Settlement procedure

The basic conditions for mutual offset are contained in the Civil Code of the Russian Federation. These include:

- Presence of counterclaims. Offsetting is carried out in the presence of at least 2 agreements, so that both organizations are simultaneously a debtor and a creditor. It is impossible to offset if only one company has debt.

- Uniformity of requirements. This refers to a uniform method of repaying debt, for example, in cash, despite the fact that the organization actually pays by supplying goods or providing services.

- Validity and indisputability of requirements. Settlement is not possible in case of assignment of claims to third parties and disputes regarding the fulfillment of obligations.

- Legality of requirements. Art. 411 of the Civil Code of the Russian Federation contains an open list of grounds on which it is unacceptable to carry out offsets. There should also be no restrictions or prohibitions in concluded agreements.

- Written registration of mutual settlement. The Civil Code does not contain instructions on how to fill out the netting act; therefore, it is drawn up taking into account the requirements for primary accounting documentation. This means that it must necessarily reflect the following: the parties, the grounds for offset (numbers of contracts, work completion certificates, etc.), the amount of offset and the date of final write-off of mutual claims.

- The deadline for fulfilling obligations has arrived. Settlement is possible only for those contracts where the performance period has already arrived or is not defined. In case of different deadlines, the offset is carried out after the later one. Settlement cannot be carried out against future deliveries of goods or provision of services.

If these conditions are met, in order to carry out mutual offset, it is necessary to draw up a corresponding act (agreement) and provide the other party with a copy of it.

A sample settlement agreement can be found on our website.

A detailed algorithm of actions for unilateral and bilateral offset is described in detail in the Ready-made solution from ConsultantPlus, which you can view by getting free access.

According to clause 4 of the information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 29, 2001 No. 65, a document notifying about the test must be received. The act (agreement) of offset must be signed by persons authorized to sign documents by power of attorney or order. If the document is signed by persons who do not have these powers, transactions on mutual offsets may be considered void.

The date of offset is considered to be the date of signing the act or the date specified in the document. It is this that is subsequently reflected in accounting and affects taxation. Situations not prescribed by law or contract are resolved in accordance with business customs.

Read about the nuances of preparing primary documents in the article “Primary document: requirements for the form and the consequences of violating it.”

How can a simplifier carry out an act of mutual settlement with an organization in the general mode?

Question from Clerk.Ru reader Natasha (Novy Urengoy)

I work as an accountant, subject to taxation under the simplified tax system of 6%. Organization N entered into an agreement (services) with us, including VAT. My organization M entered into an agreement (services) excluding VAT. Now organization N wants us to carry out an act of mutual offset. As I understand it, organization M must return the VAT amount to the bank, or am I wrong? Could there be another way out in this situation? And why does organization N include two contracts in the reconciliation report? These are different accounts, is this correct?

A netting agreement, as a rule, is concluded when its participants intend to pay off their accounts payable at the expense of receivables, without resorting to cash settlements.

The interpretation of the concept of offset of mutual claims is given in Art. 410 of the Civil Code of the Russian Federation. The obligation is terminated in whole or in part by offsetting a counterclaim of the same type, the due date of which has come or is not specified or determined by the moment of demand.

The legislator has established a number of restrictions when conducting offset operations (Article 411 of the Civil Code of the Russian Federation). In addition, claims are not offset (the obligation does not terminate) if the organization received from the counterparty a notice of offset of a claim for which the statute of limitations (three years) has expired. In this case, the party that received the application for offset is not obliged to send the counterparty a notice that he has missed the statute of limitations (the limitation period is applied by the court if there is an application when considering the relevant dispute) (clause 10 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 29, 2001 N 65 “Review practice of resolving disputes related to the termination of obligations by offsetting counterclaims of the same kind").

From Art. 410 of the Civil Code of the Russian Federation it follows that only two subjects of civil law relations can be participants in the offset of counterclaims. However, in practice, organizations quite often use multilateral offsets (with the participation of three or more parties), because a vicious circle of debt obligations is a fairly common phenomenon.

For reference.

Actions of citizens and legal entities aimed at establishing, changing or terminating civil rights and obligations, in accordance with Art. Art. 153 and 154 of the Civil Code of the Russian Federation are recognized as transactions. They can be one-, two-, or multilateral (treaties). According to paragraph 1 of Art. 420 of the Civil Code of the Russian Federation, a contract is an agreement between two or more persons to establish, change or terminate civil rights and obligations. Based on clause 2 of Art. 421 of the Civil Code of the Russian Federation, the parties may enter into an agreement, both provided for and not provided for by law or other legal acts.

Thus, a multilateral netting agreement has the right to exist as an agreement, although not directly provided for by civil law, but at the same time not contradicting it.

The legality of multilateral offset will also not raise doubts if the following conditions are met:

— the obligations presented for offset must be homogeneous;

- by the time the offset is carried out, the repayment period of the obligations must have arrived, either the period for such repayment is not determined, or it is determined by the moment of demand.

For reference.

Homogeneous obligations are those that are reduced to one equivalent, usually monetary.

Multilateral offset must necessarily be carried out in the opposite direction to the flow of the debt incurred, and for an allowable amount. The legal structure of a multilateral offset is the mutual repayment of obligations and claims of its participants; therefore, persons who are not obligated to any of the participants in the offset cannot participate in a multilateral offset. The implementation of such an offset is possible only if there is a circular debt among its participants, therefore, each of the participants in the offset is associated with other mutual claims (See Resolutions of the Presidium of the Supreme Arbitration Court of the Russian Federation dated May 30, 2000 N 6088/99 and the Federal Antimonopoly Service of the Ural District dated July 30, 2001 N F09-1214 /2001-GK in case No. A60-411/2001).

Having agreed to offset claims, organizations must sign an act (agreement or any similar document) about the offset. Since the form of such a document has not been established, when drawing it up it is necessary to be guided by the requirements for primary documents. They are indicated in paragraph 2 of Art. 9 of Law No. 129-FZ “On Accounting”. In addition, the act as a settlement document must be signed by the chief accountant (clause 3 of Article 7 of Law No. 129-FZ).

It will not be superfluous if the document drawn up by the parties contains information about the state of settlements between the parties at the beginning of the offset. In this case, you need to indicate the amount of debt, as well as details of contracts, primary documents and invoices. Such papers confirm the transactions on the basis of which the debt was formed. Next, it is necessary to reflect the amount of the offset and the state of settlements between the parties after the offset.

Reflecting the operation of offsetting mutual claims in accounting, as a rule, does not cause difficulties. In particular, if the offset terminates the obligations arising under contracts of purchase and sale, paid services, performance of work, i.e. when obligations are reflected in accounts 60 “Settlements with suppliers and contractors” and 62 “Settlements with buyers and customers”, the following entry is made in accounting: Dt. 60 – Kt. 62.

Regarding VAT accounting, it is recommended to consider the following. On January 1, 2009, changes made to the Tax Code by Federal Law No. 224-FZ of November 26, 2008 came into force. These changes abolished the obligation of taxpayers in non-monetary settlements to transfer funds to each other in the amount of refundable VAT, i.e., para. 2 clause 4 art. 168 and paragraph 2 of Art. 172 of the Tax Code of the Russian Federation. Therefore, at present, the termination by offset of counter homogeneous claims does not lead to the emergence of any additional obligations for VAT accounting: tax is calculated at the time of sale of goods, works, services, property rights, and the presentation of amounts of “input” VAT for deduction - taking into account the general rules provided for in Ch. 21 Tax Code of the Russian Federation.

However, if through offset the debt associated with the purchase of goods (work, services) registered before January 1, 2009 is repaid, one should be guided by the requirements of the Tax Code, the version of which was in force at that time.

In any case, in the act of offsetting mutual claims, the VAT amounts must be highlighted as a separate line (clause 4 of Article 168 of the Tax Code of the Russian Federation).

It’s very easy to get personal advice on any tax online - you just need to fill out a special form . Every day two or three of the most interesting questions will be selected, the answers to which you can read in Tatyana Potapova’s consultations.

Hello Guest! Offer from "Clerk"

Online professional retraining “Accountant on the simplified tax system” with a diploma for 250 academic hours . Learn everything new to avoid mistakes. Online training for 2 months, the stream starts on March 1.

Sign up

Reflection of offsets in accounting

The offset procedure does not depend on the taxation system and is shown in the same way in accounting. The differences lie in how it is reflected in tax accounting.

So, in accounting, the offset of claims is reflected in subaccounts containing information about accounts payable and receivable. Most often these are accounts 60 “Settlements with suppliers and contractors”, 62 “Settlements with buyers and customers”, 76 “Settlements with various debtors and creditors”.

However, claims are rarely equivalent in monetary terms, so offsets are often carried out to partially write off obligations, and the remaining amount of debt is repaid with separate documents or money.

The posting reflecting the offset is generated on the day of signing the act or on the date specified in the document and has the form: Dt 60 (62, 76) – Kt 62 (60, 76) - partial (full) repayment of the counter obligation by offsetting mutual claims.

See also: “Dt 60 and Kt 60, 50, 51, 76, 62 in accounting (nuances).”

Procedure for recognizing revenue and expenses during netting

When receivables are repaid, enterprises using a cash accounting system generate revenue. At the same time, for organizations with the object “income”, it is necessary to take into account the following features:

- The date of recognition of income is the day the act is signed or indicated in the document.

- Organizations that use “income” as the object of taxation recognize revenue in terms of offset.

- The balance of outstanding debt, if any, is recognized as income after repayment in cash or other form.

For enterprises using the “income minus expenses” scheme, the date of offset is simultaneously the day the income is received and the expense is incurred. The amounts are taken into account in equal amounts. When using the “income minus expenses” accounting scheme, the organization must take into account the condition of applying the simplified tax system, which concerns the right to reflect expenses in accounting only after the actual fulfillment of obligations to the second party - the sale of goods (works, services).

Offsetting under the simplified tax system and tax accounting

With the object “income”, this operation is reflected in the book of income and expenses as receipt of revenue. The date indicated is the moment of repayment of obligations, that is, either the date provided for in the act (agreement) on netting (this will be the basis for the operation), or the date of signing this act (agreement). This conclusion is confirmed by the letter of the Ministry of Finance dated December 28, 2011 No. 03-11-06/2/185, as well as the current judicial practice.

The obligation to accept the offset for accounting also arises if there is no act. Then the document confirming this business transaction will be a reconciliation act or any other suitable primary accounting document.

If the income from the operation was not taken into account, then it is highly advisable to submit an updated declaration under the simplified tax system and make an additional payment, otherwise the organization will face sanctions under Art. 122 Tax Code of the Russian Federation .

The act of offset in itself documents only the write-off of mutual claims and does not lead to the emergence of income or expenses. However, according to Art. 346.17 of the Tax Code of the Russian Federation, the income of enterprises under special tax regimes can be recognized not only as the receipt of funds, but also as the repayment of receivables in alternative ways, for example, by terminating a counter-obligation. Thus, in the book of income and expenses, writing off claims in any form will be reflected as income of the enterprise.

You can find out how simplifier expenses are taken into account when offsetting in the Ready-made solution from K+, having received trial access to the system.

Read more about income simplification in the article “STS-income in 2019-2020 (6 percent): what you need to know?”

Mutual settlement

Mutual settlement is a procedure for offsetting counter obligations of the parties to a transaction, in which cash settlements under two independent agreements are closed in a non-cash manner, where both entrepreneurs participate simultaneously. That is, at the time of mutual settlement, both appear as both a debtor (debtor) and a creditor in relation to each other, and each party incurs expenses and income. The amounts of expense and income are equal amounts. The following are considered mandatory conditions for conducting a settlement transaction: - obligations have arisen between the parties under at least two agreements under which mutual claims have arisen; - one party, according to the concluded agreement, must in fact fulfill obligations to the other - provide a service or ship goods; — the due date for payment, stipulated by the terms of the contract, that is, it is impossible to offset future debts; — the agreement does not contain a prohibition on non-monetary settlements between the parties. If the debtor fails to repay the entire amount through mutual offset, then the balance of the debt is listed as the seller's accounts payable. To carry out mutual settlement, mutual consent of both parties to the agreement is required. Based on the reconciliation acts signed by the parties and the agreement on netting, the parties enter into an agreement on netting or sign an act of netting. Is it necessary to reflect in the book of income and expenses the number and date of the document confirming the settlement of claims transaction? The Law indicates that this is a mandatory procedure. Offsetting in the book of income and expenses will be accepted by tax authorities only if it is completed correctly. If the act of offset does not fall into the book of income and expenses, then the transaction is considered invalid by the tax service. Each of these documents is signed by the authorized persons of the parties in two copies, one for each party, and after signing, the mutual settlement transaction is reflected by the parties in accounting in 1C “Accounting” (the accountant will be told how to correctly set off in order to reflect in the book of income and expenses “ cribs” posted on the official websites of the Federal Tax Service). For posting, we enter the netting act in 1C 8.3, for example, so that the completion of the transaction is reflected in the book of income and expenses. Managers of organizations should carefully consider the procedures for mutual settlements, because the Law provides for some restrictions on such transactions. A ban on concluding such a procedure is sometimes specified in the transaction agreement! Tax authorities study mutual settlement agreements very carefully, because such an agreement, if incorrectly drawn up, can be recognized by the tax inspectorate as an exchange agreement, which implies completely different tax and accounting records.

An example of netting using the simplified tax system

Let's look at the reflection of offsets in accounting and tax accounting using an example.

Yasen LLC applies a simplified “income” taxation system. From April 5, it leased the production premises to Lipa LLC for a period of 11 months. And on April 10, an agreement was concluded that Lipa LLC would provide transport services for the period until December 31 of the current year.

In June, the enterprises decided to offset mutual claims and found out that, according to the agreements, the accounts payable of Yasen LLC amounted to 42,000 rubles. (under the contract for the provision of transport - 58,000 rubles (under the lease agreement). On June 15, an act of offset was signed in the amount of 42,000 rubles.

For 3 months (April, May, June), the accountant of Yasen LLC did the following for each wiring transportation service:

Dt 44–Kt 76/2 - transport costs are reflected.

As a result, as of June 15, Yasen LLC accumulated accounts payable to Lipa LLC on account 76.

As well as Yasen LLC revenue was recognized:

Dt 62/3–Kt 90/1 (revenue from renting out production premises) - 58,000 rubles.

After signing the netting act, the accountant of Yasen LLC made the following entry:

Dt 76/2–Kt 62/3 (offset of claims in accordance with the act dated June 15, 2021) - 42,000 rubles.

Since the company “Yasen” LLC is on the simplified tax system “income”, when filling out the book of income and expenses, the accountant reflected in the income the revenue in the amount of partial write-off of mutual claims.

After Lipa LLC deposited the balance of the debt into the settlement account, the accountant of Yasen LLC reflected it in his accounting with the entry: Dt 51–Kt 62/3 - 16,000 rubles, and also included it in income when calculating the single tax under the simplified tax system.

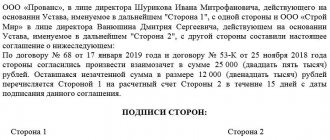

Sample act of offset

Act No.__

on carrying out mutual settlement between Yasen LLC and Lipa LLC.

Ulyanovsk June 15, 2022

As of the date of drawing up this act, there are mutual obligations between the parties:

- LLC "Lipa" (tenant) has before LLC "Yasen" (lessor) under an agreement dated 04/05/2021 No. __ (act of acceptance and transfer of production premises dated 04/05/2021 No. __) in the amount of 58,000 rubles.

- Yasen LLC (customer) has before Lipa LLC (contractor) under contract dated 04/10/2021 No. __ (Acceptance and transfer certificates for services rendered dated 04/15/2021 No. __, dated 05/15/2021 No. __, dated 06/15/2021 No. __) in the amount of 42,000 rubles.

The parties agreed to mutually offset the debt in the amount of 42,000 rubles, thereby fully repaying the obligations of Yasen LLC to Lipa LLC.

Yasen LLC Lipa LLC

_______________ _____________

M.P. M.P.

The article “Which object under the simplified tax system is more profitable - “income” or “income minus expenses”?” will help you make the right choice of taxation system under the simplified tax system.

Frequently asked questions ↑

Next, we will consider the main issues related to the implementation of mutual offsets:

- Does offset apply to the income of the enterprise?

- What does contraction have to do with VAT?

- How to display the repayment of counter homogeneous claims in 1C.

Is offset income under the simplified tax system?

The question that the repayment of accounts receivable is income was discussed above (see the subheading “Reflection in accounting ...”). ,

The profit received is recognized by taxpayers on the day the act is signed (Article 346.17 of the Tax Code of the Russian Federation).

In this case, the repayment of the buyer's receivables is considered the seller's income, regardless of which taxation method he chose.

As a result, in the book of income and expenses, it is necessary to make an appropriate display of the received amount of debt that was paid by the counterparty.

Whereas the buyer, who is a single tax payer at a rate of 15%, recognizes expenses in the form of closed accounts payable.

Relationship with VAT

When filling out the netting act, it is imperative to indicate the total amount of debt of the parties to the agreement, including VAT. You also need to indicate the amount of debt that is canceled by offsetting with the allocated VAT.

Video: accounting for costs of legal systems under the simplified tax system

To make it clearer how accounting entries are made in this case, it is necessary to consider a specific example.

Enterprise “X”, on the basis of an agreement dated 04/20/2014, shipped products to IP Sviridov K.L. in accordance with the invoice dated 05/01/2014. The total amount for the goods including VAT (30 thousand rubles) was 330 thousand rubles.

In turn, individual entrepreneur K.L. Sviridov, on the basis of an agreement dated February 20, 2014, conducted marketing research for the X enterprise.

The work completion certificate was signed by the parties on June 1, 2014. The total amount for services including VAT (21.6 thousand rubles) amounted to 141.6 thousand rubles.

On the day of signing the act, IP Sviridov K.L. issued an invoice to enterprise “X”. In accordance with the terms of the existing agreements, the parties signed an act of offset of mutual claims dated July 20, 2014, in the amount of 141.6 thousand rubles.

The entrepreneur paid the difference in the amount of debt under the agreement dated April 20, 2014 3 days after signing the act.

The amount of payment including VAT (17,127 rubles) amounted to 188.4 thousand rubles. Transactions are displayed in the accounting of enterprise “X” as follows.

20.04.2014:

| Dt 62 Kt 90 (330 thousand rubles) | Goods shipped, including VAT |

| Dt 90 Kt 68 (30 thousand rubles) | The VAT amount for the above products is displayed |

01.06.2014:

| Dt 26 Kt 60 (120 thousand rubles) | Market research services received are displayed |

| Dt 19 Kt 60 (RUB 21.6 thousand) | VAT on the above services is displayed |

20.07.2014:

| Dt 60 Kt 62 (141.6 thousand rubles) | Settlement has been made |

| Dt 68 Kt 19 (21.6 thousand rubles) | VAT on services provided is deductible |

Reflection when working with 1C

When using the 1C Accounting 8 program, the taxpayer’s income and expenses are taken into account on the basis of standard accounting documents.

The formation of a ledger of income and expenses according to the simplified tax system occurs in the “Reports” menu – “Income ledger…”. Here the results of its completion are checked. A special 1C accounting mechanism has been introduced for this operation.

This tool is quite useful for taxpayers who use “Income minus expenses” as a tax object. Recording of offsets also occurs in the ledger of expenses and income.

Photo: interface in 1C program

To display the organization’s costs, you need to open the corresponding menu:

Photo: interface in 1C program

Results

Mutual obligations to each other in business are not uncommon. Mutual offset allows organizations to pay each other, while saving time and money on bank commissions. Accounting for offset transactions is the same for all tax regimes. For a company using simplified taxation system (STS) income, offset means the receipt of revenue, which must be taken into account for tax purposes.

Sources:

- Tax Code of the Russian Federation

- Civil Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Registration of the test

For offset, a statement from one party is sufficient. Therefore, the offset will be considered to have taken place from the moment your counterparty or you receive written notice of the offset. This notification can be made in any form.

If you are the one sending the notice of set-off, be sure to keep proof that your buyer received the notice. For example, this could be a postal notification of the delivery of a letter with an inventory of the attachments. Otherwise, the counterparty will be able to demand payment for goods (work, services), the obligation to pay for which you consider terminated. He will also be able to collect from you the contractual penalty or interest for the use of other people's funds.

Advice

To avoid controversial situations, it is better to draw up a bilateral settlement document (agreement, act, protocol). Before drawing up this document, we recommend that you reconcile mutual settlements.

Both the unilateral notification and the offset agreement must indicate:

— names of the parties;

— details of the documents on the basis of which mutual obligations arose that are subject to offset (contracts, invoices, acceptance certificates for work performed or services rendered);

- the amount of amounts to be counted.

Otherwise, the offset may be declared invalid, which will entail the consequences already mentioned above.

Attention! Termination of the buyer's obligation to pay for goods (works, services) by offset is equivalent to their payment.

The agreement might look like this.

Agreement

on termination of obligations by offsetting mutual claims

Moscow July 7, 2010

Limited Liability Company "Romashka" represented by General Director E.A. Romanov, acting on the basis of the Charter, on the one hand, and the Limited Liability Company "Vasilek" represented by director V.P. Vasiliev, acting on the basis of the Charter, on the other hand, referred to as the “Parties”, have entered into this agreement as follows.

1. Obligation of Romashka LLC to pay for the work performed by Vasilek LLC under contract No. 57/10 dated 06/11/2010 (acceptance certificate for work performed dated 06/17/2010), worth 30,000 (Thirty thousand) rubles. is terminated by offsetting the counterclaim to Vasilek LLC for payment for goods supplied by Romashka LLC under supply agreement No. 46/P dated 06/04/2010 (consignment note No. 448 dated 06/18/2010), worth 90,000 (Ninety thousand) rubles.

2. After the entry into force of this agreement, the debt of Romashka LLC under contract No. 57/10 dated June 11, 2010 in the amount of 30,000 (Thirty thousand) rubles. is considered repaid, and the debt of Vasilek LLC under supply agreement No. 46/P dated 06/04/2010 is recognized as equal to 60,000 (Sixty thousand) rubles.

3. The remaining debt in the amount of 60,000 (Sixty thousand) rubles. Vasilek LLC undertakes to transfer to the current account of Romashka LLC before 07/30/2010.

4. This agreement is drawn up in 2 copies having equal legal force, one for each of the parties.

5. The Agreement comes into force from the moment it is signed by the Parties.

Romashka LLC Vasilek LLC

General Director: Director:

Determining the date of offset of mutual claims

Sometimes it is not easy to determine the date of set-off if the parties, for example, acted as follows:

- One of the parties first sent a statement of offset;

- Then the parties entered into an agreement on the stage-by-stage offset of mutual claims, in which they specified the terms and amounts of offset and indicated that each time the offset was carried out, a bilateral act would be signed;

- Subsequently, offsets were carried out repeatedly (with a frequency of approximately once a month) with the execution (signing) of an offset act.

In this case, what date is considered the offset date? The opinions of regulatory and judicial authorities are shown in Table 1

| No. | Document wording | Explanatory document |

| 1 | “...a transaction for the offset of counterclaims of the same type is considered completed at the moment the counterparty receives an application for offset, despite the fact that the obligations are considered terminated on a different date.” | Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated February 19, 2013 N 8364/11 in case N A40-158480/09-44-854 |

| 2 | “...for tax purposes, on the date of signing the act of offsetting mutual claims, the taxpayer recognizes income from the performance of the duties of an agent.” | Letter of the Ministry of Finance of the Russian Federation dated September 23, 2013 N 03-11-06/2/39230 |

Thus, despite the fact that the offset transaction is considered completed at the time of filing an application by one of the parties, from the point of view of the Tax Code, the date of determination of income will be considered the date of signing the offset act. If there are several such acts, there will be several dates for determining income under the simplified tax system.

It is necessary to take into account that the date of offset may be separately agreed upon by the parties in the act of offset and may differ from the date of signing the act.

Types and features of netting

- Unilateral netting

- Bilateral offset

When conducting a unilateral offset, a statement from one of the parties is sufficient. After receiving the application, the parties clarify mutual obligations, usually drawing up a reconciliation act for mutual settlements to confirm them.

When conducting a bilateral offset, the parties express mutual agreement on its conduct. It is also carried out on the basis of reconciliation of mutual settlements. The forms of expressing consent to set off may vary.

Usually only the deed of offset is signed. In complex cases, which are characterized by phased and partial offsets, an offset agreement or contract may be drawn up.