Regulatory regulation of write-off of expired goods

The ban on the sale of expired goods is established by Art.

472 of the Civil Code of the Russian Federation. When applying the norms of this article, trading companies should also take into account the fact that they need to sell a product in such a way that the consumer has time to use it (consume it) after purchase. The Guide from ConsultantPlus will help you correctly specify the condition on the shelf life of the goods in the supply contract and avoid risks. Get trial access to the system for free and proceed to the material.

The requirements of the Civil Code are supplemented by the provisions of the Law “On Protection of Consumer Rights” dated 02/07/1992 No. 2300-1. In particular, in Art. 5 of Law No. 2300-1 establishes the types of goods for which the manufacturer is obliged to establish and indicate an expiration date:

If the expiration date is not indicated directly on such a product, it cannot be sold either.

Expired goods or goods without a mandatory expiration date may be returned to the supplier, recycled or destroyed.

NOTE! Since December 9, 2018, a ban has been introduced on agreements between retail chains and suppliers on reimbursement, return or replacement of quality food products with a shelf life of no more than 30 days. For goods with a long shelf life, such conditions are acceptable, but only if they were not imposed on the seller. In addition, the supply agreement cannot include a provision for the seller to reimburse the costs of disposal or destruction of unsold goods (see Law No. 446-FZ dated November 28, 2018).

About the nuances of accounting for VAT when returning goods to a supplier, read the article “What is the procedure for accounting for VAT when returning goods to a supplier?”

IMPORTANT! If the goods are not returned to the supplier, then they will require a conclusion from the relevant state supervision authority (sanitary, veterinary, merchandising, etc.) on what should be done with these goods. It is allowed to destroy without expert assessment:

- food products that have obvious signs of spoilage and may be dangerous when consumed;

- goods whose owner cannot confirm their exact origin.

For the procedure for writing off commodity losses, see here.

Write-off of goods that have become unusable: postings

The write-off of damaged and missing goods is carried out on the basis of data from an inventory carried out to document the fact of theft or damage. If such a product belongs to a category for which there are norms of natural loss, then within their limits the cost of damaged/missing inventory items can be written off as costs.

In addition, accounting records will vary depending on whether the company has a reserve for writing off losses and whether those responsible for the damage/shortage have been found.

When writing off goods, the postings will be as follows:

| Operations | D/t | K/t |

| Write-off of damaged goods or shortages | 94 | 41 |

| If there is a shortage of retail goods, the markup on them is reversed | 41 | 42 |

| Write-off of inventory items within the limits of natural loss (NU): | ||

| - due to the loss reserve | 96 | 94 |

| - for sales costs | 44 | 94 |

| Write-off of goods exceeding EU norms | ||

| - for expenses if it is impossible to identify the culprit | 91/2 | 94 |

| - at the expense of the perpetrators, assessing the amount of damage at market value | 73 | 94 |

| The difference between the amount of damages recovered and the booking price is taken into account and written off to other income | 73 98 | 98 91/1 |

| If the amount of shortage/damage exceeds the EU norms, the VAT previously accepted for deduction must be restored | 94 | 68 |

Preparation of primary accounting reports for expired goods

The write-off procedure is determined by the company's management. Internal company regulations should establish:

- the procedure for identifying and withdrawing from sale expired goods;

- the procedure for sending them for recycling or destruction;

- the procedure for documenting the entire process.

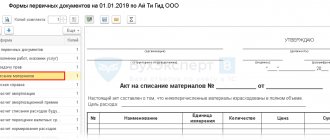

As a general rule, the identification of goods unfit for sale is activated. The act indicates: names of goods (according to accounting nomenclature), quantity, location at the time of expiration. A separate section of the act must indicate the further fate of expired goods - disposal, destruction or return to the supplier.

The unified album of primary forms (approved by Goskomstat on December 25, 1998) for such purposes proposes the TORG-15 form for recording the fact of damage and TORG-16 for recording withdrawal from circulation and the decision on destruction or disposal.

Look for forms and samples of filling out forms for write-off in the articles:

- “Unified form No. TORG-15 - form and sample”;

- “Unified form No. TORG-16 - form and sample”.

In this case, the business entity is allowed to develop forms for writing off inventory items independently, taking into account the requirements for the preparation of primary documents, which are specified in Art. 9 of the Law “On Accounting” dated December 6, 2011 No. 402-FZ.

The transfer of goods for disposal to a specialized company is formalized in the same way as sales (invoice, UPD, etc.).

Inventory: identifying shortages and damage

Detection of the fact of shortage (damage) of goods is the basis for conducting an inventory (Part 3 of Article 11 of the Law of December 6, 2011 No. 402-FZ). An exception to this rule is the shortage (damage) of goods identified before the goods are registered. The fact of shortage (damage) can also be revealed during the inventory process carried out for other reasons.

At its discretion, the organization can conduct an inventory of goods at any time. However, there are cases when inventory must be carried out without fail:

- before preparing annual financial statements;

- when changing materially responsible persons (for example, warehouse manager, storekeeper);

- when facts of theft, abuse or damage are revealed;

- in the event of force majeure (for example, natural disasters);

- during reorganization or liquidation of the organization;

- in other cases provided for by law (for example, when selling an enterprise as a property complex) (Article 561 of the Civil Code of the Russian Federation).

Such rules are established in paragraph 27 of the Regulations on Accounting and Reporting.

For information on what conditions must be met when conducting an inventory of goods, see the table.

To document the inventory of goods, you can use the following standard forms:

- inventory list of inventory items (form No. INV-3);

- act of inventory of shipped inventory (form No. INV-4);

- inventory list of inventory items accepted for safekeeping (form No. INV-5);

- act of inventory of inventory items in transit (form No. INV-6).

When registering inventory results, the following documents must be drawn up:

- matching statement in form No. INV-19;

- statement of accounting of the results identified by the inventory, according to form No. INV-26.

This is stated in section 2 of the instructions approved by Decree of the Goskomstat of Russia dated August 18, 1998 No. 88, and in Decree of the Goskomstat of Russia dated March 27, 2000 No. 26.

For more information on filling out these forms, see the table.

Typical write-off transactions

To better understand the principle of using a particular account, it is best to consider situations using an example.

Example

On March 31, 2021, we conducted an inventory at the central warehouse of the supermarket chain. Based on the results of the inventory, the following was revealed:

- a batch of rice cereal with an expiration date until 03/20/2021 worth 12,000 rubles;

- a batch of buckwheat with an expiration date until 04/05/2021 worth 16,000 rubles.

- Based on the expiration dates, it was decided to withdraw both batches from sale.

An entry was made in the accounting: Dt 41 / Expired goods (hereinafter referred to as ISG Goods) Kt 41 / Goods for sale

- Both goods had no external signs of damage. Therefore, samples of both cereals were sent for examination.

Expenses for expert analysis (1,770 rubles including VAT) and the cost of transferred samples were reflected in accounting:

Dt 91 Kt 76 — 1,500 rub. — examination;

Dt 19 Kt 76 - 270 rub. — VAT on examination services;

Dt 91 Kt 41 / ISG products - 100 rub. — cost of samples (a sample was taken from each product costing 50 rubles, 2 × 50 = 100).

- Based on the results of the examination, buckwheat groats were allowed to be disposed of, while rice groats were ordered to be destroyed.

3.1. A third-party organization was hired to destroy the rice grains, and they billed RUB 2,360 for their services. (including 360 rubles VAT). The accountant recorded the following entries:

Dt 94 Kt 41 / ISG products - 11,950 rub. (12,000 – 50);

Dt 91 Kt 94 — 11,950 rub. — the cost of destroyed goods is written off;

Dt 91 Kt 76 — 2,000 rub. — expenses for the services of a third-party destruction organization are taken into account;

Dt 19 Kt 76 — 360 rub. — VAT on services provided by a third party.

3.2. Buckwheat was sold to an animal shelter for 8,000 rubles. The following entries were made in accounting:

Dt 62 Kt 90 - 8,000 rub. — revenue from sales accrued;

Dt 90 Kt 68 / VAT - 1,220 rub. — VAT on sales;

Dt 90 Kt 41 / ISG products - RUB 15,950. (16,000 – 50).

Accounting: markdown

If an organization plans to discount damaged goods, then make the following entries in accounting:

Debit 94 Credit 41

– the cost of damaged goods is reflected (based on the act in form No. TORG-15);

Debit 94 Credit 42

– the trade margin attributable to damaged goods is reversed (if goods are recorded at sales prices).

For the convenience of reflecting the markdown of goods to account 41, open a separate sub-account, for example, “Goods subject to markdown”.

Debit 41 subaccount “Goods subject to markdown” Credit 94

– goods subject to discounting have been capitalized (at market value, taking into account their physical condition);

Debit 44 Credit 41 subaccount “Goods subject to markdown”

– samples of damaged goods were submitted for examination (if examination is necessary for the sale of damaged goods);

Debit 44 Credit 60

– expenses for conducting an examination are reflected (if an examination is necessary for the sale of damaged goods);

Debit 62 Credit 90-1

– revenue from the sale of goods at a discount is reflected;

Debit 90-2 Credit 41 subaccount “Goods subject to markdown”

– the cost of discounted goods is written off (the cost at which they were capitalized);

Debit 90-3 Credit 68 subaccount “VAT calculations”

– VAT is charged on the sale of discounted goods (if the organization is a VAT payer);

Debit 90-2 Credit 44

– costs associated with sales are included in the cost of sales (if an examination is required to sell damaged goods).

If damaged goods cannot be used (sold) in the future, reflect their value in accounting on account 94 “Shortages and losses from damage to valuables” in correspondence with property accounting accounts (account 41). Moreover, if goods are recorded at sales prices, then simultaneously with the fact of damage to goods being reflected on account 94, the trade margin attributable to damaged goods and previously recorded on account 42 must be reversed. This is stated in the instructions for using the Chart of Accounts (account 94, 41, 42). When reflecting the fact of damage to goods in accounting, make the following entries:

Debit 94 Credit 41

– damage to goods is reflected;

Debit 94 Credit 42

– the trade margin attributable to damaged goods is reversed (if goods are recorded at sales prices).

This procedure for reflecting damage to goods in accounting is reflected in subparagraph “b” of paragraph 29 of Order No. 119n of the Ministry of Finance of Russia dated December 28, 2001.

Tax nuances of writing off goods

Subp. 49 clause 1 art. 264 of the Tax Code of the Russian Federation provides for the inclusion in expenses for calculating income tax of other expenses related to production and sales. Expenses must meet the criterion of economic justification in accordance with Art. 252, 265 Tax Code of the Russian Federation.

If identifying, removing from circulation, recycling or destroying expired goods is a legal responsibility of the seller, the results of these operations may reduce the tax base for income taxes. These conclusions are also confirmed by letters from the Ministry of Finance, for example dated 04/23/2019 No. 07-01-09/29286, dated 07/09/2018 No. 03-03-06/1/47374.

This also implies the possibility of deducting VAT paid for services related to the examination, recycling or destruction of expired goods.

What about VAT, which you deducted on the item being written off? Does it need to be restored? This issue is controversial. You can find out how law enforcement practice is developing in this regard from the analytical collection from K+, having received free trial access to the system.

How to write off a defective product from a buyer if the supplier refuses to accept it?

Our trade organization accepted a defective product from the buyer, but our supplier for some reason did not accept it. That is, this product is stuck in our warehouse

According to the norms of Russian legislation (clause 1 of Article 475 of the Civil Code of the Russian Federation), if the defects of the goods were not specified by the seller, the buyer to whom the goods of inadequate quality were transferred has the right, at his choice, to demand from the seller:

- A proportionate reduction in the purchase price;

- Free elimination of product defects within a reasonable time;

- Reimbursement of your expenses to eliminate product defects.

And in the event of a significant violation of the requirements for the quality of the goods, the buyer, on the basis of clause 2 of Art. 475 of the Civil Code of the Russian Federation also has the right to demand the replacement of goods of inadequate quality with goods that comply with the contract (clause 2 of Article 475, clause 1 of Article 476, clause 1 of Article 503 of the Civil Code of the Russian Federation, Article 12, clause 1 of Article 18 Law RF dated 02/07/1992 N 2300-1).

As follows from your comments, the retail trade did just that, completed all the necessary documents and returned the defective goods to the wholesale trade.

In turn, wholesale sellers have the right to make claims to their supplier - he is obliged to accept the defect and compensate for losses (i.e. return or offset funds against other supplies, as well as reimburse transportation costs, examination or disposal costs, if the agreement to dispose of or destroy the goods on site by the wholesaler).

Inspectors always pay attention to such moments during inspections. And if the organization received compensation for the defect, then the expenses do not raise questions for the tax authorities when checking the tax base for income tax.

If a defect was identified by the buyer of a product after its receipt, in order to document the fact of an external defect, the following must be received from the buyer:

- An act on identified defects in the quality of the goods, drawn up in any form, indicating all mandatory details in accordance with Part 2 of Art. 9 of Law N 402-FZ;

- Examination report (if necessary);

- A claim with requirements regarding defective products (return, replacement, discount) and with reference to a clause of the contract or a rule of law regarding the violation;

- An invoice for the release of materials to the party, in the “grounds” column of which should be written: “return of defects according to act N ___ dated ____.” In this case, the name of the product must be that which was indicated upon shipment to the buyer;

- An act of destruction of defective products, or documents confirming the costs of correcting the defect;

- Documents confirming transportation costs, etc.

If the supplier does not voluntarily agree to admit his guilt regarding defective products, then there is a judicial option. On the other hand, the Tax Code of the Russian Federation does not contain a direct condition for recognizing losses from defects in expenses only if there is compensation from the supplier (manufacturer) who is responsible for the defect (see, for example, paragraph 47, paragraph 1, Article 264 of the Tax Code of the Russian Federation).

In some cases, the Russian Ministry of Finance allows the recognition as expenses of costs associated with the disposal and destruction of goods that have become unusable due to the expiration of the shelf life for those goods, the taxpayer’s obligation to destroy or dispose of which is provided for by law (see, for example, the letter of the Ministry of Finance of the Russian Federation dated May 26 .2016 N 03-03-06/1/30409, dated September 15, 2011 N 03-03-06/1/553).

The Law “On Protection of Consumer Rights” does not provide for establishing an expiration date for shoes. Thus, the issue is controversial and contains tax risks.

Due to the ambiguity of tax consequences, it is advisable for an organization to distribute the defect, for which the supplier refused to reimburse expenses, into those subject to sale at a reduced price and subject to destruction. Selling defects at a reduced price will generate income, and documents for returning defects from retail will be the justification for the reduced price.

The assessment must be documented. The costs of destroying defective items unsuitable for sale can be economically justified by calculations confirming that this event provides savings on storage (i.e., economic benefits not only in generating income, but also in reducing costs - freeing up warehouse space, for example.) Such calculations will increase the organization’s chances of defending its position in a tax dispute.

In addition, an important circumstance is the proportionality of the costs of defects in the total cost of purchased shoes. The fact is that reject amounts exceeding “usual” amounts for the industry are an additional tax risk factor.

Results

The procedure for writing off expired goods has its own nuances in terms of documentation, the need for an examination and accounting for expenses (losses) from write-off for tax purposes.

Sources:

- Labor Code of the Russian Federation

- Law of the Russian Federation dated 02/07/1992 N 2300-1 “On the protection of consumer rights”

- Tax Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.