How to use the calculator

Instructions for using the average salary calculator

- Specify the calculation period - any number of months preceding the calculation date.

- Indicate the date on which the calculation is made, the method of recording working hours, and the days excluded.

- Enter wages and bonuses for the selected months. When you pay your salary for the first month, for convenience, the data is automatically entered for all the following months.

- Click "CALCULATE". You will receive data on your average daily earnings with all the calculation details.

About the average salary calculator

The average salary calculator will be useful for independent calculations, as well as for checking the accuracy of the calculations made by the accounting department. Calculation of wages based on average earnings may be required to calculate wages for the periods:

- suspension of the enterprise's activities;

- long downtime;

- the employee is on a business trip;

- downtime during a strike (letter of the Ministry of Finance of the Russian Federation No. 149KV dated January 23, 1996).

In addition, based on average earnings, severance benefits are calculated for employees upon their dismissal as a result of liquidation of an enterprise or reduction of staff.

For your information! Any event that entailed the need to use average indicators for calculating wages will be called the moment the right to maintain average earnings arises.

The calculator is not used to calculate payments and benefits for vacations, sick leave and periods of maternity leave. These payments, although made on the basis of average earnings, are actually calculated using a different methodology, which includes the calculation of payments that are not included in wages.

Solution concept

Since the taxation of personal income tax and contributions is configured for the types of accruals, you will need to describe two types of accruals: for the non-taxable and taxable part of the compensation. Let both accruals be made automatically in the Dismissal if the value of the indicator Amount of Compensation by agreement of the parties .

In the Dismissal , the employee’s average daily earnings are automatically calculated to calculate severance pay - this is the average earnings for 1 working day. The question arises of how to convert average daily earnings into average monthly earnings to determine the taxable and non-taxable portion of compensation. This issue is not regulated by law. In some organizations, it is customary to multiply the average daily earnings by the number of working days in the next three months according to the employee’s work schedule, in others, the multiplication occurs by the average monthly number of working days, increased three times.

To make the solution universal, the number of working days to determine three times the average monthly earnings based on the daily average will be requested from the user as the value of the indicator Number of days to calculate the non-taxable part of dismissal compensation .

Thus, the schematic formula for calculating the non-taxable amount of compensation will look like this:

Average daily earnings of an employee * Number of working days for calculating the non-taxable part of compensation upon dismissal

The amount of compensation exceeding the taxable amount will be considered a non-taxable part of the compensation.

There are a number of nuances when calculating compensation:

- If an employee had no income in the billing period, and we change the billing period to calculate average earnings in the document Dismissal, these changes will not be taken into account when calculating compensation. The amount of average earnings will need to be indicated manually in the document, then the compensation will be calculated.

- We will configure accruals for compensation as “shooting” - they will be calculated only if the value of the compensation amount is entered. Such accruals do not fall into the document Dismissal , if an employee who is on parental leave is dismissed, and Return from child care leave (Human Resources - Parental leave and returns from leave) was not entered for her (or the date of return is later than the date of dismissal ). In this case, you will need to add lines with accruals to the Dismissal manually.

Legal regulation

All accounting operations, one way or another related to the calculation of average earnings, are regulated by the same Decree of the Government of the Russian Federation No. 922, as amended on December 10, 2016.

Thus, when calculating, all types of payments within the framework of remuneration are taken into account. Let us clarify what exactly labor is, since any allowances for food, travel, financial assistance of any kind, various compensations will be excluded from the total income received as a result of labor activity.

The calculation period is taken to be the last 12 months before the start of the period for the emergence of rights to average earnings.

The 12-month period excludes time periods during which the employee did not actually perform his job duties. Thus, the following times are subject to exclusion:

- confirmed disability of the employee;

- employee maternity leave;

- downtime of the enterprise due to the fault of the enterprise itself, or for reasons beyond its control, for example in the case of a strike in which the employee, although he did not take part, was not able to perform his labor functions;

- provided as additional days off to care for disabled children;

Accordingly, amounts received by employees during the above periods are also excluded from the calculation of average earnings.

Calculation of compensation upon dismissal by agreement of the parties

Let's look at the calculation of compensation using an example.

Example

The employee resigns on March 30, 2018; upon dismissal, he is awarded compensation upon dismissal by agreement of the parties in the amount of 180,000 rubles.

The average daily earnings of an employee are calculated in the amount of 2,222.22 rubles.

To determine the non-taxable part of compensation in an organization, it is customary to multiply the employee’s average daily earnings by the number of working days in the next three months according to the employee’s work schedule.

Entering indicators for calculation

The number of working days in the next three months after dismissal according to the employee’s work schedule from March 31 to June 30, 2018 will be 61 days.

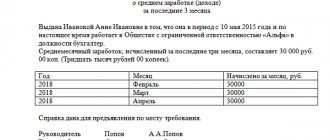

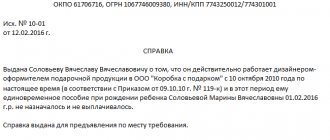

The number of days of compensation and the amount of compensation itself is entered through the journal Data for salary calculation (Salary - Data for salary calculation) based on the created Template for entering initial data - Entering compensation upon dismissal by agreement of the parties . In our example, 61 days and 180,000 rubles are indicated:

Compensation calculation

Compensation is calculated automatically in the Dismissal .

On the Accruals and Deductions , compensation upon dismissal is calculated by agreement of the parties, and the amount is automatically divided into non-taxable and taxable amounts:

We will check the calculation of the non-taxable amount of compensation upon dismissal by agreement of the parties.

Non-taxable amount of compensation:

- RUB 2,222.22 <Employee’s average daily earnings> * 61 <Number of working days for calculating the non-taxable part of compensation> = RUB 135,555.42.

Let's look at how the taxable amount of compensation was calculated.

Taxable amount of compensation:

- 180,000 rub. <Amount of compensation> – (2,222.22 rubles. <Employee’s average daily earnings> * 61 <Number of working days to calculate the non-taxable part of compensation>) = 44,444.58 rubles.

In case of manual adjustment of average earnings on the Conditions of Dismissal , automatic recalculation of compensation amounts on the Accruals and Deductions will not occur!

In this case, you will also need to edit the value of the average earnings indicator on the Accruals and deductions .

For example, on the Dismissal Conditions , we manually edited the data for calculating average earnings so that the average earnings were 2,500 rubles. After this, you will have to manually enter the amount of average earnings into the Average indicators. earnings (total) for the types of calculations Compensation upon dismissal by agreement of the parties (NON-TAXABLE) and Compensation upon dismissal by agreement of the parties in excess of 3 times the average earnings (TAXABLE) :

If you are dismissed on the last day of the month, the average salary is calculated without taking into account the month of dismissal. This is a feature of the ZUP calculation algorithms that cannot be corrected.

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- Severance pay upon dismissal by agreement of the parties You do not have access to view To gain access: Complete a commercial...

- Settlements with an employee upon dismissal, including payment of compensation for unused vacation Dismissal of an employee is an operation without which no activity can proceed...

- Calculation of compensation for unused vacation upon dismissal in 1C 8.3 Accounting 3.0: step-by-step instructions A resigning employee who has not taken any vacation at all is not an uncommon situation. However…

- Calculation of compensation for unworked days upon dismissal in ZUP 3 Let's consider how to calculate compensation for unworked days in ZUP 3...

Accounting for bonuses

When calculating average earnings, bonuses and other types of additional remuneration are taken into account according to a special algorithm.

Thus, one bonus is taken into account for any one indicator for each month that is calculated. That is, if we assume that the employee received two additional remunerations in one month, but according to different indicators, for example, one for exceeding the plan, the other for an improvement proposal, then only one of them will be taken into account.

In the same way, the following are taken into account:

- bonuses and any other remuneration issued based on the results of two or more (up to 12) months;

- bonuses and other types of remuneration issued based on annual results within a calculated period of 12 months. The time of accrual of annual bonuses will not matter, the main thing is that the period for which the bonus was issued was included in the last 12 months;

- one-time payments for long service.

No salary

If the employee does not have any payments during the calculation period (12 months) or for a time period exceeding this period, the accounting department must take the employee’s monthly salaries for the previous period as a basis. Thus, if from June 1, 2017 to June 1. In 2022, the employee did not receive a salary or did not work at all, then the time period from June 1, 2016 to June 1, 2016 will be taken as the calculation period. 2022.

If the employee did not have payments before the start of the pay period, then the accounting department will take as a basis the salary in the month from which the employee became entitled to maintain the average salary.

In the case where payments did not take place and during the period of occurrence of the case giving the right to maintain the average monthly earnings, the calculation will be carried out based on the salary assigned to the employee.

How to calculate three times your average monthly earnings

Article 178 of the Labor Code of the Russian Federation provides for two amounts of severance pay:

- Average monthly earnings - paid in the event of liquidation of an organization and reduction in the number or staff of employees.

- Two-week average earnings - paid in other cases, including upon termination of an employment contract:

- with a person employed in seasonal work in connection with the liquidation of an organization, reduction in the number or staff of the organization’s employees (Article 296 of the Labor Code of the Russian Federation);

- with a foreign worker or stateless person in connection with the suspension or cancellation of the permit to attract and use foreign workers, on the basis of which such a worker was issued a work permit (Article 327.7 of the Labor Code of the Russian Federation).

We also note a benefit in the amount of three months' average earnings paid to the head of the organization, his deputy or chief accountant in connection with a change in the owner of the property, to a manager dismissed by decision of the owner of the organization.

In this case, an employment or collective agreement may provide for increased amounts of severance pay, with the exception of the cases specified in Art. 349.3 Labor Code of the Russian Federation. In particular, this article applies to the following categories of workers:

- managers, their deputies, chief accountants and members of collegial executive bodies of state corporations, state-owned companies, as well as business companies, who have concluded employment contracts, as well as business entities, more than 50% of the shares (shares) in the authorized capital of which are in state or municipal ownership;

- managers, their deputies, chief accountants of state extra-budgetary funds of the Russian Federation, territorial compulsory medical insurance funds, state or municipal institutions, state or municipal unitary enterprises.

The amount of compensation for these employees is three times their average monthly earnings. Payment to them of other benefits or compensation upon dismissal by agreement of the parties (Article 78 of the Labor Code of the Russian Federation) cannot be provided for by such an agreement.

The three-month average earnings do not include:

- wages due to the employee;

- average earnings retained in cases where an employee is sent on a business trip, for vocational training or additional vocational education outside of work, in other cases in which, in accordance with labor legislation and other acts containing labor law norms, the employee retains average earnings;

- reimbursement of expenses associated with business trips, moving to work in another area;

- monetary compensation for all unused vacations;

- average monthly earnings retained for the period of employment in the event of liquidation of an organization or reduction in the number or staff of employees.

Severance pay is paid to the employee, along with other compensation and amounts due, on the last day of work. If the employee did not work on the day of dismissal, then the corresponding amounts must be paid no later than the next day after the dismissed request for payment is presented (Article 140 of the Labor Code of the Russian Federation).

The benefit is accrued based on the order of dismissal of the employee. There is no need to draw up a separate order for payment of benefits. The amount of the benefit is indicated in the calculation note issued upon dismissal.

Severance pay, which generally does not exceed three times the average monthly salary, is not subject to personal income tax and insurance contributions (Letter of the Ministry of Finance of the Russian Federation dated July 2, 2019 No. 03-04-06/48330).

Calculating average monthly earnings can be useful when calculating vacation pay, laying off an employee, or in situations where his rights are infringed.

Different life situations lead to a change in activity type. If this happens through the fault of the employer, then the person can count on temporary financial support. The terms of such payments will be limited to a minimum of 2 months.

To determine material payments, you must know the possible average income for 1 month. Take into account the number of days already worked and the number of working days that will be paid in the future.

The need to determine the amount of average monthly earnings may arise in several cases:

- If an employee is going to be laid off due to a reduction in staff.

- Determination of vacation pay for the employee’s rest period.

- Situations when there is a deterioration in working conditions for an employee or other infringements that are prescribed in the collective agreement of the enterprise.

If an employee has been laid off, the company undertakes to pay an amount equal to the average monthly salary for the period of time determined by the Labor Code of the Russian Federation.

If, after being laid off, it is not possible to get a job immediately, the company will provide financial assistance, which is determined by the size of the average monthly income.

Calculation of average daily earnings is needed to determine the payments that a person should receive.

Situations when it is necessary to calculate the average amount of income per working day can be completely different. The calculation is carried out to determine the payments that a person should receive.

All cases are regulated by the legislative framework and present the following options:

- If a person has temporarily lost his ability to work for some reason.

- Payments provided to women on maternity leave when caring for a child up to 1.5 years old.

- In cases of unused vacation, a person may receive monetary compensation.

- If a person became a donor and did not go to work on a certain day due to donating blood.

- The employee was seconded on official business during the work week.

- Days when a person was absent from work while caring for a child or disabled relative.

There are other situations where payment is provided in the amount of average daily income. In the process of signing a rental agreement, clauses regarding payments are negotiated by the two parties.

To determine a specific amount, you should use a special formula that accountants use in their work. This scheme is approved by the TR of the Russian Federation and is relevant for modern legislation:

- First, you should add up your wages for all 12 months. To get the most accurate number possible, it is best to use checks or bank statements.

- The resulting number must be divided by 12 working months. Since wage amounts may vary due to periodic accrual of bonuses, remunerations and additional payments, dividing by 12 will help determine the arithmetic average.

- The arithmetic mean is divided by the index 29.3. The presented index represents the optimal number of working days in a month.

If a workweek has more or fewer working days, then the index 29.3 is not used. It is enough to calculate the total number of working days per month.

Calculation example

The employee received the following amounts during the year: 10000, 10050, 12500, 20000, 7700, 8900, 12000, 10880, 12222, 10500, 9500, 10400. The working week is represented by 6 working days.

We calculate:

- 10000 10050 12500 20000 7700 8900 12000 10880 12222 10500 9500 10400 = 134652. Addition of all amounts that the employee received each month during the year.

- 134652/12=11221. The arithmetic mean of income is determined.

- 11221/29.3=382.97. Calculation for the subsequent months after termination of cooperation with this company.

The cost of one working day is determined.

Average monthly earnings should be skillfully calculated using the appropriate instructions and provisions of the labor code.

To accurately determine the average monthly income, you can contact the company’s accounting department.

You can independently determine the amount of the benefit, which is determined precisely by calculating the average monthly earnings.

Average monthly earnings = amount of full salary/actually worked days * number of calendar days.

The formula for determining the amount of average monthly earnings is very easy to use. Anyone can use this algorithm for calculations. First, you should carry out mathematical calculations that will determine each component of the formula, and then substitute it into the general scheme for data processing.

Calculation formula:

- First, you should take a statement from the accounting department, which clearly indicates the salary that the employee receives monthly.

- It is worth getting a certificate from HR or accounting that indicates how many days were worked out of the full pay period.

- Using the calendar, calculate the number of working days in accordance with the working week that remain after dismissal.

Having collected all the data, you can begin to process it: divide the amount of the full salary by the days actually worked. Multiply the resulting result by the number of calendar days.

This formula is relevant when determining the benefit that an employee who has been laid off will receive.

Calculation example

Sometimes it is very difficult to figure out the definition of many nuances, even if the calculation formula is elementary.

The employee was dismissed due to staff reduction on April 15, 2018. The billing period is determined from March 1 to March 31. The monthly salary during the employment period was 1000 rubles.

We calculate how much you can get for a year of work: 12,000 rubles: you need to multiply the monthly wage by the number of months in the year. The work period was 250 days. This means that the average daily earnings are determined in accordance with the following rules: 12000/250. We get 4.8 for each day.

This example is relevant if the severance pay was received on the same day on which the calculation was made.

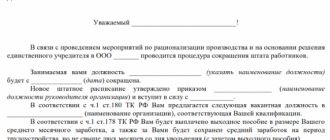

No enterprise or production can give its employees guarantees that it will not go bankrupt or disband. If the financial situation of the production is deplorable and liquidation is planned, then employees must be warned at least 2 months in advance.

In addition, employees are entitled to a number of material benefits. What can workers count on during the liquidation of production?

When contracting

If an employee is laid off, he has the right to compensation, which is the amount of average monthly earnings. Payments are made within 2 months after dismissal. Sometimes payments are made for 3 months.

Upon dismissal

- Additional remuneration for the work of class teachers and teaching staff.

- Bonuses and other remunerations to personnel for the performance of labor duties approved by the LNA of the enterprise.

- Other types of payments in accordance with the payment procedure adopted by the employer.

Calculations in case of salary increase

The calculation of the average salary in the event of a salary increase carried out by the employer or as a result of the adoption of framework legislation will be carried out taking into account exactly when the salary increase took place.

- If the salary was increased during the pay period, then the average monthly salary will be calculated taking into account the increasing coefficient, calculated according to the scheme: the official salary in the month of the increase is divided by the official salary before the increase. The difference will be the coefficient, the calculation of which is included in the calculator system.

- If the salary was increased after the end of the billing period, but before the occurrence of an event giving the right to maintain the average monthly salary, then the average earnings for the billing period will be increased.

- If the salary was increased after the occurrence of an event giving the right to maintain the average salary, then the average salary will be increased from the day the salary was increased until the day the right to maintain the average salary ends.

The very fact of a salary increase will entail an increase not only in official salaries, but also in other types of remuneration directly resulting from the size of the salary.