Registration of labor relations in the proper form plays a significant role in the further process of labor activity. And if for employers shadow employment, along with risks, also has advantages - they save on taxes and contributions, simplify reporting, ignore the guarantees provided for by the Labor Code of the Russian Federation, then for workers informal employment is more associated with adverse consequences than with advantages.

By agreeing to such working conditions, a person may forget about paid leave, receiving payments during illness, or dismissal with severance pay. And even if the employer promises the applicant to respect his labor rights properly, despite the lack of official documentation, in most cases these assurances are unfounded.

Thus, legal employment is a guarantee of the employee’s financial stability in any life situations, since the Labor Code of the Russian Federation obliges employers to pay employees the average salary when certain circumstances occur.

The average salary indicator is needed to pay employees for periods of absence from the office, as well as to calculate a number of accruals. This value is used to calculate vacation pay, sick leave, payment for absence from the workplace due to a business trip or medical examination, for dismissal payments when staff are reduced, and also to calculate maternity benefits. But in order to make payments correctly, the accountant needs to know how to make calculations and what to take into account for these purposes.

The rules for calculating the average monthly salary in situations established by the Labor Code of the Russian Federation are unified (Article 139 of the Labor Code of the Russian Federation). Average daily earnings are used in calculations. However, depending on the situation, there may be special features, for example, when recording working hours in aggregate.

The specifics of the procedure for calculating the average salary are provided for by the regulation of the same name, approved by Resolution of the Cabinet of Ministers of the Russian Federation of December 24, 2007 No. 922 (hereinafter referred to as Regulation No. 922).

To calculate the average monthly accruals for paying sick leave and maternity leave, a different procedure is applied, approved by Resolution No. 375 of June 15, 2007 (hereinafter referred to as Regulation No. 375).

Billing period for calculating average earnings

Regardless of what kind of labor regime the company operates, the average monthly salary is calculated based on the salary actually paid to the employee and the production rate for the last 12 months (calendar) preceding the paid event (Article 139 of the Labor Code of the Russian Federation, clause 4 of Regulation No. 922). That is, the billing period for cases provided for by the Labor Code is 12 months.

In this case, calendar months are taken in full - from the 1st to the 30th (31st) day, and for the February period - from the 1st to the 28th (29th) day.

At the same time, Article 139 of the Labor Code of the Russian Federation allows the introduction of other periods. The main thing is that this is officially documented and does not worsen the situation of the staff.

When calculating the average amount of payments, individual days and the amounts of their payment are not counted (clause 5 of Regulation No. 922). These are the periods:

- maintaining the average salary for the employee. Exceptions include breaks provided to nursing mothers;

- receiving sick leave or maternity benefits;

- downtime due to the fault of the employer or for reasons beyond our control;

- inability to work due to a strike, provided that the employee did not participate in it;

- additional paid days off to care for children with disabilities;

- other cases of release from work duties with or without retention of payments.

Please note that we are talking about cases regulated by labor legislation. In other situations, for example, for calculating maternity and child benefits, the period will be different.

Amounts included in the calculation of average earnings

What charges are taken into account in the calculations is briefly discussed in Art. 139 of the Labor Code of the Russian Federation: these are all payments within the framework of the company’s remuneration system. This issue is discussed in more detail in clause 2 of Regulation No. 922. It specifies what exactly is to be taken into account:

- wages, including piecework, as a percentage of sales, goods, commissions;

- monetary remuneration for civil servants;

- fees in media editorial offices;

- teachers' salaries for overload;

- allowances and additional payments, including for professional skills, combination, length of service, knowledge of other languages;

- payments related to working conditions;

- bonus accruals and remunerations made within the framework of the company’s remuneration rules;

- other types of salary payments.

Payments with social characteristics and that are not payment for work should be excluded from the calculation. We are talking about financial assistance, payment for travel, lunches, vacations, housing and communal services and other similar payments.

How to take bonuses into account in average earnings

Monthly bonuses, which are paid with wages, are included in the calculation in the accounting department in the month for which they were accrued.

The accountant must take into account the bonuses that the company pays to employees based on the results of the quarter or year in the average earnings in the amount of accrued amounts for the billing period.

Payments such as one-time remuneration for length of service or for years of work, various bonuses at the end of the year, one-time bonuses for a special important task, as well as annual bonuses, must be included in earnings in the amount of accrued amounts in the billing period.

Formula for calculating average earnings

To determine the average amount of wage payments, average daily earnings are used. If a company takes into account working hours in aggregate, then another indicator is taken - average hourly earnings (clause 9 of Regulation No. 922).

Thus, the average salary is calculated using the formula: average earnings (AE) = average daily earnings x number of days of the paid period.

When recording working hours in total, another formula is used: average earnings (AE) = average hourly earnings x number of scheduled working hours in the paid period.

Calculation of average earnings

To do this, you need to know the average daily earnings (ADEW).

It is determined by the formula (does not apply to the calculation of vacations and compensation for unused vacation, as well as to the calculation of benefits): SDNZ = salary for days worked in the billing period / number of days worked.

To calculate vacation pay, which as a general rule is paid for calendar days and not working days, a different formula is used. We will talk about it below.

In practice, situations arise when an employee did not have wage payments during the required period or did not work. In this case, the calculation is carried out taking into account the following features:

- the average salary is determined based on the amounts accrued for the period preceding the settlement period and equal to it;

- if there was no salary at all in previous years, then you need to take accruals for days worked in the month the paid event occurred;

- if there were no payments at all, the tariff rate and salary (official salary) are used in the calculation.

An example of calculating average earnings during a business trip

An employee of an organization with a five-day work week was sent on a business trip from February 11 to 17, 2022. The billing period is 12 months - from February 1, 2022 to January 31, 2022. During this period, the employee was sick for three days (from March 12 to March 14, 2022) and was on annual paid leave from July 2 to July 29, 2022.

During the billing period, the employee was paid:

- salary - 522,000 rubles;

- vacation pay - 39,400 rubles;

- sick leave benefit - 6,041.25 rubles.

Calculation:

- according to the production calendar from February 1, 2022 to January 31, 2022 there were 247 working days;

- the employee worked (247 workers - 3 days of sick leave - 20 days of vacation (working)) - 224 days;

- When calculating average earnings, wages for the pay period are included, but sick leave and vacation payments are not taken into account.

SDNZ: 522,000 rubles/224 days = 2,330.36 rubles.

SZ: 2,330.36 × 5 days of business trip (working) = 11,651.80 rubles.

How does vacation affect payouts?

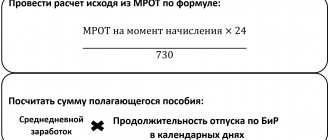

Sick leave is paid to the employee by the employer on the basis of Order of the Ministry of Health No. 624n.

The amount to be paid is calculated using the formula:

Number of sick days* % of insurance period * average daily wage.

In this case, the average daily wage is calculated using the formula:

Salary for 24 months/730 days.

The employer is obliged to pay for all days of incapacity for work of the employee. Except for cases when the form contains a note about violation of hospital regulations.

The amount of sick leave insurance also affects the amount of sick leave; the percentage depends on how long the employee has officially worked throughout his life.

- Less than 5 years - 60%.

- From 5 to 8 years - 80%.

- More than 8 years - 100%.

Is it taken into account when determining average earnings or not?

Yes. To calculate the average daily earnings of an employee, the amounts from which the employer pays contributions to the Social Insurance Fund are taken into account.

Is compensation for unused vacation time included in disability benefits?

Yes. Since compensation refers to those deductions for which the company pays insurance premiums. Therefore, when calculating sick leave, compensation is taken into account.

How to calculate - examples

Example 1.

It is necessary to calculate the amount of payment for a temporary disability certificate for 9 days, the employee’s length of service is 2 years, income for 2017 is 480,000 rubles, for 2022 - 540,000 rubles.

Total payable: (480,000+540,000/730)*0.6*9=RUB 7,545.2.

Example 2.

Ivanov I.I. brought a certificate of temporary incapacity for work for 12 calendar days. Insurance experience 6 years. Over the last 24 months the following payments have been made to him:

| Period | Salary | Vacation pay | Total |

| 2017 | 600 000 | 47 761,57 | 647 761,57 |

| 2018 | 635 000 | 50 568,82 | 685 568,8 |

Sick leave calculation is calculated using the formula:

Number of days on sick leave* % of length of insurance * average daily wage.

In this case, the average daily wage is calculated using the formula:

Salary for 2 years / 730 days.

| Operation | Bottom line |

| Payments for temporary disability are 80% | 80% |

| Base for calculating average earnings: 647761.57+685568.8 =1333330.37 | 1333330.37 rub. |

| Average daily salary: 1,333,330.37/730 = 1,826.47 | RUB 1,826.47 |

| Sick leave benefit: 1,826.47*12 = 21,917.78 | RUB 21,917.78 |

Features of calculating average earnings for sick leave

The rules for calculating sick leave are determined by the regulation on the specifics of the procedure for calculating benefits for temporary disability, pregnancy and childbirth, and child care, approved by Decree of the Government of the Russian Federation of June 15, 2007 No. 375. To pay for sick leave, the average daily earnings are used (clause 15 of Regulation No. 375) . It includes all employee payments for which contributions to the Social Insurance Fund are accrued. The average salary is determined by the formula (Part 3, Article 14 of Law No. 255-FZ, Clause 15 (1) of Regulation No. 375): SRDNZ = earnings for the billing period / 730.

The billing period for the purpose of calculating benefits for sick leave is two calendar years preceding the year of illness (Part 1, Article 14 of Law No. 255-FZ, Clause 6 of Regulation No. 375). At the same time, the average earnings for each year are limited by the maximum value of the base for calculating contributions (Part 3.2 of Law No. 255-FZ, Clause 19 (1) of Regulation No. 375).

If over the last two calendar years the employee had no earnings or their amount did not exceed the minimum wage, then the average earnings are considered equal to the federal minimum wage established on the day of illness, taking into account regional coefficients (Part 1.1 of Article 14 of Law No. 255-FZ).

Calculation example

Monthly contributory payments to an employee who submitted sick leave in 2022 and 2022 were 60,000 rubles. During the billing period, earnings amounted to: 720,000 720,000 = 1,440,000 rubles.

The maximum base for calculating contributions to the Social Insurance Fund in 2019 is 865,000 rubles, in 2020 - 912,000 rubles. The employee’s earnings for each year of the billing period did not exceed the base limits.

We determine the average daily earnings: 1,440,000 / 730 = 1,972.60 rubles.

Are vacation pay included in the calculation of benefits?

Vacation pay is classified as a type of earnings subject to insurance contributions (Article 420 of the Tax Code of the Russian Federation). To calculate temporary disability benefits, all types of income for which insurance premiums are calculated are taken into account (Clause 2, Article 14 of Federal Law No. 255-FZ of December 29, 2006). These standards will continue to apply in 2022. The answer to the question that interests many employees and employers: “is sick leave taken into account when calculating vacation pay in 2022?” positive - yes, it is taken into account. This is confirmed by Government Decree No. 375 of June 15, 2007, which approved the procedure for calculating benefits paid from the Social Insurance Fund.

Subtleties of calculating average earnings for vacation pay

The guarantee of paid vacation is provided for in Art. 114 Labor Code of the Russian Federation. It says that during the main vacation, workers retain their average earnings. Since this case is provided for by the Labor Code of the Russian Federation, the procedure provided for in paragraph 2 of Regulation No. 922 is applied here.

For vacation accruals, the average salary includes payments named by the company’s remuneration system. The period for calculation will be 12 calendar months before the vacation month (clause 4 of the provisions). If an employee goes on vacation in June, then for calculations the period of time is taken from June 1 of last year to May 31 of this year.

As a rule, vacation is granted in calendar days (Article 115 of the Labor Code of the Russian Federation). To pay for such vacations, the average earnings are determined by the formula (clause 9 of the regulations): SZ = average daily earnings x number of calendar days of vacation.

To determine the average daily earnings, the indicator of the average monthly number of calendar days is used, equal to 29.3 (clause 10 of the regulation). However, the exact formula depends on whether the employee has fully worked the months of the pay period or not.

Months worked out in full (clause 10 of the regulations):

SDNZ = salary for the pay period (minus unaccounted amounts) / 12 / 29.3

Calculation example.

The employee was granted additional paid leave from January 20 to January 22, 2022. He worked out the entire billing period from January 1, 2022 to December 31, 2022. The salary for the billing period amounted to 600,000 rubles.

SDNZ amounted to: (600,000 rubles / 12 / 29.3) = 1,706.50 rubles.

SZ per month: 1706.50 × 3 (vacation days) = 5,119.50 rubles.

There were shortcomings in the months (clause 10 of the regulations):

SDNZ = salary for the billing period / (29.3 x number of fully worked months, number of days in unworked months).

Number of days in unworked month = 29.3 / (by the number of calendar days of the month x by the number of calendar days falling within the time worked in a given month).

Calculation example

The employee goes on a two-week vacation from January 11 to January 24, 2022. The billing period is January 1—December 31, 2020. The calculation includes 530,000 rubles.

During this period the employee did not work:

- 7 calendar days - in February (vacation);

- 7 days - in December (sick leave);

- 2 calendar days in March, 30 calendar days in April, 3 calendar days in May (presidential non-working days from March 30 to April 30, from May 6 to 8, 2022);

- March 2–29, 2022 and October 1–31, 2022 – business trip.

Thus, the employee worked fully for 6 months: January, June, July, August, September, November.

We count the number of days in months that are not fully worked:

- February: (29.3 / 29 days x (29 days - 7 days)) = 22.23 days;

- March - excluded from the calculation, since the employee did not work there at all (non-working days and business trips);

- April - non-working days throughout the month;

- May - (29.3 / 31 days x (31 days - 3 days) = 26.46 days;

- October - business trips are excluded from the calculation;

- December - (29.3 / 31 days x (31 days - 7 days) = 22.68 days.

SDNZ: 530,000 rubles / (29.3 × 6 months 22.23 days 26.46 days 22.68 days)) = 2,144.27 rubles.

NW: RUB 2,144.27 x 14 days = 30,019.78 rubles.

How does the newsletter affect accruals before vacation?

According to the Labor Code of the Russian Federation, each employee has the right to 28 calendar days of vacation annually. To calculate the number of calendar days for vacation, you need to know how long the employee works at the company. Based on a standard vacation of 28 days, for each month worked, each employee receives 2.33 days (28 days/12 months)

Amount of days

Sick leave does not affect the calculation of the number of vacation days. According to Art. 121 of the Labor Code of the Russian Federation, the calculation includes days:

- actually spent;

- taken at your own expense;

- non-working due to the fault of the employer;

- when an employee did not work, but his place of work was retained (for example, weekends).

The calculation does not include:

- absence from work without good reason;

- maternity leave.

Note: when calculating, days spent by an employee on sick leave are not taken into account.

Cash payments

To the question whether payments for temporary disability are taken into account when calculating leave, whether they are included in average earnings, the answer, unfortunately, is negative. For the calculation, only days actually worked are taken into account, for which the employer will make contributions:

- salary;

- bonuses;

- other payments and compensations subject to insurance premiums.

Since an employee is absent from the workplace during illness and is not paid a salary for these days, sick leave is not included in the list for calculating vacation pay. Read more about how an employee’s vacation ballot is opened and how vacation pay is paid and accrued, read here.

Compensation for unused annual vacation time

Not included. The calculation of compensation for unused vacation is calculated in the same way as the calculation of vacation pay, based on the employee’s average daily earnings for the actual time of work.

How to calculate the amount - examples

Example 1.

Ivan Petrovich wants to rest for two weeks. Income for the last 12 months. is 523,000 rubles. How is the amount of vacation payments calculated in this case?

Vacation pay is calculated using the formula:

Average daily earnings * number of vacation days. Average daily earnings = Annual income/12 months/29.3. The value 29.3 is a constant value established by Decree of the Government of the Russian Federation No. 922 of December 24, 2007, which determines the average number of days in a month for a year.

| Operation | Bottom line |

| We calculate the amount of the average daily earnings of a worker: 523,000 / 12 / 29.3 = 1487.5 | 1487.5 rub. |

| Amount to be paid: 1487.5 *14= 20,824.8 | RUB 20,824.8 |

Example 2.

Petrov P.P. joined the company on October 12, 2022. How many vacation days did he earn as of February 16, 2022?

With the standard 28 calendar days provided for by the Labor Code of the Russian Federation, for each full month he receives 28/12 = 2.33 days.

Hence:

| Period | Calculation | Quantity |

| October | in October he worked 20 days: (2.33/31)*20= 1.5 | 1,5 |

| November | for the whole month: 2.33 | 2,33 |

| December | for the whole month: 2.33 | 2,33 |

| January | for the whole month: 2.33 | 2,33 |

| February | in 16 days: (2.33/28)*16=1.3 | 1,3 |

| Total: | 1,5+(2,33*3)+1,3 = 9,8 | 9.8 days of rest |

Calculation of average earnings upon dismissal

When an employee is dismissed, a company is liquidated or staff is reduced, he is paid severance pay in the amount of average monthly earnings (Part 1 of Article 178 of the Labor Code of the Russian Federation).

Since this payment is provided for by the Labor Code of the Russian Federation, the general procedure is used to calculate average earnings using average daily earnings (regulation No. 922).

According to paragraph 9 of the regulation, to determine the average salary, you need to multiply the average daily salary by the number of paid working days.

The average daily salary is calculated using the formula:

SDNZ = accruals for days worked in the billing period / number of days worked.

Calculation example

An employee of a company with a five-day work week was dismissed due to staff reduction on August 17, 2022. He is paid for the period from August 18 to September 17, 2022, that is, 23 working days. Billing period: August 1, 2022 – July 31, 2022. The salary for this period amounted to 420,000 rubles (vacation pay is not taken into account). He worked there for 230 days.

SDNZ = 420,000/ 230 days. = 1,826 rubles;

SZ - 1,826 rubles x 23 days. = 41,998 rubles.

How to calculate average earnings from 2022

The average earnings include all types of payments to the benefit of the employee, for which insurance premiums are calculated.

Lawyers, individual entrepreneurs, members of peasant and farm enterprises, notaries and other persons engaged in private practice, the average earnings are taken equal to the minimum wage, taking into account regional coefficients in the regions where it is introduced.

Wages paid in non-monetary form are recalculated to account for average earnings as the cost of goods (work, services) at market prices on the day of payment.

Income received in foreign currency is accounted for in rubles at the exchange rate of the Central Bank of the Russian Federation on the day the benefit is calculated.

Calculation of average earnings for benefits

Events related to the birth of a child are also subject to payment. The woman receives maternity benefits and, for the first year and a half of the baby’s life, child benefits. Their size is also tied to average earnings. Maternity pay makes up 100 percent of the average salary. And the child benefit is 40 percent of this amount every month, but not less than the lower limit determined by the state (Article 11 of Law No. 255-FZ).

To calculate payments, you should be guided by regulation No. 375.

For calculations, the average salary for the two calendar years before the year of maternity leave is used. The time spent working in another place is also taken into account (clause 6 of the regulations). The average earnings include all employee accruals for which contributions to the Social Insurance Fund are accrued.

If an employee goes on a second maternity leave without going to work and, accordingly, he was not paid a salary for the last two years, then to calculate the average amount of wage payments, unpaid years can be replaced. For this purpose, the two years preceding the initial decree are taken. Years can be changed only if, as a result, maternity and child benefits will be larger (clause 11 of the regulation).

To calculate the amount of benefits, the average daily earnings are used (clause 15 of the regulation). It is determined by the formula (clause 15 (2) of the regulation): SDNZ = earnings for the billing period / by the number of calendar days in this period.

The following are excluded from the calculation:

- sick days;

- maternity leave;

- Holiday to care for the child;

- release from work with retention of salary, if no contributions were accrued for it.

In this case, the average daily salary cannot be more than the amount obtained by dividing the maximum values of the bases for calculating contributions in force in the two years preceding the leave by 730.

Accordingly, the calculation of this value is carried out according to the formula: maximum size of the SDNZ = maximum values of the bases for the 2 previous years / 730.

In addition, if the employee has had no salary at all over the last two years or its monthly amount did not exceed the minimum wage, then the average earnings are taken to be equal to the minimum wage (clause 11(1) of the regulation). Average daily earnings from the minimum wage are calculated according to the formula (clause 15 (3) of the regulation): minimum SDNZ = minimum wage on the date of vacation x 24 / 730.

Calculation example

The employee will go on maternity leave starting January 18. In the last two years, contributions subject to contributions amounted to: 663,000 rubles: in 2022 - 339,000 rubles in 2022 - 324,000 rubles.

The total number of calendar days in 2022 and 2022 is (365,366) = 731. Since the woman was on sick leave for 21 days in the calculation period, only (731 - 21) = 710 days are included in the calculation.

SDNZ: 663,000 /710 days. = 993.80 rubles.

In 2022, the limits for insurance contributions to the Social Insurance Fund are 865,000 rubles, in 2020 - 912,000 rubles.

SDNZ in the maximum possible amount: (865,000,912,000) / 730 = 2,434.25 rubles.

The smallest possible amount of SDNZ: 12,792 (2022 minimum wage) x 24 / 730 = 420.56 rubles.

Other types of "children's" benefits

In addition to sick leave, maternity leave and child care benefits, the employee is entitled to so-called “children’s” benefits. They are provided for by Federal Law No. 81-FZ dated May 19, 1995. This is a benefit for registration in the early stages of pregnancy and a one-time benefit for the birth of a child.

The benefit for early registration is paid on the basis of a certificate issued by a doctor. Such certificates are issued to women who register before 12 weeks of pregnancy.

Until July 1, 2022, this benefit was paid one-time by the FSS. The amount was fixed, and from February 1, 2022 it was 708.23 rubles.

Starting from July 1, 2022, benefits for registration in the early stages of pregnancy are paid by the Pension Fund at the request of the employee. The benefit became monthly. Its value is equal to 50% of the regional subsistence level for the working population in a constituent entity of the Russian Federation. From January 1, the benefit amount is subject to recalculation. The payment period is from the month of registration with a medical organization (but not earlier than six weeks of pregnancy), until the month of childbirth or termination of pregnancy.

The benefit is not always due, but only if the following conditions are simultaneously met:

- the pregnancy is six weeks or more, and the woman registered with a medical organization before twelve weeks of pregnancy;

- the size of the average per capita family income does not exceed the subsistence minimum per capita in the constituent entity of the Russian Federation on the date of application for the benefit (see “Benefits for registration in the early stages of pregnancy will be paid according to the new rules”).

The size of the lump sum benefit for the birth of a child is a fixed amount that does not depend on the employee’s length of service or earnings. It is indexed annually. To calculate the benefit for the current calendar year, you need to take last year’s value and multiply by the coefficient approved by the Social Insurance Fund for the current year (read more about this in the article “How to calculate “child benefits” in 2015: new amounts and “transitional” situations”) .

From February 2022, the amount of the benefit for the birth of a child is 18,886.32 rubles.

These types of benefits are not subject to income tax or insurance premiums.