What payments are included in the calculation of vacation pay in 2020-2021?

According to the current labor legislation, each employee has the right to use annual leave (Article 114 of the Labor Code of the Russian Federation), which arises no earlier than 6 months after the start of work with a particular employer, which does not prevent its early provision (Article 122 of the Labor Code of the Russian Federation).

This leave time is subject to payment by the employer. The normal duration of vacation is 28 calendar days (Article 115 of the Labor Code of the Russian Federation), but it can be longer due to:

- additional leave given due to special working conditions (Articles 116–119, 348.10 of the Labor Code of the Russian Federation);

- non-working holidays falling within the vacation period (Article 120 of the Labor Code of the Russian Federation).

It is possible to split the vacation into several parts (Article 125 of the Labor Code of the Russian Federation), with each of them paid separately. If an employee quits without taking advantage of his right to annual leave, he is entitled to compensation for this (Article 127 of the Labor Code of the Russian Federation), the calculation of which is done according to the same rules as the calculation of regular vacation pay.

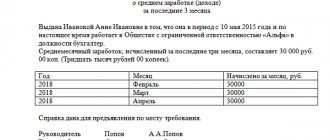

Payment for the period while on vacation is determined based on average earnings, the uniform general rules for calculating which are contained in Art. 139 Labor Code of the Russian Federation. The rules are as follows:

- The calculation of this earnings includes all payments provided for by the employer’s wage system, regardless of the source from which they are made.

- For the calculation, they take the actually accrued income and the actual work time for the 12 calendar months preceding the month of the event for which the average earnings are calculated. But the employer can approve a different period for calculation if this does not lead to a worsening of the employee’s situation.

- Average daily earnings are defined as the total amount of income for the calculation period (calculation period), divided by 12 months and by the average number of calendar days in a month (29.3).

- The responsibility for establishing the nuances of calculating average earnings is assigned to the Government of the Russian Federation.

Thus, bonuses included in the wage system (Article 129 of the Labor Code of the Russian Federation) are taken into account in income to calculate average earnings when calculating vacation pay. The list of bonuses taken into account in this system must be recorded in at least one of the following documents: (Article 135 of the Labor Code of the Russian Federation):

- contract of employment;

- wage regulations;

- regulations on incentives (bonuses);

- collective agreement.

For more information on the preparation of a document reflecting the remuneration system, read the article “Regulations on remuneration of employees - sample 2020-2021” .

When should you recalculate?

The need for recalculation may arise in the following cases:

- when indexing wages;

- when paying an annual bonus;

- when changing the duration of leave after going on it (due to sick leave, recall to work);

- counting error;

- provision of vacation in advance and subsequent dismissal of the employee - how to return overpaid vacation pay.

The rules for calculating vacation pay are set out in this article.

You can also calculate your vacation pay yourself using a convenient online calculator.

How to calculate when increasing salaries?

If an organization increases salaries, tariff rates, and prices, then the average salary for vacation pay must be recalculated in accordance with the rules set out in paragraph 16 of Resolution No. 922:

- If indexation occurred during the billing period (12 previous calendar months), then payments in the billing period accrued before the increase are increased in proportion to the indexation carried out (multiplied by a coefficient equal to the result of dividing the salary after the increase by the previously valid salary (tariff rate)).

- If indexation occurred after the billing period, but before the start of the vacation (that is, in the current month when vacation pay is calculated), the average earnings calculated by income increase by the indexation factor.

- If indexation occurred while you were on vacation, then only the average earnings for those days that fell on vacation from the date of increase to its end are increased by the indexation factor.

Examples

Increase in the billing period:

Initial data:

Popova goes on vacation from June 24, 2019 for 14 days. Salary increases - from 05/01/2019.

Salary before increase = 20,000, after = 22,000.

Calculation:

Since the salary increased in the billing period for (from 06/01/2018 to 05/31/2019), it is necessary to index the salary accrued for the period from 06/01/2018 to 04/30/2019.

Indexation coefficient = 22,000 / 20,000 = 1.1.

Salary after indexation = 20,000 * 1.1 = 22,000.

Vacation pay = 22,000 * 12 / (29.3 * 12) * 14 = 10,511.95.

Increase after the billing period before the start of the vacation:

Initial data:

Popova goes on vacation from June 24, 2019 for 14 days. The salary increases from 06/01/2019.

Salary for the month before indexation = 20,000. Indexation coefficient = 1.2.

Calculation:

Since the date of the salary increase falls after the billing period (from 06/01/2018 to 05/31/2019), but before the start of the annual vacation, you need to calculate the average earnings based on actual payments, and then multiply by the indexation coefficient.

Average daily earnings = (20,000 * 12) / (29.3 * 12) = 682.59.

Average daily earnings after indexation = 682.59 * 1.2 = 819.11.

Vacation pay = 819.11 * 14 = 11,467.57.

Increase during vacation:

Initial data:

Popova went on vacation from 06/24/2019 to 07/07/2019. Average daily earnings = 682.59.

The salary increases from 07/01/2019, coefficient = 1.2.

Calculation:

Recalculation is carried out only for the period from 07/01/2019 to 07/07/2019 - for 7 days.

Vacation pay accrued before vacation for 7 days = 682.59 * 7 = 4,778.13.

Vacation pay after indexation = 682.59 * 1.2 * 7 = 5,733.76.

You need to pay extra = 5,733.76 – 4,778.13 = 955.63.

Due to sick leave during vacation

If, while on vacation, an employee falls ill and takes sick leave, he has the right to extend the days of rest that coincided with the incapacity for work, or to transfer them to another time.

It is not always necessary to recalculate.

If an employee decides to extend the current vacation time, then no recalculation is made, since in fact the employee will take the full vacation granted to him, he will just return to work later.

The return to work date will be delayed by the number of days that coincide with the sick leave.

If an employee decides to postpone vacation days, then he returns to work on time, and the employer must resolve the issue of recalculating vacation pay:

- If rest days are provided in the current month, then there is no need to recalculate anything, since the billing period does not change.

- If vacation days are postponed to another month or a later time, for example, to next year, then vacation pay should be recalculated. When you subsequently go on annual leave, the calculation period will be different - 12 months preceding the month of registration of the vacation. Since the calculation is carried out for a different time, the average daily earnings may differ, therefore, recalculation is necessary.

Upon the employee’s return to work, the accountant must perform the following actions:

- Calculate how many days the employee did not use.

- Multiply the average daily earnings used for the calculation by the number of days off due to sick leave.

- To refund an overpayment - you can only deduct 20% from your salary; if this is not enough, then you can ask the employee to return the rest to the cash desk voluntarily.

- If the transfer is carried out for the coming months, then vacation pay can be recalculated. Calculate vacation pay for unused days due to sick leave, as well as vacation pay based on the new billing period. The difference is either retained or paid extra.

Example

Initial data:

Petrov's annual vacation is from June 01 to June 28, 2022. Monthly salary consists of salary = 20,000. June salary = 3,000.

The period from 06/01/2018 to 05/31/2019 has been fully worked out.

During the rest period, Petrov was sick for 5 days; these days, in agreement with the employer, it was decided to postpone these days from July 20 to July 25, 2022.

Calculation:

Average daily earnings for vacation in June 2022 = 20,000 * 12 / 29.3 * 12 = 682.60.

Vacation pay = 682.6 * 28 = 19,112.80.

Due to sick leave, Petrov actually took only 23 days off instead of 28, 5 days were postponed to the next month.

Overpayment = 682.6 * 5 = 3,413.

Average daily earnings for vacation in July 2022 = (20,000 * 11 + 3000) / (29.3 * 11 + 7 * 29.3 / 30) = 677.52.

Vacation pay for postponed days = 677.52 * 5 = 3,387.6.

Difference = 3413 – 3387.6 = 25.4 – must be withheld from the employee.

In case of early recall to work

If an employee returns to work ahead of time due to production needs, and the employee has given his consent to the early recall, then a recalculation must be made if the days not taken off are transferred to the next month or a later date.

The recalculation rules are similar to those indicated above when transferring rest days due to sick leave.

The accountant needs to calculate the part of the paid vacation pay that fell on the unused part of the vacation. This amount must be withheld from the employee.

If days not taken off are postponed to the coming months, then you can recalculate by calculating the amount of vacation pay for the postponed days and comparing them with the amount previously paid.

In case of payment of annual bonus

If an annual bonus is paid for the year preceding the year of registration of annual leave, then it must be taken into account when calculating vacation pay (clause 15 of Resolution No. 922).

If the employee has already managed to go on paid leave this year, and the average earnings do not include the annual bonus, then it must be taken into account later upon the fact of its accrual and payment.

In this case, the accountant must calculate the amount that needs to be paid in addition to previously paid vacation pay in connection with the payment of the annual bonus.

Example

Initial data:

Petrov took a vacation from 02/10/2019 to 02/23/2019 for 14 calendar days. Total earnings for the billing period amounted to 250,000.

Average daily earnings = 711.04 and vacation pay = 9,954.50.

In March 2022, a bonus for 2022 in the amount of 50,000 was accrued.

Calculation:

Since the annual bonus is assigned for 2022, which precedes the year in which annual leave is calculated, bonuses must be included in average earnings.

Since upon going on annual leave the bonus was not taken into account (since it had not yet been paid), it must be taken into account after accrual.

Average daily earnings including bonus = (250,000 + 50,000) / 29.3 * 12 = 853.24.

Vacation pay including bonus = 853.24 * 14 = 11,945.39.

The employee needs to be paid extra = 11,945.39 – 9,954.50 = 1,990.89.

What governs the process of including premiums in the calculation?

The provisions on the specifics of the procedure for calculating average wages, approved by Decree of the Government of the Russian Federation dated December 24, 2007 No. 922 (hereinafter referred to as Regulation No. 922), are devoted to the nuances that are important for calculating average earnings, and it is this that specifically talks about bonuses.

Prizes are mentioned in sub. “n” clause 2 of Regulation No. 922, which notes that these payments must be provided for by the current wage system. But the main points regarding bonuses are set out in paragraph 15 of Regulation No. 922. They prescribe bonus payments accrued:

- Monthly, take into account their actual amount, but not more than one for each month of the calculation period in relation to each of the bonus indicators.

- For a period of work of more than a month, include in the calculation in their actual amount in relation to each of the bonus indicators, if the period of their accrual is not longer than the duration of the calculation period, otherwise - in the amount corresponding to the monthly part of the bonus for each of the months constituting the calculation period.

- For the year preceding the event with which the calculation is associated, take into account their actual amount, regardless of when this payment is actually accrued.

We talk about other types of bonuses in the material “What types of bonuses and employee benefits are there?” .

The general rule for bonuses, established by clause 15 of regulation No. 922, is the need to take into account the amount of the bonus in proportion to the time actually worked in the calculation period, if this period has not been fully worked out or there are periods in it that are not subject to inclusion in the calculation (clause 5 of the regulation No. 922). This rule applies provided that at the time of calculating the bonus, the actual time worked was not taken into account. Bonuses that take into account the share of time worked usually (but not always) include those accrued over a certain period, for example, monthly, quarterly, annual.

The following periods are not subject to consideration when determining average daily earnings (clause 5 of Regulation No. 922):

- maintaining average earnings;

- being on sick leave;

- failure to perform work due to the fault of the employer or for reasons beyond the control of either party;

- use of additional days off intended for caring for disabled children;

- other paid or unpaid periods of release from work.

The proportion taking into account the share of time worked for the distribution of each bonus is calculated as the ratio of working days actually worked in the calculation period to the total number of working days included in this period (letter of the Ministry of Health and Social Development of the Russian Federation dated June 26, 2008 No. 2337-17).

What bonus rules are important for calculating holiday pay?

So, according to the rules stated above, the bonus should be taken into account when calculating vacation pay if it:

- taken into account in the wage system;

- named in the employer’s internal regulations reflecting the bonus procedure;

- accrued in the calculation period or must be taken into account (annual premium) in this period;

- cannot be regarded as a duplicate payment of the same frequency for a similar bonus indicator in the same period;

- recalculated in proportion to the share of time actually worked during the calculation period, if such recalculation is necessary in relation to it.

Of the duplicate payments, the current rules do not prevent the choice of the largest one. The rules for such a choice should be reflected in the internal regulations on bonuses.

The possibility of accepting bonuses in the calculation of average earnings in full or in part depends on three circumstances:

- whether the calculation period has been fully worked out;

- whether the entire period for calculating the premium is included in the calculation period;

- bonuses were calculated in proportion to the share of time worked or without taking this ratio into account.

conclusions

One-time bonuses paid to employees may be included in the calculation of holiday pay due if certain requirements are met.

In order for the amount of such a payment to be fully taken into account when calculating average earnings, the bonus period must be entirely included in the calculated annual interval (otherwise only its proportional share will be taken into account).

One-time payments for holidays are taken into account when calculating vacation pay according to the general rules specified for any one-time incentives.

Accounting for monthly and quarterly bonuses

Depending on the combination of the three above circumstances, the following options for accounting for both monthly and quarterly bonuses are possible:

- The full amount of the premium will be taken into account if:

- the entire calculation period has been worked out, and neither the period for which the bonus was accrued nor the fact of accounting (non-accounting) of time worked when calculating it will matter;

- the entire calculation period has not been worked out, but the entire period for calculating the bonus falls within it and when calculating the bonus, the actual time worked is taken into account;

- falls entirely into the calculation, but when calculating the bonus, the actual time worked is not taken into account;

- does not fall into the calculated one or is included in it partially, while the fact of accounting (non-accounting) of time worked does not play a role when calculating the bonus.

For more information on calculating quarterly bonuses, see the article “Calculation of quarterly bonuses for actual hours worked .

The total number of bonuses accrued in relation to the same bonus indicator for the entire calculation period cannot exceed:

- for monthly – 12 units;

- quarterly - 4 units;

- semi-annual - 2 units (paragraph 3, clause 15 of regulation No. 922).

Examples of accounting for quarterly and monthly bonuses when calculating vacation pay are available in the ConsultantPlus system. Get trial access to the system for free and proceed to calculations.

How is the annual bonus calculated?

The annual bonus is also included in the calculation, but there are special conditions for its accounting:

- it must relate to the year preceding the year of the event with which the calculation of average earnings is associated, i.e. if vacation pay is calculated in 2022, then the annual bonus for 2019 is taken into account;

- taking it into account is not linked to the actual time of accrual of this bonus, i.e. if at the time of calculating vacation pay the annual bonus has not yet been accrued and therefore cannot be taken into account in income, then after accrual of this bonus the average earnings will have to be recalculated and additional vacation pay will be paid to the employee (letter Rostruda dated 05/03/2007 No. 1253-6-1).

The options for taking the annual bonus into account are as follows:

- it is accepted in full if:

- the entire calculation period has been worked out (letter of Rostrud dated February 13, 2007 No. 317-6-1), while the fact of accounting (non-accounting) of time worked does not play a role when calculating bonuses;

- the calculation period has not been fully worked out, but the period for calculating the bonus absolutely corresponds to the calculation period and the bonus was accrued taking into account the actual time worked;

- absolutely corresponds to the calculated one, but the bonus was awarded without taking into account the actual time worked;

- does not correspond to the calculated one (letter of the Ministry of Health and Social Development of the Russian Federation dated 03/05/2008 No. 535-17), while the fact of accounting (non-accounting) of time worked does not play a role when calculating the bonus.

K+ experts have prepared an example of taking into account the annual bonus when calculating vacation pay. Get free trial access to the system and proceed to recommendations.

We talk about calculating the annual bonus in more detail in the article “How to calculate and account for the annual bonus?” .

Are bonuses taken into account when calculating vacation pay?

The basis for calculating vacation pay is the average salary for the previous period. It is formed by two main components: salary and additional payments. The task seems extremely simple: you just need to take the arithmetic average of income, that is, divide its amount by the number of months between vacations.

In practice, however, a number of difficulties may arise due to the peculiarities of the working conditions of each individual employee and the time characteristics of the period.

As everyone knows, bonuses can be one-time, monthly, quarterly and annual. A common situation is when an employee does not work the entire period, but only part of it. The reasons may be different: illness, absenteeism, downtime and, finally, a strike.

The general scheme for calculating monthly additional incentive remuneration is prescribed in the terms of the employment agreement (collective or individual employment agreement). Each organization has its own, and there is no point in considering their options in detail in this article. For example, an enterprise may provide bonuses for each employee who has no complaints or absenteeism in the form of a percentage or fixed increase in salary.

The quarterly bonus is calculated on the basis of wages for three months, if there are no gaps in the employee’s time sheet. In this case, only the months included in the period preceding the vacation are taken into account. For example, if an employee goes on vacation in the middle or end of March, then the quarterly bonus is accrued only for January and February. In this case, the bonus for the first quarter will be taken into account when calculating the next vacation pay.

Annual, quarterly, monthly and one-time bonuses included in the billing period are taken into account for the annual amount of vacation pay.

One-time and one-time bonuses: accounting features

One-time and one-time bonuses that meet the general necessary requirements for this type of payments (included in the remuneration system, recorded in internal regulations, accrued during the calculation period) are taken into account in the amount of income when calculating average earnings for vacation pay. In particular, it is possible to take into account in the calculation bonuses accrued for unearned achievements (for an anniversary or a holiday), if they meet these general requirements (letter of the Ministry of Finance of the Russian Federation dated March 22, 2012 No. 03-03-06/1/150, Ministry of Health and Social Development of the Russian Federation dated October 13, 2011 No. 22-2/377012-772).

One-time and one-time bonuses usually do not cover any period and therefore do not depend on the fact of coincidence or non-coincidence with the calculation period. In this case, they are confined only to the calculation period and, therefore, are taken into account in this calculation in full.

But if a one-time bonus is paid for the result of work carried out during a certain period, then when accounting for it, one must follow the rules in force for bonuses accrued for the corresponding period. However, for bonuses of this kind, the accrual periods may differ from the usual ones and may be, for example, six months or several years.

For semi-annual bonuses, the rules for taking into account will be similar to the rules applicable for monthly and quarterly bonuses. The difference will be that no more than two semi-annual bonuses can be included in the calculation period for the same bonus indicator.

If the premium is accrued for a period exceeding the value of the calculation period (1 year), then the rule will come into force that in each month of the calculation period it is necessary to take into account the amount of such premium in the amount attributable to its monthly part. Moreover, the premium amount determined in this way will be taken into account:

- in full if the entire calculation period has been completed;

- a volume proportional to the share of time actually worked in the calculation period, if this period is not fully worked.

Consequences of errors in calculating premiums

Errors in accounting for bonuses when calculating average earnings are divided into 2 types according to their impact on the amount of income determined for the billing period:

- inflating this income and, accordingly, the amount of vacation pay;

- underestimating this income and, accordingly, leading to the accrual of vacation pay in a smaller amount.

Overstatement occurs when the following is included in the calculation of premiums:

- not included in the wage system;

- not reflected in internal regulations;

- accrued outside the calculation period or not related (if the premium is annual) to this period;

- duplicating each other in terms of bonuses at the same frequency;

- not recalculated in proportion to the share of time actually worked in the calculation period, if this had to be done.

An understatement occurs if income does not include any of the premiums accrued during the calculation period. In addition, both overestimation and underestimation may be associated with incorrect calculation of the bonus amount or its incorrect recalculation in proportion to the time actually worked in the calculation period.

In any case, identified errors require corrections, since:

- overstatement unlawfully increases labor costs included in the costs that reduce the profit base;

- understatement infringes on the rights of the employee.

It is quite easy to correct an underestimation of the amount: you need to recalculate and pay the employee the missing amount. Overstatement amounts due to a counting error can be withheld from the employee’s salary (Article 137 of the Labor Code of the Russian Federation). But overstated amounts that are not related to such an error and are essentially explained by the employer’s violation of the law when calculating average earnings are quite difficult to get back from the employee: he may not agree to voluntary deduction and the judicial authorities are unlikely to recognize his obligation to do this , since he is not to blame for the current situation.

Read about what other deductions are possible from an employee’s salary in the material “Art. 137 Labor Code of the Russian Federation: questions and answers" .

Is a one-time payment not related to wages included in the average salary calculation base?

Such bonuses are also issued at some enterprises. They are issued by management for the anniversary of a distinguished employee, professional or other holiday. They are accrued irregularly. These payments, which are not included in the calculation of average earnings, are not provided for by the current wage system and are issued in separate orders.

It should be remembered that formulations like “... to award bonuses in connection with the 60th anniversary and for outstanding performance” arouse increased interest of the inspection authorities, especially if the order concerns the managers of the enterprise.

Recalculation of vacation pay in case of payment of a bonus for a holiday or some other significant date (that is, if it is not related to the performance of work duties) is not required.

Results

Bonuses accrued in the 12-month period preceding the month of calculation of vacation pay must be taken into account when determining the income involved in calculating average earnings, if these bonuses are provided for by the current remuneration system. However, the process of including the entire bonus amount or a certain part of it in the calculation requires compliance with a number of rules, depending on the full (incomplete) working out of the calculation period, the coincidence (non-coincidence) of the bonus accrual period with the calculated one, and the accounting (non-accounting) of time worked when calculating the bonus.

Read the latest news about personal income tax on bonuses in the articles:

- “The Ministry of Finance has returned to the issue of personal income tax on bonuses”;

- “How to correctly reflect a one-time bonus in 6-NDFL (nuances).”

Sources:

- Labor Code of the Russian Federation

- Decree of the Government of the Russian Federation of December 24, 2007 N 922

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

What are bonuses for?

Employees who are not privy to the intricacies of accounting sometimes think that the boss can give a bonus at his own discretion. This is partly true, but not every “incentive payment” (as bonuses are defined in Article 129 of the Labor Code of the Russian Federation) is included in wages and affects its average value. Russian legislation provides for a different approach to remuneration and monetary remuneration.

The award is given for specific labor achievements or performance results that directly or indirectly affect the economic performance of the enterprise. It is included in the actual amount of the employee’s salary and is provided for by the remuneration system adopted in this organization (Labor Code of the Russian Federation, Article 139, part two).

The calculation of average wages is regulated by Decree of the Government of the Russian Federation No. 916 of November 11, 2009. Subparagraph “n” of this legal act makes reference to the term “remuneration system”. It means a method of determining the amount of remuneration due to an employee based on labor costs and economic results.

The payment system is specifically established by a collective agreement (agreement, local act, which most often means an employment contract).

Thus, only payments that directly stimulate work activity are considered included in wages along with the official salary.