UPD form and its application

Federal Law No. 402-FZ “On Accounting” simplified the forms of primary accounting documents (PUD), but determined a list of mandatory details for them (Article 9 402-FZ), each fact of economic life is subject to mandatory registration.

The PUD details are:

- Name;

- Date of preparation;

- name of the economic entity of the compiler;

- content of the fact of the operation;

- the measurement value of the operation in physical and (or) monetary terms (indicating the units of measurement);

- the name of the position of the person who completed the transaction, operation and is responsible for the correctness of its execution;

- signatures of persons indicating last names and initials or other details necessary for their identification.

The form of the universal transfer document was developed by the Federal Tax Service based on the requirements of the accounting law No. 402-FZ and Government Decree No. 1137 and proposed for use by letter of the Federal Tax Service of Russia dated October 21, 2013 No. MMV-20-3 / [email protected] Rules for filling out UPD are relevant for the supply of goods and performance of work (services).

Taking into account the specifics of primary business papers, it is clear what forms the UPD combines - it is used instead of:

- waybill;

- invoices;

- act of acceptance and delivery of works (services).

IMPORTANT!

The form developed by the Federal Tax Service is recommended. The organization has the right to develop its own and approve it in its accounting policies. It is important to follow the rules for filling out the UPD in 2022 and use all the required details listed above.

In some Russian regions, there are special requirements for filling out a universal transfer deed established by local regulations. For example, in Bashkiria, as of December 1, 2020, it has been established that the parties to a transaction must fill out the UTD in a form that contains a special column 10b, which indicates the region of origin of the Russian product. If foreign products are supplied, column 10b is not filled in.

A typical set of documents when switching to UPD

The selection of documents for the introduction of UPD corresponds to the stages of transition:

- Approved UPD form (can be an appendix to the general order on the transition to UPD, but can also be approved separately).

- Notifications to all counterparties about the transition to UPD. In this case, it is necessary to take into account the need to coordinate the UPD with each of them.

- Internal regulations on the use of UPD. For example, instructions for employees who will work with UPD. The following procedures should be established in internal documents:

- UTD numbering;

- signing the UPD;

- making corrections to the UPD;

- UTD storage;

- exceptions when other documents are drawn up instead of the UTD (for example, in the event of a counterparty’s refusal to work with the UTD).

You should also make appropriate changes to your accounting policies.

For more information on familiarizing employees with internal regulations, see the material “Familiarization sheet with local regulations - sample” .

- Order to switch to UPD. It should include all the main aspects listed above.

A sample order for the transition to UPD can be downloaded from our website using the link below:

Who uses UPD

Any organization, individual entrepreneurs, and even public sector employees have the right to use the universal primary system. It makes no difference which taxation regime an economic entity applies. The organizational and legal form, as well as the form of ownership, also does not matter. Use UPD when processing transactions:

- Sales (of goods, services, works).

- Transfer of property rights over the company's own assets.

- Registration of transactions regarding intermediary operations.

The list of operations and transactions is contained in the letter of the Federal Tax Service dated October 21, 2013 No. ММВ-20-3/ [email protected] UPD contains invoice details; organizations and individual entrepreneurs are allowed to use it on any form of taxation.

IMPORTANT!

Organizations and individual entrepreneurs that are not VAT payers are not required to pay this tax when applying the UTD form. For organizations that are on the general taxation system, the UTD, like an invoice, makes it possible to offset input VAT when paying to the budget.

It is important to use statuses “1” or “2” correctly:

- 1 - if it is necessary for the document to replace both the invoice and the primary document;

- 2 - the UPD invoice does not replace, it is only a replacement for the primary document.

IMPORTANT!

From 07/01/2021, if a seller sells a traceable product to an individual who purchases it for personal, non-business needs, he must still issue him an invoice or UPD with the details of the product sold.

Is it possible to adjust universal transfer documents?

Along with invoices, universal transfer documents can be adjusted and corrected. When adjusting and making changes to the actual conditions of the transaction, in agreement with other parties to the transaction, the UCD allows you to adjust the UPD - a universal adjustment document. Unlike a universal transfer document, the UCD must contain the date on which the counterparty received notice or on which it agreed to change the terms of the transaction.

If the universal transfer documents contain an error that needs to be corrected, the UPD is considered corrective. Those. a new version of already compiled documentation. The features of the correction are determined taking into account the status and which specific paper parameters need to be changed:

- If in documents with the first status there are inaccuracies in terms of primary documentation and invoices, and these inaccuracies are gross (prevent the tax service from carrying out an audit), you should write down the correction number and date in an additional line;

- If the inaccuracies are not gross or are located only in the primary documentation, then the universal transfer document is corrected only as primary documentation. Regardless of the previous status, the status of the document should be changed to the second one. This way you can draw attention to the correction. At the same time, neither the chief accountant nor the management of the organization are required to sign the document. In addition, the amended universal conveyance does not need to be registered;

- If changes have been made to the universal transfer documents with the second status, in relation to the primary documents, you need to perform actions similar to the above. However, in such a situation, the SF based on the corrected information must be set separately.

Important! In tax accounting, the recognition date is the actual date of the transaction, which is not determined by the time of making changes to the UPD.

New requirements for UPD from July 1, 2022

From 01.07.2021, by Decree of the Government of the Russian Federation of 02.04.2021 No. 534, amendments were made to Government Decree No. 1137 on changing the form of the invoice. The UPD form now differs from the invoice in that a line is included in the invoice form for the purpose of tracking the goods. The invoice contains details that allow you to identify the document on the shipment of goods (on the performance of work, provision of services), on the transfer of property rights (subclause 4, clause 5, article 169 of the Tax Code of the Russian Federation).

The new procedure for issuing and receiving invoices is established by Order of the Ministry of Finance dated 02/05/2021 No. 14n. The update of the procedure is due to the introduction of a national system of mandatory traceability of goods.

If the UPD for July 2022 and subsequent months acts as an invoice (status “1”), it must be supplemented with page 5a “Shipment document No.”. Federal Tax Service specialists, in a letter dated June 17, 2021 No. ЗГ-3-3/ [email protected] , reminded that the UPD form is only recommended and taxpayers themselves make changes to it. But, for use simultaneously for the purpose of calculating income tax and settlements with the budget for VAT, it includes mandatory details.

On the new line indicate:

- number and date of the primary document (invoice or act);

- which lines this document belongs to (now in the invoice table the lines with different goods/services are numbered, column 1 with a serial number has been introduced).

If there are several lines in the tabular part of the UPD, all lines are indicated on page 5a and the details are repeated. With 10 pages of the document and number 1 dated 07/01/2021 in the UPD, page 5a is filled out as follows:

No. 1-10 N 1 dated 07/01/2021

IMPORTANT!

Organizations that, from July 1, 2021, carry out transactions with traceable goods, supplement the information in the UPD with the details contained in the invoice issued when carrying out transactions with goods subject to traceability.

In documents with status “2” a new line is not needed. When receiving an advance, you cannot use a universal transfer document, only an invoice.

replaces both the invoice and the primary document

Universal transfer documents or invoice – what to choose?

Each enterprise can, at its own discretion, choose to work with invoices or universal transfer documents. You should know that in order to use the UPD as a SF, the document must contain all the data required for the SF.

Universal transfer documents differ in functionality. They allow you to optimize the circulation of documentation, and when executed in electronic format, reduce the volume of transactions carried out through the operator, i.e. minimize EDI costs. In addition, electronic UPD makes it possible to always have original documents “available”.

Recommendations for filling out individual details of the form

The table shows the details, the use of which will ensure the correct completion of the UPD: pay attention to the column of recommendations and explanations.

| № Rows, graphs | UPD details | Possible meanings, recommendations and explanations |

| lines (1) – (7) columns 1–11 | — | For UPD with status “1”, they are filled out in accordance with Appendix No. 1 to the Decree of the Government of the Russian Federation of December 26, 2011 No. 1137. If invoices in an organization are signed by another person authorized to do so by an order (another administrative document) for the organization or a power of attorney on behalf of the organization, then the administrative document is indicated in the invoice or the position of the authorized person who signed the specific invoice is indicated. In the document, the content of the transaction in the UPD corresponds to the invoice. It is acceptable to supplement the indicators on pages (3) and (4) with information about the TIN, checkpoint of the consignor and TIN, checkpoint of the consignee. For a universal transfer document with status “2”, it is permissible to fill out pages (1), (1a), (2), (6), (7), columns 1, 2 or 2a, 3 and 9 in order to fulfill the requirements of clause 1 Art. 9 of the Federal Law of December 6, 2011 No. 402-FZ on the presence in the document of detailed information about the content of the fact of economic life and the value of natural and (or) monetary measurement. The standard UPD does not provide for filling out column 12, but if necessary, it is added based on the specifics of the transaction. Indicators that clarify the conditions for the fulfillment of a fact of economic life are reflected in pages (2a), (2b), (3), (4), (5), (6), (6a), (6b), columns (4), (5), (6), etc. |

| line [10] | Goods (cargo) transferred/ services, results of work, license passed | The instructions tell you how to correctly sign the UPD - indicate the position of the person who made the shipment and (or) the one who is authorized to act on the transaction of transfer of work results (services, property rights) on behalf of the economic entity; his signature indicating his last name and initials. The person authorized to act in a transaction on behalf of an economic entity is determined by the norms of the relevant chapters of the Civil Code of the Russian Federation. An indicator that specifies the circumstances of the operation (transaction). If this person is the one who is authorized to sign invoices and signed the document on behalf of the manager or chief accountant (up to line [8]), then only information about his position and full name is filled in without repeating the signature. |

| Line [13] | Responsible for the correct execution of the transaction, operation | The position of the person responsible for the correct execution of the transaction, operations on the part of the seller, his signature indicating the surname and initials. An indicator that allows you to determine who is responsible for processing the transaction. If the person responsible for processing the transaction is the one who made the shipment and (or) is authorized to act on the transaction on behalf of the economic entity (page [10]), then if there is a signature in line [10], only information about the position is filled in and full name without repeating the signature. If the person responsible for processing the transaction is the person authorized to sign invoices and signed the document on behalf of the manager or chief accountant (up to line [8]), then only information about his position and full name is filled in without repeating the signature. If, due to the document flow established in an economic entity, several persons are simultaneously responsible for the correct execution of the transaction, then an additional line must be entered into the document, for example, [13a] to indicate the position, full name and signature of the second person in charge. |

| Line [15] | Goods (cargo) received/ services, results of work, rights accepted | It is permissible to indicate the position of the person who received the cargo and (or) authorized to accept services, work results, rights under the transaction of transfer of work results (services, property rights), who put mandatory signatures in the UPD on the part of the buyer indicating the surname and initials. The person authorized to act in a transaction on behalf of an economic entity is determined by the norms of the relevant chapters of the Civil Code of the Russian Federation. An indicator that specifies the circumstances of the operation (transaction). |

| Line [18] | Responsible for the correct execution of the transaction, operation | The position of the person responsible for the correct execution of the transaction, operations on the part of the buyer, his signature indicating the surname and initials. An indicator that allows you to determine the person responsible for processing the transaction. If the person responsible for processing the transaction is a person authorized to act on the transaction on behalf of the economic entity (line [15]), then only information about the position and full name is filled in without repeating the signature. If, due to the document flow established in an economic entity, several persons are simultaneously responsible for the correct execution of the transaction, then an additional line must be entered into the document - for example, [18a] to indicate the position, full name and signature of the second responsible person. |

| M.P. | Seals of economic entities who compiled the document. This requirement is not legally required. The absence of a seal in the presence of all the mandatory details provided for in Article 9 of Law No. 402-FZ is not a basis for refusing to accept a document for tax registration. |

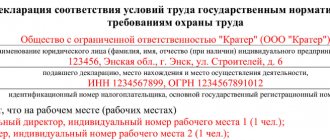

A sample form will help us understand how to fill out the form. Let's consider 2 examples: the first - when performing work and providing services.

Examples of completed forms

When performing work and providing services

IMPORTANT!

Added line 5a “Shipping Document”.

When shipping goods

The second example of filling out the UPD is when shipping goods. To fill out a universal transfer document instead of a consignment note (TORG12), you need to change the status from “1” to “2” and leave the pages “Consignor and his address” (3) and “Consignee and his address” (4) blank.

IMPORTANT!

Line 5a is not added to such a document.

Cases of using universal transfer documents

You can use universal transfer documents if you wish. In other words, you can decide for yourself whether you need UPD or whether you will work with them in conjunction with classic document formats.

Let's consider cases in which universal transfer documents can be used:

- Transfer under a license agreement contract or as exclusive property rights;

- Carrying out mediation activities;

- Provision of services;

- Transfer of results of completed work;

- Sending products with or without transportation.

To be able to use universal transfer documents, an enterprise must confirm working with them by indicating this fact in its accounting policy. A decree of the company management on approval of the UPD form is also formed.