation days upon dismissal?” .

In addition to this obligation, the employer has the right to withhold from the resigning employee’s income the amount of advance vacation pay (Article 137 of the Labor Code of the Russian Federation).

This right may not be exercised in all cases. If the dismissal of an employee occurs on the grounds listed in Art. 137 of the Labor Code of the Russian Federation, it will not be possible to withhold overpaid vacation pay from him. For example, such a prohibition on retention applies to the situation of dismissal due to staff reduction or closure of a company, as well as in other cases provided for by law.

Find out how the latest judicial practice on this issue is shaping up from the analytical collection from ConsultantPlus. Get trial access to the system and access the material for free.

In addition, the employer can deal with the employee’s debt in a different way. We'll talk about this in the next section.

Find out how to calculate the number of vacation days in 2022 from this publication.

Vacation followed by dismissal: when to pay

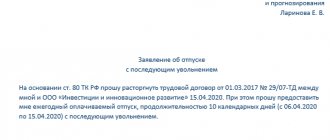

When an employee wants to resign under such conditions, the employer must be guided by the provisions of Art.

127 of the Labor Code of the Russian Federation and some regulations (listed below). Firstly, this request must be formalized in a written statement from the employee, for example this one.

Secondly, the deadlines for settlements with the employee must be met. In our case, the day of dismissal will be the last day of rest. Therefore, calculations must be made before going on vacation, because... upon its completion, the obligations of the parties will cease to be valid.

Documents are transferred in the same order: a work book and some other documents (for example, a pay slip, a 2-NDFL certificate, a certificate of form 182n, an extract from the SZV-STAZH form, etc.), which the employer is obliged to issue to the employee on the last day of work .

IMPORTANT!

The most important points are calculating the amount of vacation pay and calculating vacation days upon dismissal; the online calculator on our website will help you avoid mistakes. You can use it completely free.

Is it possible to do without deductions?

You can avoid deductions by signing a debt forgiveness agreement. Forgiving an employee’s debt means not raising the issue of the existence of a debt and not demanding its repayment.

In everyday life, settling a debt between individuals through forgiveness does not entail any consequences for both parties to the transaction. In a situation where one of the parties is a legal entity, debt forgiveness entails additional paperwork and also requires adjustment of tax obligations.

At the beginning of the procedure for forgiveness of vacation debt, you will need to draw up a document that reflects the will of the parties to repay the debt. Such a document may be an agreement on debt forgiveness for vacation overpayment.

The preparation of such a document is similar to similar agreements drawn up in the normal course of business. After the title of the document, the date and place of its preparation are indicated, followed by the parties to the agreement and its main text. It may contain the following content:

“...The employer exempts the employee from repaying the debt for 14 unworked vacation days in the amount of 10,025 (ten thousand twenty-five) rubles, which arose in connection with his dismissal under clause 3, part 1, art. 77 of the Labor Code of the Russian Federation until the end of the working year, towards which he used annual paid leave...”

The final elements of the agreement are the details and signatures of the parties.

Read about the next steps of debt forgiveness for unearned vacation pay in the next section.

Deduction for unworked vacation days: cases and sizes

Providing leave in advance, that is, for the working year that the employee has not yet worked, is a common practice. However, it is somewhat risky. An employee can receive vacation pay, take vacations that have not yet been “earned,” and then decide... to quit. And the employer will inevitably face the question: can he withhold vacation pay for unworked days of vacation? Let's figure out in what cases and to what extent this is possible.

In what cases is vacation considered advanced?

As a rule, labor leave is granted for work during each working year (annually) <1>. The working year for which labor leave is granted is a period of time equal in length to a calendar year. Only it is calculated not from January 1, but from the date of hiring <2>. Thus, the employee has the right to vacation from the first day of work.

In a situation where leave is granted to an employee before the end of the full working year, it is advanced .

Note! A full working year is equal to 12 months minus the total duration of leave to which the employee is entitled <3>.

If leave is granted from the date from which the full working year is worked, then in this case it will be granted for time worked.

Example An employee was hired on October 24, 2016. Labor leave is granted to him for the working year 10/24/2016 - 10/23/2017. A full working year, taking into account 24 calendar days of labor leave to which the employee is entitled, will be considered worked from September 30, 2017. Situation 1. The employee went on vacation on July 17, 2017. In this case, the vacation is advanced. Situation 2. The employee plans to go on vacation on October 2, 2017. In such a situation, leave is granted for a full working year worked.

When can you make a hold and when can you not?

If an employee is dismissed before the end of the working year, for which he has already used vacation, the employer can make a deduction for unworked vacation days <4>. However, not every reason for dismissal allows this. In other words, if an employment contract is terminated for a number of reasons, the employer does not have the right to withhold vacation pay from the employee’s final payment for the vacation provided in advance . Cases when this cannot be done are clearly listed in clause 2, part 2, art. 107 TK. Let's look at some of them.

Thus, the employer does not have the right to withhold vacation pay upon termination of the employment contract by agreement of the parties . At the same time, the norm is clause 2, part 2, art. 107 of the Labor Code provides a reference to Art. 37 of the Labor Code, which determines the procedure for dismissal on this basis. The very basis is contained in clause 1, part 2, art. 35 TK. In this regard, employers often withhold vacation pay, since, in their opinion, the basis for dismissal is precisely clause 1, part 2, art. 35 of the Labor Code, which in clause 2, part 2, art. 107 TC is not named. This is erroneous. When dismissing an employee by agreement of the parties, it is impossible to deduct for unworked days of labor leave provided in advance.

As a general rule, when terminating an employment contract at the request of the employee , a deduction can be made from the employee’s final payment . However, in this case there is one “but”. It depends on the reasons for dismissal. Thus, the legislation provides the right to an employee, in the presence of circumstances that exclude or significantly complicate the continuation of work (health status, retirement age, radioactive contamination of the territory and other cases), to terminate the employment contract for an indefinite period within the period specified in the employee’s application <6>. The list of circumstances that exclude or significantly complicate the continuation of work is not exhaustive . Therefore, these include obtaining education in the direction of the employer and retirement. But if an employee is dismissed at his request, in these cases it is impossible to withhold vacation pay for unworked vacation.

Example A month after reaching retirement age, an employee turned to the employer with a request to terminate an employment contract concluded for an indefinite period, at his request. In a statement sent to the employer, he indicated the reason for the termination of the employment relationship: “In connection with retirement.” In this case, the deduction of vacation pay for days of labor leave provided in advance is not made.

We will separately mention cases when an employee, although dismissed on grounds that allow the employer to make a deduction, but the latter does not have the right to do this. So, no hold is made if <7>:

— upon dismissal, the employee is not accrued any payments;

- the employer, having the right to do so, did not deduct when paying the settlement or withheld only part of the employee’s debt.

Thus, in all other cases, the employer has the right to make a deduction by issuing an appropriate administrative document.

Note! Deductions for unworked but used days of labor leave are made during the final calculation from the amount of wages due to the employee. It is not allowed to make deductions from the amounts of severance pay, compensation and other payments that, according to the law, cannot be recovered <8>.

The number of days for which deduction should be made is calculated in the same manner as the duration of labor leave, granted in proportion to the time worked <9>.

How much should I keep?

As a general rule, the amount of withholding cannot exceed 20 percent of the wages due for payment <10>. At the same time, the legislation does not contain a direct indication of whether it applies in the case under consideration. In this regard, the opinions of experts differ.

Some of them believe that in relation to a situation where, upon dismissal of an employee, unearned vacation pay is withheld, this provision does not apply. They proceed from a literal reading of the norm and argue their position as follows. In this situation, we are not talking about the payment of regular wages, but about the final settlement. Consequently, the employer has the right to withhold the full amount of the employee’s vacation pay debt. Even if this amount is more than 20 percent of the salary paid to the employee upon dismissal.

A number of experts, whose point of view we share, believe that the 20 percent limit applies in the case under consideration . It seems that it was introduced by the legislator to protect the interests of the employee and is, to a certain extent, a guarantee that the employee will be paid a certain minimum amount of money that will allow him to satisfy his basic life needs. At the same time, employers should keep in mind that in this case it will not always be possible to retain the full amount of vacation pay arrears for unworked days of vacation.

Example request of an employee, the employment relationship with him is terminated due to moving to another country <11>. He is due 700 rubles. wages for the period worked before dismissal. The employer decided to withhold from this amount the average earnings for 6 calendar days of unworked vacation. According to the calculation, the employee’s debt is 150 rubles. The employer made a deduction for unworked vacation days in the amount of 140 rubles. (RUB 700 x 20 percent).

In any case, we recommend that employers withhold no more than 20 percent of the amounts due. Otherwise, exceeding this limit may be regarded by inspection authorities as a violation of labor laws.

Note! Deduction for unworked days of vacation provided in advance is made on the basis of the average daily earnings calculated when the employee goes on vacation, and not at the time of his dismissal <12>. There is no need to make a new calculation of average earnings in such a situation.

Example In August 2022, an employee was granted leave for the working year from 01/09/2017 to 01/08/2018 . In October 2022, the employee quits. The amount of average earnings for days of unworked vacation is determined based on the average daily earnings calculated when vacation was granted in August 2022.

In accordance with the law, it is possible to recover from an employee only wages that were overpaid as a result of a counting error <13>. In other cases, including incorrect application of the law, its collection is not allowed.

| An example from judicial practice The plaintiff filed a claim with the court to recover from the former employee the amount of overpaid wages, which, as a result of an error, was paid to him twice. From the case materials, it appears that upon dismissal, the defendant was transferred the final payment amount, including wages for the month worked before dismissal. When creating the payroll statement, the accountant re-included in it the amount of wages, which was subsequently also transferred to the defendant. Under such circumstances, the court came to the conclusion that the accrual and payment of an excess amount of money to the defendant did not occur as a result of a calculation error, but as a result of the accountant’s negligence in preparing the wage payment sheet. The plaintiff's claim was denied, since there were no grounds for collecting the excess amounts received by the defendant. Absentee decision of the district court dated April 28, 2017 Determination of the judicial panel for civil cases of the regional court from 06/19/2017 |

According to the norms of civil law, excess wages received by an employee is unjust enrichment <14>. At the same time, it and payments equivalent to it are not subject to return <15>. But only if, as we noted above, there is no accounting error, as well as dishonesty on the part of the recipient of this amount.

If we talk about withholding vacation pay for unworked days of vacation, then it is hardly possible to convict the employee of dishonesty in this case. After all, it is the employer who makes the deduction. And if he did not do this or withheld the debt partially, the employee is not to blame.

Thus, if the employer, having the right to withhold for unworked days of labor leave, did not make it during the final payment or withheld the amount of the debt in part, then further collection, including through the court, is impossible.

The same applies to the situation when:

- at the final settlement, the employer withheld only 20 percent of the payments due to the employee, which did not cover the amount of the employee’s debt for unworked days of leave;

— upon dismissal, the employee was not accrued any payments.

Subsequently, collection of the remaining amount of debt through court proceedings is not carried out.

Tax nuances of vacation advance forgiveness

The debt forgiveness agreement signed by the parties automatically triggers the tax adjustments associated with this event.

For the employee, recalculation of tax obligations does not lead to material losses - the tax on his income in the form of a forgiven debt has already been withheld when he was paid vacation pay. Changing the status of the amount received from vacation pay to a bonus from the employer (debt forgiveness) does not have an impact on personal income tax obligations.

What to do with personal income tax if an employee voluntarily repays the debt on advance vacation pay, see the material “Personal income tax on unearned vacation pay is subject to return .

The employer's situation is different. In connection with the “act of goodwill” in relation to the employee, the income tax will have to be recalculated. In this case, it becomes necessary to exclude from expenses the amount of unearned vacation pay (clause 1 of Article 252, clause 49 of Article 270 of the Tax Code of the Russian Federation). Tax officials consider such expenses to be economically unjustified (letter from the Federal Tax Service for the city of Moscow dated June 30, 2008 No. 20-12/061148).

With regard to the amount of unearned vacation insurance premiums accrued, it should be noted that there are no grounds for their recalculation - they were accrued within the framework of the labor relationship. The legality of their inclusion in tax expenses is not disputed by officials of the Ministry of Finance (letter dated April 23, 2010 No. 03-03-05/85).

Methodology for calculating advance vacation pay

If the employer is not inclined to be generous and forgive the employee unearned amounts, the accounting department will have to work hard. The algorithm for their calculation includes the following steps:

- determining the number of unworked vacation days;

- clarification of information about average daily earnings;

- calculation of the amount of advance vacation pay.

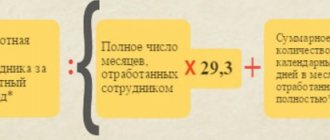

Determine the number of days of unworked vacation. For calculation we use the formula:

KDno = KDio – [KD o / 12 months. × KM],

Where:

KDno and KDio - the number of vacation days, unworked and used, respectively;

KD o - duration of the next vacation;

KM - the number of months of work at this enterprise.

For example, during his work, an employee of the company did not use part of his vacations in full, but in the working year before his dismissal, his vacation was in full accordance with the vacation schedule. As a result, at the time of his dismissal, he had “two-way” vacation pay: not paid off for the previous period (15 days) and advance pay for the unfinished current year (10 days). In this situation, the employer, instead of deducting for unworked vacation days, is obliged to give the employee compensation for unused days.

If the employee had not had incompletely used vacations in previous periods, then, based on the results of this calculation stage, the number of unworked vacation days would be 10, and to calculate advance vacation pay, the accountant would have to proceed to the next step of the calculation algorithm.

We clarify information about earnings and calculate unearned vacation pay.

This stage is associated not only with calculations, but also with clarifying the available information. The accountant will have to provide information about the average daily earnings, based on which the employee was paid for vacation days. This indicator has already been calculated earlier (before the employee went on vacation).

The amount of vacation pay for the unworked vacation period (∑Ond) is calculated based on the number of days of unworked vacation (KDno) and average daily earnings (AS) according to the formula:

∑Ond = KDno× SZ.

Additional adjustments will be needed if, during the employee’s rest period, all employees of the company received a salary increase. The date of this event is of particular importance - the vacation period is calculated from it, the payment for which will have to be adjusted by an increasing factor.

The sequence of actions in this situation is as follows: unworked days are counted from the end date of the vacation, and it is determined how many days fall in the time period after the salary increase (and how many before this event). The average daily earnings for these periods will be different due to the application of the adjustment factor.

The amount of unearned vacation pay will be calculated using a complicated formula:

∑Ond = KD0× SZ0 + KD1× SZ1,

Where:

KD0 and KD1 - unworked vacation days before and after the salary increase;

SZ0 and SZ1 are the average daily earnings, calculated for vacation pay and increased by a factor, respectively.

What to do if an employee decides to resign of his own free will during his next vacation? How to make a payment upon dismissal? Is it possible to withhold paid vacation pay? The answers to these and other questions are considered in detail by ConsultantPlus experts. Get trial access to the system and study the ready-made solution for free.

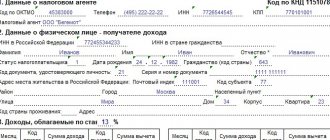

Withholding personal income tax upon dismissal

There is no special rule in the Tax Code for determining the tax base for personal income tax if previously accrued vacation pay, on which tax has already been paid, is subsequently withheld from payments upon dismissal. Therefore, there are different opinions on how the employer (tax agent for personal income tax) should act. He can:

- reduce the tax base for personal income tax by the amount of vacation pay for unworked vacation days. Then he will have an overpayment of personal income tax;

- do not reduce the tax base for personal income tax, since deductions are made from amounts paid minus personal income tax.

In a normal situation, when payments exceed the amount of withholding, it is easier for the employer not to reflect the debt to the employee for the return of personal income tax, but to immediately calculate the tax on the amount of payments taking into account the withholding.

Example of calculating advance holiday pay

The manager of Breeze LLC, R. N. Gavrilov, is resigning, having used the standard vacation duration (28 days) this year. At the time of the severance of the employment relationship with the employee, the accountant of Breeze LLC had the following information:

- number of vacation days received in advance from the employer - 12;

- Average daily earnings for calculating vacation pay are 1,120 rubles.

Additional terms:

- while the employee was on vacation, the company increased salaries - the increase occurred on May 20 and affected the entire work team;

- R.N. Gavrilov’s vacation ended on May 30;

- the employee’s salary before and after the increase was 25,000 and 28,000 rubles. respectively.

The accounting specialist began the calculation by determining the unworked vacation days falling during the period after the salary increase. Of the 12 advanced vacation days, the period after the increase accounted for 11 days (from May 20 to 30); unworked rest days, paid without taking into account the increasing factor, accounted for 1 day (12 - 11).

The accountant made the following calculation using the formula from the previous section:

∑Ond = 1 day × 1,120 rub. + 11 days × [RUB 1,120 × (28,000 rub. / 25,000 rub.)] = 14,918.40 rub.

At the time of R.N. Gavrilov’s dismissal, this amount amounted to his debt to the employer as received, but not worked out.

We will tell you in the next section how much of this debt will be returned to the employer.

For information about how leave policies may change, see here.

Deduction for used vacation upon dismissal

The amount of vacation pay not worked by the employee and the amount that can be withheld from his income obtained as a result of the calculation do not always coincide.

IMPORTANT! The amount of deductions is limited by law (Article 138 of the Labor Code of the Russian Federation) and amounts to 20% of the income received by the employee. In some cases, it is allowed to exceed the established limit to an amount not exceeding half of the income received.

It should be taken into account that in addition to advance vacation pay, the employee may have other obligations (under writs of execution, in connection with compensation for damage, etc.). Then they, together with advance vacation pay, should not exceed the specified limit on the amount of deduction.

The accountant needs to find out what part of the calculated amount of unearned vacation pay can be deducted from the employee’s income. If he has no other deductions, and the amount of vacation pay received in advance is less than 1/5 of the amount received upon dismissal, no problems arise - the advanced vacation pay can be withheld in full.

If established by Art. 138 of the Labor Code of the Russian Federation, the restriction does not allow the employer to reimburse the full specified amount, you can try to do the following:

- ask the employee to voluntarily repay the remaining balance of the debt;

- apply to the judicial authorities to resolve the issue of collection (Articles 382-383 of the Labor Code of the Russian Federation);

- forgive the balance of the debt.

Each of these methods has its own nuances. For example, voluntary repayment of debt entails recalculation of personal income tax, and forgiveness of debt leads to adjustment of income tax obligations.

The judicial way of resolving the issue, as practice shows, is not always in favor of the employer. For example, in the appeal ruling of the Supreme Court of the Republic of Karelia dated January 11, 2013 No. 33-111/2013, the court defended the interests of the employer, and in the ruling of the Presidium of the Rostov Regional Court dated September 15, 2011 No. 44g-109 on a similar issue, the opposite point of view was expressed.

Find out what the Labor Code of the Russian Federation establishes regarding deductions from wages from this article.

Refund of vacation pay upon dismissal: fiction or the employee’s obligation?

For work we will need: - Labor Code of the Russian Federation; — Determination of the Supreme Court of the Russian Federation dated August 29, 2014 No. 70-KG14-4.

Sometimes we are faced with a situation where, when leaving a job, the employer demands a refund. For example, when an employee used his vacation in full, but did not work the full working year. Should the employee run to the bank and pay this debt or not?

Paragraph 5 hours 2 tbsp. 137 of the Labor Code of the Russian Federation establishes that deductions from an employee’s salary to pay off his debt to the employer can be made when the employee is dismissed before the end of the working year for which he has already received annual paid leave for unworked vacation days.

It is possible to withhold money from wages, but in a situation where the employer must pay the employee some part of his wages. But if the employee has already received a salary for all the time he worked and the employer does not owe him anything, then it is impossible to demand the return of overpaid amounts.

In accordance with Part 1 of Art. 138 of the Labor Code of the Russian Federation, the total amount of all deductions for each payment of wages cannot exceed 20 percent.

For example: an employee received a full vacation in advance, took it off, and upon leaving the vacation wrote a letter of resignation. The amount of overpaid vacation pay is RUB 60,000. The employer accrued wages for the two weeks worked in the amount of 50,000 rubles. When dismissing an employee, the employer has the right to withhold only 20% of RUB 50,000. Thus, the amount to be paid will be 40,000 rubles. (50,000 – 10,000). Deduction from salary of more than 10,000 rubles. will be a violation of the Labor Code of the Russian Federation.

Thus, the employee still owes another 50,000 rubles, which the employer will not recover in court. According to Part 4 of Art. 137 of the Labor Code of the Russian Federation: wages overpaid to an employee (including in the event of incorrect application of labor legislation or other regulatory legal acts containing labor law norms) cannot be recovered from him, except for the following cases: - counting error; — if the body for the consideration of individual labor disputes recognizes the employee’s guilt in failure to comply with labor standards; if the wages were overpaid to the employee in connection with his unlawful actions established by the court.

There are no other grounds for collecting money from an employee in court.

Receiving vacation in advance and, as a consequence, vacation pay in full is not a calculation error, and therefore the court will refuse the employer to collect funds from the employee.

Arbitrage practice

1. Review of the judicial practice of the Supreme Court of the Russian Federation for the third quarter of 2013: “...If an employee is dismissed before the end of the working year, for which he has already received annual paid leave, the debt for unworked vacation days is not subject to recovery in court, including if, during the calculation, the employer was unable to deduct this amount from the wages due for payment due to its insufficiency...”;

2. Determination of the Supreme Court of the Russian Federation dated August 29, 2014 No. 70-KG14-4: “... Thus, the norms of international, labor and civil law do not contain grounds for collecting the amount of debt in court from an employee who used vacation in advance if the employer in fact, during the calculation, I was unable to make a deduction for unworked vacation days due to the insufficiency of the amounts due during the calculation...”;

3. Determination of the Judicial Collegium for Civil Cases of the Supreme Court of the Russian Federation dated March 14, 2014 No. 19-KG13-18: “... The legal norms provided for in Article 137 of the Labor Code of the Russian Federation, Article 1109 of the Civil Code of the Russian Federation are consistent with the provisions of the International Labor Organization Convention of July 1 1949 No. 95 “Regarding the protection of wages” (Article 8), Article 1 of Protocol No. 1 to the Convention for the Protection of Human Rights and Fundamental Freedoms, mandatory for application by virtue of Part 4 of Article 15 of the Constitution of the Russian Federation, Article 10 of the Labor Code of the Russian Federation, and contain an exhaustive list of cases when it is permissible to recover overpaid wages from an employee.

Thus, the current legislation does not contain grounds for collecting the amount of debt in court from an employee who used vacation in advance, if the employer, in fact, during the calculation, was unable to make a deduction for unworked vacation days due to the insufficiency of the amounts due during the calculation...”

Source: Education Ombudsman

Subscribe to the author's channel about the legal aspects of education. Author - Ivan Platonov

Results

Deduction for unworked vacation upon dismissal is made from the final payment amounts received by the employee. In certain legally established cases, such deductions are not permitted or limited.

Sources:

- Tax Code of the Russian Federation

- Labor Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

If the salary is not enough

What if the employer did not withhold everything from the former employee? For example, at the time of his dismissal he was not entitled to a salary. Will he be able to recover the balance in court ? Most likely no. This conclusion follows from the ruling of the Judicial Collegium for Civil Cases of the Supreme Court of the Russian Federation dated 02/05/2018 No. 59-KG17-19.

The bottom line is this: the employer (department of the Ministry of Internal Affairs) could not withhold payment from the employee for unworked vacation, since at the time of dismissal she was not owed any payments . The woman did not want to voluntarily compensate for the excess, and the employer filed a lawsuit.

The first and second instances sided with the organization, but the Supreme Court supported the employee. The judges simply did not find legal grounds that would allow judicial collection of the debt under such circumstances.

That is, simply because the amount of payment upon dismissal turned out to be less than the debt, it will not be possible to collect the balance through the court. The only thing left for the employer in this case is to offer the employee to repay the debt voluntarily.