The time that an employee spends on a business trip (work trip) in accordance with the issued order of the employer is recognized as working time. For these days, the posted worker is paid an average salary, and expenses related to the trip are also compensated.

The period of stay on a business trip (for daily allowances) is calculated by calendar days. It also includes: days of departure and arrival, travel. If these days fall on a weekend, then he can be considered a worker only at the initiative of the employer. Then the daily allowance (or travel allowance) is paid for that day as well. One of the following options may apply to the average daily earnings due:

- The business traveler receives an additional paid day off.

- Or he is paid double his average daily wage.

Both the first and second options are agreed upon with the employer. Expenses for business trips of an individual entrepreneur who works alone, without staff, are not compensated, since he himself is an employer.

For accounting purposes, expenses for business trips are documented in an advance report. At the same time, the accounting department takes into account all expenses that the employer decides to reimburse. Moreover, there may not be documentary evidence here.

Travel allowances are considered expenses for ordinary activities. They are accepted for accounting on the date of signing (approval) of the advance report by the employer.

Above-limit travel allowances, personal income tax and general mandatory contributions for 2017

The employer has the right to send an employee on a business trip in Russia or abroad. The business traveler is compensated daily for travel expenses. The date of payment of daily allowances is the day they are accrued. The day of approval of the business trip report is the date of receipt of income (in the form of daily allowance).

In 2022, a fixed limit on daily expenses has been determined, from which mandatory insurance and personal income tax contributions are not calculated (Read also the article: → “Deadlines for submitting reports on 6-NDFL in 2022”).

| Type of business trip | Legal limit on travel expenses for one day |

| Business trip to Russia | 700 rub. |

| Business trip abroad, outside the Russian Federation | 2,500 rub. |

The tax-free limit on contributions is established at a time; it cannot be determined on a cumulative basis. An organization has the right to prescribe in local regulations its daily allowance for business trips within the Russian Federation and beyond its borders. Moreover, it can exceed a fixed limit. Such daily allowances are called excess (i.e., above the established norm, limit). The amount exceeded by law will be subject to personal income tax and contributions for compulsory insurance (in addition to the injury tax) in the generally accepted manner.

This innovation has been in effect since 2022. Previously, travel expenses were not subject to general mandatory contributions if the limits were specified in the organization’s local acts.

So, from 2022, excess travel expenses are subject to personal income tax and mandatory insurance contributions, regardless of whether the excess amounts are fixed in the internal regulations of the organization or not.

Personal income tax is calculated on the final day of the month in which the business trip report was agreed upon. The tax is withheld after this date on the first payment, mainly from salary. It can be transferred to the budget on the day the income is paid or the day after that, but not later.

Payment procedure

The employee must receive compensation for the entire time he is on a business trip. The company is obliged to pay in this way not only working days, but also all weekends and holidays if they coincide with this period. In this case, the employee’s salary is calculated as usual (double the amount for weekends and non-working holidays). Daily travel allowances are also paid for the period the employee is on the road. For example, if he traveled by train from Moscow to Novosibirsk for three days, then he is also paid daily allowance for these days. Days of forced downtime are also paid. Payment of daily travel expenses in 2022 for public sector employees follows the same rules.

In order to make the payment, an order is issued to send the employee on a business trip, which may also contain an order to charge the employee an advance for the trip. Upon returning, the employee will have to report on the money spent: submit an advance report to the accounting department.

The duration of the business trip can be confirmed by travel documents or a memo if the employee uses a personal or company car to get to the destination and back.

When should business travel allowances be displayed in 6-NDFL?

Since only excess travel expenses are subject to tax, they should be displayed in the reporting - Section 2 6-NDFL. Amounts within the norm (limit) are not subject to personal income tax or general mandatory contributions. Consequently, they are not carried out according to the calculation form.

All above-limit amounts for daily and other payments (for example, severance pay for a dismissed person) are carried out under item “130” of section 2, item “020” of section 1 of 6-NDFL. This rule does not apply to amounts within the limit.

The average earnings that are due for the days of travel are part of the salary. Consequently, it is recognized as income on the final day of the month for which it was accrued. This day is displayed at position “100” in section 2 (

Reflection in 6 personal income tax of the excess portion of daily expenses.

Indicate the date of actual receipt of income for travel expenses as the last day of the month in which the advance report was approved.

This rule is established by subparagraph 6 of paragraph 1 of Article 223 of the Tax Code.

On line 100 of section 2 of the 6-NDFL calculation, indicate - 01/31/2018.

Tax must be withheld directly from the taxpayer’s income upon actual payment of this income (Clause 4, Article 226 of the Tax Code of the Russian Federation). But if, on the date of actual payment, income for personal income tax purposes has not yet been received, tax cannot be withheld. If the tax agent does not pay other amounts in favor of a person in the current year, he is obliged to report the impossibility of withholding tax to the tax authorities and to the person (clause 5 of Article 226 of the Tax Code of the Russian Federation). If the tax was not withheld, enter “00.00.0000” in lines 110 and 120 of section 2.

Rationale How to draw up and submit a calculation using Form 6-NDFL

Situation: how to reflect income that is not taxed within the established standards in the calculation of 6-NDFL

The answer to this question depends on the type of standardized income.

Gifts, prizes, financial assistance

Daily allowances, compensation and other similar income

For personal income tax purposes, daily allowances also fall into the category of standardized expenses (clause 3 of Article 217 of the Tax Code). However, the maximum amount of daily allowance exempt from taxation should be determined not on an accrual basis from the beginning of the year, but on each payment. In this case, the date of actual receipt of income in the form of daily allowances is the last day of the month in which the employee’s advance report on the business trip was approved (subclause 6, clause 1, article 223 of the Tax Code).

In the calculation of 6-NDFL, reflect only the excess portion of the daily allowance. Do not include daily allowances within the standards in the calculation.

For example, in nine months, an employee of the organization went on business trips across Russia twice: - in July. The duration of the business trip is three days. Daily allowances were paid at the rate of 1200 rubles. per day for a total of 3,600 rubles. The advance report was approved on July 25; - in August. The duration of the business trip is three days. Daily allowance was paid at the rate of 1100 rubles. per day for a total of 3,300 rubles. The advance report was approved on August 28.

The daily allowance rate for personal income tax purposes is 700 rubles. in a day. The amount of excess daily allowance was: – for July – 1500 rubles. ((1200 rub. – 700 rub.) × 3 days). Personal income tax amount – 195 rubles; – for August – 1200 rub. ((1100 rub. – 700 rub.) × 3 days). Personal income tax amount – 156 rubles.

The dates of actual receipt of income are July 31 and August 31, respectively. The accountant withholds personal income tax from the nearest cash payments - August 3 and September 5.

In calculating 6-NDFL for nine months, the accountant reflected the excess daily allowance and the tax withheld from it as follows:

in section I:

– on line 020 – 2700 rubles; – on line 040 – 351 rubles; – on line 070 – 351 rubles;

in section II:

– on line 100 – 07/31/2018; – on line 110 – 08/03/2018; – on line 120 – 08/06/2018; – on line 130 – 1500 rubles; – line 140 – 195 rubles;

– on line 100 – 08/31/2018; – on line 110 – 09/05/2018; – on line 120 – 09/06/2018; – on line 130 – 1200 rubles; – on line 140 – 156 rubles.

The same procedure applies to other income, which is normalized with each payment.

Section 2

Section 2 indicates the dates of receipt and withholding of tax, the deadline set for transferring tax to the budget, as well as the amount of income actually received and withheld personal income tax. To correctly fill out section 2, all income will have to be grouped: – by the dates when they were actually paid; - according to the timing when the personal income tax amounts withheld from these incomes must be transferred to the budget.

That is, for each date of actual payment, indicate a separate tax amount. And if on the same day you paid income for which different deadlines for paying personal income tax were established, then these amounts must also be indicated separately. This is stated in the letters of the Federal Tax Service dated May 11, 2016 No. BS-4-11/8312 and dated March 18, 2016 No. BS-4-11/4538.

When filling out section 2, indicate all transactions in chronological order. There is no need to group them according to the tax rates specified in section 1. If the page runs out of free lines 100–140, go to the next page. It doesn't matter that it may start from section 1 for a different tax rate. Continue making transactions in a row. If there are more pages with completed sections 1 than are needed to fill out section 2, then put dashes in the empty lines 100–140. Such clarifications are in the letter of the Federal Tax Service dated April 27, 2016 No. BS-4-11/7663.

In section 2, include only those transactions that relate to the last three months of the reporting period (letter of the Federal Tax Service dated February 18, 2016 No. BS-3-11/650). In this case, focus on the date no later than which personal income tax must be transferred to the budget. That is, reflect the income paid and the tax withheld in the reporting period in which the deadline for paying personal income tax falls. It doesn't matter when you actually paid the income, withheld and remitted the tax. For example, in section 2 of the calculation for nine months, you need to reflect data on the payment of income (tax withholding), for which the deadline for paying personal income tax falls for the period from July 1 to September 30 inclusive. Such clarifications are given in the letter of the Federal Tax Service dated October 24, 2016 No. BS-4-11/20126.

Please complete Section 2 in this order.1

on line 100 – the date of actual receipt of income. For example, for income in the form of wages - this is the last day of the month for which the salary was accrued, and for remuneration under civil contracts - the day the remuneration is paid,

on line 110 – tax withholding dates;

on line 120 – dates no later than which the tax must be transferred to the budget. Indicate these dates in accordance with paragraph 6 of Article 226 and paragraph 9 of Article 226.1 of the Tax Code (letter of the Federal Tax Service dated January 20, 2016 No. BS-4-11/546). As a rule, this is the day following the day the income is paid. But, for example, for sick leave and vacation pay, the deadline for transferring tax to the budget is different: the last day of the month in which such payments were made. If the established deadline for tax transfer falls on a weekend, in line 120 indicate the next working day (clause 7, article 6.1 of the Tax Code, letter of the Federal Tax Service dated May 16, 2016 No. BS-4-11/8568);

on line 130 – the amount of income (including personal income tax) received as of the date that the tax agent indicated on each line 100;

on line 140 – the amount of tax that the agent withheld as of the date on each line 110.

This is stated in paragraphs 4.1–4.2 of the Procedure approved by Order of the Federal Tax Service dated October 14, 2015 No. ММВ-7-11/450.

If tax was not withheld from the payment (for example, for payment in kind or because deductions exceeded accruals), enter “00.00.0000” in lines 110 and 120 of section 2. These are the latest clarifications from the tax service (see letters from the Federal Tax Service dated 08/09/2016 No. GD-3-11/3605, dated 08/05/2016 No. GD-4-11/14373 and dated 08/01/2016 No. BS-4-11/13984). The Order does not say what to indicate in lines 110 and 120 in such situations. Previously, tax department specialists advised entering here the same dates as in cases where the tax was withheld (letter of the Federal Tax Service dated March 28, 2016 No. BS-4-11/5278). If you followed these recommendations, there will be no penalties for calculation errors. It is not necessary to submit updated calculations and correct withholding dates to zero. If the Federal Tax Service Inspectorate asks you to explain why personal income tax was not withheld if you had income, send an explanation to the inspectorate.

Uniform requirements for registration of 6-NDFL

This is a standard reporting form according to which a tax agent (individual entrepreneur, organization) reports for the income of its personnel. The document was introduced and applied since 2016. Its structure consists of a title page and 2 sections. This type of reporting is generated on an accrual basis for the first quarter, six months, 9 and 12 months.

Form 6-NDFL

Entries are made based on available information on income, deductions, and personal income tax. The tax agent must enter the information. He also submits the completed document to the Federal Tax Service.

The rules for filling out this form are determined and formalized by the Federal Tax Service of the Russian Federation. Amounts and details are required to be filled out. If there are not enough pages for the information that needs to be entered, then the required number of pages is taken to fill out. In familiar places that are not filled in, dashes are added.

The form can be filled out on a computer and printed. Then dashes are not placed in empty positions. The font used is Courier New 1 (6-18 points).

The date is written on each completed page and the signature of the head of the organization (individual entrepreneur, notary, lawyer, representative of the tax agent) is affixed.

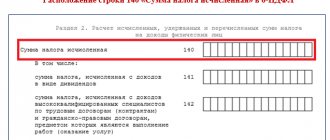

The procedure for displaying above-limit travel expenses in 6-NDFL

In order to display excess amounts, Section 2 of 6-NDFL is drawn up. Here the dates and amounts of income and personal income tax are specified. The section includes 5 lines.

| Key points of section 2 line by line | Section 2 details (what does it include?) |

| Page “100” (Date of actual receipt of income) | This refers to income, the size of which is displayed at position “130”; the last day of the month is written (Article 223 of the Tax Code of the Russian Federation); sickness benefits and vacation pay are recorded on the actual date of receipt |

| Page “110” (Dating of withheld personal income tax) | Income tax is withheld on the day the actual income is received (displayed in position “130”), and it is from this that the tax is calculated |

| Page “120” (Date of income transfer) | The duration is influenced by the type of income: sickness benefits and vacation pay are issued before the end of the month; in some cases, the information is reflected the next day after receiving the money. Usually the date is recorded here, no later than which personal income tax is deducted |

| Page “130” (Amount of income received) | This includes: the exact amount of total actual income without deduction of withholding tax; amount of excess travel allowances |

| Page “140” (Value of withheld personal income tax) | The summed personal income tax that was withheld on the date recorded in position “110” |

If the beginning of an operation belongs to one reporting period, and the end to another, then section 2 of this form records information on the final period.

Example 1. Display and calculation of excess travel expenses, income tax, income in 6-NDFL

An employee of Proekt LLC, Tsarev N.M., was on a three-day business trip (July 2022) around the Russian Federation. His daily allowance for 3 days amounted to 3,000 rubles. (1,000 rubles for each business trip day). The advance report that the traveler submitted to the director was approved on July 28, 2017.

Tsarev N.M.’s accrued July pay amounted to 70,000 rubles. So, for July 2022 he was paid:

- 07.2017 - advance payment towards pay 35,000 rubles;

- 08.2017 - the balance of July earnings, taking into account the withheld income tax on it and on travel expenses.

The calculated tax was received by the budget on August 4, 2017. Daily travel allowances issued to an employee (1,000 rubles) exceed the fixed limit, i.e. 700 rubles. This means that personal income tax must be withheld from the difference, i.e., the amount exceeding the limit. Accordingly, this fact should be reflected in 6-NDFL (section 2, for 9 months).

| Calculation of amounts for pay, personal income tax and travel allowances | Line-by-line display of above-limit travel allowances issued to Tsarev N.M. (6-NDFL, section 2) |

| The total amount of travel allowances issued to N.M. Tsarev for 3 days of the business trip: 1,000 * 3 = 3,000 rubles. Amount of daily allowance for 3 days of a business trip, from which, by law, personal income tax does not need to be calculated: 700 rubles. per day * 3 days = 2,100 rub. The amount of daily allowance exceeding the limit is withheld from personal income tax (13%): 3,000 – 2,100 = 900 rubles. Personal income tax withheld from the excess amount of daily allowance: 900 rubles. * 13% = 117 Personal income tax on earnings: 70,000 * 13% = 9,100 rubles. Actual earnings received by N. M. Tsarev for July: 70,000 rubles. + 900 rub. = 70,900 rub. The summed personal income tax from pay and the excess amount of daily allowance: 117 + 9,100 = 9,217 rubles. | Page “100” (Date of receipt of income) - 07/31/2017 Page “110” (Dating of personal income tax withholding) - 08/3/2017 Page “120” (Dating of personal income tax enrollment) - 08/04/2017 Page “130” (Amount of actual salary of Tsarev N.M.) - 70,900 rubles. Page “140” (Total amount of personal income tax withheld) - 9,217 rubles. |

Dates for excess daily allowance

To reflect the amount of excess daily allowance in form 6-NDFL, it is necessary to determine the dates that will be indicated in Section 2 of the Calculation.

The date of actual receipt of income for daily allowances subject to personal income tax is the last day of the month in which the advance report is approved after the employee returns from a business trip (clause 6, clause 1, article 223 of the Tax Code of the Russian Federation). Thus, this date must be indicated on line 100 “Date of actual receipt of income” of form 6-NDFL.

The date of tax withholding (line 110) will be the date of actual payment of income from which personal income tax was withheld (clause 4 of Article 226 of the Tax Code of the Russian Federation). It is important to keep in mind that this date cannot be earlier than the last day of the month, because personal income tax cannot be withheld if income is not received. And since the income was received on the last day of the month, then personal income tax can be withheld at the next payment of income made on the last day of the month or later (Letter of the Federal Tax Service dated April 29, 2016 No. BS-4-11/7893).

Accordingly, personal income tax on excess daily allowances must be transferred no later than the business day following the day when personal income tax was withheld from daily allowances.

Example 2. An example of the design of section 2 of 6-NDFL for above-limit business trips

An employee of Proekt LLC, Tsarev N.M., was on a business trip around Russia from August 1 to August 5, 2022. He was given an advance with daily allowance (5,000 rubles) on August 28. The amount of excess travel allowances was 5 * (1,000 – 700) = 1,500 rubles. The advance report was submitted to the director of Proekt LLC on August 8, 2017.

Thus, Tsarev N.M. was given: 08/15/2917 an advance on pay, the balance on pay - 09/06/2017 and vacation pay on 09/1/2017. Section 2 6-NDFL (for 9 months) is drawn up line by line as follows:

- «100»: 31.08.2017.

- «110»: 01.09.2017.

- «120»: 04.09.2017

- “130”: 1,500 rub.

- “140”: 195 rub.

Sample of filling out section 2 of form 6-NDFL