At every accounting forum, the topic of not closing the 20th account has been repeatedly raised. The fact is that there is more than one or two reasons for this, and many factors need to be taken into account - these are the settings of the accounting policy, and the entry of production documents, and accounting by item groups, etc. Moreover, the account does not always have to be closed on 20! We will present in our publication the most common causes of this problem.

In general, to make it clear why we need the 20th account, let’s say this: to determine the cost of finished products.

During the entire production cycle, direct costs are debited to account 20. This is the cost of raw materials and supplies necessary for production, wages and insurance premiums for workers in the production workshop, rental of production space, depreciation of machines and other equipment, that is, everything that was spent on production. And the credit of the same account records the release of finished products.

Thus, if we divide the amount of expenses in debit 20 of account by the number of units of finished products, we will obtain the cost of production.

When you start the “Month Closing” processing in the “Operations” section, the program should automatically close account 20 so that the final balance on this account on the last day of the month is zero.

But it is not always the case. Let's look at situations where the closure of account 20 should not have happened, and how to distinguish this from an error.

What is account 20 in accounting

Account 20 is one of the registers in Section III of the Chart of Accounts. It summarizes information about the costs associated with the production of products (works, services).

Expenses

The main function of account 20 “Main production” is calculation, since it describes the economic process of manufacturing a product and collects all information about the costs of its production. Also, using an account card, you can track information about the movement of property in the enterprise.

The difference between this register and the others in accounting is that its balance at the end of the reporting period is not calculated using a formula, but is entered manually. This is due to the fact that cost information is collected on the account over a period of time (at least a month). Until the end of the period, the exact cost of the goods is unknown, since it includes many components - depreciation, wages for workers and management, utilities, transportation costs.

Thus, at the end of the reporting period (and necessarily at the end of the year), the account. 20, like production shops, is subject to inventory to identify work in progress. After this, the amount spent on the production of finished products (actual cost) is calculated, which is written off using one of the methods adopted by the enterprise’s accounting policy.

No revenue

In the accounting policy settings there is an item “Costs are written off”, which can take three values: without taking into account revenue, taking into account all revenue and taking into account revenue only from production services.

What does this mean?

The first option “Without taking into account revenue” means that the program will close account 20 regardless of whether there were sales in the current month or not.

Why is this option bad? If you have a long production cycle, and, for example, products are produced for six months and only then sold, then it may happen that, according to tax reporting, the enterprise will be unprofitable throughout the entire production process, and only at the time of sale will a profit arise.

The same situation can occur when releasing seasonal products that are sold only in a certain season, for example, sunscreen.

What is good about this cost write-off option? The fact that account 20 is closed without taking into account sales.

Check this setting item, and if you have selected the “Excluding revenue” option, and account 20 is not closed, then proceed to the next heading of our article.

The second option for writing off costs is “Taking into account all revenue.” With this method, account 20 will be closed only for those item groups for which there were sales.

For example, you produce two types of goods: clothing and shoes, and in product groups you have corresponding names. At the same time, there were sales of clothing in the current period, but no shoes. Then account 20 will not be closed completely: the costs of clothing production will be written off and taken into account when calculating the financial result, but the costs of producing shoes will not. They will freeze until implementation begins.

If you selected the option “Taking into account all revenue” and account 20 is not closed, check your sales by product group. To do this, create a balance sheet for account 90.01.1 for the period under review and set the grouping by item groups in the report settings. The report is located in the “Reports” section - “Account balance sheet”.

And finally, the third option for cost accounting: “Taking into account revenue only from production services.” When choosing this method 20, the account is closed only if the documents “Rendering production services” were entered.

Accordingly, if you find that this method of writing off costs is selected in the accounting policy, then you need to check the availability of the relevant documents.

What counts in the 20 count?

Account 20 is used to account for the following costs:

- production of products from agricultural and industrial enterprises, as well as subsidiary farms;

- costs of repair work, maintenance of cars and other vehicles;

- costs of organizations providing transport services;

- costs of construction, installation and design and survey work;

- costs of performing research and development work;

- costs of catering organizations;

- salaries of key and administrative personnel;

- depreciation of production equipment;

- amounts of payments for renting premises and paying for utilities;

- other expenses related to the activities of the production enterprise.

Debit 20 reflects all direct costs associated with the manufacture of products (performance of work and provision of services), costs of auxiliary production, indirect costs, as well as losses from defects. Credit 20 reflects the amount of the actual cost of goods, the production of which has already been completed, or work performed and services rendered.

Counting scheme 20

When determining the type of account 20 - whether it is active or passive - you need to understand the following: since the company cannot consume more raw materials and materials than it was written off for, therefore, debit turnover on the account. 20 will always be more credit. And this means that the count. 20 - active. Balance (remaining) according to account. 20 at the end of the month reflects the amount of work in progress costs.

Unfinished production

Work in progress is a situation where production costs have been incurred, but no output has occurred. In this case, the program does not write off expenses from account 20, and it remains unclosed.

At this moment, the setting of the enterprise’s accounting policy is responsible. Let's go to the "Main" section and select the "Accounting Policy" item.

In the window that opens, you will see two types of activities that can be taken into account on account 20: “Production of products” and “Performance of work, provision of services to customers.”

If you are engaged only in the production of products and do not provide services, then you should only have the “Product Production” flag. It is during its installation that the program focuses on product output while writing off production costs.

If you have the “Performance of work, provision of services to customers” flag, then the program does not keep records of work in progress and closes account 20, regardless of whether you produced products or not.

Here the following question may arise: “How can we take into account work in progress if the organization is engaged in both the production of products and the provision of services to customers? Indeed, in this case, you need to set both flags and 20 the account will be completely closed.”

In such cases, the accountant needs to enter the document “WIP Inventory” in the “Production” section, which indicates materials transferred to account 20 that have not yet been processed or other direct costs that should not be closed in the current period.

When creating a new document “WIP Inventory”, in the header you need to indicate the organization and department in which the unfinished work remains, and then in the tabular section add item groups to which unspent materials were previously transferred. Unfortunately, the accountant will need to calculate the amounts for accounting and tax accounting manually.

The amount that will be indicated in this document will remain unclosed on the 20th account after the end of the month.

How to close

Closing of account 20 occurs when the production of products is completed, work is performed or services are provided. To close the account, it is necessary to reflect it in the accounting entry for a loan for the amount of goods produced. Thus, after closing the account, it can either be reset to zero (if there are no other work in progress) or remain with a debit balance (if there is still work in progress).

Note! Account lending 20 does not always mean production is complete. If a defect is detected, it is also written off from credit 20 to debit 28 “Defects in production”.

Current legislation provides for the possibility of closing an account. 20 in one of three ways: direct, intermediate or direct implementation. The characteristics of the closing method must be spelled out in the accounting policy of the enterprise, and immediately before closing, the accountant must highlight the balances of work in progress, if any.

Direct method

This method is used when the actual price of manufactured products is unknown during the reporting period, so they are accounted for at conditional prices, mainly at planned costs. In the process of closing the account. 20 accounting department adjusts the cost of manufactured products to the actual cost.

With this closing method, accounting makes the following entries:

- Dt43 Kt20 - finished products are transferred to the warehouse at the planned cost;

- Dt90-02 Kt43 - writing off deviations of actual and planned cost to cost of sales.

Attention! When using this closing method, it becomes impossible to take into account the actual price of products during the month.

Intermediate method

When using this method, an account is additionally used in accounting. 40 “Product release”. This account reflects deviations of the planned cost from the actual one, while credit 40 includes the planned cost, and debit the actual cost.

Intermediate method of closing an account. 20

At the end of the reporting period, the total amount of the difference is written off proportionally to the account. 43 and 90-02. During the month, the accountant makes the following entries:

- Dt43 Kt40 - capitalization of finished products at planned cost;

- Dt90-02 Kt43 - write-off of sold products at planned cost.

How to close account 20 at the end of the month:

- Dt40 Kt20 - write-off of the actual cost of manufactured products;

- Dt43 Kt40 and Dt90-02 Kt40 are adjusting entries that bring the planned cost to the actual cost.

Direct implementation

This method of closing an account. 20 applies when the manufactured goods are not stored in a warehouse, but are immediately sold by the buyer. In this case, the costs are immediately written off to the cost of sales - Dt90-02 Kt20.

Nomenclature groups in production documents

Particular attention should be paid to the item groups that you indicate for the debit and credit of account 20. Because if they do not match, then at the end of the period there will be a balance on account 20.

Let's give a conditional example. Typically, materials are transferred to production using the “Requirement-invoice” document in the “Production” section.

So in this document, in addition to the name and quantity of raw materials, the cost account, the department to which the material is transferred and the nomenclature group are indicated.

And it is very important to indicate the same product group when releasing finished products in the document “Production Report for a Shift” in the “Production” section.

If you have many item groups, then a situation may arise that you transferred materials to the production of goods with the item group “Shoes”, but in the end produced goods under the item group “Shoes”. And for the program these are different groups. Accordingly, in this case, the cost of finished products will be incorrectly calculated and account 20 will remain open.

Another nuance is the composition of nomenclature groups.

There are often situations where the same type of product is listed in different product groups. For example, the product “Shoes” is used in the product groups “Men’s Footwear” and “Women’s Footwear”. In this case, the program does not know what to attribute certain costs to and therefore does not do this at all or displays an error when closing the month.

Subaccounts

For account 20 the following recommended sub-accounts can be opened for the main activities of the enterprise:

- 20-01 “Crop production”. This takes into account the costs of crop production and its branches - horticulture, floriculture, growing seedlings.

- 20-02 “Livestock” - accounting for the costs of output from livestock farming and its industries - dairy and beef cattle breeding, sheep farming, fish farming, beekeeping, etc.

- 20-03 “Industrial production”. This subaccount reflects all direct costs associated with the manufacture of goods, preparation and development of production, other production costs, as well as production maintenance and management costs.

- 20-04 “Other main production” - cost accounting for other main activities of manufacturing enterprises.

Accounting for wages of production workers

Often, the amount of wages of production employees hangs on account 20, and this happens due to incorrect settings of accruals.

The first reference book, which is responsible for this, is located in the “Salaries and Personnel” section and is called “Methods of salary accounting.” You can open it from the “Salary Settings” item.

In the window that opens, you need to click on the green checkmark “Reflection in accounting” and select “Wage accounting methods”.

In this directory, all options for attributing wage costs to salaries should be created, taking into account accounting accounts, cost items and item groups. For example, you have employees involved in the production of shoes, those responsible for clothing and administrative personnel. In this case, you should have three options for reflecting expenses:

- Dt 20.01, cost item “Payment”, Nomenclature group “Footwear”;

- Dt 20.01, cost item “Wages”, Nomenclature group “Clothing”;

- Dt 26, cost item “Payment”.

If you have a division of employees by a specific type of product, for example, there is a cutter responsible for certain shoes, then this type of product can also be indicated in the method of accounting for salaries, as in the figure below.

After preparing the salary accounting methods, we will move on to setting up accruals. To do this, in the “Salary and Personnel” section, select the “Salary Settings” item.

In the window that opens, click on the green checkmark “Payroll calculation” and select the “Accruals” item.

For each method of salary accounting, you need to create your own accrual type, which you can then use in personnel recruitment or transfer. The most convenient way to create new accruals is by copying, for example, the “Payment by salary” accrual. In this case, you will only need to change the name, code and indicate the reflection method.

If these settings are not completed, then the salary of the production department will not be included in the cost of manufactured products, or will hang on account 20 due to non-indication or incorrect indication of item groups.

Interaction with other accounts

Account correspondence 20 on debit is carried out with the following sections:

- Section 1 - 02, 04, 08.

- Section 2 - 10, 11, 16.

- Section 3 - 20, 21, 23, 25, 26, 28, 29-3.

- Section 4 - 40, 41, 43.

- Section 6 - 60, 68, 69, 70, 71, 73, 75, 76, 79.

- Section 8 - 94, 96.

On loan account 20 interaction with other accounts is carried out as follows:

- Section 2 - 1, 11.

- Section 3 - 21, 28.

- Section 4 - 40, 43.

- Section 6 - 76, 79.

- Section 8 - 90, 91, 94, 99.

Main characteristics

There are accounts that must be closed at the end of the period, since they reflect the results of business activities that form profits and losses. These include account 20 “Main production”.

The name of the account speaks for itself - it reflects the main activities of the enterprise, that is, direct costs for the formation of the cost of products (works, services).

From the author! It doesn’t matter whether the company is producing products or providing services, the main condition for using the 20th account is the presence of a core activity.

The costs of producing products (works, services) are accumulated in the debit of the account. In addition to expenses, there is the material value of work in progress.

When the work is completed, the loan account is closed. However, this may be the detection of a manufacturing defect. In such cases, 20 must be closed for the amount of unusable goods:

- Dt 28 “Defects in production” Kt 20 “Main production”.

Direct expenses that are usually attributed to account 20:

- Purchase of raw materials and materials involved in the production process.

- Remuneration and contributions to the budget of production workers.

- Repair and depreciation of production equipment.

- Expenses for modernization and innovation.

- Other costs.

20 is essentially active. Closing account 20 using manual operations is a long and labor-intensive process, since analytical accounting is deployed on it:

- according to the nomenclature that contains types of activities;

- by department;

- by cost items;

- on the work of production programs (if there are investment projects).

Account postings 20

All transactions performed under debit 20 show the accrual, reflection and accounting of the cost of all materials and costs of manufacturing products.

Typical wiring

The correspondence with Section 1 reflects the inclusion of depreciation costs in the cost of production:

- Dt20 Kt02 - for products used in primary production and trade;

- Dt20 Kt04 - for depreciation of intangible assets;

- Dt20 Kt08 - construction costs are reflected.

Correspondence with Section 2 reflects the write-off of the cost of materials:

- Dt20 Kt10 - the cost of materials written off for main production is taken into account;

- Dt20 Kt11 - write-off of the cost of animals for the main production is taken into account;

- Dt20 Kt16 - writing off the amount of deviations in the cost of materials.

The correspondence with Section 3 reflects the inclusion in the cost of other types of expenses:

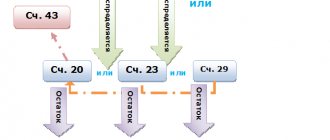

- Dt20 Kt20 - intra-production turnover of products;

- Dt20 Kt21 - transfer of self-made semi-finished products to the main production;

- Dt20 Kt23 - inclusion in the cost price of the cost of services of auxiliary production;

- Dt20 Kt25 - inclusion of overhead costs in the cost of production;

- Dt20 Kt26 - inclusion of general business expenses in the cost of production;

- Dt20 Kt28 - inclusion in the cost of losses from defects;

- Dt20 Kt29 - inclusion in the cost of production the cost of services of service industries and farms.

Correspondence with Section 4 occurs as follows:

- Dt20 Kt40 - write-off of planned cost;

- Dt20 Kt41 - transfer to the main production of goods purchased for sale;

- Dt20 Kt43 - supply of finished products for the needs of the main production.

Correspondence with Section 6 occurs as follows:

- Dt20 Kt60 - payment to third parties for services provided for the main production;

- Dt20 Kt68 - inclusion of taxes and fees in the budget in the cost of production;

- Dt20 Kt69 - calculation of insurance premiums for employees of the main production;

- Dt20 Kt70 - payroll;

- Dt20 Kt71 - payment of expenses of accountable persons for the needs of the main production;

- Dt20 Kt73 - inclusion of compensation for wear and tear of personal property in the cost of production;

- Dt20 Kt75 - contribution of the main production costs by the founders of the enterprise;

- Dt20 Kt76 - inclusion of insurance costs in the cost price;

- Dt20 Kt79 - inclusion of separate production costs in the cost price.

Correspondence with Section 8 occurs as follows:

- Dt20 Kt94 - inclusion in the cost price of the amount of identified shortages for various reasons (from damage to property, based on inventory results);

- Dt20 Kt96 - accrual from the cost of production of amounts to the reserve for future expenses (for repairs, vacation pay).

Note! Entries for credit 20 reflect the receipt of materials, waste, and finished products from the main production.

The relationship with Section 2 reflects the return of materials and supplies from main production:

- Dt10 Kt20 - taking into account unused materials and waste.

- Dt11 Kt20 - increase in the cost of animals due to weight gain.

Correspondence with Section 3 accounts occurs as follows:

- Dt21 Kt20 - receipt of self-made semi-finished products from the main production;

- Dt28 Kt20 - reflection of losses in the cost of irreparable defective products.

Correspondence with Section 4 accounts:

- Dt40 Kt20 - write-off of the actual cost of manufactured products;

- Dt43 Kt20 - posting of finished products.

Capitalization of finished products

The relationship with the accounts of Section 6 reflects:

- Dt76 Kt20 - reduction in the cost of work in progress;

- Dt79 Kt20 - performance of work by the main production.

Correspondence with Section 8 occurs as follows:

- Dt90 Kt20 - write-off of actual cost;

- Dt91 Kt20 - write-off of works or services of the main production;

- Dt94 Kt20 - reflection of the amounts of shortage of work in progress identified during the inventory process;

- Dt99 Kt20 - the costs of the main production are attributed to the losses of the enterprise.

Closing the 20th account in 1C

The topic of closing the 20th account never loses its relevance and raises a large number of questions from both beginners and experienced accountants. We will discuss the procedure for closing an account depending on the nature of the enterprise’s activities and the operations reflected in the program. Using the example of the 1C: Accounting program ed. 3.0 we will look at how the closure of cost accounts is automated, what accounting policy settings affect the correctness of transactions. We’ll also talk about the main mistakes that may occur.

Account 20.01 is closed monthly (except for cases where part of the costs remains in work in progress). Closing an account in the program is automated and occurs as a routine operation at the end of the month. That is, if all operations in which the 20th account is involved are reflected correctly in the program, then it will close automatically.

Let's start with the organization's accounting policy settings. To check the accounting policy settings in the 1C: Accounting program 8th ed. 3.0 you need to go to the Main → Accounting Policy section. Here we indicate what types of activities are reflected in account 20.01 “Main production”. The program provides us with a choice of one of two options: “Production of products” or “Performing work, specifying services.” After selecting the setting option in the “Closing the month” processing, the routine operation “Closing accounts 20, 23, 25, 26” appears, which is responsible for automatically closing the account.

Next, you need to determine the procedure for closing the 20th account: “without taking into account revenue”, “taking into account all revenue”, “taking into account revenue only from production services”. In the first case, account 20.01 is closed immediately, secondly, the account will be closed only if there is revenue from the item group selected on the 20th account, and thirdly, it depends on the availability of the document “Provision of production services” in the current period.

Now let’s check the settings for closing the 20th account in tax accounting. Here I want to make a small digression and say that there are often situations when account 20.01 is closed in accounting on 90.02, and in tax account on 90.08. This contradicts the accounting methodology and entails incorrect completion of the “Income Tax Declaration” (direct expenses fall into indirect expenses). To prevent this from happening, you need to go from the “Main” section to the “Taxes and Reports” subsection → “Income Tax” and set the “List of direct expenses”. Here we indicate the main cost items, or more precisely, the main types of expenses specified in them in tax accounting, which should be classified as direct expenses. Typically, the following list of types of expenses is indicated here (if necessary, it can be adjusted): “Depreciation”, “Material costs”, “Taxes and fees”, “Payroll”, “Insurance premiums”, “Other expenses”. In total, each direct cost account has six entries, each of which is filled out, as shown in Figure 1 (only the type of expense in NU and the debit account are selected). Important note: this list must be created annually, since the validity period is set for a specific working year.

After the accounting policy settings have been checked, we will look at examples of how the 20th account is closed. The bakery “Tasty Like Grandma’s”, which produces baked goods, will help us with this.

The organization produces products monthly, issuing them in the “Shift Production Report” program in the “Production” section. This document creates an entry for the debit of account 43 and the credit of account 20 for the planned cost of finished products. When closing the month, the program will adjust the cost of production to the actual cost, calculated based on the actual costs collected on account 20.01.

Now about the actual costs. The most common of them are material expenses, wages of workers employed in the main production and salary taxes, depreciation of fixed assets related to the main type of activity, and services of third-party organizations.

Everything is clear with material expenses, we write it off to the 20th account using the document “Requirement-invoice” or fill out the “Materials” tab in the Production Report for the shift. Be sure to indicate the invoice and cost item, item group.

Salaries of workers in primary production. The way wages are reflected in accounting is determined by the way wages are reflected, which is configured in the “Pay and Personnel” section, subsection “Salary Settings” → “Reflection in Accounting”. We also indicate invoice 20.01, the cost item “Payment” and fill in the fields “Nomenclature group”, “Products”. (Figure 2). Personal income tax and contributions will be automatically charged to the same account.

As for depreciation of fixed assets, the cost account we need is specified in the method of reflecting depreciation selected in Acceptance for accounting of fixed assets. Depreciation is calculated using a routine operation at the end of the month.

If there are services from third-party organizations, then in the document “Receipts (acts, invoices)” select account 20.01 and item group.

After all operations have been completed, you can proceed to closing the month. To do this, go to the “Operations” section → Closing the period → Closing the month. When the closure of the month is completed, open the routine operation “Closing accounts 20, 23, 25, 26”, click “Show transactions”. We see that account 20.01 is closed on 90.02 in accounting and tax accounting (Figure 3). This is the correct behavior of the program in accordance with accounting methodology. If you need to leave a balance on account 20.01 for the current month, you can use the document “WIP Inventory” in the “Production” section indicating the cost account and item group.

If, when performing a routine operation, errors occur or the closing of the month is completed, but the final balance remains on the 20th account and, according to the Accounting Policy settings, the account is closed taking into account all revenue, you need to create a balance sheet for accounts 20.01 and 90.01.1, grouped by nomenclature groups. The item groups of the accounts must match.

This concludes our conversation. We have discussed the procedure for closing the 20th account depending on the operations carried out in the program and the accounting policy settings. I hope you find the information here helpful, thank you for your time, and good luck with your accounting!

If you would like to receive individual advice on this issue, you can contact our 1C Consultation Line. If an oral consultation is not enough, our expert can remotely connect to your computer and help you find the optimal solution to the problem. The first consultation is completely free!

If you liked the article, like it and share it with your colleagues.

Work in 1C with pleasure!

General information

Let's define what belongs to work in progress:

- material assets that are in production, in addition, not yet participating in the production process, but accepted into it,

- manufactured products, but not shipped to a warehouse for storage.

To establish the amount of work in progress, initially at the end of the reporting month, all material assets are taken into account and then their value is determined.

Upon completion of the work, it is necessary to close the loan account. If a defect is detected during the production process, 20 the account is closed for the amount of defective products: Dt 28 “Defects in production” Kt20 “Main production”. The entries in the debit of account 20 take into account direct costs that are directly related to the manufacture of main products, activities performed and services provided. In addition, the costs of various related productions, losses incurred from low-quality products and other costs (25.26 accounts) for management and service work related to the main production.

Credit 20 of the account takes into account the return of semi-finished products and raw materials from production and the write-off of accumulated expenses for finished goods. According to PBU 10/99, production costs and

provision of products to the buyer is classified according to the following types:

— material costs (purchase of raw materials for use in the production process),

- salary,

— social plan accruals on wages,

— repair (depreciation) of fixed capital (equipment),

- other expenses.

Each enterprise establishes a more detailed list of costs independently.

Three Cost Allocation Methods

Three methods have been adopted for allocating costs for main production:

- Straight.

- Indirect (intermediate).

- Direct sales of manufactured products.

Ease of direct sales of manufactured products

The simplest of them is direct implementation. It is suitable for companies that provide services. Since the issue of trade, defects and work in progress does not arise, you can apply the accounting certificate in 1C, regardless of the configuration.

It is necessary to create a balance sheet for account 20 in order to see the final balance at closing. Go to the “Accounting, Taxes, Reporting” menu, “Accounting” submenu. Find the section “Operations entered manually” or “Operations log” and click the “Create” button. You need to enter the following wiring into the operation:

- Dt 90.02 “Cost of sales” Kt 20 - enter the debit balance from the balance sheet.

From the author! With this method, detailed analytics are not carried out. All costs add up to 2-3 standard types, otherwise transactions to close account 20 will take a lot of time.

For example, for Creator LLC, renting its own non-residential premises is the main activity. The cost of rent consists of a variety of direct and indirect costs. Account 20 collected expenses in the amount of 6,000,000 rubles:

- utility costs for the maintenance of rented premises;

- repair and emergency work;

- salaries of employees serving tenants;

- taxes and fees on employee salaries;

- rental of land plots on which buildings stand.

Table 1. Analysis of account 20 for August 2022 Limited Liability Company "Creator"

| Cor. Check | Debit | Credit | ||

| Opening balance | ||||

| 02 | 740.953,52 | |||

| 10 | 633.633,68 | |||

| 23 | 1.589.272,19 | |||

| 26 | 602.185,03 | |||

| 60 | 1.200.496,72 | |||

| 69 | 264.734,74 | |||

| 70 | 882.449,12 | |||

| 71 | 19500,00 | |||

| 76 | 66.775,00 | |||

| 90 | 6.000.000,00 | |||

| Turnover | 6.000.000,00 | 6.000.000,00 | ||

| Closing balance | ||||

Output data: BU (accounting data)

Once a month, the accounting department issues acts to tenants using the document “Sales of services” in 1C, which generates the following transactions:

- Dt 62.01 “Settlements with buyers and customers” Kt 90.01 “Revenue” - for the rental amount of 9,400,000 rubles;

- Dt 90.03 “Value Added Tax” Kt 68.02 “Value Added Tax” - 18% VAT in the amount of RUB 1,433,898.31 is allocated. to be paid to the budget.

When closing a period, the method of direct sales of released products is used:

- Dt 90.02 Kt 20 - the actual cost of 6,000,000 rubles is closed.

Therefore, net revenue will be:

- 9,400,000 - 1,433,898.31 - 6,000,000 = 1,966,101.69 rubles.

When the actual cost is unknown

The direct method is used in manufacturing enterprises if the actual cost of finished products is unknown. Therefore, the company takes into account costs at the planned cost, and at the end of the month makes an adjustment, bringing the price of manufactured products to the actual price. Wiring used:

- Dt 43 “Finished products” Kt 20 - for the amount of adjustment;

- Dt 90.02 Kt 43 - deviations of the actual cost from the planned cost are written off.

Using an intermediate method

The indirect method involves the participation of 40 “Release of products (works, services)”. It simultaneously takes into account the planned (credit) and actual (debit) cost. Balance at 40 is the resulting deviations. The accounting department needs to close interim accounts at the end of the month:

- Dt 43 Kt 40 - finished products are received at the planned price;

- Dt 90.02 Kt 43 - products sold are written off at planned cost;

- Dt 40 Kt 20 - the cost of production is written off in fact;

- Dt 43 Kt 40 - adjustment between two costs;

- Dt 90.02 Kt 40 - all adjustments are written off.

From the author! Using the interim cost allocation method involves manually closing the month.

Closing an account

Closing is carried out at the end of the reporting month or upon the end of the production period or cycle. Often the 20 account has no balance, that is, it is reset to zero. If a debit balance has formed for “Main Production”, then it will reflect the value of work in progress as of a specific date. This balance is carried forward to the beginning of the next reporting period. Closing account 20 can be carried out for certain types of goods, works or services produced, and for other analytical registers the balance will be reflected in the form of work in progress.

Closing can be done in one of the following ways:

- straight;

- intermediate;

- direct sales of released products.

The closing methodology and cost allocation basis are prescribed in the accounting policy and cannot be changed or canceled during the reporting period.

Here is a brief instruction on how to close a 20 account using the direct method. During the reporting period or production cycle, there is no accurate information about the price of the product. Production results are reflected at deemed cost. You can take into account prices at planned cost, but accounting at actual cost during the reporting period is not allowed. After its completion, the accountant will already know the amount of the actual cost, after which the appropriate adjustment will be made to close the 20th account.

Postings at closing

The accounting entries in this case will be as follows:

- Dt 43 Kt 20 - adjustment to the actual cost;

- Dt 90.02 Kt 43 - reflection of deviation.

For the intermediate method, account 40 “Product Output” is used. It reflects data on the deviation of the planned value from the actual value. The debit reflects the fact, and the credit shows the plan.

Closing of account 20 is carried out after writing off the resulting deviation according to the following transactions:

- Dt 40 Kt 20 - write-off of actual cost;

- Dt 43, 90.2 Kt 40 - bringing the planned indicator to the actual one.

When directly selling released goods, works or services, all products are immediately sold, and costs are written off directly to cost, after which account 20 is closed using posting Dt 90.02 Kt 20.

Account 20 is closed depending on the chosen cost distribution method:

- the balance can only be due to work in progress;

- the direct method writes off 43, 90 accounts;

- the indirect method runs through intermediary accounts 40, 43;

- the direct implementation method debits to account 90;

- in 1C versions 8.2 and 8.3 the account is closed automatically.

In accounting, closing a month is a whole cycle of operations that must be carried out to correctly form the company’s balance sheet.