What is a waybill

A waybill is a primary document that records the vehicle’s mileage. Based on this document, gasoline consumption can be determined.

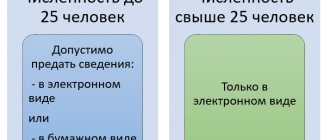

Organizations for which the use of vehicles is the main activity must use the PL form with the details specified in Section I of Order No. 368 of the Ministry of Transport dated September 11, 2020.

The document came into force on 01/01/2021. Main innovations:

- A waybill is required for any vehicle operation, regardless of the type and nuances of transportation.

- A new detail “Transportation information” has been introduced.

- It is necessary to indicate the brand of the trailer.

- The responsible person is obliged to indicate the time the vehicle leaves the line and the time it returns.

From 09/01/2021, waybills are filled out taking into account the new rules for technical control of vehicles, approved. by order of the Ministry of Transport dated January 15, 2021 No. 9.

For organizations that use a car for production or management needs, it is possible to develop a PL taking into account the requirements of the Law “On Accounting” dated December 6, 2011 No. 402-FZ.

Do you doubt the correctness of the posting or write-off of material assets? On our forum you can get an answer to any question that raises your doubts. For example, in this thread you can clarify what the basic fuel consumption rate is recommended by the Ministry of Transport.

An example of an order for approval of a DP can be found here.

In practice, organizations often use PLs that were approved by Decree of the State Statistics Committee of the Russian Federation dated November 28, 1997 No. 78. This resolution has PL forms depending on the type of vehicle (for example, Form 3 - for a passenger car, Form 4-P - for a truck) .

For a sample of filling out the updated waybill, see here .

You can learn about filling out waybills taking into account the latest innovations in the Ready-made solution from ConsultantPlus. Trial access to the legal system is free.

and you can get a prompt answer on filling out the waybill in our discussions in the VK group .

Waybills must be recorded in the waybill register. Accounting for waybills and fuels and lubricants is interconnected. In organizations that are not motor transport by nature of activity, PLs can be drawn up with such regularity that it is possible to confirm the validity of the expense. The main thing is to confirm the expenses. Such conclusions are contained, for example, in the letter of the Ministry of Finance of Russia dated 04/07/2006 No. 03-03-04/1/327, the resolution of the Federal Antimonopoly Service of the Volga-Vyatka District dated 04/27/2009 No. A38-4082/2008-17-282-17-282.

Read about waybills for individual entrepreneurs in the article “What are the features of a waybill for individual entrepreneurs (form)?”

Accounting for fuel consumption in the waybill

If we analyze the PL forms contained in Resolution No. 78, we will see that they contain special columns designed to reflect the turnover of fuel and lubricants. This indicates how much fuel is in the tank, how much has been dispensed and how much is left. Using simple calculations, the amount of fuel used is determined.

If we turn to Order No. 368 of the Ministry of Transport, then among the mandatory details of the submarine there will not be a requirement to reflect the movement of fuel. In this case, the document must contain speedometer readings at the beginning and end of the journey, which will allow determining the number of kilometers traveled by the vehicle.

When the PL is developed by the organization independently and it does not contain information on the use of fuels and lubricants, but contains only data on the number of kilometers, the standard volume of used fuels and lubricants can be calculated using the order of the Ministry of Transport of Russia dated March 14, 2008 No. AM-23-r. It contains fuel consumption standards for different brands of vehicles and formulas for calculating consumption.

Thus, on the basis of the PL, either the actual or standard write-off of fuel and lubricants is calculated. The data calculated in this way is used for reflection in accounting.

However, the use of PL to account for fuel consumption is impossible in some cases. For example, when chainsaws, walk-behind tractors, and other similar special equipment are refueled with gasoline. In these cases, a fuel and lubricants write-off act is applied.

A sample act for writing off fuel and lubricants can be viewed and downloaded on our website using the link below:

Nuances of fuel cards

Features of the use of fuel cards depend on the terms of the agreement with the organization issuing the fuel card. Here are examples of additional options when using fuel cards in addition to paying for fuel at gas stations, depending on the terms of a specific agreement:

What are the advantages of a fuel card:

You will learn about the procedure for working with advance reports from the article “Features of advance reports in accounting .

The organization that issues gasoline cards provides access to a personal account where you can monitor and manage fuel cards: change spending limits for each card, receive detailed information in real time on expenses (at which gas station, in what quantity and for what fuel were produced expenses), receive invoices for advance payments.

Accounting for fuel and lubricants

Like all inventories, fuel and lubricants are accounted for in the accounting department at actual cost. Expenses that are included in the actual cost are indicated in Section II of FSBU 5/2019 “Inventories”.

Important! Since 2022, inventory accounting has been carried out in accordance with the new federal standard FSBU 5/2019 “Inventories” (it replaced PBU 5/01). ConsultantPlus experts spoke in detail about how the rules for accounting for inventories have changed. You can see the explanations if you get trial access to the legal system. It's free.

Acceptance of fuel and lubricants for accounting can be carried out on the basis of gas station receipts attached to the advance report (if the driver purchased the fuel in cash) or on the basis of coupon stubs (if gasoline was purchased using coupons). If the driver purchases gasoline using a fuel card, then accounting for fuel and lubricants on fuel cards is carried out on the basis of a report from the company issuing the card. Write-off of fuel and lubricants can be carried out using the following methods (section III):

- at average cost;

- at the cost of the 1st time of acquisition of inventory (FIFO).

There is another way to write off - at the cost of each unit. But in practice, it is not applicable for writing off fuel and lubricants.

The most common way to write off fuel and lubricants is at average cost, when the cost of the remaining material is added to the cost of its receipt and divided by the total amount of the remainder and receipt in kind.

Fuel cards were issued to employees: how to take them into account

Next, fuel cards are handed over to employees. To do this, you need an order to assign a fuel card to a specific driver. Orders do not have standardized forms. An order to attach a fuel card is created on the usual enterprise order form, which is also used in other cases. You can download an example of an order for free from the link at the beginning of our article.

In addition, it is necessary to fill out a register for issuing fuel cards, according to which fuel cards are issued to employees against signature. The organization develops the format of the journal independently. You can download an example of a fuel card logbook form for legal entities at the beginning of our article for free.

The transfer of fuel cards is done as follows:

After the costs of fuel cards are included as expenses, their accounting in the accounting department does not stop. Gasoline cards are accounted for in account 012, which is located behind the balance sheet.

If the cards were received free of charge and no entries reflected in the balance were made, then when transferring the gas cards to employees, there is also no need to make any additional entries.

As a result, in both cases, after the transfer of fuel cards, there is an off-balance sheet account 012, which reflects the fuel cards assigned to the organization.

Accounting for fuel cards in 1C 8.3 is carried out using normal operations:

- posting cards for refueling - “Receipt” functionality;

- issuing cards for refilling - “Requirements-invoices” functionality.

Write-off of gasoline using waybills (tax accounting)

If everything is quite simple with the write-off of fuel and lubricants in accounting, then the recognition of these expenses in tax accounting raises questions.

1st question: in what expenses should fuel and lubricants be taken into account? There are 2 options here: material or other expenses. According to sub. 5 p. 1 art. 254 of the Tax Code of the Russian Federation, fuels and lubricants are included in material costs if they are used for technological needs. Fuel and lubricants are included in other expenses if they are used to maintain official vehicles (subclause 11, clause 1, article 264 of the Tax Code of the Russian Federation).

IMPORTANT! If the main activity of an organization is related to the transportation of goods or people, then fuel and lubricants are material costs. If vehicles are used as service vehicles, then fuel and lubricants are other expenses.

The second question: should we normalize the costs of writing off fuel and lubricants within the framework of tax accounting? The answer to this can be found by linking the details of the waybill and legislative norms:

- The PL calculates the actual use of fuel and lubricants. The Tax Code of the Russian Federation does not contain direct indications that expenses for fuel and lubricants should be taken into tax accounting only according to actual standards.

- The PL contains information only about the actual mileage. However, fuels and lubricants can be calculated according to order No. AM-23-r, paragraph 3 of which states that the standards established by it are also intended for tax calculations. The Ministry of Finance of Russia in its letters (for example, dated 03/22/2019 No. 03-03-07/19283, dated 06/03/2013 No. 03-03-06/1/20097) confirms that order No. AM-23-r can be used to establish justification of costs and determine the cost of fuel and lubricants in tax accounting according to standards multiplied by mileage.

IMPORTANT! In tax accounting, fuels and lubricants can be taken both according to actual use and according to the quantity calculated based on the standards.

In practice, a situation is possible when an organization uses transport for which fuel consumption standards are not approved in Order No. AM-23-r. But in paragraph 6 of this document there is an explanation that an organization or individual entrepreneur can individually (with the help of scientific organizations) develop and approve the necessary standards.

The position of the Ministry of Finance of Russia (see, for example, letter dated June 22, 2010 No. 03-03-06/4/61) is that before developing standards for the write-off of fuel and lubricants in a scientific organization, a legal entity or individual entrepreneur can be guided by technical documentation.

There are no explanations in the Tax Code of the Russian Federation on how to act in such a situation. In cases where an organization independently established standards for writing off fuel and lubricants and, having exceeded them, took into account the amount of excess fuel use in tax accounting, the tax inspectorate may not recognize this as an expense. Accordingly, additional income tax may be charged. In this case, the court may well support the position of the inspectorate (see, for example, the resolution of the Administrative Court of the North Caucasus District dated September 25, 2015 in case No. A53-24671/2014).

Read about the amount of fines for not having a waybill in this article .

Why do you need a fuel card?

A fuel card is also called a gas card and a petrol card.

A fuel card for legal entities is a method of paying for fuel and lubricants at gas stations. Fuel cards for individuals can be used in a similar way, however, in our review we will focus on the features of working with fuel cards for individual entrepreneurs and legal entities.

Let's look at how a fuel card works. An organization or individual entrepreneur enters into an agreement for fuel cards with the company that issues them. This could be a fuel supplier or an intermediary. It is possible to receive several cards under one agreement.

The organization accepts fuel cards for registration in the accounting department (we will describe how to do this below) and issues them to employees. As a rule, these are drivers, but a refueling card can be obtained by any employee who, as part of their work duties, drives a car and fills it with gasoline. This could be a director, manager, courier, and so on. In other words, not only transport organizations can apply for a fuel card, but also any others that use transport for business purposes.

Employees pay at gas stations not with cash or corporate cards, but with fuel cards. Thus, you can use your fuel card like any other bank card - as a means of payment.

At the end of the month (or at other intervals), the organization issuing fuel cards submits a report on the funds spent, as well as a complete package of closing documents, which includes invoices.

We wrote about VAT on advance reports in the article “The procedure for reflecting VAT on advance reports in accounting .

An example of writing off fuel and lubricants using waybills

One of the most common types of fuel and lubricants is gasoline. Let's consider the example of purchasing and writing off gasoline.

Pervy LLC (located in the Moscow region) purchased 100 liters of gasoline in September at a price of 38 rubles. without VAT.

At the same time, at the beginning of the month, the LLC had a stock of gasoline of the same brand in the amount of 50 liters at an average cost of 44 rubles.

Gasoline in the amount of 30 liters was used to refuel a VAZ-11183 Kalina car. The organization uses a car for official transportation of management personnel.

The organization uses average cost estimates for materials.

Accounting for fuel and lubricants upon admission

| Dt | CT | Amount, rub. | Operation (document) |

| 10 | 60 | 3 800 | Gasoline received credit (TORG-12) |

| 19 | 60 | 760 | VAT reflected (invoice) |

We calculate the average write-off cost for September: (50 l × 44 rubles + 100 l × 38 rubles) / (50 l + 100 l) = 40 rubles.

Option 1. Accounting for fuel and lubricants when writing off after the fact

The following marks are made in the submarine: fuel in the tank at the beginning of the voyage - 10 liters, issued - 30 liters, remaining after the voyage - 20 liters.

We calculate the actual use: 10 + 30 – 20 = 20 liters.

Amount to be written off: 20 l × 40 rub. = 800 rub.

| Dt | CT | Amount, rub. | Operation (document) |

| 26 | 10 | 800 | Write-off of gasoline (accounting statement-calculation) |

Option 2. Accounting for fuel and lubricants when writing off according to standards

Mileage marks are made in the PL: at the beginning of the voyage - 2,500 km, at the end - 2,550 km. This means that 50 km have been covered.

In paragraph 7 of Section II of Order No. AM-23-r there is a formula for calculating gasoline consumption:

Qн= 0.01 × Hs × S × (1 + 0.01 × D),

where: Qн — standard fuel consumption, l;

Hs - basic fuel consumption rate (l/100 km);

S—vehicle mileage, km;

D is the correction factor (its values are given in Appendix 2 to Order No. AM-23-r).

According to the table in sub. 7.1 by car make we find Hs. It is equal to 8 liters.

According to Appendix 2, coefficient D = 10% (for the Moscow region).

We calculate gasoline consumption: 0.01 × 8 × 50 × (1 + 0.01 × 10) = 4.4 l

Amount to be written off: 4.4 l × 40 rub. = 176 rub.

| Dt | CT | Amount, rub. | Operation (document) |

| 26 | 10 | 176 | Write-off of gasoline (accounting statement-calculation) |

Since the car is used as a company car, the cost of accounting for fuel and lubricants in the tax accounting of fuel and lubricants will be recognized as other expenses. The amount of expenses will be equal to the amounts recorded in the accounting records.

Fuel cards have arrived: how to take them into account

So, we have described all the advantages of fuel cards for legal entities. How to apply for such a card and how to keep records of fuel cards in an organization?

To begin with, we select the fuel card issuer that suits us according to the terms and conditions and conclude an agreement with it.

We receive fuel cards in the required quantity. The card can be provided either free of charge or for a fee.

Acceptance of fuel cards from the issuing organization occurs according to the act of acceptance and transfer of fuel cards.

Accounting for fuel cards in accounting depends on whether the price of the fuel card is highlighted as a separate line in the documents transferring them to the organization or not.

Let’s say that the issuer of fuel cards transferred ten cards for refueling under the act with an allocated price of 120 rubles per piece (including 20% VAT - 20 rubles). The invoice is included in the package of documents provided.

Fuel cards can be used for more than 12 months, their cost is less than 40,000 rubles. We take them into account on account 10 “Materials”. We make the following transactions:

Read about the new FSBU 6/2020 in our article “Procedure for accounting for fixed assets according to FSBU 6/2020” .

Now let’s assume that the value assessment of petrol cards upon transfer has not been carried out. This fact does not negate the need to keep accounting of fuel cards. If their cost is not indicated, then we will keep records of fuel cards on an off-balance sheet account, for example 012, at a conditional valuation of 1 ruble per 1 piece. In this case, upon receipt of cards, the following posting is made: