The purpose of introducing a new report from organizations to the Pension Fund

The new SZV-M report was put into effect not so long ago: in 2016, Resolution of the Board of the Pension Fund N 83p was issued, which provided for such an obligation for employers.

The purpose of this report is to provide information to the Pension Fund about insured persons. The fund needed such information because the indexation of insurance pensions for age pensioners was suspended, which in turn required tracking working pensioners. That is, at its core, the SZV-M report is necessary for the fund to implement anti-crisis measures in the field of pension provision.

Obligation to provide information in the SZV-M form to the Pension Fund of Russia

Immediately after the resolution of the Board of the Pension Fund was issued on the provision of information about insured persons, policyholders had an additional obligation - to submit a report in the SZV-M form. Since almost all employers are policyholders, regardless of the number of employees in the company, such reporting is provided for joint stock companies, limited liability companies and individual entrepreneurs.

Important ! However, it should be remembered that individual entrepreneurs who have no employees at all and conduct all their business activities individually are not required to provide such a report.

Procedure for filling out the SZV-M report

The form for providing information on insured persons is approved by the above-mentioned resolution. However, the Pension Fund services do not provide any explanation on how to fill out such a report, emphasizing that the SZV-M form includes the necessary instructions for completion.

So, this document consists of four parts:

- Information about the policyholder;

- Information about the reporting period;

- Information about the type of report: original, supplementary, or canceling;

- Information about the persons insured by the policyholder.

All sections are required to be completed. However, in section 4 in the tabular section, the employer may not indicate the employee’s TIN if he does not know such data.

Important ! When filling out the form, you should never make mistakes, since the PFR inspection officer may fine you.

What else needs to be filled out?

If a woman goes on maternity leave in the middle of the reporting period, then information about her work experience in the reporting year must be recorded two or even three times:

- From January 1 (or from the date of commencement of work experience at this enterprise, if the woman got a job with the employer in the reporting year) to the last day of work before maternity leave.

- From the first to the last day of vacation according to accounting (if the vacation does not transfer to the next reporting period).

- From the first day of parental leave up to 1.5 years until December 31 of the reporting year. This period follows about.

If a woman, before going on maternity leave, was on sick leave due to temporary disability, which is not uncommon for a pregnant woman, this period is also allocated in a separate line and regardless of the number of days paid by the employer and the Social Insurance Fund.

In practice, situations often arise when an expectant mother, before going on maternity leave, decides to use her current paid leave. This time is noted in the SZV-STAZH form with the code “DLOTPUSK”.

When filling out more than one line for an employee of an organization, the data in columns 2-5 does not need to be repeated; data on length of service should be indicated sequentially, observing chronology.

The need to indicate information about maternity leavers in SZV-M

When compiling a SZV-M report, quite often the compiler has the question of whether it is necessary to include information about maternity leavers in the report. Moreover, by maternity leave, we can mean both women who went on maternity leave and employees who are on maternity leave for up to one and a half or three years of their children.

As mentioned above, the SZV-M report includes information on insured persons. At the same time, no matter what leave, called maternity leave, a woman goes on, she does not cease to be an insured person, therefore, this question clearly has a positive answer - women on maternity leave must be included in the SZV-M report.

However, not all maternity leavers are insured persons. So, if an employee who went on maternity leave temporarily arrived in our country and was a highly qualified specialist, she is not an insured person, which means there is no need to provide information about her to the Russian Pension Fund. In this case, such an employee does not need to be included in the tabular part of the SZV-M report.

Who are maternity leavers?

The definition of “maternity leave” is derived from the word “maternity leave,” because a decree was the name given to the legislative act that in 1917 introduced paid leave for women in Russia associated with the birth of a child, which allowed her to retain her job. The full name of this document sounds like the decree “On Maternity Benefits”. Accordingly, the leave granted under it (maternity leave) applied only to the period of time that is now called maternity leave.

Parental leave was added to maternity leave only in 1956 (Resolution of the USSR Council of Ministers of October 13, 1956 No. 1414). Its initial duration was 3 months, and then increased to 1 year (in 1968), to 1.5 years (in 1982) and to its current value of 3 years (in 1989).

Until 1982, this leave was not paid. After it was increased to 1.5 years, they began to pay for 1 year of this time. And since 1989, a modern procedure has been in force, in which the first 1.5 years of 3 years of vacation are subject to payment (Clause 1, Article 11.1 of the Law of December 29, 2006 No. 255-FZ “On Compulsory Social Insurance...”).

Parental leave is often also called maternity leave. However, it is incorrect to apply such a definition to him - its establishment has nothing to do with the decree, which served as the source of the words “maternity leaver” and “maternity leaver.”

Moreover, the right to register it arises not only from the child’s mother, but also from any other person (including males) who actually cares for him (Article 256 of the Labor Code of the Russian Federation). Maternity leave and care leave also differ in the procedure for their documentary support (sick leave is required to provide maternity leave), and the procedure for calculating and paying benefits due.

Procedure and deadlines for submitting SZV-M

There are two ways to submit reports:

- In paper form;

- In electronic form.

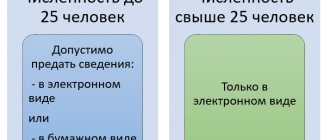

Moreover, the first method is “dying out” as electronic services are gaining momentum. In addition, not all employers can use the paper format, but only those whose staff does not exceed 25 people. For such small companies, there are several options for providing a “paper” SZV-M report:

- Personal visit to the territorial body of the Pension Fund;

- Transfer of the report with a trusted person;

- Sending a report by mail.

Organizations with a staff of 25 or more people are required to provide a report exclusively through electronic document management with the document certified by an electronic digital signature. If for some reason an employer with more than 26 employees provides a paper report to the Pension Fund, he will be fined.

There are certain deadlines for submitting information about insured persons in the SZV-M form. Initially, in 2016, ten days of the month following the reporting month were allocated for the preparation and provision of such a report. However, from 2022 this period has been extended by five days, and now reports must be submitted no later than the 15th day of the month following the reporting month. If the 15th falls on a weekend, the deadline is moved to the next closest working date.

Thus, the deadlines for submitting SZV-M in 2022 are as follows:

- for January – February 15;

- for February – March 15;

- for March – April 15;

- for April – May 16;

- For May – June 16;

- For June – July 16;

- For July – August 15;

- For August – September 17;

- For September – October 15;

- For October – November 15;

- For November – December 17;

- For December – January 15, 2022.

In case of untimely submission of reports on insured employees, the organization risks receiving a fairly large fine.

Monthly report SZV-M

It would seem that what could be simpler than the SZV-M report? There are no complex calculations or comparative tables in it. But in practice, it turns out that when the deadline approaches, the question arises whether or not to include this or that employee in the report.

Every month, starting from 2016, organizations and individual entrepreneurs (policyholders) must submit information on all insured individuals in relation to all insured persons working for them (including persons with whom a civil law contract has been concluded), if insurance premiums are paid for them to the Pension Fund of Russia.

These are general concepts for generating the SZV-M report. But there are cases in which it is unclear whether an employee should be included in the report or not. Let's look at some of them.

In July, the employee goes on vacation with subsequent dismissal. The dismissal date will be in August. The organization calculated the employee and issued him documents before the vacation. This employee must be included in the report for August, because it includes all employees with whom an employment or civil contract was in force during the month. And the date of termination of the employment contract is considered to be the last day of vacation; accordingly, in August the contract with the employee was still in force.

The organization employs foreign citizens and stateless persons. If employment or civil law contracts have been concluded with them, then a report must be submitted on them. Exceptions are made for foreigners or stateless persons temporarily staying in the territory of the Russian Federation, who belong to the category of highly qualified specialists. Such employees are not subject to registration in the compulsory pension insurance system, and there is no need to submit a report on them.

If employees work part-time, then they need to be included in the report, because they have an employment relationship with the employer, and employment contracts have been concluded with them.

An employment contract or a civil contract with an employee was concluded on the last working day of the reporting month. Despite the fact that the work has not yet been completed, an acceptance certificate has not been issued, payment has not been made, but the contract was concluded during the reporting period. This means that this employee must be included in the report. In a situation where the contract is terminated on the first day of the reporting month, you must also submit the SZV-M form for this employee.

If an employee is on leave without pay for more than one month, but an open-ended employment contract has been signed with him , then the employment contract in this case continues to be valid. Accordingly, this employee must be included in the report. The same applies to those who were on sick leave due to temporary disability, on maternity leave, on parental leave, as well as during periods of downtime, absenteeism and other similar situations.

If the organization has no employees, and the functions of the manager are performed by the only founder. This situation has been controversial for some time. But by letter of the Ministry of Labor of Russia dated 03/16/2018 No. 17-4/10/B-1846, brought to the attention of the Pension Fund Branches by letter of the Pension Fund of the Russian Federation dated 03/29/2018 No. ЛЧ-08-24/5721, changes were made for which it is necessary to submit a report.

But if there were payments to an employee outside the framework of an employment or civil contract , the subject of which is the performance of work or the provision of services, then there is no need to submit a report for such employees. Such cases include, for example, bonuses to former employees of the organization.

At the same time, the simplicity of the report does not relieve responsibility for its late submission or submission with incomplete or unreliable information. In these cases, a fine of 500 rubles is provided for each insured person.

As you can see, despite its apparent simplicity, there are many nuances in SZV-M. If you have your own examples on this topic, write in the comments, we’ll discuss.

Victoria Kurakhtenkova - salary expert at the Salary 360° project

Consulting on the correctness of payroll calculations for more than two years.

Read other articles by the author on our blog:

- Clinical examination: changes in the Labor Code of the Russian Federation

- Employment at 0.5 rate

The procedure for correcting errors in SZV-M

It is strictly forbidden to correct errors in the SZV-M form itself. In order to correct incorrectly entered data, you need to make a new report and indicate the corresponding value in the third section:

- DOP is a complementary form of SZV-M. Applies if you forgot to indicate an employee in the report. In this case, the report should contain only information about the forgotten employee.

- OTMN is a canceling version of the report. It is used if an extra employee was included in SZV-M by mistake. In this case, it is necessary to indicate information about such an employee in section 4.

How to make changes to SZV-M when changing an employee’s last name

The SZV-M report indicates the full name of the employee, SNILS and Taxpayer Identification Number. Pension and tax codes are issued once and do not change. But an employee can change his last name

The information in the report and in the database of the Russian Pension Fund (PFR) must match, then there will be no errors during verification. If the Pension Fund of Russia does not yet have information about the change of the employee’s surname, then the old data must be indicated in the SZV-M.

The employee himself can change personal data in the Pension Fund database through his personal account on the fund’s website. Or the employer can do this: submit an application in the ADV-2 form, approved by Resolution of the Pension Fund Board of September 27, 2022 No. 485p.

The law does not establish a period during which it is necessary to provide information about a change of surname to the Pension Fund. The main thing is that the information in the SZV-M report coincides with what is in the database on the date of submission of the report.

The updated SNILS will serve as confirmation that the information about the name in the Pension Fund of Russia database is now up-to-date. Since 2022, plastic SNILS cards will not be issued, but an employee can provide an electronic document or a printout. After this, you can indicate a new surname in the SZV-M.

Answers to frequently asked questions

Question N1: Hello! For a couple of months, our organization was provided accounting services under a contract by a woman who was an individual entrepreneur. We always included information about it in the SZV-M report. In the first month there were no comments from the Pension Fund, but in the second month we were fined. Not long ago she went on maternity leave. Do we need to indicate information about it in the SZV-M report?

Answer: Firstly, information about such an employee did not need to be indicated in the SZV-M earlier, since this woman is your counterparty, not an employee. If you did this, then it was a mistake and the Pension Fund of Russia did not notice it the first time. Secondly, an individual entrepreneur providing services to an organization is not a person insured by the organization, be it a maternity leaver or a working person, which means that information about him does not need to be included in the SZV-M report. An individual entrepreneur must independently inform the Pension Fund about himself and his employees.

Employee maternity leave and SZV-M

Each accounting document has its own subtleties.

But with the advent of a new document, new questions arise: how to fill it out, who fills it out and where to submit it. The emergence of a new form for the SZV-M pension fund raised many questions. So, let's figure it out from the very beginning. How to reflect workers on maternity leave in SZV-M, do they need to be included in the general list?

Is it necessary to enter information about maternity leavers into SZV-M?

Maternity maids are employees on maternity leave. These include:

- Women on maternity leave.

- Employees who are on vacation and caring for children. In this case, maternity leave can be taken out not only by the mother, but also by the father, and the child’s immediate or distant relatives (depending on the circumstances). (Ministry of Health and Social Development Ave. No. 1012 N).

Employers submit information about those employees who officially work in the organization or work on the basis of a contract of any nature.

If such an agreement is concluded with a maternity leaver, then throughout the entire period of child care, the employer is obliged to enter information about her in the SZV-M form . If an employee is on maternity leave, it means that the person is listed as working for that company. And it doesn’t matter whether the employee was paid for this period.

Who should fill out the SZV-M report

This form was developed by the Pension Fund of the Russian Federation. It reflects all information about employees. The last name, first name, patronymic of the employees, their SNILS, and if data is available, the TIN are indicated. It looks like this:

Only employers who have employees or have entered into at least one employment contract fill out such a document. This may be a contract for one day or a one-time performance of work, but if a contract of a legal nature is concluded, then it is necessary to submit the SZV-M form to the pension fund.

You will have to submit and fill out the form until the organization closes. Even if there are no more employees left, but the company continues to operate, the form is filled out for one head of the company. In this case, there is no need to be confused: an individual entrepreneur who does not have employees does not submit a report! So, who submits the SZV-M report:

- An individual entrepreneur who has entered into an employment contract with at least one employee.

- Organizations and firms that have also entered into contracts and have one or more employees on staff.

- When signing contracts for one day or for seasonal work.

- All employers who have employees.

For details on filling out and submitting the SZV-M, watch the video:

What will need to be indicated in the SZV-M for an employee on maternity leave?

As already written, it does not matter who takes parental leave (father, mother, relative or guardian), the following individual data must be entered into the form:

- Full name of the employee on maternity leave.

- SNILS of a maternity leave person.

- TIN, if this data is known to the employer.

In addition, in a certain section of the RSV-1 form you will need to indicate:

- “Children” - when providing maternity leave for up to 1.5 years to the child’s parent (father or mother).

- “For children” - when providing maternity leave for up to 3 years to the mother or father.

- “Children” - when providing maternity leave for up to 3 years to any other relative of the child or his guardian.

Maternity leave in the RSV-1 report is noted in section 6.8, and the code “DECREE” is indicated there.

The pension fund did not consider it necessary to notify the employer whether to include maternity leave in the reporting.

Therefore, we can safely say that employees on maternity leave should be included in the SZV-M report. Special sections were allocated for them in the form. Maternity leavers are those employees who are listed as working at an enterprise or organization and whose employment relationship has not been terminated.

It is important for the responsible person to remember that any error or inaccuracy in indicating the staffing table may lead to penalties. Therefore, you should not forget any of your employees, no matter where they are. Once there is an employment agreement, it means that the employee is registered with the company. And individual accounting is kept according to it too.

The report is submitted to the regulatory authority no later than the 15th. This reporting is monthly, so every month on the 15th the document is first checked through the program (you can download it on the Pension Fund website) and then the document is sent to the fund.

The workplace of the responsible person must be prepared for sending such documents; appropriate programs must be installed so that documentary reporting can be sent on time and without technical problems.

Let us remind you once again that failure to submit the SZV-M form on time will result in a fine of 500 rubles for each employee. And if it is a large organization, then the fine will be large, and it can only be challenged in court.