Make perfect incoming invoices

To put it very simply, the VAT amount is the difference between the sales book and the purchase book. That is, from the amount of VAT on sales you need to subtract the amount of VAT on purchases. Your incoming invoices reduce tax, so they must be perfect: serial number and date of preparation, details of the seller and buyer, quantity and volume of goods or services, etc. All requirements are listed in Article 169 of the Tax Code of the Russian Federation. The Federal Tax Service will carefully study them and compare them with outgoing invoices from suppliers.

People are not involved in the learning process. This process is fully automated. The ASK VAT 3 system works. So you should not think that errors or inconsistencies will not be noticed due to the human factor.

How to fill out a zero VAT return

How to fill out a zero VAT return? Which sheets should be submitted in the zero VAT return?

A zero VAT return is drawn up on the form of this report valid for the corresponding period. Since there are no digital data to fill it out, only 2 mandatory sections are drawn up in it:

- title page;

- section 1.

You will find the details of how to fill them out below.

For individual entrepreneurs, we recommend our article “Zero VAT return for individual entrepreneurs on OSNO.”

Calculate the VAT amount in advance

Some of our accounting clients ask us to calculate the VAT amount in advance. For example, the report and payment must be made on October 26, and on September 25 our specialists already tell you the approximate amount of the tax. You can do this too.

Look at your sales and forecast your sales for the coming two weeks. After that, find all incoming invoices to reduce the VAT amount. and you’ll simply be mentally prepared for the fact that in October a certain amount will be used to pay taxes.

In what cases is a zero VAT return submitted?

Do I need to submit a zero VAT return?

Yes need! Moreover, like any VAT return, the zero return must also be submitted within the deadline established for this report. A zero VAT return is submitted in cases where there are no digital indicators to fill out its sections 2–12. This may occur at the beginning or at the end of the taxpayer’s work, during seasonal activities, or temporary breaks in work.

Note! The VAT declaration was updated by order of the Federal Tax Service dated March 26, 2021 No. ED-7-3/228 [email protected] The form is used from the reporting campaign for the 3rd quarter of 2022.

You will find a line-by-line algorithm with examples of filling out all twelve sections of the report in ConsultantPlus. Trial access to the system can be obtained for free.

The declaration will not be zero if there is data to fill out at least one of these sections.

It must be submitted by all those persons who have an obligation to file a VAT return. This obligation applies to VAT taxpayers, tax agents, as well as non-payers of taxes or those exempt from paying VAT but issuing invoices. Tax payers are considered to be all legal entities and individuals - entrepreneurs who have chosen the general taxation system.

For information about who becomes a tax agent for VAT, read the article “Who is recognized as a tax agent for VAT (responsibilities, nuances)” .

The VAT return must be submitted electronically. This also applies to a zero VAT return. As an exception, permission to submit this tax report on paper is granted only to tax defaulters (or exempt from payment under Articles 145, 145.1 of the Tax Code of the Russian Federation) who acted as tax agents in the reporting period (letter of the Federal Tax Service dated February 19, 2016 No. ED-3- 15/679, dated January 30, 2015 No. OA-4-17/ [email protected] ).

Don't buy VAT

Just before submitting the report and paying the tax, you will be asked to buy VAT. Offers appear in advertising and Telegram. We do not recommend doing this. This is illegal and directly contrary to the tax code. You may get problems from the tax office or even become a debtor. All the details are in our material on this topic.

There is still time until October 26th. Do not put off sending the report and paying the tax itself until the last day. Check that your email signature is valid and prepare to spend some money on taxes this month.

Simplified VAT return

If during the reporting quarter there was no activity at all, and there was no movement in the current accounts and in the cash register of the enterprise, then the taxpayer can submit a single simplified declaration, which provides for the submission of information about the absence of grounds for payment of several taxes at once. A simplified VAT return (single) is submitted to the Federal Tax Service by the 20th day of the month following the reporting month (clause 2 of Article 80 of the Tax Code of the Russian Federation).

The form of such a simplified declaration was approved by Order of the Ministry of Finance dated July 10, 2007 No. 62n. The same order describes the procedure for filling it out and submitting it to the tax authority.

ConsultantPlus experts provided a step-by-step algorithm for filling out a single simplified declaration. If you do not have access to the K+ system, get a trial demo access for free.

Features of filling out the title page

The title page contains information about the taxpayer, the Federal Tax Service and the tax period for which the report is being prepared. It states:

- Taxpayer codes and name.

When filling out the title page, the taxpayer must indicate his INN and KPP codes, the exact name (for legal entities - as stated in the charter, and for individual entrepreneurs - full full name, as in the passport). You should fill in the number of your Federal Tax Service (it is easy to find out by looking at your registration documents, or you can use the search on the Federal Tax Service website).

In the field “at location (accounting)” the codes are indicated that are given in Appendix 3 to the Procedure for filling out the declaration (hereinafter referred to as the Procedure) (Federal Tax Service order No. ММВ-7-3/ dated October 29, 2014).

- Adjustment symbol.

When submitting the first declaration for the reporting period, you should enter code 0 in the “Adjustment number” field, and when submitting clarifying reports, the following serial numbers should be entered.

- Taxable period.

When specifying the tax period, the appropriate code is entered (their list is contained in Appendix 3 to the Procedure). So, when submitting a reporting declaration for the 1st quarter, code 21 is entered. And if, for example, a declaration for the 1st quarter of a company that is being liquidated or reorganized is submitted, then 51 should be indicated.

- Other marks.

The title page should indicate the number of pages on which the declaration is drawn up. Also indicate whether the report was submitted by the taxpayer himself (tax agent) or his authorized representative. It is imperative to decipher the full name and position of the responsible person who signed the declaration.

For an example of filling out a zero VAT return, see ConsultantPlus, having received a free trial demo access to the system:

The information in the field “To be completed by a tax authority employee” is entered into the title page by tax officials.

Responsibility for failure to submit a declaration

If a declaration (including a zero declaration) is not submitted within the prescribed period, a fine of 1,000 rubles is imposed on the legal entity or individual entrepreneur. (clause 1 of article 119 of the Tax Code of the Russian Federation). Since 2015, a VAT return submitted on paper is also considered not submitted (clause 5 of Article 174 of the Tax Code of the Russian Federation).

In addition, administrative penalties will be imposed on officials (fines ranging from 300–500 rubles). If the reporting is delayed by more than 10 working days, the Federal Tax Service will be able to exercise its right to block the organization’s current accounts (subclause 1, clause 3, article 76 of the Tax Code of the Russian Federation).

Read more about this responsibility here.

Features of filling out a zero VAT declaration

Order of the Federal Tax Service of Russia No. ММВ-7-3/ [email protected] in addition to the declaration form also contains the procedure for filling it out. This procedure provides that the title page and section 1 of the report, reflecting the results of tax assessment (clause 3 of Appendix No. 2), are mandatory for submission to the tax authority. The remaining sections, if there is no data to be included in them, are not filled out in the declaration.

That is, VAT reporting with zero indicators will consist of only two sheets. The individual entrepreneur will include information about himself in them, taking into account the features inherent in this information in comparison with similar data reflected by the legal entity:

- will provide a TIN consisting of 12 digits (not 10, like a legal entity);

- in the fields intended for checkpoints (this IP code is not assigned), will put dashes (clause 16.3 of Appendix No. 2 to the order of the Federal Tax Service of Russia No. MMV-7-3 / [email protected] );

- The taxpayer will indicate his last name, first name, and patronymic as the name of the taxpayer.

Other data on the title page should be shown in the usual order for the declaration, without any exceptions depending on who applies it:

- adjustment number (there will be dashes here in the original declaration);

- tax period code and the year to which this period relates;

- codes of the tax authority and place of registration;

- activity code (OKVED);

- telephone number for contact;

- number of sheets (two);

- information about the person who signed the declaration.

The data on the reorganization has nothing to do with the individual entrepreneur, and he will enter dashes in the appropriate fields. The same should be done in the fields provided to indicate the number of documents attached to the report.

In section 2, in addition to the TIN, it is necessary to indicate the codes OKTMO (indicating a certain territorial affiliation of the taxpayer) and KBK (for regular tax it corresponds to the value 18210301000011000110), and in all other lines dashes should be entered.

For an example of filling out a zero VAT return, see ConsultantPlus. Trial access to the system can be obtained for free.

Individual entrepreneur on OSNO: what rules apply to him regarding VAT

An individual entrepreneur using OSNO (and this obligation appears immediately at the time of tax registration, if he does not declare the choice of a different taxation system), just like organizations operating under this regime, must charge and pay VAT and report on this tax .

Only persons who have a small (up to 2 million rubles without VAT) sales volume (not related to the sale of goods subject to excise taxes) for the 3 months preceding the expression of a desire not to pay tax (clauses 1, 2 of Article 145) can be exempted from such obligations Tax Code of the Russian Federation). VAT reporting is generated and submitted to the tax authority quarterly (clause 5 of Article 174 of the Tax Code of the Russian Federation), covering each past quarter as a reporting period (Article 163 of the Tax Code of the Russian Federation). Failure to submit it in case of non-operation or other reasons for the lack of data to fill out is not provided for by law. That is, the taxpayer must submit mandatory VAT reporting (declaration) in any case, regardless of whether he had VAT-related transactions during the tax period or not.

Please note that in addition to the main VAT declaration, there is another one generated in relation to the tax arising when importing goods from the EAEU countries (form KND 1151088). It must be submitted only if the relevant operations are carried out during the period (clause 20 of Section III of Appendix No. 18 to the Treaty on the Eurasian Economic Union, signed on May 29, 2014).

The taxpayer sends the report created for the period to the Federal Tax Service exclusively in electronic form. Other options of the Tax Code of the Russian Federation are not only not provided for, but also lead to the assessment of reporting as not filed (clause 5 of Article 174), and this is a fine. The paper version of submitting the report is acceptable only for tax evaders who generate it only periodically due to the necessity provided for by law (fulfilling the duties of a tax agent, paying VAT when importing goods into the territory of the Russian Federation, issuing an invoice with the allocation of the tax amount).

Is it necessary to file a “zero” VAT return in the absence of taxable objects, ConsultantPlus experts explained. Get free demo access to K+ and go to the Ready Solution to find out all the details of this procedure.

Deadlines for submitting zero VAT reporting

When choosing to use one or another form for generating zero VAT reporting, you must keep in mind that the filing deadlines for them are different, although they fall in the same month (coming after the end of the reporting quarter):

- a regular declaration should be submitted no later than the 25th of this month (clause 5 of Article 174 of the Tax Code of the Russian Federation);

- a single declaration is submitted no later than the 20th day of the same month (clause 2 of article 80 of the Tax Code of the Russian Federation).

That is, with approximately the same level of complexity for filling out, drawing up a zero VAT report in the form of a single declaration gives an advantage in choosing the form for submitting this reporting (on paper or electronically), but limits the taxpayer in the deadline for its submission. Moreover, in fact, the gap in the number of days between the specified deadlines can (due to the application of the rule established by clause 7 of Article 6.1 of the Tax Code of the Russian Federation on the postponement of deadlines coinciding with weekends) both decrease and increase.

Tax period for VAT

The tax period for paying VAT is a quarter (Article 163 of the Tax Code of the Russian Federation). The declaration must be submitted to the tax authorities within the following deadlines:

| Quarter | Deadline for submitting the declaration |

| 1st quarter | Until April 25 |

| 2nd quarter | Until July 25 |

| 3rd quarter | Until October 25 |

| 4th quarter | Until January 25 |

Payment of VAT is made in equal installments until the 25th day of each month of the next quarter (Article 174 of the Tax Code of the Russian Federation):

| Quarter | VAT payment deadlines |

| 1st quarter | Until April 25, until May 25, until June 25 |

| 2nd quarter | Until July 25, until August 25, until September 25 |

| 3rd quarter | Until October 25, until November 25, until December 25 |

| 4th quarter | Until January 25, until February 25, until March 25 |

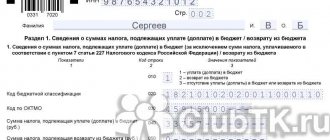

Example 1. Sample of filling out the VAT zero for individual entrepreneurs (title and section 1)

As an example of filling out the “zero”, conditional data is taken. Below is a sample of filling out the key data on the title page and the first section. So, entrepreneur Leonid Semenovich Petrov submits the initial zero declaration for 2022.

On the title page he indicates: adjustment number (“0”), INN (“7721089350”), tax period “21” (1st quarter), reporting year “2022”, as well as the necessary codes - Federal Tax Service (“7722”), according to location (“214”), according to OKVED (“62.02.9”). Next, the individual entrepreneur writes down his contact telephone number, the number of pages (“2”), indicates himself as a taxpayer (“1”), and affixes the date and personal signature. Write dashes in the remaining fields.

When filling out the first section, Petrov L.S. registers the same INN, as well as the OK code) established by the KBK “18210301000011000110”. The remaining fields have dashes. Accordingly, at the end of the page he must put the required date and signature.

Results

Application of OSNO for individual entrepreneurs who, due to low sales turnover, did not take advantage of the exemption from taxpayer obligations under Art. 145 of the Tax Code of the Russian Federation entails the need to calculate and pay VAT, as well as submit reports on this tax. Moreover, the obligation to submit such reports is not canceled in the absence of data for calculating tax. That is, even if there is no activity, a VAT return must be submitted.

If you have zero data to fill out, you can generate reports on one of two forms:

- ordinary, of which in this case only two sheets will be used (the title sheet and the one corresponding to section 1);

- a single simplified one, intended for entering information about mandatory reports, for which the reporting person does not have the data to fill out in the absence of activity.

The use of a single simplified form makes it possible to submit a VAT report not only in the mandatory electronic form, but also in paper form, but limits the taxpayer in the deadline for its submission, shifting it to the 20th (instead of the 25th) day of the month following the reporting quarter.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Zero profit declaration

For this case, the customer will need an identical set of documents as for the previous declaration (name of the business entity, INN, KPP, OKATO, main OKVED code, full name of the manager, name of the reporting period), with the addition of the taxpayer attribute code. The Federal Tax Service Inspectorate accepts the report, both on all nineteen sheets and on five sheets in a short version (title page, subsection 1.1 of section 1, as well as sheet 02 and appendices 1 and 2). The deadline for submitting a declaration for the 1st quarter, half a year, 9 months is set until the 28th day of the month following the reporting one, and the annual report is submitted until March 28th of the year following the reporting one.

| Preparation of zero reporting | |

| Preparation of reports | 2,000 rub. |

| Delivery by mail (one instance) | 600 rub. |

| Delivery by courier (one instance) | 800 rub. |

How will the VAT report be reflected in the single simplified tax return?

In a single simplified tax return, an entrepreneur will have to fill out only one sheet (the first, since the second is intended for individuals who are not individual entrepreneurs). It, as in a regular VAT report, will necessarily show:

- INN IP, his full name and contact phone number;

- the year to which the report relates;

- name and code of the tax authority;

- OKTMO codes (it should be reflected in the field intended for OKATO) and OKVED;

- number of completed pages (one);

- zeros (they act as dashes in this declaration) in the fields intended to indicate the number of documents attached to the report.

The differences will boil down to the following:

- You will need to enter data about the type of document (primary or corrective). In the case of an initial zero declaration, the number 1 will be reflected here.

- Information about the tax will appear in the main table of the report and will be indicated by entering its full name (value added tax) and the number of the chapter of the Tax Code of the Russian Federation regulating the application of this tax (for VAT this is 21). Here you should also make a note that the tax period for the tax is a quarter (this is equivalent to putting the number 3 in the corresponding field) and indicate the number of this quarter (01, 02, 03 or 04).

Thus, the same information will be included in a single declaration as in a regular VAT report compiled on the basis of zero data, but they will have a slightly different appearance.

For a sample of filling out a single simplified declaration, see ConsultantPlus by obtaining free trial access to the system.