Briefly about the history of the taxation system in Russia

The tax system of the Russian Federation began to take shape after the collapse of the USSR, namely in December 1991.

Then the law “On the Fundamentals of the Tax System of the Russian Federation” was adopted. He introduced new taxes and fees, for example, VAT, income tax, excise taxes on alcohol and tobacco products and others. In 1998, the 1st part of the Tax Code of the Russian Federation was approved, in 2000 - the 2nd part. This code has become the main legislative act in the Russian tax system. The Tax Code of the Russian Federation determined the relationship between the state and taxpayers, the structure and elements of the Russian tax system. Separately, it is worth highlighting the formation of state bodies to supervise taxation in the Russian Federation. In 1990, the State Tax Inspectorate was created, which was then transformed into the State Tax Service. In 1998, the Ministry of Taxes and Duties appeared. In 2004, it was reorganized, and its functions were transferred to the Ministry of Finance of the Russian Federation. From the same year, the well-known Federal Tax Service began to function, which continues to operate to this day.

The tax system is... (concept and structure)

The tax system of the Russian Federation can be defined as the totality of all taxes and fees adopted in Russia, as well as administrators of taxes and fees (government bodies) and their payers.

The structure of the Russian tax system implies a complex interaction of all its constituent elements: taxes (and, since 2017, also insurance premiums) and fees, their payers, the legal framework and government bodies.

The structure of the tax system of the Russian Federation has 3 levels:

- federal;

- regional;

- local.

The tax level determines the corresponding budget level to which it is credited.

Since the tax system of the Russian Federation has a 3-level structure, the legislative framework on taxes and fees is also divided into 3 levels:

- Federal legislation is the highest level of the legislative framework. It operates throughout the Russian Federation. By-laws and other normative legal acts must not contradict it. This category includes both parts of the Tax Code of the Russian Federation, federal laws that are consistent with the provisions of the Tax Code of the Russian Federation, decrees of the President of the Russian Federation, resolutions of the Government of the Russian Federation and, of course, the Constitution of the Russian Federation.

- Regional legislation includes the laws of the constituent entities of the Russian Federation on taxation in a specific region of our country.

- Local legislation consists of normative legal acts that are adopted by representative bodies of local government (councils of deputies, legislative assemblies).

Research staff of Nizhny Novgorod State University named after. N.I. Lobachevsky conducted a study assessing the risks and effectiveness of various tax systems at different levels of the budget system. You can get acquainted with the conclusions of Doctor of Economic Sciences M. Yu. Malkina and her assistants in ConsultantPlus. If you do not have access to the K+ system, get a trial online access for free.

In addition, on the basis of the Tax Code of the Russian Federation, the Ministry of Finance of the Russian Federation and the Federal Tax Service of the Russian Federation develop orders, clarifications, clarifications, letters and other similar documents. They are necessary to specify the provisions and articles of the Tax Code of the Russian Federation and other federal laws of the Russian Federation in the field of taxation. Such documents clarify situations that are unclear from the point of view of taxpayers and can be drawn up on the basis of their requests.

Read more about federal, state and local taxes in this article.

Federal taxes

All economic entities on the territory of the Russian Federation pay taxes in this group according to the same rules. These rules, as well as any changes made to them for these taxes, are determined only by the provisions of the Tax Code of the Russian Federation.

Among federal taxes, special regimes constitute a special category (Section VIII.1 of the Tax Code of the Russian Federation).

Their peculiarity is that when using any special regime, the taxpayer has the right not to pay some other federal, regional and local taxes.

In addition, starting from 2022, the Tax Code of the Russian Federation also regulates the payment of mandatory payments to social funds (Chapter 34). Although the listed insurance premiums, strictly speaking, do not relate to taxes (since they are not gratuitous payments, but assume the receipt of insurance compensation in the future), they can also be conditionally classified as a “federal” group.

Despite their name, not all taxes in this group are credited to the federal budget. Only VAT, water tax, excise taxes (not all, only for certain types of goods) and mineral extraction tax in terms of hydrocarbon raw materials are fully included in it. The remaining federal taxes are partially, in various proportions provided for by the Budget Code of the Russian Federation (Chapters 7-9), credited to regional and local budgets. This is how one of the main functions of taxes manifests itself - regulatory. The government, by redistributing financial flows between various budgets, stimulates the development of priority sectors or regions.

Elements of the tax system of the Russian Federation

As noted earlier, the tax system of the Russian Federation involves the interaction of all its elements and an integrated approach to solving tax problems. All constituent elements form the tax structure of the Russian Federation.

The structure of the Russian tax system includes:

- all taxes, insurance premiums and fees accepted on the territory of our country in accordance with the Tax Code of the Russian Federation;

- subjects of taxes and fees;

- regulatory framework;

- government authorities in the field of taxation and finance.

Now let's look at each element of the Russian tax system in more detail.

Taxes and fees established in Russia are obligatory for those categories of taxpayers who are responsible for their payment in accordance with the provisions of the Tax Code of the Russian Federation. The concept of tax and fee is defined in the Tax Code of the Russian Federation.

The subjects of taxation are taxpayers (legal entities and individuals) and tax agents, that is, those who, according to the Tax Code of the Russian Federation, pay taxes and fees. As an example of tax agents, we can cite enterprises and organizations that calculate and transfer personal income tax on the accrued income of their personnel, and also submit the corresponding tax reports (6-NDFL) after the end of the tax period (year).

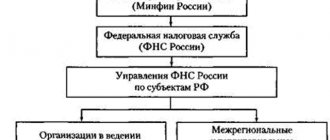

The system of tax authorities of the Russian Federation includes:

- Ministry of Finance of the Russian Federation.

- Federal Tax Service of the Russian Federation.

The Ministry of Finance of the Russian Federation determines the main directions of the tax policy of our state, forecasts tax revenues and makes proposals for improving the tax system of the Russian Federation as a whole. His department includes the Federal Tax Service of the Russian Federation as an executive body of state power.

The main functions of the Federal Tax Service of the Russian Federation are:

- accounting of taxpayers and fees;

- control over compliance with tax legislation requirements;

- supervision and verification of tax accruals, their payment to the relevant budget and tax reporting.

Read about tax audits in our section of the same name “Tax Audits”.

The Federal Tax Service of the Russian Federation is a unified system of all tax authorities. The unified centralized system of tax authorities consists of:

- Management in each subject of the Russian Federation. The territorial tax authorities and inspectorates of the Federal Tax Service of the Russian Federation are subordinate to him.

- Interregional inspections of the Federal Tax Service for each federal district. Subordinate to them are interregional inspectorates for the largest taxpayers, for centralized data processing (DPC), as well as interdistrict inspections.

What are the taxes in the Russian Federation?

In total, there are 14 taxes in our country: 8 federal, including state duty, 3 regional and 3 local. There are 5 special taxation systems that stand a little apart. We will also highlight insurance premiums and the new experimental taxation regime for self-employed persons, introduced in 2022.

Read more about the experiment on taxation of the self-employed here.

Federal taxes throughout the territory of our state have the same tax rates, calculation rules and transfers in accordance with the Tax Code of the Russian Federation. These include:

- personal income tax;

- corporate income tax;

- VAT;

- excise taxes;

- water tax;

- mineral extraction tax;

- state duty.

Special tax systems also fall into this category: simplified tax system, production division, unified agricultural tax and PSN (patent).

Regional taxes are also approved by the Tax Code of the Russian Federation at the federal level. Regional authorities have the opportunity to change taxation conditions at their discretion and within the limits adopted by the Tax Code. For example, regions can set a tax rate, but not more than the amount prescribed in the Tax Code of the Russian Federation. All changes are fixed by the laws of the constituent entities of the Russian Federation. This includes transport tax, gambling tax, and corporate property tax. Regional government bodies can also introduce special tax regimes and make their own changes to them, but in accordance with the provisions of the Tax Code of the Russian Federation.

Local taxes, however, like other taxes and fees in Russia, are also approved by the Tax Code of the Russian Federation. Local self-government bodies can make changes and additions to them within the framework of the Code. Local taxes include:

- land tax;

- property tax for individuals;

- trade fee.

Depending on the manner of collection, taxes can be divided into 2 main categories: direct and indirect. Direct taxes are charged directly on the income or value of the taxpayer's property. Indirect taxes are included in the cost of goods, services and works. In fact, they are paid by the buyer of the product, and the seller acts as an intermediary between the indirect tax and the state. In the Russian Federation there are only 2 indirect taxes: VAT and excise taxes. All others are direct.

For more information about direct and indirect taxes, read the article “What taxes are classified as direct and indirect (table)?”

Classification of tax payments

The key grouping implies the division of all fiscal obligations into three groups:

- Federal - payments, conditions and tax standards for which are approved at the highest level - by the Government of the Russian Federation. For example, personal income tax, income tax, VAT. Regional and municipal authorities cannot set additional conditions, norms and taxation procedures for such payments.

- Regional - obligations, the conditions for application of which are established by the legislative authorities of the region, subject, autonomous region. For example, transport fee.

- Local or municipal are fees that are regulated at the municipal level. For example, land tax.

IMPORTANT!

A complete list of taxes and their types, principles of taxation are enshrined in the Tax Code of the Russian Federation, that is, at the federal level. Regional and local authorities cannot introduce new obligations, but have the right to regulate the taxation procedure for individual obligations (rates, objects of taxation, benefits, deductions, reporting periods, advance payments).

The second most important grouping is classification by method of seizure. There are direct and indirect obligations. Direct taxes include those fees that taxpayers pay directly from income, profits, and property received. For example, personal income tax, property, land, transport taxes.

Indirect is a premium of a certain kind that is included in the cost of a product, work or service. For example, VAT or excise tax.

Read more in the article “Current tax classification with examples”

Types of taxation systems in the Russian Federation: basic, simplified taxation system, etc.

Choosing a taxation system in Russia for business entities is an important event that allows you to determine the tax burden for business. Let's look at the main types of taxation in Russia.

The tax system of the Russian Federation includes 5 tax regimes plus another experimental one (from 2022):

- Basic taxation system (OSNO).

This mode is assigned to a business entity automatically immediately after registration with the Federal Tax Service. It can be used by both LLCs and individual entrepreneurs. The taxpayer has the right to switch to a special regime subject to compliance with the conditions established by tax legislation.

- Simplified taxation system (USNO).

The simplified tax system has the right to be used by taxpayers who:

- the average number of employees does not exceed 100 people;

- the residual value of depreciable fixed assets does not exceed 150 million rubles;

- income for 9 months do not exceed the amount of 112.5 million rubles, adjusted by the deflator coefficient (according to the latest clarifications of the Ministry of Finance in 2022, for the transition to the simplified tax system from 2022, taking into account indexation, it is equal to 123.3 million rubles).

- Unified Agricultural Tax (USAT).

Only agricultural producers have the right to use this regime.

Read about the details of using the Unified Agricultural Tax in the section “Unified Agricultural Tax”.

- Patent (PSN).

PSN has the right to be used exclusively by individual entrepreneurs. The meaning of this regime is that a merchant buys a patent for a certain period not exceeding 12 months.

See here for details.

Tax bases and rates for local taxes

Land tax. The base is the cadastral value of land plots (Article 390 of the Tax Code of the Russian Federation). Rates are set by municipalities depending on the purpose of the land, but cannot exceed 1.5% (Article 394 of the Tax Code of the Russian Federation).

Property tax for individuals. The base is the cadastral value of real estate (Article 402 of the Tax Code of the Russian Federation). Rates are set by municipalities depending on the nature of the property, but cannot exceed 2% (Article 406 of the Tax Code of the Russian Federation).

Trade fee. Base - the area of movable and immovable property that is used for trade at least once during the quarter. Rates are set by municipalities, but cannot exceed the amount of tax on the patent tax system in that municipality, and for retail markets - 550 rubles. (Article 415 of the Tax Code of the Russian Federation).

How to choose the best tax system

- BASIC.

This regime has the highest tax burden:

| Tax | OOO | IP |

| Income tax | 20% | – |

| Personal income tax | – | 13% |

| VAT | 10 or 20% of the markup amount depending on the type of goods | |

| Excise taxes | The rate depends on the type of product | |

| Property tax | The rate is set by regional authorities | |

| MET | The rate depends on the type of minerals | |

| Transport tax | The rate is set by regional authorities and depends on the power of the vehicle | |

| Water tax | The rate depends on the type of water body | |

If your business is just starting to develop, we recommend paying attention to special modes. Let's consider the main one - the simplified tax system.

- USNO

The taxpayer must first decide on the type of taxable object. With the simplified tax system there are 2 of them:

- Income from which 6% is paid to the budget.

- The difference between income and expenses, from which 15% should be transferred to the state.

| pros | Minuses | ||

| Income (6%) | Income minus expenses (15%) | Income (6%) | Income minus expenses (15%) |

| The single tax replaces the income tax (personal income tax for individual entrepreneurs), VAT, property tax (with the exception of the tax calculated from the cadastral value of real estate) | A closed list of expenses that can be used to reduce income received for the year | ||

| One year-end declaration is submitted to the Federal Tax Service | In case of loss, a minimum tax of 1% of income is paid | ||

| Accounting is carried out in a simplified version | |||

| The tax amount can be reduced by the amount of the transferred insurance premiums | Opening branches is not available | ||

To decide which type of simplified tax system to choose, you need to study the amount of documented expenses. If it is at least 60% of the amount of income, then a simplified tax system of 15% is more profitable; if less, then it is better to choose a simplified tax system of 6%.

For the nuances of using the simplified tax system, see the “STS” section.

Practical recommendations on choosing the optimal taxation system for organizations and individual entrepreneurs are provided by ConsultantPlus experts. Get free access and go to Ready-made solutions using the links provided.

Tax bases and rates for federal taxes

Value added tax (VAT). Base - the cost of goods, works, services sold (Article 153 of the Tax Code of the Russian Federation). Rates: 0%, 10% and 20% depending on what goods are sold and to whom (Article 164 of the Tax Code of the Russian Federation).

Excise taxes. Base - the volume or cost of excisable goods sold (Article 187 of the Tax Code of the Russian Federation). Rates depend on the specific product (Article 193 of the Tax Code of the Russian Federation).

Personal income tax (NDFL). The base is the monetary expression of the income of an individual (Article 210 of the Tax Code of the Russian Federation). Rates: 9%, 13%, 30%, 35% depending on the type of income (Article 224 of the Tax Code of the Russian Federation).

Corporate income tax. The base is the monetary expression of profit (Article 274 of the Tax Code of the Russian Federation). Rates: 0%, 5%, 9%, 13%, 15%, 20%, 30% depending on what income led to the formation of profit and what organization received it (Article 284 of the Tax Code of the Russian Federation).

Fees for the use of objects of the animal world and for the use of objects of aquatic biological resources. Base - one harvested land animal or a ton of aquatic biological resources. The rate depends on the type of production (Article 333.3 of the Tax Code of the Russian Federation)

Water tax. Base - the volume of water taken, the area of the water area, the amount of electricity produced, or the product of the volume of rafted wood by the rafting distance, depending on the type of use of water resources (Article 333.10 of the Tax Code of the Russian Federation). The rate also depends on the type of use of water resources (Article 333.12 of the Tax Code of the Russian Federation).

Government duty. The tax base of the Tax Code of the Russian Federation has not been established, but in fact it is a service for performing a legally significant action, or the price of a claim. The rates depend on the specific action (Chapter 25.3 of the Tax Code of the Russian Federation).

Tax on additional income from the production of hydrocarbons. Base is the monetary expression of additional income from the extraction of hydrocarbons at a subsoil site (Article 333.50 of the Tax Code of the Russian Federation). Rate: 50% (Article 333.54 of the Tax Code of the Russian Federation).

Mineral extraction tax (MET). Base - the cost or quantity of minerals extracted from the subsoil and extracted from mining waste, depending on the type of mineral (Article 338 of the Tax Code of the Russian Federation). The rates also depend on the type of mineral (Article 342 of the Tax Code of the Russian Federation).

Results

The Russian tax system involves a complex interaction of all elements that form its structure. The elements of the tax system of the Russian Federation include: taxes and fees, their payers, the regulatory framework and government authorities in the tax field. The structure of the Russian Federation system in the field of taxation has 3 levels: federal, regional and local. At each of these levels, relevant legislative acts are adopted, which should not contradict the provisions of the Tax Code and the Constitution of the Russian Federation.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Federal, regional and local taxes: table 2018

Article of the Tax Code of the Russian Federation in Russia establishes the following categories of taxes and fees:

- Federal taxes are established by the Tax Code of the Russian Federation and apply to all constituent entities of the Russian Federation. Mandatory for payment throughout the country.

- Regional taxes - these taxes, obligatory for payment on the territory of the constituent entities of the Russian Federation, are established by the norms of the Tax Code of the Russian Federation and are introduced in the constituent entities by regional laws. Detailing of rates and tax benefits is carried out differentially at the level of constituent entities of the Russian Federation, unless otherwise established by the Code.

- Local taxes - their list and main parameters are approved by the Tax Code of the Russian Federation; the rules for application and payment in specific territories are prescribed in legal acts issued by municipal authorities.

Federal, regional and local taxes not provided for by the Tax Code cannot be established. Taxation adjustments made at the level of constituent entities of the Russian Federation and individual municipalities are mandatory only in territories that are administratively divided into these regions or settlements. When new taxes are introduced (2018), changes to their general list are permissible only if legislators have updated the relevant information in the Tax Code by their regulatory act.

The Tax Code includes 9 types of obligations listed in Art. 13 Tax Code of the Russian Federation. The funds paid under them are sent in full to the federal budget. The exception is income tax. According to it, the amount is distributed between the federal and regional budgets.

Regional taxes in Russia in 2022 are divided into 3 types, they are approved by Art. 14 Tax Code of the Russian Federation. In relation to these types of tax obligations, the Tax Code regulates the basic provisions. The authorities of the constituent entities of the Russian Federation can detail the rules given in the Tax Code or supplement them with specific requirements. The Code may set rigid rates for these taxes or invite regional authorities, through their legal acts, to independently approve tariffs within a certain range. All payments are accumulated in regional budgets.

Local taxes in 2022 are listed in Art. 15 Tax Code of the Russian Federation. They consist of 2 taxes and one fee. The basic norms for this group of taxes are regulated by the Tax Code of the Russian Federation, and specific rates, benefits, etc. are disclosed in legal acts of municipal authorities. All transfers made by business entities go to local budgets.

A complete list of taxes in the Russian Federation and their distribution by classification categories is given in the table:

| No. | Tax name |

| Federal taxes | |

| 1 | Personal income tax (chapter of the Tax Code of the Russian Federation) |

| 2 | Corporate income tax (Chapter 25 of the Tax Code of the Russian Federation) |

| 3 | Value added tax (Chapter 21 of the Tax Code of the Russian Federation) |

| 4 | Excise taxes (Chapter 22 of the Tax Code of the Russian Federation) |

| 5 | Mineral extraction tax (Chapter 26 of the Tax Code of the Russian Federation) |

| 6 | Water tax (Chapter 25.2 of the Tax Code of the Russian Federation) |

| 7 | Fee for the use of fauna (Chapter 25.1 of the Tax Code of the Russian Federation) |

| 8 | Fee for the use of objects of aquatic biological resources (Chapter 25.1 of the Tax Code of the Russian Federation) |

| 9 | State duty (Chapter 25.3 of the Tax Code of the Russian Federation) |

| Regional taxes | |

| 1 | Enterprise property tax (Chapter 30 of the Tax Code of the Russian Federation) |

| 2 | Tax on gambling business (Chapter 29 of the Tax Code of the Russian Federation) |

| 3 | Transport tax (Chapter 28 of the Tax Code of the Russian Federation) |

| Local taxes | |

| 1 | Land tax (Chapter 31 of the Tax Code of the Russian Federation) |

| 2 | Trade tax (Chapter 33 of the Tax Code of the Russian Federation) |

| 3 | Property tax for individuals (Chapter 32 of the Tax Code of the Russian Federation) |

A separate group of taxes are special tax regimes. Their use guarantees the taxpayer exemption from certain regional and federal taxes. Among the special taxation systems are the simplified taxation system (simplified tax system), UTII (unified tax on imputed income), unified agricultural tax (unified agricultural tax) and patent (Chapter 26.2; 26.3; 26.1 and 26.5 of the Tax Code of the Russian Federation).

Another category of mandatory payments included in Chapter. Tax Code of the Russian Federation - insurance contributions (pension, medical insurance and social insurance, except for “injuries”). The administration of this type of payments has come under the influence of tax authorities since 2022.