Taxation of personal income tax for pregnancy benefits

The list of payments subject to personal income tax is listed in Article 217 of the Tax Code of the Russian Federation. However, even if the payment is not mentioned in this article, but it is expressed in cash and entails a material benefit for the employee, tax is paid on it. Also, funds issued to the worker must be mentioned in the 2-NDFL certificate.

So what about maternity benefits (M&B)? Previously, it was believed that it should be subject to personal income tax, since it is a woman’s income. However, a significant amendment has now been made to the Tax Code of the Russian Federation, according to which state compensation (which includes benefits) is exempt from taxation. Legislators claim that the development of the amendment was due to discrepancies and contradictions in the reading of the law. It was not clear whether the benefits counted towards the employee's income. The amendment clarified this point. Now all entrepreneurs are required to comply with the same standard.

Even before the adoption of the amendment, Letter No. 03-04-06/3-127 of the Ministry of Finance dated June 1, 2011 was issued, according to which all state benefits should not be subject to personal income tax. The purpose of its publication was also to clarify an ambiguous issue.

Taxation of personal income tax on additional payments up to average earnings

The amount of maternity benefit is determined based on the employee’s average salary for the last 2 years of work. This procedure is determined by part 1 of article 14 of Federal Law No. 255. The total annual income of an employee cannot exceed the maximum base for insurance payments in the Social Insurance Fund. The rule is contained in Part 3.2 of Article 14 of Federal Law No. 255. If the employee’s actual earnings are greater than the limit amount, the benefit is paid in a smaller amount.

It is also important to consider the following points: not every employee receives payments of 100% of the average salary. Sometimes benefits are determined according to the minimum wage. In all these cases, the employer can pay the employee a certain amount in order to ensure that the benefit is equal to her real average salary. This is an additional payment up to average earnings.

The entrepreneur makes payments from his own pocket, and not from the Social Insurance Fund. For this reason, the additional payment is subject to personal income tax, since it does not apply to state benefits. This rule is stipulated by Articles 209 and 217 of the Tax Code of the Russian Federation. Moreover, the additional payment must be paid to insurance contributions to various funds (for example, to the Social Insurance Fund).

ATTENTION! There are exceptions to this rule. The law allows entrepreneurs to provide financial support to employees and not pay tax on it. The “loophole” can be found in Article 217 of the Tax Code of the Russian Federation. According to the law, personal income tax will not be assessed on additional payments of up to 50 thousand rubles paid within a year from the birth of the baby. That is, the manager can make a one-time payment within the prescribed limits.

IMPORTANT! When preparing accounting documents, the additional payment must be indicated as labor costs.

Material aid

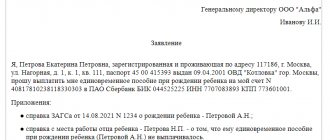

Another situation arises if the enterprise where she works provides financial assistance to a woman in labor. According to paragraph 8 of Art. 217 of the Tax Code of the Russian Federation, such material assistance, one-time and paid within one year from the birth or adoption of a child, will not be subject to personal income tax if its amount does not exceed 50 thousand rubles. If it turns out to be more, then tax is paid on the excess amount.

The conditions and procedure for providing such assistance are determined by the employer’s local regulations. The benefit is not included in the general tax base; you do not need to additionally report for it by submitting a declaration to the Federal Tax Service.

According to the norms of the Tax Code of the Russian Federation, the tax on the difference will be paid by the employer as a tax agent.

Taxation of personal income tax for child care benefits up to 1.5 years old

The benefit is paid not only to the mother of the child, but also to any person caring for him. Begins to accrue from the date of birth of children. The payment end date is:

- The day a woman goes to work.

- The baby reaches 1.5 years old.

When calculating this type of benefit, you need to take into account its minimum and maximum level:

- The minimum is the minimum wage adopted for the year of calculation of payments.

- The maximum is the maximum average earnings of a worker per day.

Childcare benefits for children under 1.5 years of age are payments exempt from personal income tax. This rule is contained in paragraph 1 of Article 217 of the Tax Code of the Russian Federation. That is, the employer, when making payments, does not have to pay anything to the state budget.

IMPORTANT! If an employer pays an employee an amount above the established benefit level, this money will be subject to personal income tax.

Who pays maternity benefits?

The basis for the absence of personal income tax is that these benefits are state compensation. They are paid to the Social Insurance Fund. Since 2022, control over benefit payments has been transferred to the Federal Tax Service.

IMPORTANT! Any entrepreneur must make payments for labor and child care. This also applies to individual entrepreneurs who have chosen a special taxation regime: imputation, simplified.

Additional nuances

Let's look at the various features of calculating benefits:

- If an employee works in several places part-time, each company must pay her money. Benefits are issued in a standard manner.

- The funds in question are not subject to personal income tax or insurance premiums. That is, the woman receives payments in full.

- Benefits will be paid only if the woman is officially employed. If she works unofficially, then only the employer makes the decision on payments. If he doesn’t pay anything, the employee won’t even be able to sue him.

The amount of benefits is determined individually in each case, depending on the worker’s salary.

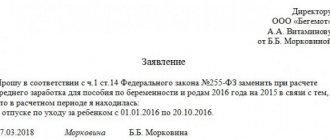

To receive payments, the employee must provide the employer with a corresponding application, as well as a certificate of incapacity for work. Papers must be submitted no later than six months from the date of the end of the leave under the BiR. If an employee wants to go on maternity leave later than the date specified in the certificate of incapacity for work, the employer must provide it from the date specified in the application.

IMPORTANT! It is not recommended to make payments under B&R for the period during which the employee actually worked. This is due to the fact that the Social Insurance Fund is unlikely to reimburse these expenses to the entrepreneur.

FOR YOUR INFORMATION! Tax exemption is due to the fact that the entrepreneur, when issuing benefits, does not spend the funds of his company. All expenses are reimbursed by the state. This is a measure to protect pregnant women, one of the social benefits.

Labor Code of the Russian Federation on maternity leave

The Labor Code guarantees the provision of maternity leave to pregnant women to prepare for childbirth and care for the baby. To exercise this right, the employee must provide the employer with a sick leave certificate from a antenatal clinic or clinic. In addition, she needs to write a corresponding statement. Otherwise, there is no basis for calculating benefits.

Below is a sample application for maternity leave.

When does standard maternity leave begin?

All pregnant women must be registered with medical institutions. A reflection of this fact is a special card that is issued for each employee. Information from this document is taken into account when issuing sick leave. From there, information will be taken to issue a certificate of registration in the early stages of pregnancy.

An employee has the right to go on sick leave from the 30th week of pregnancy. In special cases, sick leave begins from the 28th week (multiple pregnancy) or from the 27th week (living in a contaminated area). To apply for this type of leave, the employee, in an application addressed to the manager, refers to the certificate of incapacity issued to her.

The duration of sick leave for pregnant women may vary:

- In a standard situation, 70 days are provided before delivery and 70 days after this event.

- In case of complicated childbirth, the leave is increased by 16 days (part of the leave after childbirth is increased to 86 days).

- When several children are born, vacation is extended by 54 days (84 days of vacation are provided before birth, 110 days after birth).

- If the baby was born before the 30th week, then the mother is entitled to leave for 156 days.

- If a woman lives in a polluted area, her maternity leave will be 160 days.

You can also take leave when adopting a child who is not yet 3 months old. In this situation, the rest lasts 70 days starting from the date of birth of the baby. If two or more children are adopted - 110 days.

Regardless of when labor began, vacation time is used in full.

Maternity leave is calculated cumulatively and is provided to a woman completely regardless of the number of days she used before giving birth.

Article 255 of the Labor Code of the Russian Federation

When can an employee take parental leave?

After the end of maternity leave (M&P), the employee writes an application for leave to care for the baby. The duration of this leave can be up to 3 years. During the vacation, the employee retains her workplace.

During the period of parental leave, the employee retains his place of work (position).

Art. 256 Labor Code of the Russian Federation

The Labor Code of the Russian Federation gives a clear definition of maternity leave - this is leave according to the BiR, which usually lasts 140 days. Maternity leave is mistakenly called maternity leave for a child up to 1.5 or 3 years old.

Are maternity payments subject to income tax?

In addition to maternity benefits, regardless of length of insurance and type of employment, all pregnant women are entitled to the following benefits:

- a one-time benefit for women who registered before 12 weeks of pregnancy;

- benefits in connection with the birth of a child.

Table: in what amount should the BiR benefit be accrued in 2017

| Type of payment | Benefit amount, rub. |

| In general | 100% of average earnings for the previous two years (2015 and 2016 are now taken into account) |

| Maximum in general for 140 days of sick leave | 265 827,63 |

| Limit amount of benefit for complicated childbirth (156 days of maternity leave) | 296 207,93 |

| Maximum for multiple pregnancy (194 days) | 368 361,15 |

| Minimum (according to the minimum wage) until June 2022 | 34 520,55 |

| Minimum (according to the minimum wage) from July 2022 | 35 901,37 |

Should benefits be taxed?

Maternity payments refer to income that is not subject to taxes. Therefore, personal income tax cannot be deducted from these benefits; accordingly, they are not displayed in form 6-NDFL.

Is personal income tax levied on other income of a pregnant woman?

An employee who continues to work after the start of sick leave under B&R receives only wages. Simultaneous payment of B&R benefits and wages is not allowed.

Please note that if an employee receives remuneration for her work, such income is subject to tax. Accordingly, it is displayed in 6-NDFL.

If the employer gave an employee a bonus on the occasion of the birth of a child, then the amount is over 4,000 rubles. is also taxed and will be reflected in the 6-NDFL certificate according to the appropriate code.

Benefit calculation procedure

Employed women, entrepreneurs and other categories are entitled to receive benefits under the BiR. In particular:

- women who serve in the army on a contract basis. The payment is assigned in the amount of monetary allowance;

- university students. The size of the payment corresponds to the size of the scholarship in a particular institution;

- unemployed people registered with the employment center.