Find out on our website about such procedures as: transfer of a house by the developer to a management organization, holding a competition to select the best management company, creating your own management organization, obtaining a license and registration on the GIS Housing and Communal Services, as well as concluding service agreements with the owners. You can also learn about the procedures for terminating an agreement with a management company and bankruptcy of an organization from our articles.

Maintaining accounting records in a housing and communal services management company

Typically, the standard activity of a management company is that the organization purchases resources from relevant companies and then provides them to residents.

Based on this, it turns out that the acquisition of resources provokes the appearance of accounts payable and certain expenses .

Whereas the provision of resources forms receivables and income generation.

Therefore, accounting in a housing and communal services management company must necessarily consist of several stages:

- Determination of accounting policies . These are certain rules that establish all the nuances that allow you to take into account all the assets, as well as the income and expenses of the organization. The more carefully the specialists write down all the issues related to accounting, the easier it will be to maintain accounting records.

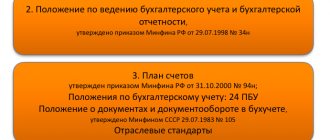

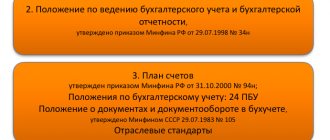

- Working chart of accounts . Its preparation is the basis of accounting, which is carried out on the basis of Order No. 94n of the Ministry of Finance. Experts advise including in the plan only those accounts that the management company will actually use in its activities.

- Approve the forms of primary documentation . The management company has several options for using primary documents. You can use standardized forms, or you can approve your own. In any case, they must be fixed in the accounting policies of the management company.

- Accounting . This is what specialists do. In practice, accounting in a management company is carried out in the same way as in most other organizations.

- Making report . A balance sheet, financial report and other documents are required. A complete list of reporting documents is contained in Federal Law No. 402.

The working chart of accounts, scientific policy, forms of primary accounting documentation must be issued in one order.

It is signed by two people - the head of the management company and the chief accountant. It is advisable to change this document annually in accordance with current legislation.

You can learn about accounting in a management company from the video:

Transition to accounting

Find out from our articles about what management of apartment management by a management company is, as well as the advantages and disadvantages of management company over other forms of management.

Solution for optimizing accounting calculations for housing and communal services

The 1C program for calculating rent and housing and communal services accounting in the cloud is a special industry solution developed for the tasks of companies in this industry. In it you can:

- maintain databases of residential and non-residential facilities with complete characteristics,

- maintain tenant databases indicating personal information, payments and debts,

- calculate fees based on instrument readings, taking into account different tariffs,

- generate, distribute and print payment receipts for owners,

- send notifications by email and SMS to residents,

- exchange data with GIS housing and communal services,

- accept requests from residents and set tasks for emergency repair services,

- order services from contractors and pay them,

- maintain work schedules for housing and communal services employees and calculate salaries,

- maintain accounting and tax records with automatic generation of reports.

The cloud format involves storing information and program functionality on a server in a remote data center. This means that the organization is not tied to a specific computer in the office - employees with access rights log into it online and make changes from anywhere and at any time. This is convenient for collaboration, since management, operators, accountants, and field teams in housing and communal services organizations are often geographically separated.

Responsibilities of the chief accountant

Bookkeeping is the main responsibility of an accountant working in an organization.

But besides this, there are a number of other powers that a specialist has:

- organization of accounting;

- formation of the company’s accounting policy based on the specifics of its core activities;

- preparation and approval of work plans, document forms, etc.;

- organization of internal control over the execution of business transactions;

- formation of accounting information systems;

- providing the necessary data to external and internal users;

- ensuring timely transfer of taxes to the budget;

- payment of insurance premiums;

- implementation of financial analysis and tax policy;

- control over cash and financial discipline;

- registration of documents in connection with shortages or illegal spending of funds of owners.

This is a short list of responsibilities that the chief accountant in a management company must perform. Based on this, we can conclude that they are no different from the responsibilities of such specialists in other organizations.

Basic postings

basic entries in their accounting

- D19 K60;

- D60 K51;

- D20 K60;

- D68 K19.

In the field of provision of housing and communal services:

- D 90/2 K20;

- D60 K62;

- D62 K90/1;

- D90/3 K68;

- D51 K62.

These postings are used when the management company uses OSNO or simplified tax system.

But there are differences, since when using “simplified” some of the above entries are not used by accountants. For example, under the simplified tax system there are tax benefits for paying VAT.

Criminal Code on the simplified tax system: accounting for payments from the population

One of the most important issues that concern accountants of management companies and homeowners associations is accounting for incoming utility bills. However, sometimes payments bypass their checking account and cash register. It would seem that the cash method is no money – no income. But what really?

Among other methods of settlements between the owners of premises in an apartment building and resource supply organizations, the method of direct settlements stands out. That is, the owners pay for utilities directly to the RSO, thereby bypassing the current account of the management company. This right is given to the owners of premises in clause 7.1 of Art. 155 of the Housing Code of the Russian Federation, which states that based on the decision of the general meeting of owners of premises in an apartment building, they can pay for all or some utilities directly to resource supply organizations.

Please note: you cannot directly pay for utilities consumed when using common property in an apartment building. Payments for utility services for general house needs are paid exclusively to the provider of utility services, that is, the management company.

IMPORTANT IN WORK

Owners of premises in an apartment building can choose such a method of managing an apartment building as its management by a management organization.

Let us recall that based on paragraphs. 2, 31 of the Decree of the Government of the Russian Federation dated May 6, 2011 No. 354 “On the provision of utility services to owners and users of premises in apartment buildings and residential buildings” (hereinafter referred to as the Rules), the management company acts for consumers as a provider of utility services and is responsible to them for the provision of utility services services of appropriate quality. At the same time, based on clause 64 of the Rules, consumers must specify the date from which direct settlements with the RSO will be made, since the management company must notify the RSO of the decision made no later than 5 business days from the date of such a decision. But even when consumers choose the option of direct settlements with RSO, the obligation to calculate fees for utility services and issue payment documents to consumers on the basis of which payment is made (clause 2 of article 155 of the RF Housing Code) remains with the management company (clause 31 of the Rules). At the same time, on the basis of clause 27 of the Decree of the Government of the Russian Federation dated February 14, 2012 No. 124 “On the rules mandatory when concluding agreements for the supply of utility resources for the purposes of providing utility services” (hereinafter referred to as the Rules for concluding a resource supply agreement), the agreement must provide for the procedure, terms and a form for the RSO to submit information to the management company about the amount of payment received from consumers for utility services and the debt of the contractor to pay for a utility resource separately for consumer payments and payments for utility services of the corresponding type consumed when using common property in an apartment building. It also follows from this paragraph that the RSO has the right to demand that the contractor suspend or limit the provision of utility services to the owner of the premises who is in arrears in payment (if it is technically possible to fulfill these requirements). If the performer does not do this, he will bear responsibility, including in the form of compensation to RSO for losses. From the above it is clear that information exchange with the RSO plays an important role, since the management company needs to receive timely and reliable information about payments from property owners.

GOOD TO KNOW

Since September 1, 2014, HOAs have been classified as partnerships of real estate owners (Articles 123.12–123.13 of the Civil Code of the Russian Federation).

Include in expenses?

In letter dated 04/07/2014 No. 03-11-06/2/15441, the Russian Ministry of Finance gave the following explanations: “... in accordance with clause 1 of Art. 346.15 of the Tax Code of the Russian Federation, according to which, when determining the object of taxation, sales income determined for the purposes of applying Ch. 25 of the Tax Code of the Russian Federation, in accordance with Art. 249 of the Tax Code of the Russian Federation, which states that income from sales is the proceeds from the sale of goods (works, services) both of one’s own production and those previously purchased. Sales refers to the transfer on a paid (and sometimes gratuitous) basis of goods and results of work by one person to another person, as well as the provision of services for a fee by one person to another person. Revenue is determined based on all receipts associated with payments for goods sold (work, services) or property rights, expressed in cash or in kind...” Further, the Ministry of Finance reminds that for the purpose of applying the simplified tax system, the date of receipt of income is the day of receipt of funds in bank accounts or at the cash desk, receipt of other property (work, services) or property rights, as well as repayment of debt (payment) to the taxpayer in another way (cash method ).

In our case, when using the option of direct payments for utilities, the management company has no receipts at all to the current account for the utilities provided to the owners of the premises. In this regard, the Ministry of Finance makes a completely logical conclusion that if, based on contractual relations, the owners of premises in an apartment building directly pay for utility services to the RSO and the payment for utilities does not go to the account of the management company, these funds are not taken into account as part of its income when determining the tax base for the tax paid in connection with the application of the simplified tax system.

IMPORTANT IN WORK

If the management organization applies the simplified tax system with the object of taxation “income minus expenses”, payments for utility services, simultaneously with their reflection in the income side of such an organization, are accepted for deduction as expenses, since they are transferred to the relevant organizations providing these services.

Example 1.

Based on the decision of the general meeting of owners of the premises of an apartment building, from October 1, 2014, electricity payments are paid directly to the RSO. In October 2014, the payment for electricity according to the readings of the common house meter amounted to 350,000 rubles (including VAT (18%) - 53,390 rubles). The management company using the simplified tax system charged the owners of the premises a fee for a utility resource in the amount of:

- 300,000 rub. – individual consumption in the premises of the owners;

- 50,000 rub. – consumption for general household needs.

POSITION OF THE MINISTRY OF FINANCE

The amounts of payments by homeowners for housing and communal services received by the organization must be taken into account as part of its income when determining the tax base for the tax paid in connection with the application of the simplified tax system.

— Letter dated July 10, 2013 No. 03-11-06/2/26817.

In November 2014, RSO received payment from the owners for electricity in the amount of 250,000 rubles. (for October 2014). The management company received payment for electricity for general house needs for October 2014 in the amount of 35,000 rubles.

The following entries will be made in the accounting records of the management company:

| Contents of operation | Debit | Credit | Amount, (rub.) | |

| October 2014 | ||||

| The cost of utilities has been taken into account | 20 | 60 | 350 000 | |

| Sales of utilities reflected | 62 | 90-1 | 350 000 | |

| The cost of utilities has been formed | 90-2 | 20 | 350 000 | |

| November 2014 | ||||

| Payment was received from the owners of the premises for utilities (electricity for general house needs for October 2014) | 51 | 62 | 35 000 | |

| Funds transferred to RSO | 60 | 51 | 35 000 | |

| Based on RSO data (information exchange), the repayment of receivables of premises owners for electricity and the repayment of accounts payable to RSO for the supplied utility resource in October 2014 are reflected. | 60 | 62 | 285 000 | |

Please note: based on clause 7.1 of Art. 155 of the Housing Code of the Russian Federation, payment by the owners of premises for utility services to the RSO means that their obligations to pay for utility services to the management company have been fulfilled. That is, the owners of the premises, by transferring the payment to the RSO, automatically repay their debt by paying it to the management company. At the same time, the management company, receiving information that the corresponding payment has been received by the RSO, considers its debt to it to be repaid. Hence the formation of the posting Debit 60 Credit 62 .

From the above and within the given example, it follows that the management company, when forming the tax base for the single tax, will include in income only the payment for consumed electricity for general house needs in the amount of 35,000 rubles. If the management company applies the simplified tax system with the object “income reduced by the amount of expenses,” then the expenses will amount to 35,000 rubles. Consequently, the tax base of the management company will be zero.

IMPORTANT IN WORK

If the business activity of the management organization, based on contractual obligations, is an intermediary activity on behalf of the owners of premises in an apartment building for the purchase of utilities, then the income of this organization will be a commission, agency or other similar remuneration.

Income from intermediary services

In addition to direct settlements with RSO, the management company can also act under intermediary agreements. According to Part 2 of Art. 162 of the Housing Code of the Russian Federation, under an agreement for the management of an apartment building, the management organization, on the instructions of the other party (the owners of the premises in the apartment building), undertakes, for a fee, to provide services and perform work on the maintenance and repair of common property in such a building, as well as to provide utilities, for a fee within an agreed period. In this regard, the entrepreneurial activities of the management company can be carried out within the framework of concluding an intermediary agreement. One such agreement may be an agency agreement. Numerous letters from the Ministry of Finance of Russia (see, for example, letters dated January 27, 2014 No. 03-11-06/2/2828, dated July 10, 2013 No. 03-11-06/2/26817, dated December 12, 2012 No. 03-11- 06/2/146) explain how to correctly determine the income of a management company for tax purposes in connection with the application of the simplified tax system if its business activity, based on contractual obligations, is an intermediary activity. Thus, the tax base does not reflect the income specified in Art. 251 of the Tax Code of the Russian Federation, in particular, income in the form of property (including cash) received by the agent in connection with the fulfillment of obligations under the agency agreement, as well as for reimbursement of expenses incurred by the agent, is not taken into account. Moreover, reimbursable costs are not reflected for tax purposes only if, under the terms of the contract, these costs are not included by the agent as expenses in tax accounting. Consequently, if the management company entered into such agency agreements with the owners of premises in an apartment building even before it began to make transactions with companies directly providing utility services, then, indeed, only agency fees can be taken into account as part of its income.

GOOD TO KNOW

The income of an organization that applies the simplified tax system and is an agent under an agency agreement is recognized as the amount of the agency fee received.

Please note: this approach applies to all taxpayers using the simplified tax system, regardless of the selected object.

What is an accounting policy?

Fragment of the accounting policy for a housing and communal services management company - example:

Accounting policy of a housing and communal services management company – sample.

The accounting policy of the management company is regulated by the Tax Code (Article 313) and Accounting Regulation 1/2008. The developer of accounting policies is most often the chief accountant or another authorized person.

There are the following features:

- the developed accounting policy is applied from period to period;

- the activities of the management company are subject to the norms of tax and accounting legislation;

- if the legislation does not contain the necessary nuances, all instructions or methods are developed by the management company independently;

- The accounting policy must necessarily reflect which taxation system the management company applies.

The organization's accounting policy must necessarily contain accounting for materials, settlements with resource supply companies, as well as income, expenses, tax payments, and wages.

These are the basic rules that accountants use to keep records. It determines how easy it will be for specialists to carry out their work in the future.

Taxation

Management companies can choose a taxation method from the simplified tax system or OSNO.

In both cases, taxation of management companies in the housing and communal services sector is based on two types of taxes:

- for added value;

- at a profit.

Most companies use OSNO, but it has one significant drawback.

It consists in a fairly high income tax , which is 20%. In addition, VAT must be paid.

This is too large a tax deduction for a management company. But management companies in this situation have an advantage, since the services they provide are not subject to VAT (Article 149 of the Tax Code of the Russian Federation).

On the other hand, such an exemption from VAT does not change anything significant in the organization’s position. The fact is that utilities are paid at a single price , so it is very difficult for management companies to earn something from this.

If we turn to judicial practice, it turns out that only income from repairs should not be subject to VAT. The amount must be equal to the expenses incurred by the management company .

But the simplified tax system is used by small organizations whose income does not exceed 60 million rubles. Other conditions include the number of full-time employees (no more than 100).

These systems are much more convenient for management companies, which is why many of them are switching to the simplified tax system. To do this, you need to draw up an appropriate application and submit it to the tax authorities.

Difficulties in accounting and accounting of housing and communal services

- Residents carefully monitor compliance with the estimates established at meetings. The estimates must exactly match the company's expenses. But in reality, unexpected expenses often arise that need to be agreed upon and correctly reflected in the accounting accounts.

- Difficulties often arise in accounting for utility bills. They may relate to target receipts or transit payments, that is, they are posted to different accounts. Incorrect entries cause discrepancies in reporting. Errors are also typical in relation to penalty calculations.

- Organizations in the housing and communal services sector must generate two types of reports - on income-expenses and cash flows, which reflect the receipt and use of funds, as well as debts. The need to submit double reporting also often leads to complications.

These factors are the cause of common accounting errors. In addition, accounting is complicated by the fact that you have to manage a large database of real estate, calculate a large number of payments at various rates, and pay salaries to employees.

Postings under the simplified tax system

If the company uses a simplified system, then there will be no postings D68 K19 and D90/3 K68 (these are postings for the deduction and calculation of VAT ). This rule applies if, under OSNO, the management company has VAT benefits.

The main advantage of accounting in a management company using the simplified tax system is that organizations do not pay VAT and income tax . Instead, they pay a separate fee to use the simplified system. Its size depends on the subject of taxation and is 5% or 15%.

When using OSNO UK, it also has VAT benefits. For example, an organization is exempt from payment when providing utilities, carrying out work on the maintenance and repair of apartment buildings with the involvement of relevant organizations.

Postings used by the management company under the simplified tax system

For organizations that have introduced a simplified taxation system, only three accounts are used:

- Current account No. 51.

- Profit/Loss of enterprise No. 99.

- Tax payments, fees, deductions and calculations No. 68.

There are only two wires:

- Tax accrual No. 99.

- Display of tax payment No. 68.

We talked in more detail about how payments are made in housing and communal services in this article.