Why do you need a job description?

The activity of any organization begins with determining its structure (division into divisions, departments, workshops, blocks and the distribution of functions between them).

In addition, divisions are assigned responsibility for resolving issues related to the range of their tasks. At the same time, some functions may be placed under the jurisdiction of not 1, but 2 or several divisions or, conversely, not be placed under anyone’s control. To eliminate duplication of functions and the absence of those responsible for their implementation, as well as to ensure an unambiguous distribution of responsibilities between departments, the current structure of the organization and the main functions of the departments are fixed in an internal administrative document. Then the goals, objectives, functions, structure and procedure for interaction with other divisions of the legal entity are prescribed in the regulations for each division. The goal of the head of the organization (or the person appointed by him) when approving these documents is to control the completeness of the reflection of the functions performed by the unit and to eliminate their duplication.

The regulations on the unit, giving an idea of the amount of work that this unit will have to perform, serves as the basis for determining its staffing levels, establishing the qualification level and positions of the required employees, distributing responsibilities between them and developing their job descriptions. Including, it provides material for the job description of the head of the department.

The obligation to develop regulations on departments and job descriptions is not fixed at the legislative level. However, they significantly facilitate the life of the organization itself, bringing clarity to the distribution of tasks between departments and employees within them, as well as defining the circle of those responsible for resolving certain issues.

A job description developed for a specific position allows you to:

- define specific functions for this position and simplify the procedure for familiarization with them;

- facilitate the selection of personnel for vacant positions;

- familiarize the employee with his functions against signature, thereby securing him responsibility for their failure to perform them and his right to refuse to perform someone else’s work without additional payment;

- monitor the performance of a specific employee and the correct distribution of functions.

Instructions for a number of positions may be standard, but it is better to develop them for each organization independently and individually, based on the specifics of the activities of a particular legal entity, the characteristics of its industry, structure and delimitation of areas of responsibility between divisions. This document is given legal force by its approval by the head of the organization.

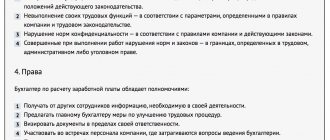

IV. Rights

The chief accountant has the right:

4.1. Represent the interests of the enterprise in relations with other structural divisions of the enterprise and other organizations on financial, economic and other issues.

4.2. Establish job responsibilities for employees subordinate to him, so that each employee knows the range of his duties and is responsible for their implementation. Employees of other departments involved in accounting report to the chief accountant on all issues of organization and maintenance of accounting and reporting.

4.3. Submit proposals for improving economic and financial activities for consideration by the management of the enterprise.

4.4. Sign and endorse documents within your competence.

4.5. Receive in a timely manner from the heads of the enterprise departments (specialists) information and documents (orders, instructions, contracts, estimates, reports, standards, etc.) necessary to perform their job duties. (For untimely, poor-quality execution and preparation of these documents, delay in transferring them for reflection in accounting and reporting, for the unreliability of the data contained in the documents, as well as for the preparation of documents reflecting illegal transactions, the officials who compiled and signed these documents are responsible ).

4.6. Submit for consideration by the director of the enterprise proposals on the appointment, relocation, dismissal of accounting employees, proposals for their encouragement or the imposition of penalties on them.

4.7. Involve specialists from departments of the enterprise in solving the tasks assigned to it (if this is provided for by the regulations on departments, if not, with the permission of the manager).

4.8. Require the director of the enterprise to provide assistance in the performance of his official duties and rights.

Possible options for the role of the chief accountant

The Law “On Accounting” dated December 6, 2011 No. 402-FZ assigns organizations the obligation to maintain accounting. It is allowed that accounting can be carried out (Article 7):

- the leader himself;

- attracted individual or legal entity;

- full-time chief accountant or other official.

Since accounting requires special knowledge, the specifics of the activities of a particular legal entity and prompt response to events occurring in it, most often these functions are assigned to the organization’s own employee, who is hired as a chief accountant. Mandatory requirements for it are set out in paragraph 4 of Art. 7 of Law No. 402-FZ:

- presence of higher or secondary specialized education;

- work experience in the field of accounting for at least 3 years out of the last 5 if you have a specialized education, and if not, at least 5 years out of the last 7;

- no outstanding convictions for economic crimes.

However, these requirements are mandatory only for chief accountants:

- in open joint-stock companies (except for credit institutions);

- insurance organizations and non-state pension funds;

- joint stock investment funds;

- management companies of mutual investment funds;

- other economic entities whose securities are admitted to circulation at organized trading (except for credit organizations);

- management bodies of state extra-budgetary funds.

For chief accountants of other economic entities, the above requirements are not mandatory.

You can find out more about what requirements for the qualifications of the chief accountant the new professional standard “Accountant” requires in ConsultantPlus. Get trial access to the system for free and go to the document.

Depending on the size of the organization, the chief accountant can work:

- As the only accountant. In this case, all accounting responsibilities fall on him. In small organizations, he usually also performs the functions of the personnel department.

- As part of a small accounting department. The chief accountant not only organizes and controls the work of the accounting department, but also performs part of the accounting work himself, just like ordinary accountants.

- As part of a large accounting service, one of the responsibilities of which is a significant amount of additional reporting and explanations presented both to the legal entity’s own divisions and to external users (owners, management structures, banks, counterparties, Federal Tax Service). In this case, control over the correct execution of accounting operations by accounting employees, preparation of reports and responses to requests becomes dominant for the chief accountant.

- As part of the accounting department, some of the functions of which are transferred to other divisions. In this case, the determining tasks for the chief accountant will be organizing the timely receipt of information, monitoring its quality and linking data.

Thus, the functions of the chief accountant largely depend on many specific conditions of the organization of which he is an employee, and the scope of his responsibilities may vary. In this regard, they need to be clearly defined in the job description of the chief accountant.

PROFESSIONAL ACCOUNTANT

1. Rights and responsibilities of the chief accountant

The rights and responsibilities of the chief accountant are established by the Law of the Republic of Belarus “On Accounting and Reporting”, other regulatory legal acts and local regulations of the organization.

According to the Law of the Republic of Belarus “On Accounting and Reporting”, the management of accounting in an organization is within the competence of the chief accountant. His responsibilities include:

setting up and maintaining accounting records in the organization;

formation of the organization's accounting policy;

preparation and timely submission of organization reports;

other responsibilities in the field of accounting and reporting.

The chief accountant reports directly to the head of the organization. When setting up and maintaining accounting records, the chief accountant must follow the norms of current legislation, follow the instructions and orders of the head of the organization, as well as the person authorized to do so by written instructions from the head. Such a written instruction may be the job description of the chief accountant.

Current legislation does not require the chief accountant to sign tax returns, state statistical and other reports - they are certified by the signatures of the head and the person who prepared the reports. Nevertheless, the head of the organization has the right to appoint the chief accountant responsible for reporting. The right to sign (endorsement) by the chief accountant of primary documents, powers of attorney, business contracts is also established by the manager and is enshrined in the job description.

The position of chief accountant was not previously included in the Sample List of Positions and Works replaced or performed by employees with whom the employer may enter into written agreements on full individual financial responsibility. Currently Art. 405 of the Labor Code of the Republic of Belarus allows the employer to independently determine the officials with whom agreements on full financial responsibility will be concluded or the conditions on whose full financial responsibility will be included in their contract.

The legislation of the Republic of Belarus establishes the fundamental right of the chief accountant - instructions and orders within his competence are mandatory for execution by all structural divisions and employees of the organization. Thus, the head of the organization is obliged to agree with the chief accountant on the list of persons who have the right to sign primary accounting documents.

Payment of bills from the organization's current account must be made subject to an appropriate written agreement. Agreements on behalf of the organization are signed by its head or a person authorized by the head. An agreement can be concluded by sending an offer (proposal to conclude a contract) by one of the parties and its acceptance (acceptance of the offer) by the other party. The exchange of documents is possible through postal, telegraphic, teletype, electronic or other communications that make it possible to reliably establish that the document comes from a party to the contract. Documents can be any written evidence confirming the fact of a transaction and allowing one to determine its conditions, for example, invoices, certificates of work performed, delivery notes and delivery notes.

The contract will be considered concluded if, in response to a written proposal to conclude a contract (offer), the other party, within the prescribed period, takes actions to fulfill the conditions specified in the proposal. It must be borne in mind that the contract is considered concluded if all essential conditions are specified in it.

In his free time from his main job, the chief accountant has the right to work part-time. A part-time work permit is not required. In addition, the chief accountant can perform one-time (casual) work (for example, restoring accounting records lost due to the departure of the previous chief accountant) under a contract agreement in the organization in which he works.

Taking into account the most important role of the chief accountant in ensuring the financial stability of the organization, the Law of the Republic of Belarus “On Accounting and Reporting” establishes serious requirements for his educational and professional level: the chief accountant must have a higher or secondary specialized education, giving the right to work as an accountant ( for example, economist, auditor, auditor, etc.), and work experience as an accountant for at least three years. A person with at least five years of experience as an accountant and an additional certificate of a professional accountant is appointed to the position of chief accountant of a socially significant organization.

In government organizations, restrictions have been established on the work of relatives of the head and cashier of the organization (parents, spouses, sons, daughters, brothers, sisters) in the position of chief accountant. In non-governmental organizations, such a prohibition may be provided for by a decision of the owner.

The specific rights and responsibilities of the chief accountant are determined by his job description.

2. Job description of the chief accountant

The form of the instruction is not fixed by law and is drawn up in any form, for example:

JOB DESCRIPTION for chief accountant

- I. General provisions

1. In his activities, the chief accountant is guided by this job description and the Regulations on the accounting department of the organization.

2. The job description is drawn up in accordance with the Law of the Republic of Belarus “On Accounting and Reporting” and the Regulations on the accounting department of the organization.

3. The chief accountant manages accounting in the organization.

4. The chief accountant is appointed to the position and dismissed from his position by the director.

5. The chief accountant heads the accounting department as an independent structural unit.

6. The chief accountant reports directly to the director and deputy director for economic issues.

7. Written instructions to the chief accountant for payment of the organization’s bills are given by the director (deputy director for economic issues) on invoices received from suppliers of goods and services, or are indicated directly in the acceptance certificate of work performed.

8. The acceptance and delivery of cases upon appointment and dismissal from a position are formalized by an act after checking the state of accounting and reporting in the presence of members of the commission approved by order of the organization.

9. During the absence of the chief accountant (business trip, vacation, illness, etc.), the rights and responsibilities of the chief accountant are transferred to his deputy.

10. The chief accountant must know:

accounting legislation;

laws of the Republic of Belarus; decrees, decrees of the President of the Republic of Belarus; resolutions and decisions of the Government of the Republic of Belarus on issues of financial and economic activity; resolutions, orders, orders, other methodological and regulatory materials of higher organizations, financial and control and audit bodies on issues of accounting and reporting, financial activities of enterprises; local regulations of the organization;

structure of the organization, strategy and prospects for its development;

the procedure for registration of business transactions and the organization of document flow in accounting areas, the procedure for acceptance, posting, storage and expenditure of funds and other property;

rules for settlements with debtors and creditors;

the procedure for writing off shortages, receivables and other losses from accounting accounts;

tax conditions for legal entities and individuals;

forms and procedure for financial settlements;

methods of economic analysis of the economic and financial activities of an organization;

rules for conducting an inventory of funds and other property of the organization, its obligations;

procedure and deadlines for preparing financial statements;

rules for storing and destroying accounting documentation;

rules for conducting documentary checks and audits;

modern computer technology and the possibilities of their use for performing accounting and computing work and analyzing the production and economic activities of an organization;

advanced domestic and foreign experience on improving accounting, international financial reporting standards;

civil law, criminal law, financial, tax and economic legislation;

economics, organization of production, labor and management;

basics of production technology;

legislation on labor and labor protection, safety regulations, industrial sanitation and fire protection.

II. Responsibilities of the chief accountant

11. The main tasks assigned to the chief accountant are:

setting up and maintaining accounting records;

formation of accounting policies;

preparation and timely submission of complete and reliable accounting, statistical, tax and other reporting.

For this purpose, the chief accountant is obliged to ensure:

selection of methods and methods of accounting and tax accounting;

building a system for reflecting relationships with separate structural divisions in accounting;

development of a working chart of accounts for the organization;

drawing up a document flow schedule;

development and approval of a working album of forms of primary accounting documentation and accounting registers;

methodological guidance in the process of creating software products in the organization to automate accounting operations;

full accounting of incoming funds, inventory and fixed assets, timely reflection in accounting of transactions related to their movement;

reliable accounting of production and distribution costs, preparation of reporting calculations of the cost of products, works, services;

accurate accounting of the results of financial and economic activities in accordance with established rules;

correct calculation and timely transfer of payments to the state budget and extra-budgetary funds, to the social protection fund;

participation in the work of legal services on issues of registration of materials on shortages and thefts of funds and inventory items (in the absence of legal services, the direct implementation of these functions);

organizing audits of the state of accounting and ensuring the safety of material assets in the accounting departments of structural divisions allocated to a separate balance sheet;

carrying out an analysis of the financial condition of the organization and presenting the results of the analysis to the manager and relevant officials or services;

ensuring the safety of accounting documents during the document flow and storage in the accounting archive before their transfer to the organization’s archive.

12. The chief accountant, together with the heads of the relevant structural divisions, is obliged to control:

compliance with established rules for processing the acceptance and release of inventory items;

correct expenditure of the wage fund, establishment of official salaries, compliance with staffing, financial and cash discipline;

compliance with established rules for conducting an inventory of material assets, fixed assets, cash, settlements and other obligations;

collection of accounts receivable and repayment of accounts payable within the established time limits, compliance with payment discipline;

the legality of writing off shortages, receivables and other losses from balance sheets.

13. The chief accountant is obliged to actively participate in the preparation of measures to prevent the formation of shortages and illegal expenditure of funds and inventory items, violations of financial, tax and economic legislation.

In case of detection of illegal actions of officials (attributions, abuses, misuse of funds and other violations), the chief accountant reports this to the director for taking action.

14. The chief accountant (authorized person) is obliged to sign all documents that serve as the basis for the acceptance and issuance of funds and inventory items.

Granting the right to sign documents to authorized persons is formalized by order upon written submission of the chief accountant.

The above documents without the signature of the chief accountant (authorized person) are considered invalid and should not be accepted for execution by financially responsible persons and accounting employees.

15. The chief accountant is prohibited from accepting for execution and registration documents on transactions that contradict the law and are not drawn up in accordance with established requirements.

16. Disagreements between the chief accountant and the heads of structural divisions are resolved by the director of the organization.

- III. Rights of the chief accountant

17. The chief accountant distributes official responsibilities for employees subordinate to him, draws up and submits job descriptions for accounting employees to the director for approval.

18. The instructions and orders of the chief accountant regarding the procedure for processing transactions and submitting the necessary documents and information to the accounting department are mandatory for all departments and services. For untimely, poor-quality execution and preparation of documents, delay in their transfer for reflection in accounting and reporting, unreliability of the data contained in them, as well as for the preparation of documents reflecting illegal transactions, upon the recommendation of the chief accountant, the director shall hold liable the persons who compiled and signed these documentation.

19. The appointment, dismissal and relocation of financially responsible persons (cashiers, warehouse managers, etc.) is carried out in agreement with the chief accountant.

20. Lists of officials who are responsible for drawing up primary documents and who are given the right to sign them are agreed upon with the chief accountant.

21. Contracts and agreements concluded by the organization, orders and regulations on the establishment of official salaries, salary allowances and bonuses for employees are endorsed by the chief accountant.

- IV. Responsibility of the chief accountant

22. The chief accountant is responsible in the following cases:

improper accounting, which resulted in neglect in accounting and distortion of financial statements;

acceptance for execution and execution of documents on transactions that contradict the established procedure for acceptance, posting, storage and expenditure of funds and other property of the organization;

untimely and incorrect reconciliation of transactions on current and other bank accounts, settlements with debtors and creditors;

violation of the procedure for writing off shortages, accounts receivable and other losses from balance sheets, incorrect inventory of all balance sheet items and recording of its results;

untimely conduct of inspections and documentary audits in production (structural) units of associations, as well as in production and enterprises allocated to a separate balance sheet;

preparation of unreliable financial statements due to the fault of the accounting department, incorrect calculation of taxes, fees and other obligatory payments provided for by the legislation of the Republic of Belarus;

violation of deadlines for submitting tax calculations, quarterly and annual accounting reports and balance sheets, statistical reporting to the relevant authorities;

other violations of regulations and instructions on the organization of accounting.

The job description of the chief accountant is drawn up in two copies: one copy is kept in the accounting files, the second is given to the chief accountant.

For failure to fulfill the duties determined by the job description, the chief accountant, as well as any other employee, may be subject to disciplinary sanctions:

comment;

rebuke;

dismissal in accordance with the Labor Code of the Republic of Belarus.

In addition, the chief accountant may be held administratively, financially and criminally liable.

Administrative liability arises only if there is his guilt and only if the head of the organization creates the necessary conditions for the performance of official duties set out in the job description.

When considering administrative cases, they are guided by the Code of Administrative Offenses and the Procedural and Executive Code of the Republic of Belarus. For committing offenses in the field of entrepreneurial activity, special deadlines for imposing disciplinary sanctions are established - no later than three years from the date of commission and six months from the date of discovery.

The fine is paid by the chief accountant no later than one month from the date of entry into force of the decision to impose the fine, and in the case of an appeal (protest) of the decision - no later than one month from the date of notification that the complaint (protest) was left unsatisfied. The fine can be paid independently or transferred by the organization with its further deduction from wages. The organization does not have the right to pay fines for officials, incl. for the chief accountant.

The chief accountant may be released from liability if the tax authority recognizes the administrative offense committed as insignificant or in the case of voluntary compensation or elimination of the harm caused.

In case of failure to pay the fine within the prescribed period, the decision to impose a fine is sent to the bailiff of the court in whose area of activity the violator lives (works) to forcibly deduct the amount of the fine from the violator’s salary or other earnings, pension or scholarship in accordance with the rules established Civil Procedure Code of the Republic of Belarus.

If an administrative offense is committed by a person who has terminated his employment relationship with the organization, this person may be summoned (or brought to law enforcement by a police officer) to the state body that revealed the offense to draw up a protocol.

An administrative penalty is imposed on the chief accountant only if he, as a rule, is in an employment relationship with the organization, i.e. is an official.

Here is a list of the main violations for which the Code of the Republic of Belarus on Administrative Offenses provides for fines:

violation of the established accounting procedure entails a warning or a fine in the amount of 4 to 20 basic units;

destruction of accounting documents necessary for the calculation and payment of taxes before the expiration of the established storage periods or their concealment entails a fine in the amount of 10 to 100 basic units;

Failure to ensure the safety of accounting documents necessary for the calculation and payment of taxes, resulting in their loss, entails a fine in the amount of 4 to 35 basic units.

The chief accountant is held to limited or full financial liability. He is subject to limited liability if a written agreement on full individual financial liability was not concluded with him or the condition on his full financial liability was not included in the contract.

The amount of damage caused is established at the level of what was actually caused, i.e. excluding lost income. The obligation to prove the fact of causing harm, incl. The fault of the chief accountant lies with the employer (with some exceptions in accordance with the law). For the employer to apply to the court for the recovery of material damage caused to him by the actions of the chief accountant, a period of one year has been established from the date of discovery of the damage. The day of discovery of damage identified as a result of an inventory of material assets during an audit or verification of the financial and economic activities of an organization is the day the corresponding act or conclusion is signed. The court has the right to reduce the amount of damage to be compensated, taking into account the degree of guilt, specific circumstances and financial situation of the offender.

Persons guilty of disclosing trade secrets may be held administratively or financially liable. The legal mechanism for the protection of trade secrets is provided by the Law of the Republic of Belarus No. 16-Z “On Trade Secrets”, which came into force on June 11, 2013.

A qualifying feature of a trade secret is the presence (absence) of a trade secret regime established in relation to information, which is understood as a set of various measures taken by the owner of a trade secret to ensure the confidentiality of the relevant information. The owner of a trade secret is entrusted with determining the composition of information constituting a trade secret and implementing a set of measures aimed at protecting it.

Classifying information as a trade secret has legal significance only if the list of such information is recorded and the obligation not to disclose a trade secret without appropriate permission is reflected in the employment agreement (contract). The volume and boundaries of information constituting a trade secret of an organization are established by order (instruction) of the manager, taking into account current legislation.

By the nature of their activities, chief accountants have access to a large amount of information, some of which may be classified as a trade secret: information about production activities and financial condition, investment projects and marketing research, procurement and sales, sales regions and product buyers, etc. For prevention violations in the field of security and protection of information from disclosure, the chief accountant when hiring must be familiarized with the organization's current regulations on trade secrets, against receipt.

In the event of economic insolvency (bankruptcy) of a legal entity, the chief accountant, as a person who has the right to give instructions or the ability to determine the actions of the legal entity, is assigned subsidiary liability for the obligations of the legal entity.

Persons who have committed violations in the form of official forgery or official negligence and formed a criminal offense in accordance with the Criminal Code of the Republic of Belarus are brought to criminal liability. Official forgery is expressed: by entering deliberately false information and entries into official documents; falsification of official documents; in the preparation and issuance of deliberately false documents, committed out of selfish or other personal interest, for example, submitting deliberately false information to the bank about the financial condition of the organization in order to obtain a loan. If official forgery is committed in the absence of selfish or other personal interest, it may entail disciplinary or administrative liability.

Official negligence, entailing criminal liability, is the failure or improper performance by the chief accountant (deputy chief accountant) of his official duties as provided for in the job description, due to dishonest or negligent attitude towards service, resulting in damage on a large or especially large scale.

In addition, the chief accountant may be brought to criminal liability for evasion of taxes and fees. 3. The procedure for the appointment and dismissal of the chief accountant

The chief accountant is appointed and dismissed from his position by the head of the organization in accordance with the constituent documents. When hiring a chief accountant, an employment agreement (contract) is concluded and a job description is drawn up. Hiring a chief accountant under a contract is not allowed. For chief accountants of government organizations, there is an additional restriction on holding a position: joint work with close relatives is prohibited if it involves the direct subordination or control of one of them to the other.

In accordance with the staffing table, the salary of the chief accountant is established. A hired employee may be assigned an irregular working day with compensation in the form of additional leave of up to seven calendar days.

Currently, the legislation of the Republic of Belarus does not provide for the obligation of an organization to inform the tax authority about a change of chief accountant. However, the tax authority has the right to require the provision of such information (subclause 1.1 of Article 81 of the Tax Code of the Republic of Belarus). In this case, the organization is obliged to provide the tax authority with the relevant information.

The change of chief accountant of a business entity must be notified to the servicing banks no later than three working days.

Within one month from the date of change of chief accountant, a new card with sample signatures and seal imprints is issued. For the period until a new card is issued, the organization has the right to issue a temporary card, which contains a sample signature of the person temporarily entitled to sign payment documents. The authenticity of the signature is certified by the head of the legal entity. In some cases, an organization has the right to issue a temporary (for a period of up to two months) card with sample signatures, which is valid along with the main one.

When the chief accountant is replaced, affairs are transferred to the successor according to an act, the form and content of which are established by the organization independently. A commission approved by order of the organization takes part in drawing up the act after receiving a resignation letter from the chief accountant (or upon expiration of the contract term). The commission includes at least three employees competent in accounting matters.

We recommend the following form of the acceptance certificate:

| LLC "Pramen" | I APPROVED | |||

| (name of company) | Director | Petrov | I. M. Petrov | |

| (signature) | (initials, surname) | |||

| "5" August 20 15 | ||||

ACT OF ACCEPTANCE OF CASES

Minsk "5" August 20 15

This act was drawn up by the former chief accountant of Pramen LLC I. A. Ivanov and the newly appointed chief accountant E. V. Svirid stating that, on the basis of order No. 46 of August 5, 2015, they carried out the delivery and acceptance of cases as of 1 August 2015

The delivery and acceptance of cases was carried out in the presence of members of the commission for the acceptance and delivery of cases: deputy chief accountant K. A. Sidorova, accountants E. S. Zhdanova and Yu. V. Snegur.

As a result of the delivery and acceptance of cases, it was established that:

1. Accounting was carried out in accordance with the legislation and accounting policies of the organization in the 1C: Accounting program version 7.7. Tax returns for all reporting periods were compiled and submitted to the tax authority at the place of registration.

2. Presented current documentation and accounting archive for 2010–2015. in the amount of 250 (two hundred and fifty) cases according to the inventory.

3. All summary and analytical information was transmitted on electronic media, which is identical to the data presented in tax and accounting reports on paper.

4. Regulatory and reference literature and equipment were handed over according to the inventory.

Application:

1. Inventory of files in the accounting archive on page 10.

2. Inventory of reference literature and equipment on page 1.

| Passed the case | Accepted the case | ||||

| Ivanov | I. A. Ivanov | Svirid | E. V. Svirid | ||

| (signature) | (initials, surname) | (signature) | (initials, surname) | ||

Members of the commission were present during the delivery and acceptance of cases:

| Chief accountant's assistant | Sidorova | K. A. Sidorova |

| (signature) | (initials, surname) | |

| Accountant | Zhdanova | E. S. Zhdanova |

| (signature) | (initials, surname) | |

| Accountant | Snegur | Yu. V. Snegur |

| (signature) | (initials, surname) |

The act of acceptance of cases may also include other information relating to issues that were within the competence of the chief accountant of the organization, in particular, work books of employees, contracts, employment agreements, a corner stamp, a round seal of the organization (an imprint is affixed on the act transferable seal, stamps), etc. The act must be approved by the head of the organization.

If, during the acceptance and transfer, missing accounting documents or shortcomings related to accounting and tax calculations are revealed, it is necessary to take measures to restore the documents and eliminate the shortcomings. Therefore, it is recommended that the acceptance certificate of affairs be drawn up not in the last days of work of the resigning chief accountant, but as early as possible.

If there is no new chief accountant at the time of drawing up the act, the persons responsible for receiving cases may be:

Head of the organization;

any accounting employee who will temporarily act as chief accountant.

If, at the time of transfer of cases, facts are established that have resulted or may result in damage to the organization, the employer has the right to apply disciplinary and financial liability measures to the chief accountant. According to paragraph 1 of Art. 47 of the Labor Code of the Republic of Belarus, if a gross violation of labor duties is established on the part of the chief accountant, he may be dismissed for a single violation of labor duties.

The dismissal of the chief accountant is carried out in the same way as the dismissal of other employees of the organization. The Labor Code of the Republic of Belarus provides an additional basis for the dismissal of the chief accountant from his position - a change in the owner of the organization's property.

If the chief accountant is a financially responsible person, then an inventory of material assets under his control is carried out. If, at the conclusion of the contract, full financial liability was provided for damage caused to the employer through the fault of the employee by excessive monetary payments (overpaid wages, overpayment of travel expenses, etc.), an inventory of settlement transactions is made.

Main tasks of the chief accountant

Regardless of the size of the organization of which he is an employee, the chief accountant belongs to the category of managers. He must have certain knowledge and perform a number of functions required for the position. These requirements for him are given in the Qualification Directory of Positions of Managers, Specialists and Other Employees, approved by Decree of the Ministry of Labor of the Russian Federation dated August 21, 1998 No. 37, and the professional standard “Accountant” approved by Order of the Ministry of Labor of the Russian Federation dated December 22, 2014 No. 1061n.

The professional standard is mandatory only for accountants of state and municipal institutions and organizations with a state share of more than 50% (Clause 1, Article 4 of the Law “On Amendments to the Labor Code...” dated 05/02/2015 No. 122-FZ) from 07/01/2016. Other organizations may be guided by its requirements, but have the right not to use it.

The knowledge portion of these documents lists:

- legislation on accounting, including issues of organizing accounting, rules for its maintenance, reporting;

- tax law;

- civil, financial and economic legislation;

- labor law;

- codes of ethics for professional accountants and corporate governance;

- statistical and management accounting;

- specifics, technology, structure, strategy and prospects for the organization;

- audit rules;

- methods of financial analysis of economic activity;

- accounting and reference legal databases.

The main functions of the chief accountant are provided by the Qualification Directory:

- organizing optimal accounting, including document flow, accounting work and development of accounting policies;

Read about what you need to pay attention to when developing an accounting policy in the article “ Drawing up a statement of accounting policies in an organization .

- compliance of transactions recorded by accounting with the requirements of current legislation;

- compiling all types of required reporting and meeting deadlines for its submission;

- correct calculation of taxes, insurance premiums and other charges;

- timely transfer of all necessary payments;

- participation in the formation of tax policy and financial analysis of activities;

- methodological assistance to other employees of the organization in matters of accounting and financial analysis.

Note that the main function of the chief accountant in the professional standard is the preparation of reports (Article 3.2 of the Accountant standard), however, the labor actions related to this position include all those listed for the chief accountant in the Qualification Directory .

The serious role of the chief accountant in an enterprise also implies increased responsibility. Which one you can find out in ConsultantPlus by getting free trial access to the system.

III. Job responsibilities

To perform the functions assigned to him, the chief accountant of the enterprise is obliged to:

3.1. Organize accounting of economic and financial activities and control over the economical use of material, labor and financial resources, and the safety of the enterprise’s property.

3.2. Formulate an accounting policy in accordance with accounting legislation, based on the structure and characteristics of the enterprise’s activities, the need to ensure its financial stability.

3.3. Organize accounting of property, liabilities and business transactions, incoming fixed assets, inventory and cash, execution of cost estimates, performance of work (services), results of financial and economic activities of the enterprise, as well as financial, settlement and credit transactions, timely reflection on accounting accounts of transactions related to their movement.

3.4. Monitor compliance with the procedure for preparing primary and accounting documents, settlements and payment obligations, spending the wage fund, conducting inventories of fixed assets, inventory and cash, checking the organization of accounting and reporting, as well as documentary audits in the divisions of the enterprise (branches ).

3.5. Take measures to prevent shortages, illegal spending of funds and inventory, violations of financial and economic legislation.

3.6. Ensure the legality, timeliness and correctness of the execution of documents, work (services) performed, payroll calculations, correct calculation and transfer of taxes and fees to the federal, regional and local budgets, insurance contributions to state extra-budgetary social funds, payments to banking institutions, funds for financing capital investments, repaying bank loan debts on time, as well as deductions for material incentives for enterprise employees.

3.7. Participate in the preparation of materials on shortages and thefts of funds and inventory items, control the transfer, if necessary, of these materials to investigative and judicial authorities.

3.8. Lead the work on the preparation and adoption of a working chart of accounts, forms of primary accounting documents used for registration of business transactions for which standard forms are not provided, development of forms of internal accounting documents, as well as ensuring the procedure for conducting inventories, monitoring the conduct of business transactions, compliance with technology processing of accounting information and document flow procedures.

3.9. Participate in conducting an economic analysis of the economic and financial activities of an enterprise based on accounting and reporting data in order to identify on-farm reserves, eliminate losses and unproductive costs.

3.10. Work to ensure strict compliance with staffing, financial and cash discipline, estimates of administrative, economic and other expenses, the legality of writing off shortages, accounts receivable and other losses from accounting accounts, the safety of accounting documents, their execution and delivery in the prescribed manner to the archive.

3.11. Take measures to accumulate financial resources to ensure the sustainability of the enterprise.

3.12. Ensure the rational organization of accounting and reporting at the enterprise on the basis of maximum centralization of accounting and computing work and the use of modern technical means and information technologies, progressive forms and methods of accounting and control, the formation and timely submission of complete and reliable accounting information about the activities of the enterprise, its property status , income and expenses, as well as the development and implementation of measures aimed at strengthening financial discipline.

3.13. Interact with banks on the placement of available funds on bank deposits (certificates) and the acquisition of highly liquid government securities, control over accounting transactions with deposit and loan agreements, securities.

3.14. Participate in the development and implementation of rational planning and accounting documentation, progressive forms and methods of accounting based on the use of modern computer technology.

3.15. Ensure the preparation of balance sheets and operational summary reports on income and expenses of funds, the use of the budget, other accounting and statistical reporting, and their submission in the prescribed manner to the relevant authorities.

3.16. Provide methodological assistance to employees of enterprise departments on accounting, control, and reporting issues.

3.17. Manage employees of the company's accounting department.

Problems of Ch. accountant of a small company (LLC, JSC)

Features of the work of a chief accountant in a small organization include:

- absolute interchangeability of accounting staff, the need to be able to do everything yourself;

- the possibility of reducing the volume of accounting work and reporting through the use of special regimes or the use of concessions provided by the SMP;

- little demand for accounting data for financial analysis purposes;

- no need for a large number of additional forms of internal reporting;

- lack of demand for audits;

- lack of close attention from inspection authorities, a relatively small number of requests for clarification.

Functions of the chief accountant of a large enterprise

The chief accountant of a large enterprise has practically no opportunity to do actual accounting. The priorities in his work are:

- organization of an accounting scheme that covers in its full diversity all aspects of the enterprise’s activities;

- organization of complex document flow;

- development of an accounting policy that is significantly more detailed and voluminous than in a small legal entity;

- distribution of accounting functions among accountants, organization of their precise work, interaction and interchangeability;

- control and linkage of data used for the preparation of all types of reporting, including internal and statistical;

- generating reports as fully as possible using all forms of existing reports and drawing up the necessary explanations;

- calculation of a larger number of taxes, some of which are usually irrelevant for a small organization;

- mandatory participation in financial analysis and calculation of forecast data;

Read about methods for analyzing a financial results statement in the article “Methods for analyzing a profit and loss statement .

- working with inspectors during audits;

- a large amount of work in order to respond to various types of requests relating to accounting and taxation issues.

II. Functions

The chief accountant is assigned the following functions:

2.1. Management of accounting and reporting at the enterprise.

2.2. Formation of accounting policies with the development of measures for its implementation.

2.3. Providing methodological assistance to employees of enterprise departments on accounting, control and reporting issues.

2.4. Ensuring the preparation of salary calculations, accruals and transfers of taxes and fees to budgets of various levels, payments to banking institutions.

2.5. Identification of on-farm reserves, implementation of measures to eliminate losses and unproductive costs.

2.6. Introduction of modern technical means and information technologies.

2.7. Monitoring the timely and correct execution of accounting documentation.

2.8. Ensuring healthy and safe working conditions for subordinate performers, monitoring their compliance with the requirements of legislative and regulatory legal acts on labor protection.

Contents of the job description

Despite the significant difference between the texts of job descriptions that can be created for the chief accountant in a particular organization, its content consists of the same sections.

They are usually formed in the following sequence:

- requirements for qualifications (education, experience, knowledge);

- determining the place in the structure of the organization, the procedure for interaction with other employees;

- job responsibilities of the chief accountant;

- rights;

- responsibility.

Rights of the chief accountant

The chief accountant, who has fairly extensive responsibilities, has certain rights in addition to the generally accepted rights of citizens under the Constitution of the Russian Federation. The most important of them (summary):

- The right to put his signature on documents of an economic and financial nature that are related to issues in the scope of his official powers.

- Rights of cooperation with other institutions and enterprises. The purpose of such a relationship is to promptly resolve various types of issues within their competence.

- The right to make requests and obtain documentation regarding issues within his competence.

- The right to give instructions to subordinate services and employees, as well as to monitor their implementation.

What types of crimes exist in criminal law are detailed in this article.

What forms of guilt exist in the theory of criminal law are described in detail in this article.

What the subjective side of a crime in criminal law is is detailed in this article here: https://ruleconsult.ru/ugolovnoe/prestupleniya/obektivnaya-storona-v-ugolovnom-prave.html

You may also be interested in learning about the object of a crime in Russian criminal law.

Job Description Form

There is no strictly established form of job description, therefore it is developed and executed in the manner that applies to the preparation of such documents in the organization itself.

An indispensable condition for the entry into force of a job description is its approval by the head of the legal entity. It becomes mandatory for the employee from the moment he familiarizes himself with it and signs it.

You can download a sample job description for a chief accountant from the link below:

Results

A job description is a fairly important document that defines the specific functions of an employee. Since the chief accountant is one of the serious figures in any organization, his job description should be given special attention.

Sources:

- Resolution of the Ministry of Labor of the Russian Federation dated August 21, 1998 No. 37

- Law “On Accounting” dated December 6, 2011 N 402-FZ

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

What can you be held criminally liable for?

Chief accountant is a profession for which financial responsibility is provided. Full liability of the employee allows the employer to claim from him the full amount of direct damage caused by him.

The video shows the criminal liability of the chief accountant:

Liability Agreement

When drawing up this agreement, it is necessary that it contains the following points:

- General provisions . This should include generally accepted clauses of the agreement. As a rule, this is the date, place of conclusion of the agreement, information about the parties to the agreement. The document also contains information about what documents were accepted by the chief accountant and what functions were assigned to him. When an accountant’s work involves goods and direct material assets, the contract must contain the corresponding functions.

- Responsibilities of an accountant. This was stated above.

- Employer's responsibilities . Optimal conditions must be created for the chief accountant to fully carry out his activities. The employer undertakes to familiarize his employee with information on how to store documents, how to keep records, sale and transfer of property. After this, the accountant is required to sign as proof that he is familiar with the relevant information.

- A list of cases according to which the chief accountant is responsible for the organization’s property.

- Plan for determining the amount of material damage caused and its return . The accountant has the opportunity to voluntarily compensate for material damage. The amount of compensation is determined taking into account actual losses according to accounting data. If there is a deliberate theft of goods or their damage, then their value is determined in comparable prices for a similar type of property. The chief accountant may not compensate for the amount of damage caused if there is no evidence of his guilt in theft.

- Mandatory information about the parties to the agreement and their addresses.