Who will need the letter and when?

Current legislation provides for several options for taxation systems for the taxpayer to choose from, depending on various factors: type of activity, level of income, status of the organization or individual entrepreneur, number of employees.

Information about the system used is required by the business partners of the business entity. The fundamental question is whether the counterparty applies VAT or not, since the ability of the other party to the contract, working with value added tax, to present a tax deduction depends on this.

When concluding a contract, pay attention to the price. The clause in the agreement where the cost of the goods is established usually includes the indication “including VAT” or “VAT is not charged”. In the second case, the counterparty most likely applies a special tax regime that does not provide for this tax.

ConsultantPlus experts discussed how to submit a message about the loss of the right to use the simplified tax system. Use these instructions for free.

How to report the use of preferential treatment

Business entities using the simplified tax system are exempt from VAT, with the exception of a few cases (clause 2 of article 346.11 of the Tax Code of the Russian Federation). To confirm status under the simplified tax system, the taxpayer has the right to receive, upon request, from the tax office an information letter in form No. 26.2-7 or provide the counterparty with a notification from the Federal Tax Service about the transition to the simplified tax system (form no. 26.2-1).

Sample

The forms of documents for applying the simplified tax system are approved by order of the Federal Tax Service of Russia dated November 2, 2012 No. ММВ-7-3/, a sample letter about the simplified taxation system coming from the Federal Tax Service looks like this:

Sample of filling out a notice of transition to the simplified tax system in electronic form

An organization wishing to switch to the simplified tax system from January 1, 2022 is required to submit a notification to the tax authority within the period from October 1 to December 31, 2022. Let's consider how to fill out a notice of transition to the simplified tax system electronically using EDeclaration.

Situation (conditionally)

Akatsiya LLC was registered in 2022, UNP 100123868, located at the address: Minsk, lane. Promyshlenny, 289B, is registered with the Tax Inspectorate for the Zavodsky district of Minsk. The organization carries out wholesale trade in non-food products and from the date of state registration applies the general taxation system. From January 1, 2022, she expressed a desire to switch to the simplified tax system.

Indicators for determining the value of the criteria established for the transition to the simplified tax system (paragraph 8, paragraph 5, article 326, article 328 of the Tax Code):

| Month 2021 | Average number of employees, people. | Gross revenue, rub. |

| January | 12 | 14 380,85 |

| February | 13 | 9 821,00 |

| March | 13 | 15 638,68 |

| April | 14 | 12 856,35 |

| May | 14 | 13 258,20 |

| June | 14 | 8 361,15 |

| July | 14 | 7 652,14 |

| August | 15 | 7 962,00 |

| September | 15 | 15 234,78 |

| Average number for 9 months of 2022, people. | 14 | X |

| Gross revenue for 9 months, rub. | X | 105 165,15 |

Note Instructions for installing, configuring and updating the software and components of the Payer's Workstation, the Payer's Workstation User Guide (hereinafter referred to as the User Guide) can be downloaded on the website of the Ministry of Taxes and Taxes: - “Declaration of legal entities and individual entrepreneurs” - “Payer’s Workstation - documentation "

Explanations for filling

In the electronic declaration system "Payer's Workplace" (EDeclaration), click the "Application" tab - "Create an application" and select the "Notification of transition to a simplified taxation system" form.

In the window that opens, general information about the organization is automatically filled in, which was entered and saved through the “Parameters” - “Payer Data” tab: UNP, IMNS, name and address of the organization, information about the manager, etc.

After clicking the “Finish” button, the notification form about the transition to the simplified tax system opens, corresponding to Appendix 36 to Resolution No. 2.

In the line “(name (last name, first name, patronymic (if any)) of the payer)” we write down the name of the organization: Akatsiya LLC.”

Next, we indicate the date from which the organization applies to apply the simplified tax system: in the cell we enter the date “01/01/2022” or put a tick in the line “Transition to the simplified tax system from the next calendar year.”

Next, we provide information about the number of employees of Akatsiya LLC. The line “The number of employees on the payroll is” in the situation under consideration is closed for filling out, because it is intended to indicate information about the number of organizations applying for the application of the simplified tax system from the date of state registration. In our case, it is not filled.

In the line “Number of employees on average for the first nine months of the year”, click “Select year” and “OK”, “2021” is automatically entered.

In the tabular section, we manually enter the value of the average number of employees for January - September 2022.

The average number of employees for 9 months is determined by summing the average number of employees for all months from January to September and dividing the resulting amount by 9. The result is rounded to a whole number according to the rules of arithmetic. The calculation of the number is carried out for the organization as a whole, including branches and other separate divisions (paragraphs 2 and 7 of paragraph 5 of Article 326 of the Tax Code, part 2 of paragraph 99 of Instruction No. 2).

In the program, this indicator is calculated automatically based on the entered data and is equal to 14 people.

Note You can determine the number of employees of an organization on average for the period from the beginning of the year to the reporting period inclusive for the purposes of the simplified tax system using a calculator.

After this, we indicate information about gross revenue on an accrual basis for January - September 2022. To determine the criterion, it is calculated based on the procedure established by Art. 328 Tax Code (as amended in 2022), regardless of the fact that the organization applies the general taxation system in 2022 (paragraph 8, paragraph 5, Article 326 of the Tax Code).

In our case, gross revenue for January - September 2022 amounted to 105,165.15 rubles. In the program, we enter this value manually with an accuracy of two decimal places.

Note According to the current version of the Tax Code, organizations that have the right to switch to the use of the simplified tax system (Part 1, Clause 2, Article 327 of the Tax Code): - gross revenue for the first 9 months of 2022 is no more than 1,623,479 rubles; - number of employees of the organization on average for this period - no more than 100 people. At the same time, the draft Tax Code for 2022, published on the website of the Ministry of Finance, plans to reduce these values and establish a ban on the use of the simplified tax system in 2022 by organizations that: - gross revenue on an accrual basis for the first 9 months of 2022 exceeded RUB 1,612,500.00;—the number of employees on average during this period amounted to more than 50 people. (Clause 11, Article 2 of the draft Law on Amendments to the Laws of the Republic of Belarus).

The created notification must be saved. To do this, you can click on the icon in the upper left part of the screen, or on the Ctrl+S keys, or close the notification and click on the save button after the corresponding program proposal (subsection 8.1 of the User Guide).

Before sending a notification about the transition to the simplified tax system, you must sign an electronic signature. To do this, click the “Window” - “Statements” tab. A list of created documents will open, from which, by clicking the mouse, select the notification about the transition to the simplified tax system, the “Sign” button will be activated.

After signing, the notification receives the “Ready” status and can be sent to the Ministry of Taxation, the “Send” button is activated. Upon successful sending, the document status changes to “Sent”. You can check whether the document has been accepted by the tax authority using the “Window” element - “Responses from the Ministry of Taxes” (subclauses 8.5, 8.6 and 8.10 of the User Guide).

Note An organization, after submitting a notice of transition to the simplified tax system, has the right to refuse to apply it as a whole for 2022. To do this, it must submit a notice of refusal to apply the simplified tax system no later than 02/21/2022 (02/20/2022 - Sunday) (paragraph 2, clause 5 Article 327, Article 4 Tax Code).

The created notification in the Payer's Workstation can be saved to computer media in PDF or xml format, and also printed (subclauses 8.7 and 8.8 of the User Guide).

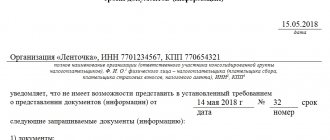

For a sample notification of the transition to the simplified tax system, see the PDF file

Read this material in ilex >>* * following the link you will be taken to the paid content of the ilex service

How to write a letter on the application of the general tax system

There are no approved forms of documents for applying the general taxation system. In this case, you will need to compose the letter yourself. There are no special rules for such letters; follow the general recommendations for business correspondence:

- prepare a letterhead with details;

- indicate all the necessary details of the counterparty to whom the letter is addressed;

- in the text indicate the date of registration of the organization or individual entrepreneur, the applied tax regime and the time from which it applies;

- put the date and signature of the authorized person;

- If necessary, attach supporting documents, for example, a copy of the VAT return with a note indicating its acceptance by the tax authority.

Sample

| Limited Liability Company "Clubtk.ru" OGRN/ OKPO 1234567891011/ 12345678 INN/KPP 1213141516/111111111 123456, St. Petersburg, Pravdy street, building 1 tel/fax (812) 7121212, e-mail: | Voronov Andrey Viktorovich |

How to notify that you are paying VAT

All requirements for a letter to a business partner stating that you are a value added tax payer are the same as for a letter under OSNO. There is no form established by law.

If the other party to the agreement wishes to receive confirmation of information from the tax office, then you have the right, in the usual manner established by the Federal Law “On Citizens' Appeals” No. 59-FZ, to send a free-form request to the tax office with a request to provide data on the applied regime and calculated taxes. The response period for an appeal will be 30 days by law.

UTII form-2 for individual entrepreneurs in 2022, waiver of the UTII regime

For an individual entrepreneur, the same rules for switching to the UTII regime apply as for legal entities. Forms UTII-1 and UTII-2 differ from each other only in the title page, everything else is the same. The main difference is in filling out the title page: instead of the name of the organization, fill in your full name. individual entrepreneur, and instead of the OGRN, the OGRNIP (main state registration number of the individual entrepreneur) is indicated.

A sample of UTII-2 is shown in the figure below.

Refusal from the UTII regime by a legal entity and individual entrepreneur occurs after submitting a special application within five days - from the moment of transition to another regime, from the day of deregistration with the Federal Tax Service as a “imputed”, from the last day of the month of the quarter in which it was the condition for the lawful use of UTII was violated (before 04/05/2017, before 07/05/2017, before 10/05/2017, before 01/05/2022, etc.).

According to paragraph 7 of the information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation No. 157 dated March 5, 2013, suspension of sales of goods and provision of services without the process of deregistration with the tax inspectorate does not exempt taxpayers from taxation of UTII.

Conclusion: the deadlines for filing an application for registration as a UTII payer and deregistration in fact coincide - either from the date of transition to a new regime, or from the day of complete cessation of business activity.

Important point: To switch to the UTII regime, an individual entrepreneur or legal entity must be engaged in certain types of activities and meet the profitability limit on the number of employees. The transition to the UTII regime occurs after submitting the appropriate application.