Financial investments and their main features

Financial investments are recognized as such if there are:

- documentary evidence;

- financial risks when investing;

- profit-oriented.

Short-term investments are investments for a period of up to one year, long-term financial investments are investments of an enterprise, respectively, for a period of more than a year.

Short-term investments are temporary uses of a firm's available cash. Its purpose, along with direct profit generation, is to protect against losses due to inflation. Short-term financial investments have high liquidity and are actually equivalent to means of payment. In accounting they are included in current assets. In the field of financial management, short-term investments are recognized as the equivalent of monetary assets; the approaches to managing both are the same.

Financial investments for the long term are included in non-current, long-term assets for accounting purposes. This type of investment carries high financial risk.

Financial investments do not include (according to the text of PBU 19/02, clause 3):

- own securities purchased for the purpose of resale or cancellation;

- bills involved in settlements of transactions;

- investments in property transferred for possession and use temporarily for a fee (rent);

- precious metals, jewelry, valuable art objects, and other similar valuables.

Important! Fixed assets, inventories, any assets that have a tangible form, as well as intangible assets (intangible assets), cannot be recognized as financial investments (PBU 19/02, clause 4).

Basic Concepts

Financial investments represent financing of other firms for subsequent profit. Both money and property can be used as a financing tool. Let's look at examples of investments:

- Buying shares.

- Purchase of receivables on the basis of an agreement on the assignment of claims.

- Formation of the authorized capital of companies.

- Providing a loan at interest.

Question: In what cases is a reserve created for the impairment of financial investments? View answer

For example, a company is engaged in providing loans. She does this not out of selfless motives, but in order to receive the loan amount in the future. Additionally, interest is added to this amount, which is the company’s revenue. The procedure for accounting for deposits is specified by PBU 19/02.

Let's consider an example of reserve formation using shares as an example. If securities are traded on the market, they are valued based on market value. This value is revalued once a year. Sometimes revaluation may be performed more frequently: once a month or once a quarter. If investments are not traded on the market, the value is established either independently or with the help of a specialist (appraiser).

Is a reserve created for the depreciation of financial investments in tax accounting ?

Types of investments

The directions of investments, regardless of the period, are generally similar, but there are some nuances.

Short term

Examples of short-term investments include the following:

- provision of borrowed funds to other legal entities at interest;

- provision of borrowed funds to its employees at interest;

- purchase of shares, bonds, and other securities;

- funds in deposit accounts of banks (credit organizations).

Short-term investments in securities make sense if there is reliable information about their high liquidity and the ability to convert them into a financial equivalent without delay. Such investment is usually preceded by serious analytical work.

Issuing loans and borrowings at interest for a period of up to a year usually involves a higher level of interest compared to long-term ones. It is believed that such a measure guarantees the return of borrowed funds. Placing finances on a short-term deposit also requires a careful approach, analysis of interest rates, and other placement conditions.

Long-term

Long-term investments can act as interest-bearing loans, deposits, securities - by analogy with short-term ones, adjusted for repayment periods - more than 1 year. As a rule, free funds are also allocated for the long term in the following areas:

- contributions to the authorized capital and its varieties (not excluding subsidiaries and dependent companies);

- contributions under a simple partnership agreement of the partner organization;

- receivables received on the basis of an agreement for assignment of the right of claim (assignment).

Due to the high risk of losing funds, long-term investments require competent strategic forecasting for the future.

Account 58 Financial investments: typical transactions

Account 58 “Financial Investments” is intended to summarize information on the presence and movement of an organization’s investments in government securities, shares, bonds and other securities of other organizations, authorized (share) capital of other organizations, as well as loans granted to other organizations.

Sub-accounts can be opened to account 58 “Financial investments”: 58-1 “Units and shares”, 58-2 “Debt securities”, 58-3 “Loans provided”, 58-4 “Deposits under a simple partnership agreement”, etc. .

Subaccount 58-1 “Shares and shares” takes into account the presence and movement of investments in shares of joint-stock companies, authorized (share) capitals of other organizations, etc.

Subaccount 58-2 “Debt securities” takes into account the presence and movement of investments in government and private debt securities (bonds, etc.).

Financial investments made by the organization are reflected in the debit of account 58 “Financial investments” and the credit of accounts that record the values to be transferred on account of these investments. For example, the acquisition by an organization of securities of other organizations for a fee is carried out in the debit of account 58 “Financial investments” and the credit of account 51 “Currency accounts” or 52 “Currency accounts”.

For debt securities for which the current market value is not determined, the organization is allowed to attribute the difference between the initial value and the nominal value during the period of their circulation evenly, as income is due on them in accordance with the terms of issue, to the financial results of the commercial organization or a decrease or increase in expenses of a non-profit organization.

When writing off the excess of the purchase price of bonds and other debt securities acquired by the organization over their nominal value, entries are made in the debit of account 76 “Settlements with various debtors and creditors” (for the amount of income due on securities) and in the credit of account 58 “Financial investments "(for part of the difference between the purchase and nominal value) and 91 "Other income and expenses" (for the difference between the amounts allocated to accounts 76 "Settlements with various debtors and creditors" and 58 "Financial investments").

When additionally accruing the amount of excess of the nominal value of bonds and other debt securities acquired by the organization over their purchase price, entries are made in the debit of accounts 76 “Settlements with various debtors and creditors” (for the amount of income due on securities) and 58 “Financial investments” ( for part of the difference between the purchase and nominal value) and to the credit of account 91 “Other income and expenses” (for the total amount allocated to accounts 76 “Settlements with various debtors and creditors” and 58 “Financial investments”);

Redemption (redemption) and sale of securities accounted for on account 58 “Financial investments” are reflected in the debit of account 91 “Other income and expenses” and the credit of account 58 “Financial investments” (except for organizations that reflect these transactions on account 90 “Sales”) ").

Subaccount 58-3 “Loans provided” takes into account the movement of monetary and other loans provided by the organization to legal entities and individuals (except for employees of the organization). Loans provided by the organization to legal entities and individuals (except for employees of the organization) secured by bills of exchange are accounted for separately in this subaccount.

Loans provided are reflected in the debit of account 58 “Financial investments” in correspondence with account 51 “Current accounts” or other relevant accounts. The loan repayment is reflected in the debit of account 51 “Current accounts” or other relevant accounts and the credit of account 58 “Financial investments”.

In subaccount 58-4 “Deposits under a simple partnership agreement,” the partner organization takes into account the presence and movement of contributions to common property under a simple partnership agreement. The provision of a deposit is reflected in the debit of account 58 “Financial investments” in correspondence with account 51 “Current accounts” and other relevant accounts for accounting for allocated property.

Upon termination of a simple partnership agreement, the return of property is reflected in the credit of account 58 “Financial investments” in correspondence with the property accounts.

Analytical accounting for account 58 “Financial investments” is carried out by types of financial investments and objects in which these investments are made (organizations that sell securities; other organizations in which the organization is a participant; borrowing organizations, etc.).

The construction of analytical accounting should provide the ability to obtain data on short-term and long-term assets. At the same time, accounting for financial investments within a group of interrelated organizations, about the activities of which consolidated financial statements are prepared, is kept separately in account 58 “Financial investments”.

Concept, essence and legal regulation of accounting for financial investments

Financial investments represent a special type of financial assets that require managers and accountants to carefully monitor all changes related to their reflection in the legislative and regulatory framework.

According to the requirements of PBU 19/02, accounting for financial investments in shares and other objects is carried out by all Russian organizations, including non-state pension funds, insurance structures and professional participants in the securities market.

Financial investments include only a certain group of assets. The regulatory requirements by which assets are recognized as financial investments are listed in clause 2 of PBU 19/02. At the same time, several criteria must be met: the company has properly executed documentation for the right to own this object and derive benefits (money or assets) from its use; all risks arising from the right to own these investments are transferred to the company - this is, for example, the risk of low liquidity, insolvency (bankruptcy) of the organization, fluctuations in cost indicators, etc.; the actual ability to bring various economic benefits to the company in the form of interest, cash dividends, price appreciation and other revenues in future periods.

Placements of funds that are or are not related to financial investments are presented in paragraphs 3–4 of PBU 19/02. The accounting unit for each organization is selected by the company independently, depending on the nature of the investments made - batch, series, aggregate, etc.

At the time of accepting assets as financial investments for accounting, it is necessary to simultaneously fulfill certain conditions: the presence of correctly executed documents recording the emergence of the organization’s right to financial investments and the receipt of funds or other assets resulting from this right; transfer of financial risks associated with the acquisition of assets to the organization; the ability and possibility of financial investments to bring economic benefits to the organization in the future.

Financial investments can be planned by the organization at the beginning of the reporting period, based on the actual performance results that the company intends to obtain at the end of the previous reporting period. An organization can carry out the planned acquisition of short-term financial investments in accordance with regulatory data on cash flows and the target level of their balances. The organization intends to make long-term financial investments in accordance with planned indicators from taking ownership of shares in other business entities.

In the process of managing financial investments, the company resolves a whole list of tasks:

– guarantees the reliability of investments; increases the amount of income from operations performed;

– increases the market value of financial investments;

– ensures their liquidity.

The main goal of managing financial investments is to ensure an acceptable balance between income from investment activities, the risk associated with making financial investments, and the liquidity of securities in accordance with the type of investment portfolio.

Modern commercial organizations, whose main activity is not financial investments, may face the problem of revaluing financial investments in the process of accounting. When this situation arises, it is necessary to compare the market price and the initial cost, which consists of the cost of the security itself and the costs of its acquisition. Commercial organizations that are financial investors in securities need to organize an effective system for analyzing financial investments, which will be able to identify the most profitable areas investment activities and minimize the risks associated with financial investments.

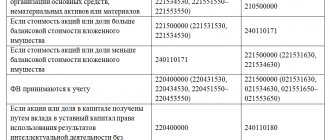

The classification of financial investments established from the perspective of PBU 19/02 is presented in Figure 1

Classification of financial investments

[flat_ab id=”11"]

The division into long-term and short-term financial investments is quite arbitrary and reflects only general cases of using assets. In practice, any long-term financial instrument (be it a stock or bond) that is purchased by a company for a period of less than 12 months will be a short-term financial investment. Conversely, conditionally short-term financial investments can be long-term if acquired for use for more than 12 months (for example, deposits or receivables).

Thus, financial investments show all types of intellectual and property values that are directed to objects of entrepreneurial activity, which ultimately result in profit or any other useful effect.

Procedure for accounting for financial investments and securities

To account for any type of financial investment in an organization, it is necessary to focus on the regulations PBU 19/02 “Accounting for financial investments.”

This document establishes the criteria for recognizing an asset as a financial investment for an enterprise, as well as:

- The procedure for the initial and subsequent assessment of financial investments.

- Methods for accounting for financial investments upon their disposal.

- Criteria for recognizing income and expenses on transactions with financial investments.

- The procedure for reflecting indicators on transactions with financial investments in the organization’s reporting.

- Accounting for financial investments in cases of their depreciation.

Financial investments, according to the chart of accounts, are accounted for in synthetic account 58. This account has four subaccounts for accounting:

- Shares 58.01

- Debt securities 58.02

- Loans provided 58.03

- Deposits under simple partnership agreements 58.04

Analytical accounting by type of financial investment is applied to these accounts.

For example, account 58.01 can be analytically represented as:

Finished works on a similar topic

Course work Accounting for financial investments and securities 490 ₽ Abstract Accounting for financial investments and securities 230 ₽ Test work Accounting for financial investments and securities 230 ₽

Receive completed work or specialist advice on your educational project Find out the cost

- 58.011 – Shares with a maturity of up to 3 months;

- 58.012 – Shares with a maturity of up to 6 months;

- 58.013 – Shares with a maturity of up to 12 months.

Account 58.03 can be analytically represented as:

- 58.031 – Loans provided with a repayment period of up to one year;

- 58.032 – Loans granted with a repayment period of more than one year.

Thus, analytical accounting can be carried out in the context of various characteristics, depending on the specifics of the activities of each individual enterprise.

Note 2

Considering that account 58 is active, an increase in financial investments is recorded as a debit to the account, and their repayment is recorded as a credit to the account.

In the balance sheet, financial investments are taken into account in its active part. If such investments have a maturity period of more than one year, then they are reflected in non-current assets. If financial investments have a maturity of more than one year, then they are taken into account as part of current assets.

Upon accrual of dividends (profits) on financial investments, they are recorded in account 76.3. This profit relates to other income, so the posting when calculating dividends will be as follows.

D-t 76.3 K-t 91

Accounting for disposal of financial investments

Clause 25 of PBU 19/02 lists the main directions of disposal of financial investments and states that this disposal is recognized in accounting on the date of the one-time termination of the conditions for their acceptance for accounting given in clause 2 of PBU 19/02.

The procedure for assessing retiring financial investments depends on their type: securities and all other financial investments. The value of retired securities is calculated depending on whether their current market value is determined or not. If it is not determined, then the value of the retiring securities is calculated in one of three ways:

— at the initial cost of each accounting unit of securities;

— at the average initial cost;

- FIFO method, i.e. at the original cost of the first securities acquired.

As we can see, of the four asset valuation methods known in Russian accounting, the LIFO method is not used in this case.

For tax purposes in accordance with clause 9 of Art. 280 of the Tax Code of the Russian Federation, retiring securities can also be valued in three ways, but among them there is no average initial cost, and at the same time the LIFO method is provided.

For each group (type) of securities during the reporting year, only one valuation method should be used (clause 31). The appendix to PBU 19/02 provides digital examples of the use of various valuation methods when disposing of financial investments. If the current market value is determined for securities, then their value upon disposal is calculated based on the latest valuation. All other retiring financial investments (except for securities) are valued at the original cost of each retiring unit

When disposing of a contribution to the authorized capital in accounting, the retiring contribution is assessed at the initial cost of each retiring unit (clause 27 of PBU 19/02).

In tax accounting, the value of property when transferred to the authorized capital of both parties is assessed not according to the valuation agreed upon by the founders, but according to the value of the property taken into account in the tax accounting of the transferring party. The cost must be documented. Therefore, upon leaving the company or its liquidation, neither income nor expenses arise for both parties if the property is returned precisely according to the tax assessment. And accordingly, the excess of the tax value, and not the accounting value, will be subject to income tax (clause 4, clause 1, article 251 of the Tax Code of the Russian Federation, clause 9, article 250 of the Tax Code of the Russian Federation).

Disposal of contributions to the authorized capital may also occur upon their sale. The sale of shares in the authorized capitals of other organizations is reflected in accounting as the debit of account 62 and the credit of account 91. At the same time, the book value of the objects recorded in the corresponding subaccount of account 58 is written off to the debit of account 91. If there are costs of sale, they are reflected in the debit of account 91.

The accounting regulation “Accounting for financial investments” PBU 19/02, approved by Order of the Ministry of Finance of the Russian Federation dated December 10, 2002 No. 126n, establishes that the initial cost of financial investments acquired for a fee includes amounts paid in accordance with the agreement to the seller. Upon disposal of financial investment objects in the event of their repayment, sale, gratuitous transfer, transfer on account of a contribution to the authorized (share) capital, transfer on account of a contribution under a simple partnership agreement, etc., their value is written off, including the amount of accumulated coupon income paid upon acquisition financial investments

The cost of disposal of financial investments for which the current market value is determined is calculated based on the latest assessment. Let's look at the reflection of accounting transactions using an example.

Example. In January 2008, the organization acquired 1,000 shares traded on the organized securities market at 102 rubles. per piece at a nominal price of 100 rubles.

In accordance with the accounting policy, subsequent assessment is carried out quarterly and as of March 31, 2008 amounted to 120 rubles. Proceeds from the sale are included in operating income.

On April 20, 2008, 300 shares were sold on the organized market at a price of 124 rubles. per share.

In accounting, these transactions are reflected in the following entries.

In January:

Debit 76 Credit 51 – 102,000 rub. – the price of the shares has been paid to the seller in accordance with the agreement;

Debit 58/1 Credit 76 – 102,000 rub. – the received shares are accepted for accounting.

In March:

Debit 58/1 Credit 91/1 – 18,000 rub. – reflects the difference between the current market value of the shares and their previous valuation (120 rubles/piece x 1000 pieces - 102,000 rubles).

In April:

Debit 76 Credit 91/1 – 37,200 rub. (300 pcs. x 124 rubles/pcs.) – the debt on payment for shares is reflected;

Debit 51 Credit 76 – 37,200 rub. – funds received;

Debit 91/2 Credit 58/1 – 36,000 rub. (300 pcs. x 120 rubles/pcs.) – the cost of sold shares has been written off according to the latest valuation;

Debit 91/9 Credit 99 – 1200 rub. – in the final turnover of April, the balance of other income and expenses was written off.

The specifics of determining the tax base for income tax on transactions with securities are established by Article 280 of the Tax Code of the Russian Federation.

Income from operations on the sale of securities is determined based on the price of their sale (clause 2 of Article 280 of the Tax Code of the Russian Federation).

The market price of securities traded on the organized securities market is recognized as the actual price of sale or other disposal of securities if this price is in the interval between the minimum and maximum prices of transactions (price interval) with the specified security registered by the trade organizer on the date of the relevant transactions (clause 5 of Article 280 of the Tax Code of the Russian Federation).

Moreover, in the case of the sale of securities traded on the organized market at a price below the minimum transaction price, the financial result is calculated from the minimum transaction price on the organized securities market.

Securities accounting

The chart of accounts for accounting the financial and economic activities of organizations, approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n, provides that all investments in financial assets, regardless of the period of placement of funds, must be reflected in active account 58 “Financial investments” without a special division into long-term and short-term.

If in the accounting system financial investments are no longer classified as long-term and short-term, then in the form of the balance sheet this classification is preserved. The classification of financial investments into long-term and short-term is carried out not for current accounting purposes, but only for financial reporting. When compiling it, the organization must analyze all these assets and determine, as of the reporting date, which of them are long-term and which are short-term financial investments. When classifying, it is advisable to understand by maturity not the period of circulation of securities (the time from the moment of issue to the moment of redemption), but the degree of their liquidity, i.e. the ability, if necessary, to easily turn them into cash in the shortest possible time.

With this approach, short-term investments should include investments in easily marketable securities, the purchase of which is made in the interests of profitable placement of temporarily free funds before the need for cash arises, as well as for the purpose of generating additional income.

Long-term financial investments represent the placement of capital in legally independent organizations for a long period (at least more than a year) and are carried out with the aim of maintaining certain business activities or commercial relations.

Securities are accounted for in account 58 “Financial investments”, to which sub-accounts can be opened: 58-1 “Units and shares”, 58-2 “Debt securities”, etc.

Due to the fact that the construction of analytical accounting should provide the ability to obtain information about short-term and long-term assets, on account 58 you can open sub-accounts for accounting for short-term and long-term financial investments, within which you can keep records by type and issue of securities.

In Chapter 25 of the Tax Code of the Russian Federation, all securities are divided into two categories - traded and non-traded on the organized securities market (hereinafter referred to as ORSM). At the same time, for the purposes of accounting and tax accounting, the organization maintains separate records of income and expenses on transactions with securities traded and not traded on the Ordinary Securities Market. Maintaining such records can be done through second-order subaccounts.

Let us recall that the working chart of accounts is approved in the order on the accounting policy of the organization.

Issue-grade securities must be accounted for in the context of individual issues, each of which has its own registration number, indicated in extracts from the register of shareholders and other documents.

However, not all investments in financial assets should be accounted for as financial investments. In particular, account 58 is not intended to account for:

- commodity (own simple ones, for which he himself is liable, or a transfer bill not accepted by the payer) bills of exchange of buyers (customers), received to secure receivables for payment for goods, property, work, services. Such bills of exchange are accounted for in accounts 62 “Settlements with buyers and customers”, 76 “Settlements with various debtors and creditors” in the same account as the buyer’s receivables, subaccount “Bills received”

— check books (accounted for in account 55 “Special accounts in banks”);

— deposit and savings certificates (accounted for in account 55 “Special accounts in banks”);

— own shares (shares in the authorized capital), purchased from shareholders (participants) (accounted for in account 81 “Own shares (shares)”).

The moment of transfer of ownership of securities is established in accordance with Articles 28, 29 of the Federal Law of April 22, 1996 No. 39-FZ “On the Securities Market”. Ownership of issue-grade securities (shares, bonds) is transferred at the moment of their transfer from one personal account in registers or from depository accounts in depositories to other personal accounts or depository accounts. If the security is issued in paper form - at the time of re-issuance of its certificate to the new owner.

In exchange practice, there are situations when purchase and simultaneous sale transactions are executed by offset (netting). This can happen, for example, when all the securities purchased on one day were immediately sold and mutual debts will be offset; there will be no transfer of ownership of the securities in the legal sense. However, in accounting it is still necessary to reflect first the purchase and then the sale of securities. In this case, it is necessary to be very careful when calculating the write-off price of securities at the time of their disposal.

Practical part

Clause 25 of PBU 19/02 lists the main directions of disposal of financial investments and states that this disposal is recognized in accounting on the date of the one-time termination of the conditions for their acceptance for accounting given in clause 2 of PBU 19/02.

The procedure for assessing retiring financial investments depends on their type: securities and all other financial investments. The value of retired securities is calculated depending on whether their current market value is determined or not. If it is not determined, then the value of the retiring securities is calculated in one of three ways:

— at the initial cost of each accounting unit of securities;

— at the average initial cost;

- FIFO method, i.e. at the original cost of the first securities acquired.

As we can see, of the four asset valuation methods known in Russian accounting, the LIFO method is not used in this case.

For tax purposes in accordance with clause 9 of Art. 280 of the Tax Code of the Russian Federation, retiring securities can also be valued in three ways, but among them there is no average initial cost, and at the same time the LIFO method is provided.

For each group (type) of securities during the reporting year, only one valuation method should be used (clause 31). The appendix to PBU 19/02 provides digital examples of the use of various valuation methods when disposing of financial investments. If the current market value is determined for securities, then their value upon disposal is calculated based on the latest valuation. All other retiring financial investments (except for securities) are valued at the original cost of each retiring unit

When disposing of a contribution to the authorized capital in accounting, the retiring contribution is assessed at the initial cost of each retiring unit (clause 27 of PBU 19/02).

In tax accounting, the value of property when transferred to the authorized capital of both parties is assessed not according to the valuation agreed upon by the founders, but according to the value of the property taken into account in the tax accounting of the transferring party. The cost must be documented. Therefore, upon leaving the company or its liquidation, neither income nor expenses arise for both parties if the property is returned precisely according to the tax assessment. And accordingly, the excess of the tax value, and not the accounting value, will be subject to income tax (clause 4, clause 1, article 251 of the Tax Code of the Russian Federation, clause 9, article 250 of the Tax Code of the Russian Federation).

Disposal of contributions to the authorized capital may also occur upon their sale. The sale of shares in the authorized capitals of other organizations is reflected in accounting as the debit of account 62 and the credit of account 91. At the same time, the book value of the objects recorded in the corresponding subaccount of account 58 is written off to the debit of account 91. If there are costs of sale, they are reflected in the debit of account 91.

The accounting regulation “Accounting for financial investments” PBU 19/02, approved by Order of the Ministry of Finance of the Russian Federation dated December 10, 2002 No. 126n, establishes that the initial cost of financial investments acquired for a fee includes amounts paid in accordance with the agreement to the seller. Upon disposal of financial investment objects in the event of their repayment, sale, gratuitous transfer, transfer on account of a contribution to the authorized (share) capital, transfer on account of a contribution under a simple partnership agreement, etc., their value is written off, including the amount of accumulated coupon income paid upon acquisition financial investments

The cost of disposal of financial investments for which the current market value is determined is calculated based on the latest assessment. Let's look at the reflection of accounting transactions using an example.

Example. In January 2008, the organization acquired 1,000 shares traded on the organized securities market at 102 rubles. per piece at a nominal price of 100 rubles.

In accordance with the accounting policy, subsequent assessment is carried out quarterly and as of March 31, 2008 amounted to 120 rubles. Proceeds from the sale are included in operating income.

On April 20, 2008, 300 shares were sold on the organized market at a price of 124 rubles. per share.

In accounting, these transactions are reflected in the following entries.

In January:

Debit 76 Credit 51 – 102,000 rub. – the price of the shares has been paid to the seller in accordance with the agreement;

Debit 58/1 Credit 76 – 102,000 rub. – the received shares are accepted for accounting.

In March:

Debit 58/1 Credit 91/1 – 18,000 rub. – reflects the difference between the current market value of the shares and their previous valuation (120 rubles/piece x 1000 pieces - 102,000 rubles).

In April:

Debit 76 Credit 91/1 – 37,200 rub. (300 pcs. x 124 rubles/pcs.) – the debt on payment for shares is reflected;

Debit 51 Credit 76 – 37,200 rub. – funds received;

Debit 91/2 Credit 58/1 – 36,000 rub. (300 pcs. x 120 rubles/pcs.) – the cost of sold shares has been written off according to the latest valuation;

Debit 91/9 Credit 99 – 1200 rub. – in the final turnover of April, the balance of other income and expenses was written off.

The specifics of determining the tax base for income tax on transactions with securities are established by Article 280 of the Tax Code of the Russian Federation.

Income from operations on the sale of securities is determined based on the price of their sale (clause 2 of Article 280 of the Tax Code of the Russian Federation).

The market price of securities traded on the organized securities market is recognized as the actual price of sale or other disposal of securities if this price is in the interval between the minimum and maximum prices of transactions (price interval) with the specified security registered by the trade organizer on the date of the relevant transactions (clause 5 of Article 280 of the Tax Code of the Russian Federation).

Moreover, in the case of the sale of securities traded on the organized market at a price below the minimum transaction price, the financial result is calculated from the minimum transaction price on the organized securities market.

Securities accounting

The chart of accounts for accounting the financial and economic activities of organizations, approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n, provides that all investments in financial assets, regardless of the period of placement of funds, must be reflected in active account 58 “Financial investments” without a special division into long-term and short-term.

If in the accounting system financial investments are no longer classified as long-term and short-term, then in the form of the balance sheet this classification is preserved. The classification of financial investments into long-term and short-term is carried out not for current accounting purposes, but only for financial reporting. When compiling it, the organization must analyze all these assets and determine, as of the reporting date, which of them are long-term and which are short-term financial investments. When classifying, it is advisable to understand by maturity not the period of circulation of securities (the time from the moment of issue to the moment of redemption), but the degree of their liquidity, i.e. the ability, if necessary, to easily turn them into cash in the shortest possible time.

With this approach, short-term investments should include investments in easily marketable securities, the purchase of which is made in the interests of profitable placement of temporarily free funds before the need for cash arises, as well as for the purpose of generating additional income.

Long-term financial investments represent the placement of capital in legally independent organizations for a long period (at least more than a year) and are carried out with the aim of maintaining certain business activities or commercial relations.

Securities are accounted for in account 58 “Financial investments”, to which sub-accounts can be opened: 58-1 “Units and shares”, 58-2 “Debt securities”, etc.

Due to the fact that the construction of analytical accounting should provide the ability to obtain information about short-term and long-term assets, on account 58 you can open sub-accounts for accounting for short-term and long-term financial investments, within which you can keep records by type and issue of securities.

In Chapter 25 of the Tax Code of the Russian Federation, all securities are divided into two categories - traded and non-traded on the organized securities market (hereinafter referred to as ORSM). At the same time, for the purposes of accounting and tax accounting, the organization maintains separate records of income and expenses on transactions with securities traded and not traded on the Ordinary Securities Market. Maintaining such records can be done through second-order subaccounts.

Let us recall that the working chart of accounts is approved in the order on the accounting policy of the organization.

Issue-grade securities must be accounted for in the context of individual issues, each of which has its own registration number, indicated in extracts from the register of shareholders and other documents.

However, not all investments in financial assets should be accounted for as financial investments. In particular, account 58 is not intended to account for:

- commodity (own simple ones, for which he himself is liable, or a transfer bill not accepted by the payer) bills of exchange of buyers (customers), received to secure receivables for payment for goods, property, work, services. Such bills of exchange are accounted for in accounts 62 “Settlements with buyers and customers”, 76 “Settlements with various debtors and creditors” in the same account as the buyer’s receivables, subaccount “Bills received”

— check books (accounted for in account 55 “Special accounts in banks”);

— deposit and savings certificates (accounted for in account 55 “Special accounts in banks”);

— own shares (shares in the authorized capital), purchased from shareholders (participants) (accounted for in account 81 “Own shares (shares)”).

The moment of transfer of ownership of securities is established in accordance with Articles 28, 29 of the Federal Law of April 22, 1996 No. 39-FZ “On the Securities Market”. Ownership of issue-grade securities (shares, bonds) is transferred at the moment of their transfer from one personal account in registers or from depository accounts in depositories to other personal accounts or depository accounts. If the security is issued in paper form - at the time of re-issuance of its certificate to the new owner.

In exchange practice, there are situations when purchase and simultaneous sale transactions are executed by offset (netting). This can happen, for example, when all the securities purchased on one day were immediately sold and mutual debts will be offset; there will be no transfer of ownership of the securities in the legal sense. However, in accounting it is still necessary to reflect first the purchase and then the sale of securities. In this case, it is necessary to be very careful when calculating the write-off price of securities at the time of their disposal.

Practical part